|

시장보고서

상품코드

1850359

고객 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Customer Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

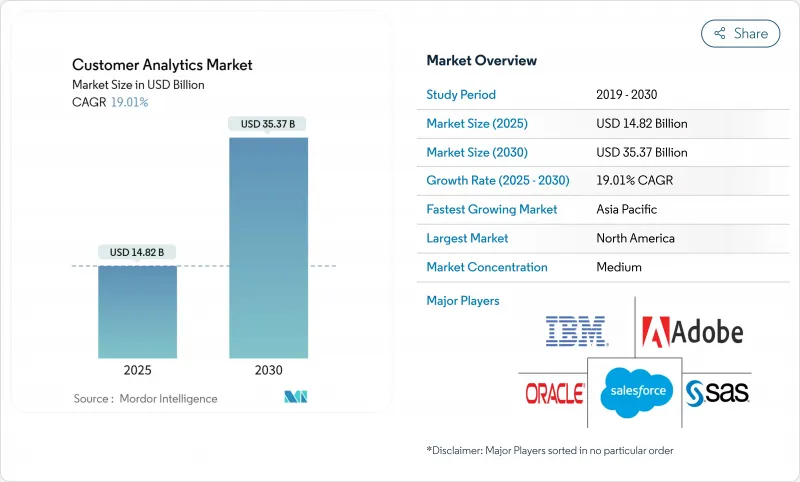

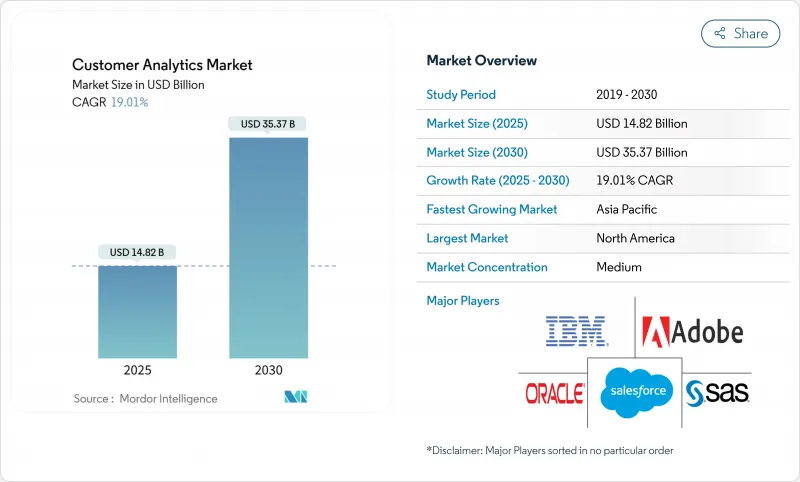

고객 분석 시장 규모는 2025년에 148억 2,000만 달러로 2030년에는 353억 7,000만 달러에 이를 것으로 예상되며, CAGR은 19.01%를 나타낼 전망입니다.

엔터프라이즈가 데이터 중심의 참여로 축 발을 옮기고 비용이 많이 드는 대량 마케팅을 대체하고 단편화된 디지털 터치 포인트를 동기화하면 도입이 가속화됩니다. 기업은 자본 지출을 회피할 수 있는 확장성이 높은 종량 과금 모델을 선호하기 때문에 클라우드 배포가 주요 아키텍처임에 변함이 없지만, 한편으로 조직이 자동화된 인사이트 생성을 요구하는 가운데 AI를 활용한 모듈이 지지를 모으고 있습니다. 소매업 뿐만 아니라 애널리틱스가 컴플라이언스 및 개인화된 케어 제공을 지원하는 헬스케어 등 규제가 엄격한 분야로의 업종별 확대도 계속되고 있습니다. 플랫폼 공급업체가 기존 용도에 애널리틱스를 통합하여 고객을 둘러싸고 소규모 전문 기업에 대한 점유율을 보호하기 때문에 경쟁이 치열해지고 있습니다. 동시에 데이터 주권에 대한 규제와 인력 부족으로 인해 기업은 아키텍처 재구성과 외부 전문가의 활용을 강요하고 단기적인 사업 확대에는 멈춤이 없어집니다.

세계의 고객 분석 시장 동향과 인사이트

하이퍼 맞춤형 고객 경험에 대한 수요 증가

획득 비용이 상승함에 따라 기업은 보존을 우선시해야 하며, 개인화는 마케팅 목표에서 핵심 경영 원칙으로 승화하고 있습니다. Adobe는 소비자의 71%가 브랜드 요구사항을 미리 읽고 싶어했음에도 불구하고 이를 대규모로 실현하는 기업은 40% 미만임을 밝혔습니다. 스트리밍 제공업체는 그 영향을 보여줍니다. Netflix는 시청자 참여의 약 80%를 실시간 행동 신호에 적응하는 데이터 구동 추천 엔진에 기인한다고 합니다. 접객 사업자는 이 변화를 반영하고 있으며, 10개에 9개 근처의 호텔이 AI에 의해 강화된 게스트 인터랙션을 도입하고 있으며, 프리미엄 숙박 요금을 획득하고 있습니다. 인사이트의 질과 수익 향상과의 연관성은 고급 세분화, 추세 모델링, 차선책 엔진에 대한 산업 횡단 투자를 촉진하고 고객 분석 시장 전체의 성장을 가속하고 있습니다.

클라우드 네이티브 애널리틱스는 중소기업 TCO 감소

중소기업에서는 구독 모델을 통해 엄청난 설비 투자가 필요 없으며 도입 주기가 단축되므로 클라우드 서비스 채택이 증가하고 있습니다. 미국의 조사에 따르면 많은 중소기업의 연간 기술 지출은 1만-4만 9,000달러이며, 확장 가능한 종량 과금 분석은 경제적으로 매력적입니다. 퍼블릭 클라우드 제공업체는 2028년까지 지출액이 1조 달러 이상에 달할 것으로 예상하고, 엔터프라이즈 아키텍트는 2025년까지 새로운 워크로드의 85%가 클라우드 우선 원칙을 준수한다고 보고했습니다. 유럽의 중견기업에서는 40%가 디지털 프로젝트의 장벽으로 재무적 불안을 꼽고 있으며, 클라우드 플랫폼은 고정비를 영업비용으로 전환함으로써 이 갭을 메우고 있습니다.

데이터 주권에 관한 법률이 세계 전개를 분단

각국 정부는 개인 데이터의 보관과 국경을 넘는 전송에 대한 관리를 강화하고 있으며, 다국적 기업은 지역 고유의 스택과 중복된 데이터 파이프라인의 구축을 강요하고 있습니다. 미국 사법부는 우려되는 국가에 의한 미국의 기밀 데이터에 대한 액세스를 차단하는 규칙을 제정하고 이 변화를 예증합니다. 조직 아키텍트는 GDPR(EU 개인정보보호규정), 클라우드 법 및 APAC의 다양한 거주 의무와 균형을 맞추어야 하며, 종종 집중 처리가 아닌 현지화 처리를 선택합니다. 이는 통합 고객 뷰 프로젝트를 지연시키고 복잡한 운영 모델에서 고객 분석 시장 채택을 지연시킵니다.

부문 분석

클라우드 솔루션은 2024년 매출의 62%를 차지했고, 2030년까지의 CAGR은 21.40%를 나타낼 것으로 예측됩니다. 종종 클라우드 도입 시장 세분화 시장 규모는 부문 수준에서 2030년까지 250억 달러 이상에 달할 것으로 예상됩니다. 금융기관이나 공공기관에서는 대기 시간과 레지던시를 엄격하게 관리하는 On-Premise 환경이 뿌리 깊게 남아 있지만, 한편, 기밀 데이터를 로컬로 유지하면서 부하가 높은 계산을 퍼블릭 클라우드에 맡기는 하이브리드 접근법에 투자가 집중되고 있습니다. Microsoft는 2025년 3분기 Azure의 성장률을 35%로 보고했으며, 증분의 거의 절반은 실시간 세분화 및 추세 모델링을 가능하게 하는 AI 서비스 때문입니다. Oracle의 AWS와의 멀티클라우드 계약은 유연한 애널리틱스 마이그레이션 경로를 추구하는 기업 수요를 충족시키기 위해 이전에 라이벌 관계에 있던 플랫폼이 어떻게 상호 연결되는지 보여줍니다.

클라우드로 전환한 기업은 실험주기의 가속화에 주목하고 있습니다. 데이터 팀은 샌드박스 환경을 몇 분 안에 시작하고 모델 검증이 완료되면 해당 환경을 해제합니다. 구독 가격은 대량의 선행 투자를 운영 비용으로 전환하므로 특히 중소기업의 경우 예산 승인이 용이합니다. 공급업체가 업계 고유의 컴플라이언스 설계도를 도입함에 따라 규제 대상 분야에서 분석 워크로드의 전환이 진행됨에 따라 고객 분석 시장이 더욱 확대되고 있습니다.

대시보드 보고 소프트웨어는 2024년 매출의 27%를 차지했습니다. 그러나 AI를 활용한 모듈은 2030년까지 연평균 복합 성장률(CAGR) 24.60%로 확대되어 고객 분석 시장에서 가장 급성장하고 있는 레이어로 자리매김하고 있습니다. 이러한 엔진은 피처 엔지니어링, 모델 선택 및 시나리오 분석을 자동화하여 원시 데이터에서 실용적인 인사이트까지의 경로를 단축합니다. Adobe는 2024년 53억 7,000만 달러를 창출하기 위해 디지털 경험 제품군 전체에 생성형 AI를 통합했습니다.

고객의 목소리, 소셜 미디어 및 웹 분석 용도는 특수한 이용 사례를 계속 개척하고 있지만, 스키마, 동의, 정체성 해결을 중앙 집중화하는 보다 광범위한 고객 데이터 플랫폼의 산하로 수렴하고 있습니다. ETL 툴은 배치 통합에서 피처 스토어를 몇 초 안에 새로 고침하는 실시간 파이프라인으로 진화하여 컨텐츠 엔진과 가격 엔진이 라이브 참여 도중 고객 컨텍스트에 반응할 수 있도록 합니다. 이러한 흐름 내에서 데이터 품질과 거버넌스를 직접 자동화하는 공급업체는 개인정보 보호에 대한 모니터링이 강화되는 동안 강력한 차별화를 도모할 수 있습니다.

고객 분석 시장은 도입 유형(On-Premise형, 클라우드 기반), 솔루션(소셜 미디어 분석 도구, 웹 분석 도구 등), 조직 규모(중소기업, 대기업), 서비스(관리 서비스, 전문 서비스), 최종 사용자 산업(통신 및 IT, 여행 및 호스피탈리티 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 클라우드의 깊은 침투, 성숙한 데이터 사이언스 인력 풀, 2024년 AI 벤처 기업에 대한 1,091억 달러 이상의 강력한 벤처 자금으로 지출을 지배했습니다. 벤더는 미국과 캐나다에 흩어져 있는 고밀도 데이터센터를 활용하여 실시간 개인화 캠페인을 위한 저지연 추론을 제공합니다. 규제 정책은 상대적으로 유연하지만, 국가 수준의 프라이버시 보호법에는 지역별 동의 관리가 필요합니다. 멕시코의 신흥 전자상거래 생태계는 소매업체가 옴니채널 구매자의 행동에 대한 인사이트를 요구하기 때문에 수요가 증가하고 있습니다.

유럽에서는 조직이 GDPR(EU 개인정보보호규정)을 준수하고 프라이버시 바이 디자인 분석 프레임 워크의 도입을 추진하고 있습니다. 독일과 영국은 제조업과 금융서비스의 현대화에 힘입어 도입을 선도하고 프랑스와 이탈리아는 정부의 지원을 받아 디지털 프로그램을 가속화하고 있습니다. 데이터 현지화가 의무화됨에 따라 공급업체는 다중 리전 클러스터의 운영을 강요하고 운영 비용이 증가하면서 프라이버시에 민감한 고객으로부터의 신뢰가 높아지고 있습니다. 신뢰할 수 있는 클라우드 라벨과 보안 애널리틱스 샌드박스를 둘러싼 EU의 노력은 아키텍처 결정에 더욱 영향을 미칩니다.

APAC는 가장 급성장하는 지역으로 기업의 43%가 향후 1년간 AI 예산의 20% 이상 증가할 계획입니다. 중국은 현지 규제에 대응하기 위해 국내 대규모 언어 모델의 규모를 확대하고 있으며, 서양 플랫폼과는 다른 병렬 생태계를 촉구하고 있습니다. 인도의 BFSI와 통신 섹터는 모바일 퍼스트 사용자에게 도달하기 위해 데이터 플랫폼에 많은 투자를 합니다. 일본과 한국은 옴니채널 소매 분석을 중시하고 호주는 강력한 클라우드 인프라와 유리한 환율을 배경으로 꾸준한 성장을 유지하고 있습니다. 전반적으로 지역 AI 지출은 2028년까지 1,100억 달러를 초과할 수 있어 고객 분석 시장의 견조한 확대를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이퍼 개인화된 CX(주류) 수요가 증가

- 클라우드 네이티브 분석에 의해 중소기업의 TCO가 삭감(주류)

- AI를 활용한 셀프서비스 분석으로 인사이트를 민주화(주류)

- 고객 데이터 플랫폼은 마케팅 기술 제품군에 번들(주류)

- 소매 미디어 네트워크가 퍼스트 파티 데이터 파이프를 개설(잠재적)

- SaaS 워크플로우 내의 내장 분석(잠재적)

- 시장 성장 억제요인

- 데이터 주권법은 세계의 전개를 분단(주류)

- 구성 가능한 데이터 제품 인력 부족(주류)

- 섀도우 IT의 만연에 의해 고객 ID가 중복되어 생성(잠재적)

- 써드파티 쿠키 폐지에 의한 광고 기술의 시그널 손실(잠재적)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 강도

제5장 시장 규모와 성장 예측

- 배포 유형별

- On-Premise

- 클라우드 기반

- 솔루션별

- 소셜 미디어 분석 도구

- 웹 분석 도구

- 대시보드 및 보고 도구

- 고객의 목소리(VoC)

- ETL(추출-변환-로드)

- 고급 분석 모듈

- 기업 규모별

- 중소기업

- 대기업

- 최종 사용자 업계별

- 통신 및 IT

- 여행 및 접객

- 소매

- BFSI

- 미디어 및 엔터테인먼트

- 헬스케어

- 운송 및 물류

- 제조업

- 기타 산업

- 서비스별

- 관리형 서비스

- 전문 서비스

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Adobe

- Alteryx

- Angoss Software Corp.

- Axtria

- Bridgei2i(Accenture)

- IBM

- Manthan Software

- Microsoft

- NGDATA

- Oracle

- Pitney Bowes

- Salesforce

- SAS Institute

- TEOCO

- Aruba Networks(HPE)

제7장 시장 기회와 향후 전망

KTH 25.11.10The customer analytics market size is valued at USD 14.82 billion in 2025 and is forecast to climb to USD 35.37 billion by 2030, advancing at a 19.01% CAGR.

Adoption accelerates as enterprises pivot toward data-driven engagement, replace high-cost mass marketing, and synchronize fragmented digital touchpoints. Cloud deployment remains the primary architecture because firms prefer scalable pay-as-you-go models that avoid capital outlays, while AI-augmented modules gain traction as organizations demand automated insight production. Vertical expansion continues beyond retail into highly regulated sectors such as healthcare, where analytics supports compliance and personalised care delivery. Competitive intensity rises as platform vendors embed analytics inside existing applications to lock in customers and defend share against smaller specialists. At the same time, data-sovereignty regulations and talent shortages temper short-term expansion by forcing businesses to re-engineer architectures and source external expertise.

Global Customer Analytics Market Trends and Insights

Rising Demand for Hyper-Personalised Customer Experience

Escalating acquisition costs force firms to prioritise retention, elevating personalisation from marketing goal to core operating principle. Adobe found 71% of consumers expect brands to anticipate needs, yet fewer than 40% of companies deliver at scale. Streaming providers illustrate impact: Netflix attributes roughly 80% of viewer engagement to its data-driven recommendation engine that adapts to real-time behavioural signals. Hospitality operators mirror this shift, with nearly nine in 10 hotels deploying AI-enhanced guest interactions that command premium room rates. The linkage between insight quality and revenue uplift encourages cross-industry investment in advanced segmentation, propensity modelling and next-best-action engines, fuelling growth across the customer analytics market.

Cloud-Native Analytics Lowers TCO for SMEs

Small and medium enterprises increasingly adopt cloud services because subscription models remove large capital outlays and shorten deployment cycles. US surveys show annual technology spending for many SMEs falls between USD 10,000 and USD 49,000, making scalable pay-per-use analytics financially attractive. Public cloud providers anticipate spending to top USD 1 trillion by 2028, and enterprise architects report that 85% of new workloads will follow cloud-first principles by 2025. For European mid-sized firms, 40% cite financial uncertainty as a barrier to digital projects-a gap that cloud platforms close by converting fixed costs into operating expenses.

Data-Sovereignty Laws Fragment Global Rollouts

Governments tighten control over personal data storage and cross-border transfers, forcing multinationals to build region-specific stacks and duplicate data pipelines. The US Department of Justice rule blocking access to sensitive American data by countries of concern exemplifies this shift and adds compliance overhead starting April 2025. Organisational architects must balance GDPR, the Cloud Act and divergent APAC residency mandates, often choosing to localise processing rather than centralise, which delays unified customer-view projects and slows customer analytics market adoption in complex operating models.

Other drivers and restraints analyzed in the detailed report include:

- AI-Augmented Self-Service Analytics Democratises Insights

- Customer Data Platforms Bundled into Mar-Tech Suites

- Shortage of Composable Data-Product Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions account for 62% of 2024 revenue and are projected to grow at a 21.40% CAGR through 2030 as firms prefer elastic scaling and reduced maintenance overhead. In many cases the customer analytics market size for cloud deployments is expected to exceed USD 25 billion by 2030 at segment level. On-premises environments persist in finance and public-sector contexts that enforce tight latency or residency controls, yet investment concentrates on hybrid approaches that keep sensitive data local while offloading heavy computation to public clouds. Microsoft reported Azure growth of 35% in Q3 2025, attributing almost half the incremental revenue to AI services that power real-time segmentation and propensity modelling. Oracle's multicloud pact with AWS demonstrates how previously rival platforms now interconnect to meet enterprise demand for flexible analytics migration paths.

Enterprises that shift to cloud note faster experimentation cycles: data teams spin up sandbox environments within minutes and de-commission them once models are validated, a process that once required weeks of procurement and installation when hardware was on-premises. Subscription pricing converts large upfront investments into operational expense, easing budget approvals especially for SMEs. As vendors introduce industry-specific compliance blueprints, regulated sectors increasingly migrate analytical workloads, further broadening the customer analytics market.

Dashboard and reporting software still represents 27% of 2024 revenue because visual summaries remain the gateway for non-technical managers. Yet AI-augmented modules are expanding at a 24.60% CAGR to 2030, positioning them as the fastest-growing layer of the customer analytics market. These engines automate feature engineering, model selection and scenario analysis, thereby shortening the path from raw data to actionable insight. Adobe integrated generative AI across its Digital Experience suite and generated USD 5.37 billion in 2024, validating appetite for embedded intelligence.

Voice-of-Customer, social-media and web-analytical applications continue carving out specialised use cases, but they are converging under broader customer-data-platform umbrellas that centralise schema, consent and identity resolution. ETL tools evolve from batch integrations into real-time pipelines that refresh feature stores in seconds, enabling content and pricing engines to react to customer context during live engagements. Suppliers that automate data quality and governance directly within these flows differentiate strongly amid growing privacy scrutiny.

Customer Analytics Market is Segmented by Deployment Type (On-Premises and Cloud-Based), Solution (Social-Media Analytical Tools, Web Analytical Tools and More), Organization Size (SMEs, Large Enterprises), Service (Managed Service, Professional Service), End-User Industry (Telecommunications and IT, Travel and Hospitality and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominates spending owing to deep cloud penetration, mature data-science talent pools and strong venture funding that topped USD 109.1 billion for AI start-ups in 2024. Vendors leverage dense data-centre footprints across the United States and Canada to deliver low-latency inference for real-time personalisation campaigns. Regulatory policy remains comparatively flexible, though state-level privacy acts require region-specific consent controls. Mexico's emerging e-commerce ecosystems create incremental demand as retailers seek insight into omnichannel buyer behaviour.

Europe follows closely as organisations comply with GDPR, driving uptake of privacy-by-design analytics frameworks. Germany and the United Kingdom lead adoption, supported by manufacturing and financial-services modernisation, while France and Italy accelerate digital programmes through government-backed stimulus. Data-localisation mandates compel vendors to operate multi-region clusters, increasing operating costs yet boosting trust among privacy-sensitive customers. EU initiatives around trusted-cloud labels and secure analytics sandboxes further influence architectural decisions.

APAC represents the fastest-expanding region, with 43% of enterprises planning >20% AI budget increases over the coming year. China scales domestic large-language models to serve local regulations, prompting parallel ecosystems distinct from Western platforms. India's BFSI and telecom sectors invest heavily in data platforms to reach mobile-first users. Japan and South Korea emphasise omnichannel retail analytics, and Australia maintains steady growth on the back of strong cloud infrastructure and favourable currency trends. Overall, regional AI expenditure could exceed USD 110 billion by 2028, sustaining robust expansion of the customer analytics market.

- Adobe

- Alteryx

- Angoss Software Corp.

- Axtria

- Bridgei2i (Accenture)

- IBM

- Manthan Software

- Microsoft

- NGDATA

- Oracle

- Pitney Bowes

- Salesforce

- SAS Institute

- TEOCO

- Aruba Networks (HPE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for hyper-personalised CX (mainstream)

- 4.2.2 Cloud-native analytics lowers TCO for SMEs (mainstream)

- 4.2.3 AI-augmented self-service analytics democratises insights (mainstream)

- 4.2.4 Customer Data Platforms bundled into mar-tech suites (mainstream)

- 4.2.5 Retail media networks opening first-party data pipes (under-the-radar)

- 4.2.6 Embedded analytics inside SaaS workflows (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Data-sovereignty laws fragment global roll-outs (mainstream)

- 4.3.2 Shortage of composable data-product talent (mainstream)

- 4.3.3 Shadow-IT sprawl creates duplicate customer IDs (under-the-radar)

- 4.3.4 Ad-tech signal loss after third-party cookie deprecation (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud-based

- 5.2 By Solution

- 5.2.1 Social-Media Analytical Tools

- 5.2.2 Web Analytical Tools

- 5.2.3 Dashboard and Reporting Tools

- 5.2.4 Voice of Customer (VoC)

- 5.2.5 ETL (Extract-Transform-Load)

- 5.2.6 Advanced Analytical Modules

- 5.3 By Organisation Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Telecommunications and IT

- 5.4.2 Travel and Hospitality

- 5.4.3 Retail

- 5.4.4 BFSI

- 5.4.5 Media and Entertainment

- 5.4.6 Healthcare

- 5.4.7 Transportation and Logistics

- 5.4.8 Manufacturing

- 5.4.9 Other Industries

- 5.5 By Service

- 5.5.1 Managed Service

- 5.5.2 Professional Service

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Israel

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 UAE

- 5.6.5.1.4 Turkey

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Presence, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adobe

- 6.4.2 Alteryx

- 6.4.3 Angoss Software Corp.

- 6.4.4 Axtria

- 6.4.5 Bridgei2i (Accenture)

- 6.4.6 IBM

- 6.4.7 Manthan Software

- 6.4.8 Microsoft

- 6.4.9 NGDATA

- 6.4.10 Oracle

- 6.4.11 Pitney Bowes

- 6.4.12 Salesforce

- 6.4.13 SAS Institute

- 6.4.14 TEOCO

- 6.4.15 Aruba Networks (HPE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis