|

시장보고서

상품코드

1850314

네트워크 슬라이싱 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Network Slicing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

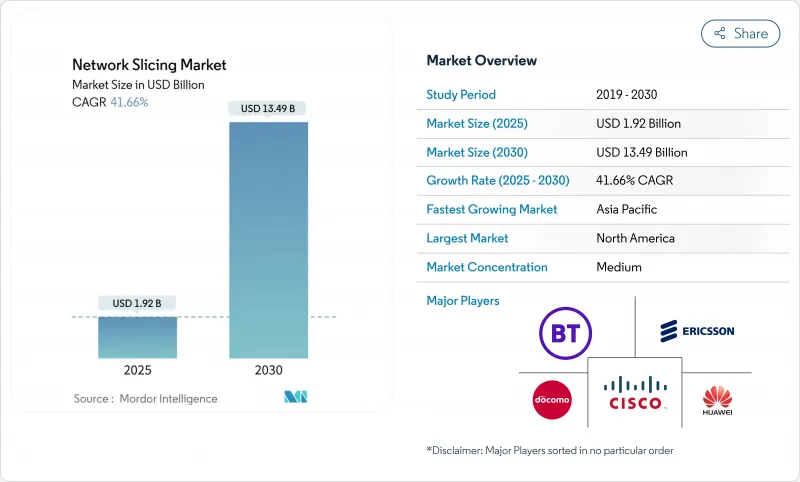

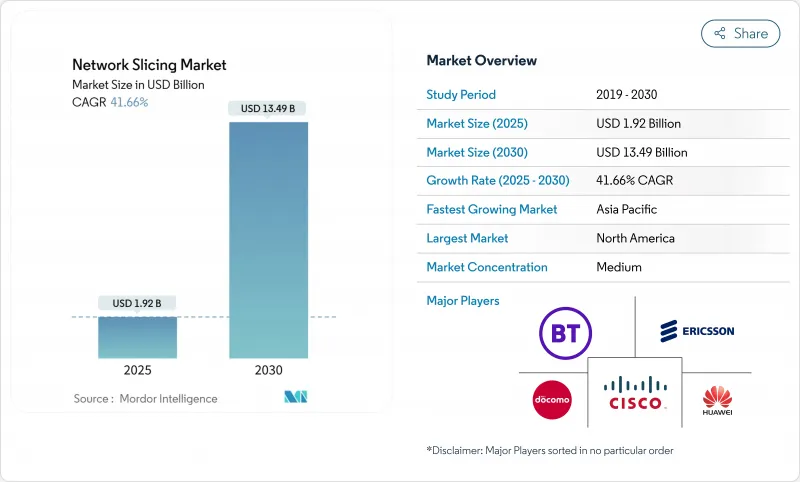

네트워크 슬라이싱 시장 규모는 2025년에 19억 2,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 41.66%로 성장할 전망이며, 2030년에는 134억 9,000만 달러에 달할 것으로 예측됩니다.

최선형 연결에서 프로그래머블 서비스 차별화된 네트워크로의 전환이 주된 계기가 되어 통신 서비스 공급자(CSP)는 서비스 수준이 보장된 가상 네트워크 부문을 통해 5G 독립형(SA)에 대한 투자를 수익화할 수 있습니다. 급속한 5G SA 전개, 인더스트리 4.0 플랜트에서 초고신뢰성 저지연 통신(URLLC)의 필요성, 슬라이스 아즈 아 서비스 모델의 매력이 채용을 가속시키고 있습니다. 슬라이스의 라이프사이클 관리를 자동화하는 오케스트레이션 플랫폼을 제공하기 위해 인프라벤더, 클라우드 네이티브 소프트웨어 전문가, 하이퍼스케일러가 격렬해지고 경쟁이 치열해지고 있습니다. 반도체 리드 타임이 56주인 것 등 공급망의 제약은 여전히 계속되고 있지만, 사업자는 계속해서 네트워크 애즈 코드 API를 통해 개발자 주도의 수익 스트림을 획득하기 위한 소프트웨어 투자를 우선하고 있습니다.

세계의 네트워크 슬라이싱 시장 동향 및 인사이트

CSP 수요 이동을 가속화하는 5G SA 롤아웃

독립형 5G 아키텍처는 네트워크 슬라이싱의 모든 기능을 해제하고 운영자는 레거시 코어에서 제공할 수 없는 서비스 수준을 보장하는 격리된 논리 네트워크를 스핀업할 수 있습니다. 일본에서는 2024년 4월까지 5G 기지국의 커버율이 98%에 이르렀으며 SA 업그레이드에 박차를 가해 슬라이싱 대응 인프라에 대한 세계 축족이 나타났습니다. 에릭슨과 12개의 티아완 통신 사업자와의 제휴는 2030년까지 300억 달러의 네트워크 API 시장을 목표로 하며, 프로그래머빌리티의 기반으로 슬라이싱에 의존하고 있습니다. T-Mobile의 하이브리드 프라이빗 5G+ 슬라이싱을 통해 응급 의료 데이터로의 전개는 차별화된 연결성이 얼마나 신속하게 상용화될 수 있는지를 보여줍니다.

URLLC 및 eMBB 슬라이싱에 대한 기업의 개인 네트워크 수요

산업 기업은 슬라이싱을 결정론적 연결에 가장 경제적인 경로로 간주합니다. 이탈리아에서는 에릭슨, TIM, 코마우가 10ms 이하의 슬라이스를 사용하여 디지털 트윈과 로봇을 동기화하여 예지 보전 및 원격 AR 지원의 운영상의 이점을 입증했습니다. 한국에서는 2024년 2월까지 56개소에 사설 5G 주파수대가 할당되어 슬라이스 분리에 의존하는 기업 운영의 인프라에 대한 규제 당국의 지원이 나타났습니다.

신흥국의 낮은 5G 보급률 및 디바이스 준비 상황

네트워크 슬라이싱에서는 SA 커버리지의 넓이와 슬라이스를 선택할 수 있는 단말이 요구되고 있지만, 2024년 말 시점의 SA 커버리지는 중국이 80%인 반면 유럽은 불과 2%에 그쳤습니다. 인도네시아의 5G 경매 지연은 정책 갭이 롤아웃을 늦추고 운영자의 슬라이스 플랫폼에 대한 투자 의욕을 줄이는 방법을 보여줍니다.

부문 분석

2024년 네트워크 슬라이싱 시장에서의 소프트웨어 점유율은 45.50%로, 사업자가 오케스트레이션, 어슈어런스, 보안 툴에 주력하고 있기 때문에 CAGR은 44.25%로 성장하고 있습니다. 소프트웨어 플랫폼에서 파생된 네트워크 슬라이싱 시장 규모는 라디오에 민감하지 않은 제어 로직과 함께 2030년까지 60억 달러 이상에 달할 것으로 예측됩니다. 공급업체는 슬라이스 대역폭을 실시간으로 조정하는 인텐트 기반 정책 엔진을 통해 차별화를 도모하고 있습니다. 테넌트 트래픽을 분리하고 슬라이스 무결성을 검증하는 보안 모듈은 현재 애드온으로 판매되지 않고 카탈로그에 내장되어 시장 출시 시간을 단축하고 멀티 테넌트 수익 창출을 지원합니다. 인프라 하드웨어는 여전히 5G SA 코어에 필수적이지만, CSP가 기존 RAN 자산에 땀을 흘리면서 새로운 자금을 자동화된 슬라이스 관리로 돌이키기 때문에 성장이 늦어지고 있습니다. 전송 업그레이드는 마이크로웨이브, 광섬유 및 IP/MPLS 링크에서 결정적인 지연을 보장해야 할 필요성에 따라 박차를 받고 있습니다.

총 소유 비용을 평가하는 운영자는 클라우드 네이티브 네트워크 기능을 상용 서버에 상주할 수 있는 개방형 인터페이스가 있는 분리형 인프라를 선호합니다. 이 피벗은 자본 투자의 첨단을 완화하고 소프트웨어 도입을 가속화하며 네트워크 슬라이싱 시장에서 자동화의 핵심 역할을 강화합니다. 메트로 데이터센터에 내장된 MEC(Multi Access Edge Computing) 노드는 소프트웨어 사용 범위를 더욱 확장하여 대기 시간에 민감한 워크로드를 위해 현지화된 슬라이스를 인스턴스화할 수 있습니다.

매니지드 서비스는 2024년 네트워크 슬라이싱 시장 점유율의 55.45%를 차지하였고, CAGR 42.36%로 성장할 전망입니다. 공급업체가 운영하는 포털 사이트에서는 IT 관리자가 온디맨드로 슬라이스를 요청하고, 서비스 품질 수준을 설정하며, 사용량에 따라 요금을 받을 수 있습니다. CSP가 보안 및 엣지 컴퓨팅과 연결성을 번들로 함으로써 관리형 서비스와 관련된 네트워크 슬라이싱 시장 규모는 2030년까지 70억 달러를 초과할 가능성이 높습니다. Network-as-a-Service(NaaS)의 변종은 사내에 스펙트럼 전문지식이 없는 중견기업에 어필하며, 정부기관은 공공안전영상을 위해 매니지드 슬라이스를 채용하여 소블린 데이터 호스팅 보증의 혜택을 받습니다.

컨설팅, 통합, 테스트 등의 전문 서비스는 복잡한 채용 사이클의 온 램프 역할을 합니다. 시스템 통합자는 슬라이스 오케스트레이션을 엔터프라이즈 SD-WAN, ERP 및 IoT 플랫폼과 연계시켜 전개 위험을 줄입니다. Proof of Concept Lab은 상용 컷오버 전에 처리량 및 대기 시간 목표를 검증하여 수술 로봇 및 실시간 품질 검사와 같은 미션 크리티컬한 이용 사례의 불확실성을 줄입니다.

네트워크 슬라이싱 시장 보고서는 컴포넌트별(인프라(RAN, 코어, 전송), 소프트웨어(MANO, 애널리틱스, 보안)), 서비스별(프로페셔널 (컨설팅, 통합, 테스트) 등), 용도별(원격 모니터링 및 모니터링, 네트워크 기능 가상화, 클라우드 RAN 등), 최종 사용자 산업별(헬스케어, 자동차, 운송, 기타), 지역별로 구분됩니다.

지역 분석

북미는 2024년 네트워크 슬라이싱 시장에서 34.92%의 점유율을 차지했으며, 조기 5G SA 출시와 관용적인 주파수 정책이 그 요인이 되고 있습니다. T-Mobile과 같은 CSP는 슬라이스 오더 API를 전국에 공개하여 기업이 퍼블릭 실적에 개인 커버리지를 통합할 수 있도록 합니다. Verizon의 프런트 라인 네트워크 슬라이스는 로스 앤젤레스와 시카고 구급 대원을 위해 제공되며 프리미엄 SLA 티어에 의해 증수를 창출하고 있습니다. 벤처 캐피탈이 오케스트레이션의 신흥 기업으로 흘러 들어가 클라우드 네이티브 설계에 유리한 혁신 루프가 강화되었습니다. 반도체 부족으로 무선 유닛의 리드 타임은 56주로 연장되었지만, 운영자는 멀티 벤더 조달 덕분에 일정대로 추이하고 있습니다.

아시아태평양의 CAGR은 42.22%로 이 지역에서 가장 빠른 페이스가 될 것으로 예측됩니다. 이는 중국이 5G 사이트를 228만 곳 돌파하고 규제 당국이 엔터프라이즈 슬라이스의 시험 운용을 촉진하기 때문입니다. 일본 총무부는 공장에서 SA 네트워크를 자체 전개할 수 있는 로컬 5G 라이선스를 발행했으며 현재 72개 검증 프로젝트가 스마트 포트, 물류 허브, 경기장에 이르고 있습니다. 한국에서는 35개의 콩그로말리트에 전용 주파수대가 할당되어 슬라이스 대응 기기나 RAN의 자동화를 둘러싼 공급자의 에코시스템이 활성화되고 있습니다.

유럽에서는 SA 커버율이 2%로 늦어져 단기적인 슬라이스 수익에 제약이 있지만 정책은 바뀌고 있습니다. 7개국이 로컬 5G용으로 26GHz대를 개방해, 6개국이 3.4-3.8GHz대에서 최대 100MHz를 허가해, 제조나 연구용의 캠퍼스 네트워크가 가능하게 되었습니다. 202억 8,000만 달러의 보다폰 쓰리 영국의 합병은 2035년까지 148억 6,000만 달러의 네트워크 업그레이드를 약속했으며, 이는 SA와 슬라이싱 채택을 가속화해야 합니다. 중동에서는 유럽 벤더가 지역 통신 사업자와 transport-network 슬라이싱을 시험적으로 도입하고 있으며, 주파수 대역과 투자가 수렴하면 유럽을 다시 채울 수 있는 아키텍처를 검증하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 5G SA의 전개가 CSP 수요 시프트를 가속

- URLLC 및 eMBB 슬라이스에 대한 엔터프라이즈 프라이빗 네트워크 수요

- 엣지 클라우드의 통합에 의해 동적인 슬라이스 오케스트레이션 가능

- ARPU 정체 중 CSP 수익화가 급무

- 언더 더 레이더 : 개발자 주도의 슬라이스 도입을 촉진하는 'Network-as-Code' API

- 언더 더 레이더 : 권리에 기초한 원격 방송 패키지(스포츠, 선거)

- 시장 성장 억제요인

- 신흥국에서의 5G 보급률 및 디바이스의 낮은 준비 상황

- 멀티 도메인 오케스트레이션의 복잡성, OPEX의 부담

- 언더 더 레이더 : 단편화된 슬라이스 SLA 보안 인증 표준

- 언더 더 레이더 : 동적 슬라이스의 스펙트럼 공유에 관한 규제 불확실성

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 가격 분석

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 인프라(RAN, 코어, 전송)

- 소프트웨어(MANO, 분석, 보안)

- 서비스별

- 전문(컨설팅, 통합, 테스트)

- 매니지드(Network-as-a-Service, Slice-as-a-Service)

- 용도별

- 원격 감시 및 감시

- 네트워크 기능 가상화 및 클라우드 RAN

- 모바일 클라우드 게임 및 미디어 스트리밍

- 원격 산업 자동화(IIoT)

- 최종 사용자 업계별

- 헬스케어

- 자동차 및 운송

- 전력 및 에너지

- 항공우주

- 미디어 및 엔터테인먼트

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- Samsung Electronics

- ZTE

- NEC

- BT Group

- NTT DOCOMO

- Mavenir

- Affirmed Networks

- Argela Technologies

- Aria Networks

- Juniper Networks

- Keysight Technologies

- NetScout

- Verizon Communications

- ATandT

- T-Mobile US

- Deutsche Telekom

제7장 시장 기회 및 향후 전망

AJY 25.11.07The Network Slicing Market size is estimated at USD 1.92 billion in 2025, and is expected to reach USD 13.49 billion by 2030, at a CAGR of 41.66% during the forecast period (2025-2030).

The shift from best-effort connections to programmable, service-differentiated networks is the prime catalyst, enabling communication service providers (CSPs) to monetize 5G standalone (SA) investments through virtual network segments with guaranteed service levels. Rapid 5G SA roll-outs, the need for ultra-reliable low-latency communication (URLLC) in Industry 4.0 plants, and the appeal of slice-as-a-service models are accelerating adoption. Competitive intensity is rising as infrastructure vendors, cloud-native software specialists, and hyperscalers race to deliver orchestration platforms that automate slice life-cycle management. Supply-chain constraints persist, notably 56-week semiconductor lead times, yet operators continue to prioritize software investments to capture developer-led revenue streams through network-as-code APIs.

Global Network Slicing Market Trends and Insights

5G SA Roll-Outs Accelerating CSP Demand Shift

Standalone 5G architecture unlocks full network slicing capabilities, letting operators spin up isolated logical networks with guaranteed service levels that legacy cores cannot provide. Japan reached 98% 5G base-station coverage in designated areas by April 2024, spurring SA upgrades and signaling a global pivot toward slicing-ready infrastructure. Ericsson's alliance with 12 tier-one operators targets a USD 30 billion network-API market by 2030, relying on slicing as the foundation for programmability. T-Mobile's hybrid private-5G-plus-slicing deployment for emergency medical data shows how differentiated connectivity can be commercialized quickly.

Enterprise Private-Network Demand for URLLC & eMBB Slices

Industrial companies view slicing as the most economical route to deterministic connectivity. In Italy, Ericsson, TIM, and Comau synchronized robots with digital twins using sub-10 ms slices, proving operational gains in predictive maintenance and remote AR support. South Korea allocated private 5G spectrum to 56 sites by February 2024, illustrating regulator support for enterprise-run infrastructure that relies on slice isolation.

Low 5G Penetration and Device Readiness in Emerging Economies

Network slicing demands widespread SA coverage plus handsets able to select slices, yet Europe had only 2% SA coverage versus China's 80% at end-2024. Delays in Indonesia's 5G auctions illustrate how policy gaps can slow roll-outs, reducing operator incentive to invest in slice platforms.

Other drivers and restraints analyzed in the detailed report include:

- Edge-Cloud Convergence Enabling Dynamic Slice Orchestration

- CSP Monetization Urgency Amid ARPU Stagnation

- Multi-Domain Orchestration Complexity and OPEX Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held a 45.50% share of the network slicing market in 2024 and is growing at a 44.25% CAGR, thanks to operator focus on orchestration, assurance, and security tooling. The network slicing market size derived from software platforms is projected to exceed USD 6 billion by 2030 alongside radio-agnostic control logic. Vendors differentiate through intent-based policy engines that adjust slice bandwidth in real time. Security modules that isolate tenant traffic and validate slice integrity are now baked into catalogues rather than sold as add-ons, lowering time to market and supporting multitenant monetization. Infrastructure hardware remains essential for 5G SA cores, yet its growth lags as CSPs sweat existing RAN assets while directing new funds to automated slice management. Transport upgrades continue, spurred by the need to guarantee deterministic latency across microwave, fiber, and IP/MPLS links.

Operators evaluating total cost of ownership favor disaggregated infrastructure with open interfaces, allowing cloud-native network functions to reside on commodity servers. This pivot moderates capex peaks and accelerates software uptake, reinforcing the central role of automation in the network slicing market. Multi-access edge computing (MEC) nodes embedded in metro data centers further extend software's reach, enabling localized slice instantiation for latency-sensitive workloads.

Managed services controlled 55.45% of the network slicing market share in 2024 and should post a 42.36% CAGR, reflecting enterprise preference for turnkey slice-as-a-service offerings. Vendor-operated portals now let IT managers request slices on demand, set quality-of-service tiers, and receive usage-based billing. The network slicing market size tied to managed services will likely surpass USD 7 billion by 2030 as CSPs bundle security and edge compute with connectivity. Network-as-a-service (NaaS) variants appeal to mid-market firms lacking in-house spectrum expertise, while government agencies adopt managed slices for public-safety footage, benefiting from sovereign data-hosting guarantees.

Professional services, including consulting, integration, and testing, serve as on-ramps for complex adoption cycles. Systems integrators align slice orchestration with enterprise SD-WAN, ERP, and IoT platforms, de-risking deployment. Proof-of-concept labs validate throughput and latency targets before commercial cut-over, reducing uncertainty for mission-critical use cases such as surgical robotics or real-time quality inspection.

The Network Slicing Market Report is Segmented by Component (Infrastructure [RAN, Core, Transport] and Software [MANO, Analytics, Security]), Service (Professional [Consulting, Integration, Testing] and More), Application (Remote Monitoring & Surveillance, Network Function Virtualization and Cloud RAN, and More), End-User Industry (Healthcare, Automotive and Transportation, and More), and Geography.

Geography Analysis

North America held a 34.92% share of the network slicing market in 2024, anchored by early 5G SA launches and permissive spectrum policies. CSPs such as T-Mobile expose slice order APIs nationwide, letting enterprises stitch private coverage into public footprints. Verizon's Frontline Network Slice caters to first responders in Los Angeles and Chicago, generating incremental revenue via premium SLA tiers. Venture capital flows into orchestration start-ups, reinforcing an innovation loop that favors cloud-native design. Semiconductor shortages have lengthened radio unit lead times to 56 weeks, yet operators remain on schedule thanks to multi-vendor sourcing.

Asia Pacific is projected to deliver a 42.22% CAGR, the fastest regional pace, as China surpasses 2.28 million 5G sites and regulators expedite enterprise slice pilots. Japan's Ministry of Internal Affairs and Communications issues local 5 G licenses that let factories self-deploy SA networks; 72 demonstration projects now span smart ports, logistics hubs, and stadiums. South Korea allocates dedicated spectrum to 35 conglomerates, stimulating a supplier ecosystem around slice-aware devices and RAN automation.

Europe lags on SA coverage at 2%, constraining near-term slice revenues, yet policy is shifting. Seven nations opened the 26 GHz band for local 5G, and six permit up to 100 MHz in the 3.4-3.8 GHz band, enabling campus networks for manufacturing and research. The USD 20.28 billion Vodafone-Three UK merger pledges USD 14.86 billion in network upgrades by 2035, which should accelerate SA and slicing adoption. In the Middle East, European vendors pilot transport-network slicing with regional operators, validating architectures that may backfill Europe once spectrum and investment converge.

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- Samsung Electronics

- ZTE

- NEC

- BT Group

- NTT DOCOMO

- Mavenir

- Affirmed Networks

- Argela Technologies

- Aria Networks

- Juniper Networks

- Keysight Technologies

- NetScout

- Verizon Communications

- ATandT

- T-Mobile US

- Deutsche Telekom

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G SA roll-outs accelerating CSP demand shift

- 4.2.2 Enterprise private-network demand for URLLC and eMBB slices

- 4.2.3 Edge-cloud convergence enabling dynamic slice orchestration

- 4.2.4 CSP monetization urgency amid ARPU stagnation

- 4.2.5 Under-the-radar: "Network-as-Code" APIs catalysing developer-led slice uptake

- 4.2.6 Under-the-radar: Rights-based remote broadcasting packages (sports, elections)

- 4.3 Market Restraints

- 4.3.1 Low 5G penetration and device readiness in emerging economies

- 4.3.2 Multi-domain orchestration complexity, OPEX burden

- 4.3.3 Under-the-radar: Fragmented slice-SLA security certification standards

- 4.3.4 Under-the-radar: Regulatory uncertainty over spectrum-sharing for dynamic slices

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Infrastructure (RAN, Core, Transport)

- 5.1.2 Software (MANO, Analytics, Security)

- 5.2 By Service

- 5.2.1 Professional (Consulting, Integration, Testing)

- 5.2.2 Managed (Network-as-a-Service, Slice-as-a-Service)

- 5.3 By Application

- 5.3.1 Remote Monitoring and Surveillance

- 5.3.2 Network Function Virtualization and Cloud RAN

- 5.3.3 Mobile Cloud Gaming and Media Streaming

- 5.3.4 Remote Industrial Automation (IIoT)

- 5.4 By End-User Industry

- 5.4.1 Healthcare

- 5.4.2 Automotive and Transportation

- 5.4.3 Power and Energy

- 5.4.4 Aviation and Aerospace

- 5.4.5 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 United Arab Emirates

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 South Africa

- 5.5.4.4 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ericsson

- 6.4.2 Huawei Technologies

- 6.4.3 Nokia

- 6.4.4 Cisco Systems

- 6.4.5 Samsung Electronics

- 6.4.6 ZTE

- 6.4.7 NEC

- 6.4.8 BT Group

- 6.4.9 NTT DOCOMO

- 6.4.10 Mavenir

- 6.4.11 Affirmed Networks

- 6.4.12 Argela Technologies

- 6.4.13 Aria Networks

- 6.4.14 Juniper Networks

- 6.4.15 Keysight Technologies

- 6.4.16 NetScout

- 6.4.17 Verizon Communications

- 6.4.18 ATandT

- 6.4.19 T-Mobile US

- 6.4.20 Deutsche Telekom

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment