|

시장보고서

상품코드

1850263

살생물제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Biocides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

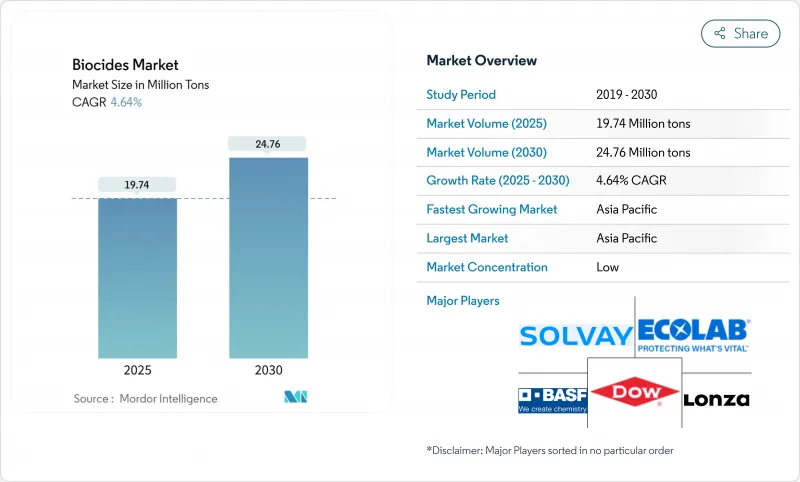

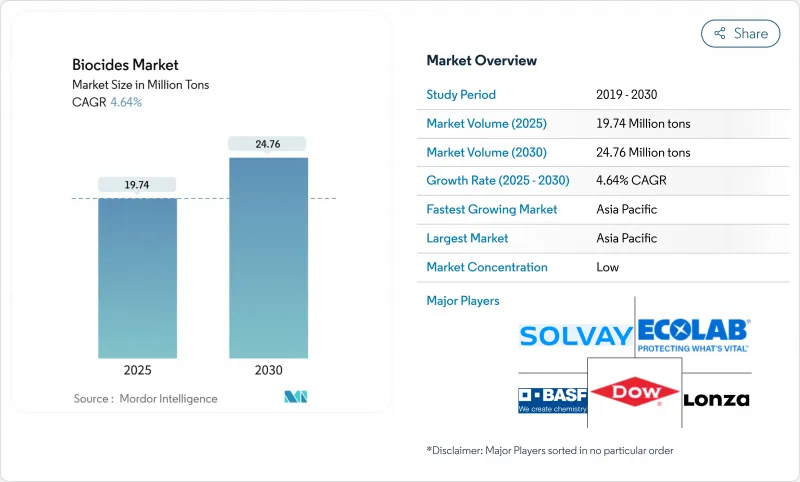

살생물제 시장 규모는 2025년에 1,974만 톤으로 평가되었고, 2030년에는 2,476만 톤에 이를 것으로 예측되며, 2025-2030년의 CAGR은 4.64%를 나타낼 전망입니다.

수처리, 식품 안전, 의료 및 건설 분야에서 항균 솔루션에 대한 견고한 수요는 최종 사용자가 더 엄격한 환경 규제에 직면하고 있음에도 불구하고 여전히 판매량 증가를 뒷받침하고 있습니다. 산업용 수 재사용 프로젝트의 꾸준한 증가는 적용 기반을 확대하고 있으며, 이에 따른 소비 증가 추세는 용량 최적화 기술이 직접적으로 더 큰 시장 규모로 이어지고 있음을 시사합니다. 동시에 지속가능성 요구사항은 제조사들이 산화성 및 바이오 기반 제형으로 포트폴리오를 다각화하도록 유도하고 있으며, 이는 전반적인 산업 확장이 질적 기술 업그레이드와 동반되고 있음을 시사합니다. 생산량 증가와 친환경 화학물질의 공존은 규모 효율성이 규정 준수 준비와 함께 개선되고 있음을 나타냅니다. 주요 공급업체들의 투자 계획에서 드러나는 증거는 또한 업계가 투기적 성장을 쫓기보다 예상 수요 곡선에 맞춰 생산 능력 증설을 조정하고 있음을 추가로 보여줍니다.

세계의 살생물제 시장 동향 및 인사이트

전 세계적으로 증가하는 수처리 수요

물 부족 심화와 재사용 목표 강화로 지자체 및 산업 운영자들은 활성 성분 부하를 낮추면서도 잔류 효능을 유지하는 살생물제 제형을 도입하고 있습니다. 유틸리티 업체들은 센서와 클라우드 분석을 통합한 투여량 제어 플랫폼을 채택하며, 이는 살생물제 시장을 성과 기반 조달 모델로 전환시키고 있습니다. 미국 규제 기관이 최근 지하수 정화에 승인한 과초산 및 안정화 브롬은 산화력과 신속한 분해가 결합된 제품이 규정 준수를 위한 최적의 선택으로 간주됨을 보여줍니다. 핵심 시사점은 데이터 기반 투여 지침을 제품에 통합하는 공급업체들이 상품화 압력 속에서 시장 지위를 방위할 가능성이 높다는 점입니다.

식품 및 음료 산업의 증가하는 수요

식품 가공업체들은 검출 가능한 잔류물을 남기지 않으면서 교차 오염을 최소화하기 위해 위생 프로토콜을 수정하고 있으며, 이는 표면뿐만 아니라 주변 공기에서도 작용하는 하이드록실 라디칼 시스템에 대한 수요를 높입니다. 포장 공장들은 이제 부패 미생물을 억제하여 유통기한을 연장하기 위해 살균제가 내장된 나노 복합재를 시험 중이며, 이는 보존 기능의 범위를 제품 자체를 넘어 확장하는 변화입니다. 공기, 표면, 포장재 살균의 융합은 통합 위생 솔루션이 여러 예산 항목에 걸친 교차 판매 기회를 창출할 수 있음을 시사합니다. 이러한 패턴은 기존 습식 화학 소독제에서 지속적 작용 기술로의 점진적 대체를 나타냅니다.

살생물제와 관련된 환경 문제와 건강 피해

규제 기관은 잔류성 또는 발암성 우려가 있는 활성 물질을 단계적으로 퇴출하고 있습니다. 유럽 위원회의 에틸렌옥사이드 사용 중단 조치는 제형 개발자들이 직면한 규제 불확실성을 보여줍니다. 선체 청소 시 10,000m²당 최대 4.3kg의 미세 플라스틱 페인트 입자가 방출된다는 연구 결과는 특정 코팅재의 생태학적 비용을 부각시킵니다. 이러한 발견은 분해 가능한 활성 성분에 대한 수요를 증대시키며, 이는 다시 바이오 기반 원료에 대한 연구 개발을 촉진합니다. 보험사와 항만 당국이 기존 코팅재에 의존하는 운영자에게 벌금을 부과할 수 있다는 신호가 나타나면서, 간접적으로 생태 최적화된 살생물제 채택이 촉진될 수 있습니다.

부문 분석

할로겐 화합물은 2024년 살생물제 시장 점유율의 28%를 차지하며, 2030년까지 연평균 5.8%의 성장률을 보일 것으로 예상됩니다. 이는 많은 최종 사용 분야에서 여전히 효능이 환경적 우려보다 우선시됨을 나타냅니다. 브롬 기반 솔루션은 염소계 제품이 한계에 부딪히는 고온 냉각 시스템에서도 생물학적 정지 효과가 지속되어 여전히 최우선 선택지로 남아 있으며, 이는 해당 부문 성장의 운영적 근거를 보여줍니다. 브롬 방출량을 조절하는 캡슐화 기술은 현재 서비스 주기를 연장하여 전체 화학물질 배출량을 감소시키고 강화되는 폐수 규제와 부합합니다. 이는 전면적인 활성 성분 교체보다는 점진적인 공정 개선을 통해 성능과 규정 준수를 동시에 달성할 수 있음을 시사합니다.

공급사들이 생분해성 프로필 개선을 통해 친환경 인증을 추구함에 따라 할로겐 계열 내 경쟁이 격화되고 있습니다. 앨버마일의 추출 공정 최적화는 브롬 단위당 에너지 투입량을 낮추며, 상류 공정에서의 지속가능성 개선이 하류 수요 증대로 이어질 수 있음을 시사합니다. 병행 연구개발에서는 실시간 모니터링이 가능한 이산화염소 발생기를 탐구 중이며, 이는 화학 기술과 더불어 디지털 역량이 차별화 요소로 부상하고 있음을 나타냅니다. 종합적으로 이러한 움직임은 할로겐 공급사들이 단순 제품 판매자에서 솔루션 파트너로 전환하고 있음을 시사합니다.

지역 분석

아시아태평양 지역은 2024년 글로벌 살생물제 시장 점유율의 35%를 차지하며, 2030년까지 5.15%의 가장 빠른 연평균 성장률(CAGR)을 보일 것으로 예상됩니다. 이는 산업 확장과 함께 강화된 공중보건 감독을 반영한 것입니다. 중국은 산업단지 내 물 재사용률 제고를 추진하며 고성능 산화성 살균제 도입을 가속화하고 있으며, 인도는 스마트 시티 미션을 통해 지방자치단체 소독 인프라에 예산을 집중하고 있습니다. 일본 공급업체들은 특수 기술 노하우를 활용해 고순도 활성 성분을 인근 국가에 수출하며 아시아 내 공급망 심화를 보여주고 있습니다. 한편 동남아시아 경제권은 모듈형 브롬 기반 시스템을 도입해 기존 염소 처리 방식을 뛰어넘고 있으며, 이는 후발 주자가 초기부터 첨단 화학 기술을 수용할 수 있음을 보여줍니다. 해당 지역의 수요 패턴을 종합하면 물량 증가와 함께 기술 동화 속도가 빠르다는 점을 시사합니다.

북미는 여전히 기술 선도자로서, 미국 환경보호청(EPA)의 지속적인 TSCA(독성물질통제법) 및 FIFRA(농약관리법) 검토로 인해 제형 개발사들은 강력한 독성학 데이터 패키지를 유지해야 합니다. 이러한 규제 강도는 지속성이 낮은 활성 성분 분야의 혁신을 촉진하며, 이는 다시 다른 관할권으로 수출됩니다. 캐나다의 산림 유산은 상당한 목재 방부제 시장을 유지하며, 현재 주 당국은 더 낮은 침출수 기준치를 규정하여 공급업체들이 구리-아졸 하이브리드 제품으로 전환하도록 유도하고 있습니다. 또한 석유화학 단지 내 대규모 냉각탑 개조 사업으로 인해 지역 시장이 혜택을 보고 있으며, 이는 수요가 신규 건설뿐만 아니라 유지보수 주기와도 연결되어 있음을 시사합니다.

유럽은 전 세계에서 가장 엄격한 살생물제 제품 허가 체계를 자랑하며, 신청자가 새로운 환경 위험 데이터를 제출하지 못할 경우 활성 물질 승인이 취소될 수 있습니다. 최근 에틸렌옥사이드의 철수는 이러한 역학을 부각시키며, 더 안전한 대체재에 대한 사업적 타당성을 강화합니다. 독일과 영국이 소비를 주도하지만, 북유럽 국가들은 종종 생분해성 솔루션을 선도적으로 도입한 후 남부 지역으로 확산시키는 역할을 합니다. 순환경제 법규는 수명 종료 시 환경 발자국이 최소화된 활성 물질을 선호하므로, 전 생애 주기 평가에 투자하는 공급업체가 향후 입찰에서 유리한 위치를 차지합니다. 누적 효과로 유럽은 시험장이 되며, 해당 규정을 충족하는 제품은 일반적으로 약간의 수정만으로 타 지역에서도 수용될 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계적인 수처리 수요 증가

- 식품 및 음료 업계에서 높은 수요

- 건강과 위생에 대한 의식의 향상

- 페인트 및 코팅 업계에서 수요 고조

- 보다 안전한 대체품에 대한 규제 지원

- 시장 성장 억제요인

- 살생물제와 관련된 환경 문제와 건강 피해

- 원재료 가격 변동

- 높은 연구개발비

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 할로겐 화합물

- 금속 화합물

- 유기 황화합물

- 유기산

- 페놀류

- 기타 유형(4급 암모늄 화합물)

- 용도별

- 수처리

- 의약품 및 퍼스널케어

- 목재 방부

- 식품 및 음료

- 페인트 및 코팅

- 기타 용도(석유 및 가스, 농업, 소독제 및 위생 관리)

- 작용기전별

- 산화살생물제

- 비산화성 살생물제

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 말레이시아

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Albemarle Corporation

- Arxada

- Baker Hughes Company

- BASF SE

- Dow

- Ecolab

- IRO Group Inc.

- Italmatch AWS

- Kemipex

- Kemira

- LANXESS

- Lonza

- Merck KGaA

- Nouryon

- Solvay

- Stepan Company

- The Lubrizol Corporation

- Thor Group Ltd.

- Valtris Specialty Chemicals

- Veolia

- Vink Chemicals GmbH & Co. KG

제7장 시장 기회와 장래의 전망

HBR 25.11.19The biocides market size is valued at 19.74 million tons in 2025 and is forecast to attain 24.76 million tons by 2030, reflecting a 4.64% CAGR during 2025-2030.

Robust demand for antimicrobial solutions in water treatment, food safety, healthcare, and construction continues to underpin volume growth, even as end-users confront stricter environmental regulations. A steady rise in industrial water reuse projects is widening the application base, and the resulting consumption uptick suggests that dosage-optimization technologies are translating directly into larger addressable volumes. At the same time, sustainability requirements are encouraging manufacturers to diversify portfolios toward oxidizing and biobased formulations, which implies that overall industry expansion is being accompanied by a qualitative technology upgrade. The coexistence of rising output and greener chemistries signals that scale efficiencies are improving alongside compliance readiness. Evidence from leading suppliers' investment plans further indicates that the industry is aligning capacity additions with the projected demand curve rather than chasing speculative growth.

Global Biocides Market Trends and Insights

Increasing Demand for Water Treatment Globally

Rising water scarcity and heightened reuse targets drive municipalities and industrial operators to deploy biocide formulations that maintain residual efficacy with lower active-ingredient loads. Utilities are adopting dosage-control platforms that integrate sensors with cloud analytics, which is nudging the biocides market toward performance-based procurement models. Peracetic acid and stabilized bromine, recently endorsed for groundwater remediation by United States regulators, demonstrate that oxidation strength combined with rapid decomposition is considered the sweet spot for compliance. A key inference is that suppliers who embed data-driven dosing guidance into their product offering will likely defend market positions against commoditization pressure.

Growing Demand From the Food and Beverage Industry

Food processors are revising sanitation protocols to minimize cross-contamination without leaving detectable residues, which lifts demand for hydroxyl-radical systems that work in ambient air as well as on surfaces. Packaging plants now trial biocide-embedded nanocomposites to extend shelf life by suppressing spoilage organisms, a shift that expands the functional scope of preservation beyond the product itself. This convergence of air, surface, and package sterilization suggests that integrated hygiene solutions can unlock cross-sell opportunities across multiple budget lines. The pattern indicates a gradual substitution away from legacy wet-chemistry disinfectants toward continuous-action technologies.

Environmental Issues and Health Hazards Related to Biocides

Regulators are phasing out active substances with persistence or carcinogenicity concerns; the European Commission's withdrawal of ethylene oxide illustrates the regulatory unpredictability facing formulators. Research estimating up to 4.3 kg of microplastic paint particles released per 10,000 m2 of ship hull during cleaning underscores the ecological cost of certain coatings. Such findings are intensifying demand for degradable actives, which in turn encourage research and development into biobased feedstocks. An emerging signal is that insurers and port authorities could start penalizing operators that rely on legacy coatings, indirectly boosting eco-optimized biocides adoption.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Awareness of Health and Hygiene

- Rising Demand in Paints and Coatings Industry

- Fluctuating Raw Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Halogen compounds account for 28% biocides market share in 2024 and are forecast to expand at a 5.8% CAGR to 2030, indicating that efficacy still outweighs environmental apprehensions in many end-uses. Bromine-based solutions remain the first choice for high-temperature cooling systems because their biostatic effect persists where chlorination falters, revealing an operational rationale behind the segment's growth. Encapsulation methods that meter bromine release now prolong service intervals, which reduces overall chemical discharge and aligns with tightening wastewater rules. The inference is that incremental process tweaks, rather than wholesale active-switching, can reconcile performance with compliance.

Competition within halogens intensifies as suppliers seek greener credentials by improving biodegradability profiles. Albemarle's extraction optimization lowers energy input per bromine unit, signaling that upstream sustainability gains can cascade into stronger downstream demand. Parallel research and development explores chlorine-dioxide generators with real-time monitoring, indicating that digital capabilities are becoming a differentiator alongside chemistry. Collectively, these initiatives suggest that halogen suppliers are pivoting from product sellers to solution partners.

The Biocides Market Report Segments the Industry by Type (Halogen Compounds, Metallic Compounds, and More), Application (Water Treatment, Pharmaceutical and Personal Care, Wood Preservation, and More), Mode of Action (Oxidizing Biocides and Non-Oxidizing Biocides), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific contributes 35% of the global biocides market share in 2024 and shows the fastest CAGR at 5.15% to 2030, reflecting industrial expansion accompanied by stricter public-health oversight. China's push for higher water-reuse ratios in industrial parks is accelerating the adoption of high-performing oxidizing biocides, while India's Smart Cities Mission channels budget toward municipal disinfection infrastructure. Japanese suppliers leverage specialty know-how to export high-purity actives to regional neighbors, indicating intra-Asian supply-chain deepening. Meanwhile, Southeast Asian economies are leapfrogging legacy chlorination by adopting modular bromine-based systems, highlighting how latecomers can embrace state-of-the-art chemistry from inception. Collectively, the region's demand pattern suggests that volume increases are accompanied by fast technology assimilation.

North America remains a technology trailblazer, where the United States Environmental Protection Agency's ongoing TSCA and FIFRA reviews compel formulators to maintain robust toxicology data packages. This regulatory rigour spurs innovation in less persistent actives, which in turn gets exported to other jurisdictions. Canada's forestry heritage sustains a sizable wood-preservation segment, and provincial authorities now stipulate lower leachate thresholds, pushing suppliers toward copper-azole hybrids. The regional market also benefits from large-scale cooling-tower retrofits in petrochemical complexes, implying that demand is tied not only to new-builds but also to maintenance cycles.

Europe stands out for the toughest biocide product authorization framework worldwide, where active-substance approvals can lapse if applicants fail to supply new environmental-risk data. The recent withdrawal of ethylene oxide underscores this dynamic, reinforcing the business case for safer substitutes. Germany and the United Kingdom dominate consumption, yet Nordic countries often pioneer biodegradable solutions that later scale southwards. Circular-economy legislation favors actives with minimal end-of-life footprint, so suppliers investing in cradle-to-grave assessments are better positioned for future tenders. The cumulative effect is that Europe acts as a proving ground: products succeeding under its rules can typically secure acceptance elsewhere with minor adaptations.

- Albemarle Corporation

- Arxada

- Baker Hughes Company

- BASF SE

- Dow

- Ecolab

- IRO Group Inc.

- Italmatch AWS

- Kemipex

- Kemira

- LANXESS

- Lonza

- Merck KGaA

- Nouryon

- Solvay

- Stepan Company

- The Lubrizol Corporation

- Thor Group Ltd.

- Valtris Specialty Chemicals

- Veolia

- Vink Chemicals GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Water Treatment Globally

- 4.2.2 Growing Demand From the Food and Beverage Industry

- 4.2.3 Heightened Awareness of Health and Hygiene

- 4.2.4 Rising Demand in Paints and Coatings Industry

- 4.2.5 Regulatory Support for Safer Alternatives

- 4.3 Market Restraints

- 4.3.1 Environmental Issues and Health Hazards Related to Biocides

- 4.3.2 Fluctuating Raw Material Prices

- 4.3.3 High Research and Development Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Halogen Compounds

- 5.1.2 Metallic Compounds

- 5.1.3 Organosulfurs

- 5.1.4 Organic Acids

- 5.1.5 Phenolics

- 5.1.6 Other Types (Quaternary Ammonium Compounds)

- 5.2 By Application

- 5.2.1 Water Treatment

- 5.2.2 Pharmaceutical and Personal-care

- 5.2.3 Wood Preservation

- 5.2.4 Food and Beverage

- 5.2.5 Paints and Coatings

- 5.2.6 Other Applications (Oil and Gas, Agriculture, Disinfectants and Sanitization)

- 5.3 By Mode of Action

- 5.3.1 Oxidizing Biocides

- 5.3.2 Non-oxidizing Biocides

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordics

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 Arxada

- 6.4.3 Baker Hughes Company

- 6.4.4 BASF SE

- 6.4.5 Dow

- 6.4.6 Ecolab

- 6.4.7 IRO Group Inc.

- 6.4.8 Italmatch AWS

- 6.4.9 Kemipex

- 6.4.10 Kemira

- 6.4.11 LANXESS

- 6.4.12 Lonza

- 6.4.13 Merck KGaA

- 6.4.14 Nouryon

- 6.4.15 Solvay

- 6.4.16 Stepan Company

- 6.4.17 The Lubrizol Corporation

- 6.4.18 Thor Group Ltd.

- 6.4.19 Valtris Specialty Chemicals

- 6.4.20 Veolia

- 6.4.21 Vink Chemicals GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increasing Awareness in the Agricultural Sector