|

시장보고서

상품코드

1850239

앰비언트 인텔리전스 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ambient Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

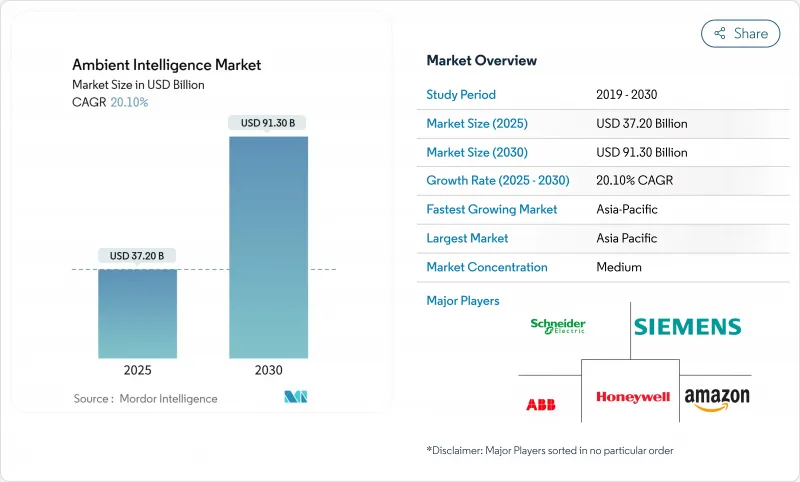

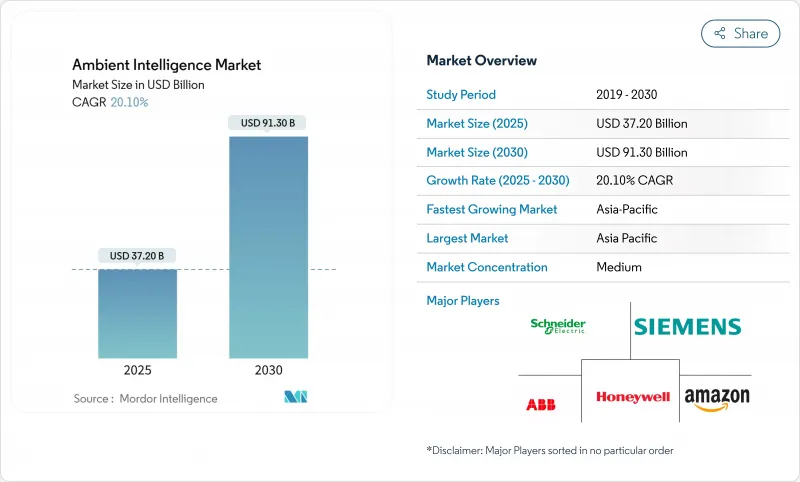

앰비언트 인텔리전스 시장 규모는 2025년에 372억 달러로 추정되고, 2030년에는 913억 달러에 이를 것으로 예측되며, CAGR 20.1%로 성장할 전망입니다.

IoT, 엣지 AI, 초저파워 반도체의 급속한 융합은 대기 시간과 클라우드 의존성을 줄이는 자율적이고 컨텍스트를 의식한 전개가 가능해집니다. 정부의 smart-city 프로그램, 디지털화된 헬스케어 워크플로우, EV 보급 증가가 공공 인프라, 병원, 자동차 전체 수요를 강화하고 있습니다. 공급업체는 배터리리스 센서 설계, 임베디드 AI 가속기, 개방형 개발자 에코시스템으로 차별화를 도모하는 한편 플랫폼 통합의 진전이 진입 장벽을 높이고 있습니다. 아시아태평양은 중국의 약 800개 파일럿 도시, 중동의 대규모 투자, 인도의 미국, 일본, 한국과의 3극 디지털 틀을 배경으로 채용을 선도하고 있습니다.

세계의 앰비언트 인텔리전스 시장 동향 및 인사이트

AI 및 IoT 디바이스의 보급

Nordic Semiconductor의 nRF54 시리즈와 같은 엣지 AI 칩셋은 센서 내부에서 실시간 추론을 수행하여 대기 시간과 대역폭 요구를 줄입니다. 수익과 예측에 따르면 엣지 AI 플랫폼의 수익은 2032년까지 1,400억 달러를 넘을 전망이며, AI 칩은 2025년까지 반도체 수요의 20% 가까이를 차지할 것으로 추정됩니다. 로컬 프로세싱은 프라이버시를 강화하고, 대역폭에 제약이 있는 장소에서의 전개를 가능하게 하며, 클라우드를 호출하지 않고 예측 유지보수, 이상 감지, 적응 조명을 지원합니다.

정부의 스마트시티 구상

중국의 800개 파일럿 프로젝트, 136개 회원 도시가 참여하는 EU의 지능형 시티 챌린지, 마스다르 시티 및 NEOM과 같은 프로젝트에 대한 UAE와 사우디아라비아의 500억 달러의 약속은 장기적인 자금 조달의 확실성을 보여줍니다. 미국, 일본, 한국이 지원하는 인도의 디지털 인프라 성장 이니셔티브는 교통, 에너지 및 안전 플랫폼에 앰비언트 인텔리전스를 통합하는 5G 및 AI 표준을 우선시합니다. 명확한 정책 목표는 조달주기를 단축하고 사양을 표준화하며 민간 투자의 위험을 줄입니다.

데이터 보안 및 개인 정보 보호에 대한 우려

앰비언트 센서는 GDPR(EU 개인정보보호규정) 등 엄격한 법률에 해당하는 행동 데이터, 생체 데이터, 위치 정보를 취득합니다. 빌딩 자동화 시스템은 컨트롤러 층에서 노출된 상태로 남아 있으며, 전체 시설에 대한 침입의 벡터가 열려 있습니다. 헬스케어의 도입은 스트림의 암호화, 온프레미스의 추론, 동의 게이트 분석 워크플로우의 실행이 필요해, 비용이 들고 파일럿이 지연됩니다.

부문 분석

Affective Computing은 2024년 앰비언트 인텔리전스 시장 규모의 27.5%를 차지했으며, 사용자의 감정에 맞게 조명, 사운드, 알림을 적응시키는 감정 인식 워크플레이스, 리테일 존, 병실을 가능하게 합니다. 수요는 기업의 웰니스 프로그램과 원격 의료 트리아지에서 가장 강하며, 목소리 톤과 얼굴 신호가 서비스 제공을 향상시킵니다.

엣지 AI Bluetooth Low Energy 노드는 로컬 추론이 서브밀리와트 무선과 융합하여 자산 추적, 스마트 태그, 마이크로 소매 디스플레이용 주소 가능한 노드를 생성하기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 28%가 됩니다. Minew의 MSA01 환경 광 센서는 초저전력 설계가 지속적인 환경 데이터를 최적화 엔진에 공급하는 방법을 보여줍니다. RFID Alliance 회원은 세계 공급망의 통합 비용을 줄이기 위해 개발자 API를 초안합니다.

스마트 빌딩 관리는 2024년 28%의 판매 점유율을 확보했는데, 이는 예측 공조 제어, 가동률 적응형 조명, 실시간 탄소 대시보드에 의한 명확한 투자 회수를 반영합니다. 건물 소유자는 녹색 임대 조건 및 에너지 성능 계약 준수를 구매의 계기로 언급합니다.

스마트 홈 오토메이션의 CAGR은 27.2%입니다. 음성으로 조작할 수 있는 어시스턴트, 셀프 파워의 창 센서, 통합 보안 허브가 소비자의 기대를 높입니다. Matter 인증 허브는 브랜드 간의 상호 운용성을 약속하고 공급업체의 봉쇄를 줄이고 소매 채널을 확장합니다.

지역 분석

아시아태평양은 여전히 앰비언트 인텔리전스 시장의 중심이며 시장 점유율은 39.8%입니다. 또한 2025-2030년 예측 기간 중 CAGR은 26.21%로, 이 지역이 가장 빠른 속도로 성장할 것으로 예측되고 있습니다. 지역 정부는 중국의 800개 프로젝트와 일본의 탈탄소 항만 계획 등 대규모 테스트 베드에 자금을 제공하여 대량 조달과 국내 칩 생산을 촉진하고 있습니다. 인도의 3극 프레임워크는 5G와 AI 플랫폼의 채용을 가속화하여 스마트 수송 회랑과 마이크로그리드의 파일럿 사업을 지원합니다.

북미에서의 도입은 인프라 투자 및 고용촉진법(Infrastructure Investment and Jobs Act)의 혜택을 받습니다. 3조 7,000억 달러의 자금 부족이 계속되고 있지만, 전력 회사와 도시는 그리드 엣지 분석, 스마트 가로등, 공공 안전 네트워크에 세액 공제를 활용하고 있습니다. 기업은 ESG 공약을 충족하기 위해 사무실을 개조하고 모듈식 센서 키트 수요를 촉진하고 있습니다.

유럽 136개 도시의 지능형 시티 챌린지는 디지털 트윈닝, 시티버스 계획, 실시간 에너지 추적을 의무화하는 로컬 그린딜을 향해 430억 유로를 투입합니다. 공급업체는 EU의 사이버 보안, 접근성 및 순환 지침을 제품 로드맵에 통합하여 지자체 건물에 대한 전개를 가속화하고 있습니다.

중동 및 아프리카에서는 아랍에미리트(UAE)(UAE) 및 사우디아라비아가 마스다르 시티, NEOM, 위성 캠퍼스에 500억 달러를 투자하고 AI 주도 폐기물, 에너지 및 이동성 시스템을 통합함으로써 도입이 진행되고 있습니다. 현지 파트너는 이러한 거대한 프로젝트에 포함된 기술 이전 조항에서 이익을 얻고 있습니다.

라틴아메리카의 도시 콩그로말리트는 범죄 감축과 전력 품질 모니터링에 중점을 두고 5G 고정 무선 회선을 통해 클라우드 대시보드에 공급하는 카메라 분석과 마이크로 PMU를 도입하고 있습니다. 벤더 금융과 다자간 은행 대출은 설비 투자 제약을 완화하고 2030년까지 한 자릿수의 CAGR 성장을 유지합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI 및 IoT 디바이스의 보급

- 정부의 스마트 시티 구상

- 에너지 효율이 높은 스마트 빌딩 수요

- 앰비언트 어시스테드 리빙(헬스케어)의 도입

- 엣지 AI SoC의 비용 저하에 의해 배터리리스 센서 실현

- ESG 주도의 실시간 탄소 추적 수요

- 시장 성장 억제요인

- 데이터 보안 및 개인정보 보호에 대한 우려

- 상호 운용성 표준의 부족

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 제품 수명주기 분석

- 고객 수용 분석

- 비교 분석

- 투자 시나리오

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 하드웨어

- 소프트웨어 및 솔루션

- 기술별

- Bluetooth 저에너지

- RFID

- 센서(주위광)

- 소프트웨어 에이전트

- 감정 컴퓨팅

- 나노 기술

- 생체 인증

- 기타 기술

- 최종 사용자 업계별

- 주택용

- 소매

- 헬스케어

- 산업

- 오피스 빌딩

- 자동차

- 기타 최종 사용자 산업

- 용도별

- 스마트 빌딩 관리

- 앰비언트 어시스테드 리빙

- 스마트 홈 오토메이션

- 스마트 소매 분석

- 스마트 매뉴팩처링 및 산업용 IoT

- 스마트 모빌리티 및 교통

- 공공 안전 및 보안

- 에너지 관리

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- Johnson Controls International plc

- Koninklijke Philips NV

- Amazon.com Inc.

- Google LLC

- Apple Inc.

- Microsoft Corp.

- Samsung Electronics Co. Ltd.

- Bosch GmbH

- Cisco Systems Inc.

- Legrand SA

- Ingersoll-Rand PLC

- Tunstall Healthcare Ltd.

- Caretech AB

- Getemed Medizin-Und Informationstechnik AG

- Televic NV

- Vitaphone GmbH

- Xiaomi Corp.

- Assisted Living Technologies Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.07The ambient intelligence market size is estimated at USD 37.2 billion in 2025 and is forecast to reach USD 91.3 billion by 2030, translating into a 20.1% CAGR.

Rapid convergence of IoT, edge AI and ultra-low-power semiconductors enables autonomous, context-aware deployments that reduce latency and cloud dependence. Government smart-city programs, digitized healthcare workflows and rising EV adoption strengthen demand across public infrastructure, hospitals and vehicles. Suppliers differentiate through battery-less sensor designs, embedded AI accelerators and open developer ecosystems, while increasing platform consolidation raises entry barriers. Asia-Pacific leads adoption on the back of nearly 800 Chinese pilot cities, large-scale Middle East investments and India's trilateral digital framework with the United States, Japan and South Korea.

Global Ambient Intelligence Market Trends and Insights

Proliferation of AI and IoT devices

Edge AI chipsets such as Nordic Semiconductor's nRF54 Series now perform real-time inference inside the sensor, cutting latency and bandwidth needs. Forecasts indicate edge AI platform revenue surpassing USD 140 billion by 2032, with AI chips representing nearly 20% of semiconductor demand by 2025. Local processing bolsters privacy allows deployment in bandwidth-constrained sites and supports predictive maintenance, anomaly detection and adaptive lighting without cloud calls.

Government smart-city initiatives

China's 800 pilot projects, the EU's Intelligent Cities Challenge with 136 member cities and the UAE-Saudi commitment of USD 50 billion to projects such as Masdar City and NEOM signal long-term funding certainty. India's Digital Infrastructure Growth Initiative, backed by the United States, Japan and South Korea, prioritizes 5G and AI standards that embed ambient intelligence into transport, energy and safety platforms. Clear policy targets shorten procurement cycles, standardize specifications and de-risk private investment.

Data security & privacy concerns

Ambient sensors capture behavioural, biometric and location data that fall under stringent laws such as GDPR. Building automation systems remain exposed at the controller layer, opening vectors for facility-wide intrusion. Healthcare deployments must encrypt streams, run on-premisses inference and consent-gate analytics workflows, adding cost and slowing pilots.

Other drivers and restraints analyzed in the detailed report include:

- Demand for energy-efficient smart buildings

- Adoption of ambient-assisted living (healthcare)

- Lack of interoperability standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Affective computing held 27.5% of the ambient intelligence market size in 2024, enabling emotion-aware workplaces, retail zones and patient rooms that adapt lighting, sound and notifications to user sentiment. Demand is strongest in corporate wellbeing programs and telehealth triage where voice tone and facial cues improve service delivery.

Edge-AI Bluetooth Low Energy nodes post a 28% CAGR to 2030 as local inference merges with sub-milliwatt radios, creating addressable nodes for asset tracking, smart tags, and micro-retail displays. Minew's MSA01 ambient light sensor illustrates how ultra-low-power designs feed continuous environmental data into optimization engines. Further down the stack, RFID Alliance members are drafting developer APIs to cut integration costs across global supply chains.

Smart building management secured 28% revenue share in 2024, reflecting clear payback from predictive HVAC control, occupancy-adaptive lighting and real-time carbon dashboards. Building owners cite compliance with green-lease clauses and energy-performance contracts as purchase triggers.

Smart home automation posts a 27.2% CAGR. Voice-activated assistants, self-powered window sensors and integrated security hubs elevate consumer expectations. Matter-certified hubs promise cross-brand interoperability, reducing vendor lock-in and widening retail channels.

The Ambient Intelligence Market is Segmented by Component (Hardware and Software, and Solutions), Technology (Bluetooth Low Energy, RFID, and More), End-User Industry (Residential, Retail, and More), Application (Smart Building Management, Ambient-Assisted Living, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the epicentre of the ambient intelligence market with 39.8% market share. The region is also expected to grow at the fastest rate with a CAGR of 26.21% during the forecast period 2025 to 2030. Regional governments fund large testbeds-China's 800 projects and Japan's decarbonized port plans among them-driving bulk procurement and domestic chip production. India's trilateral framework accelerates 5G and AI platform adoption, anchoring smart transport corridors and micro-grid pilots.

North American uptake benefits from the Infrastructure Investment and Jobs Act. Although a USD 3.7 trillion funding gap persists, utilities and cities leverage tax credits for grid-edge analytics, smart street lighting and public safety networks. Corporations retrofit offices to meet ESG pledges, fuelling demand for modular sensor kits.

Europe's 136-city Intelligent Cities Challenge channels EUR 43 billion toward digital twinning, CitiVerse planning and Local Green Deals that mandate real-time energy tracking. Vendors incorporate EU cybersecurity, accessibility and circularity directives into product roadmaps, quickening rollout in municipal buildings.

The Middle East and Africa region shows rising adoption as the UAE and Saudi Arabia outlay USD 50 billion on Masdar City, NEOM and satellite campuses, integrating AI-driven waste, energy and mobility systems. Local partners gain from technology transfer clauses embedded in these megaprojects.

Latin America's urban conglomerates focus on crime reduction and power-quality monitoring, deploying camera analytics and micro-PMUs that feed cloud dashboards via 5G fixed-wireless links. Vendor financing and multilateral bank loans mitigate capex constraints, sustaining single-digit CAGR growth through 2030.

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- Johnson Controls International plc

- Koninklijke Philips NV

- Amazon.com Inc.

- Google LLC

- Apple Inc.

- Microsoft Corp.

- Samsung Electronics Co. Ltd.

- Bosch GmbH

- Cisco Systems Inc.

- Legrand SA

- Ingersoll-Rand PLC

- Tunstall Healthcare Ltd.

- Caretech AB

- Getemed Medizin-Und Informationstechnik AG

- Televic NV

- Vitaphone GmbH

- Xiaomi Corp.

- Assisted Living Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI and IoT devices

- 4.2.2 Government smart-city initiatives

- 4.2.3 Demand for energy-efficient smart buildings

- 4.2.4 Adoption of ambient-assisted living (healthcare)

- 4.2.5 Edge-AI SoC cost drops enabling battery-less sensors

- 4.2.6 ESG-driven real-time carbon tracking demand

- 4.3 Market Restraints

- 4.3.1 Data security and privacy concerns

- 4.3.2 Lack of interoperability standards

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Product Life-Cycle Analysis

- 4.9 Customer Acceptance Analysis

- 4.10 Comparative Analysis

- 4.11 Investment Scenario

- 4.12 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software and Solutions

- 5.2 By Technology

- 5.2.1 Bluetooth Low Energy

- 5.2.2 RFID

- 5.2.3 Sensors (Ambient-light)

- 5.2.4 Software Agents

- 5.2.5 Affective Computing

- 5.2.6 Nanotechnology

- 5.2.7 Biometrics

- 5.2.8 Other Technologies

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Retail

- 5.3.3 Healthcare

- 5.3.4 Industrial

- 5.3.5 Office Building

- 5.3.6 Automotive

- 5.3.7 Other End-user Industries

- 5.4 By Application

- 5.4.1 Smart Building Management

- 5.4.2 Ambient-Assisted Living

- 5.4.3 Smart Home Automation

- 5.4.4 Smart Retail Analytics

- 5.4.5 Smart Manufacturing / Industrial IoT

- 5.4.6 Smart Mobility and Transportation

- 5.4.7 Public Safety and Security

- 5.4.8 Energy Management

- 5.4.9 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Israel

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 United Arab Emirates

- 5.5.5.1.4 Turkey

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Siemens AG

- 6.4.3 Honeywell International Inc.

- 6.4.4 ABB Ltd.

- 6.4.5 Johnson Controls International plc

- 6.4.6 Koninklijke Philips NV

- 6.4.7 Amazon.com Inc.

- 6.4.8 Google LLC

- 6.4.9 Apple Inc.

- 6.4.10 Microsoft Corp.

- 6.4.11 Samsung Electronics Co. Ltd.

- 6.4.12 Bosch GmbH

- 6.4.13 Cisco Systems Inc.

- 6.4.14 Legrand SA

- 6.4.15 Ingersoll-Rand PLC

- 6.4.16 Tunstall Healthcare Ltd.

- 6.4.17 Caretech AB

- 6.4.18 Getemed Medizin-Und Informationstechnik AG

- 6.4.19 Televic NV

- 6.4.20 Vitaphone GmbH

- 6.4.21 Xiaomi Corp.

- 6.4.22 Assisted Living Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment