|

시장보고서

상품코드

1850315

고객 셀프 서비스 소프트웨어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Customer Self-Service Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

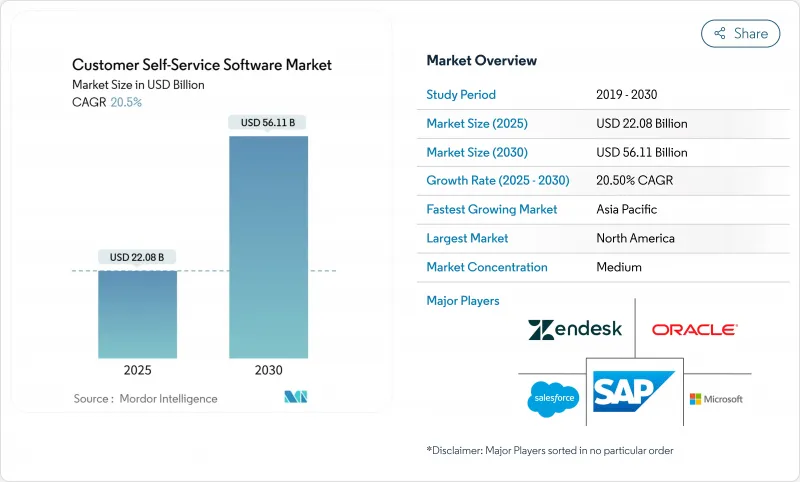

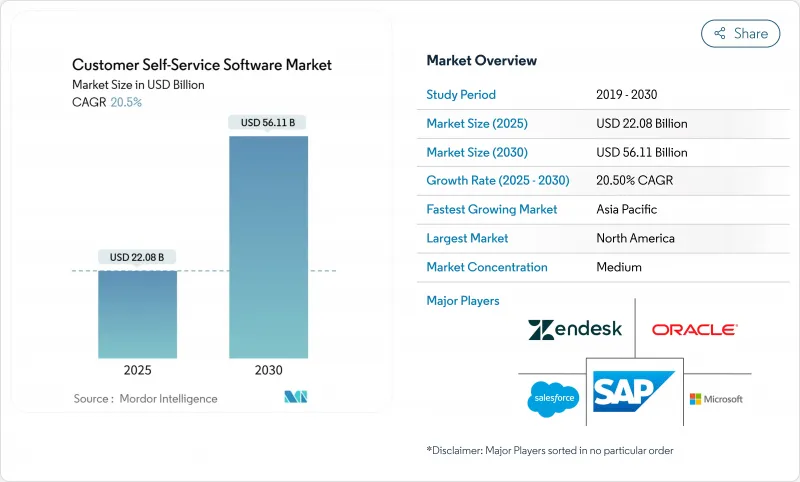

고객 셀프 서비스 소프트웨어 시장 규모는 2025년에 220억 8,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 20.5%로, 2030년에는 561억 1,000만 달러에 달할 것으로 예상됩니다.

이러한 성장은 대화형 인공지능, 클라우드 배포 및 슈퍼 개인화된 워크플로우를 통해 대기 시간을 줄이고 운영 비용을 줄이는 자율적 참여 모델로의 전환을 반영합니다. 또한, 중소기업(SME)은 구독 가격에 따라 대규모 설비 투자가 필요 없기 때문에 채용이 가속화되고 있습니다. 대화형 인터페이스는 자연스럽고 온디맨드 도움말을 요구하는 소비자의 기대에 부합하기 때문에 지속적인 투자를 모으고 있습니다. 지역별 자금 조달 패턴에서는 북미 기업이 최적화 프로젝트를 추진하고 아시아태평양 기업이 모바일 중심 고객을 수용하기 위해 첫 번째 파도 시스템을 도입함으로써 전반적인 기세가 커지고 있습니다.

세계의 고객 셀프 서비스 소프트웨어 시장 동향과 인사이트

클라우드 퍼스트에 의한 CX 변혁의 파

클라우드 네이티브 고객 경험 스택으로 전환하는 기업은 40-60%의 비용 절감과 24시간 가용성을 보고하여 고객 셀프 서비스 소프트웨어 시장에 대한 추가 투자를 촉구하는 결과가 되었습니다. 터치 포인트 간에 거의 즉시 데이터가 동기화되므로 에이전트와 봇이 전체 기록에 액세스할 수 있어 1차 해상도(FCR)가 향상됩니다. 구독 모델은 선행 투자의 필요성을 피할 수 있으므로 중소기업이 가장 이익을 얻을 수 있습니다. 그럼에도 불구하고 여러 지역에 걸친 데이터 레지던스 실은 롤아웃을 복잡하게 하므로 강력한 마이그레이션 지원을 제공하는 공급업체가 유리합니다.

AI를 활용한 셀프 서비스의 성숙도 곡선

Generic AI는 현재 의도를 해석하고, 레코드를 검색하고, 멀티스텝 워크플로우를 실행함으로써 자동화된 포털이 일반 쿼리의 최대 80%를 해결할 수 있도록 합니다. 대규모 언어 모델을 발권 흐름에 통합한 기업은 넷 프로모터 점수가 향상되어 직원이 예외 처리에 전념할 수 있습니다. 정확성이 향상됨에 따라 고객 셀프 서비스 소프트웨어 시장은 일상적인 FAQ 처리에서 고가치로 규제된 트랜잭션 완료로 전환할 것입니다.

단편화된 API 보안 기준

불일치 토큰 프로토콜과 일관성없는 암호화는 통합 비용을 증가시키고 고객 셀프 서비스 소프트웨어 시장의 배포를 지연시킵니다. 까다로운 업계에서는 CRM, ERP 및 지식 기반 연결을 하나의 보안 모델로 통합해야 하며, 그 차이는 새로운 취약점의 표면을 드러내고 있습니다. 이 구획점에 해당하는 공급업체는 사전 인증된 커넥터를 제공하고 지원을 수집합니다.

부문 분석

클라우드 부문은 2024년에 58.7%의 점유율을 차지했고 2030년까지 22.1%의 연평균 복합 성장률(CAGR)을 유지할 것으로 예측됩니다. 클라우드의 상승은 규모의 탄력성을 높여 데이터센터를 확장하지 않고도 세계 릴리스를 가능하게 합니다. 구독 가격은 선행 투자를 억제하여 재무 팀이 비용을 영업 비용으로 인식할 수 있도록 합니다. 벤더는 편향율과 사용자 감정을 시각화하는 내장 애널리틱스를 탑재한 제품의 충실을 계속하고 있습니다.

하이브리드 프레임워크는 소블린 규칙에 의해 기밀성이 높은 지역에서 SaaS가 차단되는 반면, 완전한 On-Premise 스택은 여전히 정부 기관에 집중하고 있습니다. On-Premise에서 마이그레이션하는 기업은 레거시 티켓 레코드를 유지하면서 새 트래픽을 클라우드로 마이그레이션하는 단계별 롤아웃을 채택하는 것이 일반적입니다. 유지 보수 부담을 줄이고 즉각적인 패치 적용이 더욱 매력을 높여 고객 셀프 서비스 소프트웨어 시장의 궤적을 더욱 확실히 하고 있습니다.

엔드 투 엔드 스위트는 2024년 매출의 62.3%를 차지했으며, 지식 기반, 채팅봇, 애널리틱스를 융합한 통합 허브에 대한 구매자의 요구가 밝혀졌습니다. 서비스 카테고리는 기업이 설정, 교육 및 정기적 최적화를 필요로 하기 때문에 CAGR 21.6%를 나타낼 전망입니다. 배포 파트너는 워크플로를 매핑하고 역할 기반 액세스를 관리하는 업계 플레이북을 만들고 변경 관리의 장애물을 넘어 기업을 이끌어 냅니다.

공급업체는 ITIL 프로세스 및 소매점의 주문 상태 흐름에 따라 템플릿(사전 구축됨)을 패키징한 가속기로 가치를 확장합니다. 지속적인 참여는 모듈 튜닝을 유지하고 진화하는 비즈니스 규칙과 봇 의도 사이의 드리프트를 방지합니다. 이러한 전문 서비스 레이어는 플랫폼의 견고성을 높이고 각 배포와 관련된 고객 셀프 서비스 소프트웨어 시장 규모를 확장합니다.

고객 셀프 서비스 소프트웨어 시장은 배포(클라우드, On-Premise, 하이브리드), 제공 제품(솔루션 및 서비스), 채널(웹 포털, 모바일 앱 등), 기업 규모(대기업 및 중견 중소기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어, 소매 및 전자상거래 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 클라우드의 높은 보급률, 성숙한 옴니 채널 전략, AI 모델의 튜닝에 숙련된 기술자층에 힘입어 2024년 매출의 34.2%를 창출했습니다. 많은 기업들이 제일파의 도입을 완료하고 현재는 보다 깊은 애널리틱스를 이용한 저니의 미세 조정에 주력하고 있습니다. 사이버 보안에 대한 연방 정부 수준의 주목은 제로 트러스트 지령에 적합한 플랫폼으로 정부기관과 계약자를 유도하여 리플레이스 사이클을 지속시키고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 21.7%로 예측되어 가장 빠르게 확대되는 벡터입니다. Z세대를 중심으로 한 모바일 퍼스트의 소비자층은 현지의 방언이나 노래방 스타일의 음역을 이해하는 챗봇을 요구하고 있습니다. 각국 정부는 중소기업의 디지털화 보조금을 후원하고 있으며 소매, 여행, 은행 등 고객 셀프 서비스 소프트웨어 시장 수요를 간접적으로 확대하고 있습니다. 다국어 NLP 파이프라인이 있는 공급업체는 이러한 환경에서 차별화할 수 있습니다.

유럽에서는 엄격한 개인 정보 보호법에도 불구하고 꾸준히 발전하고 있습니다. 소블린 클라우드의 프레임워크가 대두하고, 지역의 데이터센터 구축에 박차가 걸려, 컴플라이언스가 확보되고 있습니다. 엔터프라이즈 바이어는 롤아웃을 허용하기 전에 감사 기능과 동의 관리를 검토하고 사실상 경쟁 장애물을 강화하고 있습니다. 규제 오버헤드가 속도를 억제하는 것, 일단 솔루션이 컴플라이언스를 준수한다는 것이 입증되면 인접 부서에 빠르게 확산되고 장기적인 안정성이 보장됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 퍼스트의 CX 변혁 혁신 물결

- AI를 활용한 셀프 서비스 성숙도 곡선

- 고객 데이터 플랫폼을 통한 하이퍼 개인화

- Gen-Z세대 소비자에 의한 셀프 서비스 도입 증가

- 수직형 SaaS 「레이어 케이크」에 셀프 서비스 통합

- 셀프 서비스용 사이버보험료 인센티브 제공

- 시장 성장 억제요인

- 단편화된 API 보안 표준

- 서포트 에이전트의 「조용한 퇴사」에 의해 트레이닝 데이터를 삭감

- 소블린 클라우드에서 데이터 저장 장소의 제약

- 중소기업에서 CX 툴의 확산 비용 상승

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측(가치관)

- 배포별

- 클라우드

- On-Premise

- 하이브리드

- 제공별

- 솔루션

- 서비스

- 채널별

- 웹 포털

- 모바일 앱

- 대화형 챗봇/API

- 음성/IVR

- 기업 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- BFSI

- 헬스케어

- 소매업 및 전자상거래

- 정부

- IT 및 통신

- 교육

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 싱가포르

- 말레이시아

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Oracle Corporation

- Salesforce Inc.

- SAP SE

- Microsoft Corporation

- Zendesk Inc.

- Verint Systems Inc.

- NICE Ltd.

- Genesys Telecommunications Laboratories Inc.

- Freshworks Inc.

- ServiceNow Inc.

- Atlassian Corporation(Jira Service Management)

- HubSpot Inc.

- Intercom Inc.

- Pega Systems Inc.

- Zoho Corporation Pvt. Ltd.

- Zappix Inc.

- Ada Support Inc.

- LivePerson Inc.

- Richpanel Technologies Pvt. Ltd.

- Help Scout PBC

- Drift.com Inc.

- WalkMe Ltd.

- Kustomer LLC

- RingCentral Inc.

- Avaya Inc.

- BMC Software Inc.

제7장 시장 기회와 미래 동향

- 백스페이스와 미충족 요구의 평가

The Customer Self-Service Software Market size is estimated at USD 22.08 billion in 2025, and is expected to reach USD 56.11 billion by 2030, at a CAGR of 20.5% during the forecast period (2025-2030).

The growth reflects a shift toward autonomous engagement models in which conversational AI, cloud deployment, and hyper-personalised workflows reduce wait times and trim operating costs. Vendors offering integrated platforms rather than narrow point tools earn preference, while small and mid-sized enterprises (SMEs) accelerate adoption as subscription pricing removes large capital outlays. Conversational interfaces attract sustained investment because they align with consumer expectations for natural, on-demand help. Regional funding patterns reinforce overall momentum as North American enterprises pursue optimisation projects and Asia-Pacific companies deploy first-wave systems to serve mobile-centric customers.

Global Customer Self-Service Software Market Trends and Insights

Cloud-first CX Transformation Wave

Enterprises migrating to cloud-native customer experience stacks report 40-60% cost reductions and round-the-clock availability, results that encourage further investment in the customer self-service software market. Near-instant data synchronisation across touchpoints lets agents and bots access complete history, which raises first-contact resolution rates. SMEs gain the most because subscription models avoid up-front capital requirements. Nevertheless, multi-region data residency rules complicate rollouts and reward vendors with strong migration support.

AI-powered Self-service Maturity Curves

Generative AI now interprets intent, retrieves records, and executes multi-step workflows, letting automated portals resolve up to 80% of common queries. Companies that embed large language models inside ticketing flows register higher net-promoter scores and free staff to handle exceptions. As accuracy improves, the customer self-service software market will transition from handling routine FAQs to completing high-value, regulated transactions.

Fragmented API Security Standards

Mismatched token protocols and inconsistent encryption raise integration costs, slowing deployments in the customer self-service software market. Highly regulated verticals must align CRM, ERP, and knowledge-base connections under one security model, and gaps expose new vulnerability surfaces. Vendors answering this pain point with pre-certified connectors gain traction.

Other drivers and restraints analyzed in the detailed report include:

- Hyper-personalisation via Customer Data Platforms

- Rising Self-service Adoption by Gen-Z Consumers

- Data Residency Constraints in Sovereign Clouds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud segment commanded 58.7% customer self-service software market share in 2024 and is forecast to maintain a 22.1% CAGR through 2030. Its rise adds scale elasticity, enabling global releases without data-centre expansion. Subscription pricing trims up-front investment and lets finance teams recognise expenses as operating outlays. Vendors continue to enrich offerings with built-in analytics that surface deflection rates and user sentiment.

Hybrid frameworks persist where sovereignty rules block SaaS in sensitive jurisdictions, while fully on-premise stacks remain concentrated in government agencies. Firms migrating from on-premises commonly adopt phased rollouts that preserve legacy ticket records yet shift new traffic to the cloud. Lower maintenance burdens and instant patching further cement the appeal, reinforcing the customer self-service software market trajectory.

End-to-end suites held 62.3% of revenue in 2024, revealing buyer desire for unified hubs that blend knowledge bases, chatbots, and analytics. The services category will grow at 21.6% CAGR as enterprises need configuration, training, and periodic optimisation. Implementation partners craft industry playbooks that map workflows and govern role-based access, guiding firms through change-management hurdles.

Vendors extend value with packaged accelerators-pre-built templates that align to ITIL processes or retail order-status flows. Continuous-improvement engagements keep modules tuned, avoiding drift between evolving business rules and bot intents. These professional-service layers deepen platform stickiness and enlarge the customer self-service software market size attached to each deployment.

Customer Self-Service Software Market is Segmented by Deployment (Cloud, On-Premise, and Hybrid), Offering (Solution and Service), Channel (Web Portal, Mobile App, and More), Enterprise Size (Large Enterprises and Small and Mid-Sized Enterprises), End-User Industry (BFSI, Healthcare, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 34.2% of 2024 revenue, supported by high cloud penetration, mature omnichannel strategies, and a tech workforce skilled in AI model tuning. Many enterprises completed first-wave deployments and now focus on fine-tuning journeys using deeper analytics. Federal-level attention to cybersecurity nudges agencies and contractors toward platforms meeting zero-trust mandates, sustaining replacement cycles.

Asia-Pacific represents the fastest expansion vector with a projected 21.7% CAGR through 2030. Its mobile-first consumer base, dominated by Gen-Z cohorts, demands chatbots that understand local dialects and karaoke-style transliteration. Governments sponsor SME digitalisation grants, indirectly enlarging demand for the customer self-service software market across retail, travel, and banking. Vendors with multilingual NLP pipelines differentiate in these environments.

Europe advances steadily despite stringent privacy statutes. The emergence of sovereign-cloud frameworks spurs regional data-centre builds, ensuring compliance. Enterprise buyers scrutinise audit capabilities and consent management before green-lighting rollouts, effectively raising the competitive bar. Although regulatory overhead tempers speed, once solutions prove compliant, adoption spreads quickly across adjacent departments, securing long-run stability.

- Oracle Corporation

- Salesforce Inc.

- SAP SE

- Microsoft Corporation

- Zendesk Inc.

- Verint Systems Inc.

- NICE Ltd.

- Genesys Telecommunications Laboratories Inc.

- Freshworks Inc.

- ServiceNow Inc.

- Atlassian Corporation (Jira Service Management)

- HubSpot Inc.

- Intercom Inc.

- Pega Systems Inc.

- Zoho Corporation Pvt. Ltd.

- Zappix Inc.

- Ada Support Inc.

- LivePerson Inc.

- Richpanel Technologies Pvt. Ltd.

- Help Scout PBC

- Drift.com Inc.

- WalkMe Ltd.

- Kustomer LLC

- RingCentral Inc.

- Avaya Inc.

- BMC Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first CX transformation wave

- 4.2.2 AI-powered self-service maturity curves

- 4.2.3 Hyper-personalisation via customer data platforms

- 4.2.4 Rising self-service adoption by Gen-Z consumers

- 4.2.5 Embedded self-service in vertical SaaS "layer-cake"

- 4.2.6 Cyber-insurance premium incentives for self-service

- 4.3 Market Restraints

- 4.3.1 Fragmented API security standards

- 4.3.2 "Quiet quit" of support agents lowering training data

- 4.3.3 Data residency constraints in sovereign clouds

- 4.3.4 Rising CX tool sprawl cost for SMEs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.1.3 Hybrid

- 5.2 By Offering

- 5.2.1 Solution

- 5.2.2 Service

- 5.3 By Channel

- 5.3.1 Web Portal

- 5.3.2 Mobile App

- 5.3.3 Conversational Chatbot/API

- 5.3.4 Voice/IVR

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-Sized Enterprises (SMEs)

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 Retail and E-commerce

- 5.5.4 Government

- 5.5.5 IT and Telecommunication

- 5.5.6 Education

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Singapore

- 5.6.4.6 Malaysia

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 Salesforce Inc.

- 6.4.3 SAP SE

- 6.4.4 Microsoft Corporation

- 6.4.5 Zendesk Inc.

- 6.4.6 Verint Systems Inc.

- 6.4.7 NICE Ltd.

- 6.4.8 Genesys Telecommunications Laboratories Inc.

- 6.4.9 Freshworks Inc.

- 6.4.10 ServiceNow Inc.

- 6.4.11 Atlassian Corporation (Jira Service Management)

- 6.4.12 HubSpot Inc.

- 6.4.13 Intercom Inc.

- 6.4.14 Pega Systems Inc.

- 6.4.15 Zoho Corporation Pvt. Ltd.

- 6.4.16 Zappix Inc.

- 6.4.17 Ada Support Inc.

- 6.4.18 LivePerson Inc.

- 6.4.19 Richpanel Technologies Pvt. Ltd.

- 6.4.20 Help Scout PBC

- 6.4.21 Drift.com Inc.

- 6.4.22 WalkMe Ltd.

- 6.4.23 Kustomer LLC

- 6.4.24 RingCentral Inc.

- 6.4.25 Avaya Inc.

- 6.4.26 BMC Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment