|

시장보고서

상품코드

1850371

필드 서비스 관리(FSM) 시장 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2025-2030년)Field Service Management (FSM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

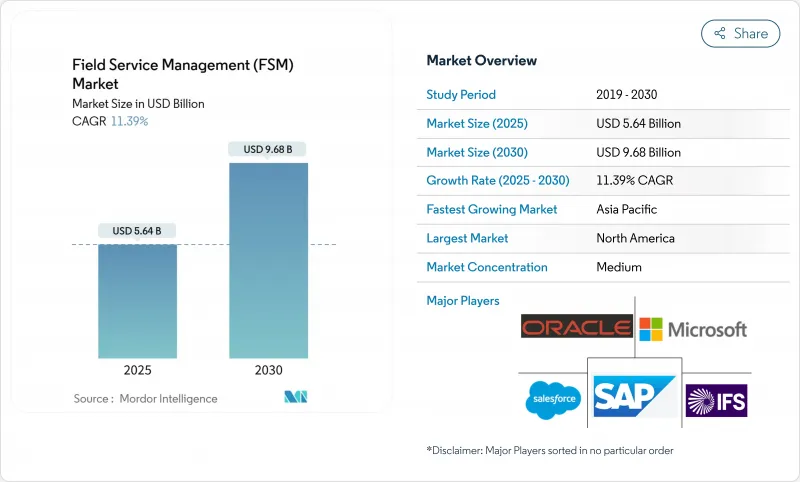

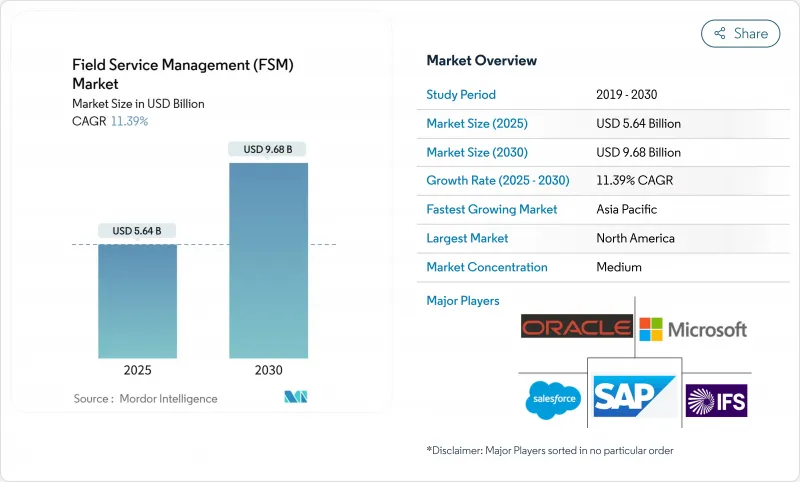

필드 서비스 관리 시장 규모는 2025년 56억 4,000만 달러로 추정되고, CAGR 11.39%로 성장할 전망이며, 2030년까지 96억 8,000만 달러로 확대될 것으로 예측됩니다.

성장의 배경에는 AI를 활용한 스케줄링, IoT를 활용한 예지보전, 5G를 활용한 커넥티비티의 급속한 도입이 있으며, 이들은 공동으로 서비스 사이클 시간을 단축하고 최초 수리율을 향상시킵니다. 조직은 유연성, 자본 비용 절감, 쉬운 통합을 보장하기 위해 워크로드를 클라우드로 이행하는 반면, 고급 분석은 기술자 파견 및 재고 계획을 재구성합니다. 공급업체는 파트너 에코시스템을 확장하고, 구현 서비스 및 업계 고유의 확장 기능을 가속화하며, 소프트웨어 및 서비스 제공업체 모두에 새로운 수익 풀을 열고 있습니다. 또한 필드 서비스 관리 시장은 Equipment-as-a-Service와 같은 일회성 제품 판매를 장기적인 서비스 계약으로 전환하고 고객과의 관계를 고정화하는 경상 수익 모델에서도 이익을 얻고 있습니다.

세계의 필드 서비스 관리(FSM) 시장 동향 및 인사이트

유틸리티 및 통신 사업에서 실시간 기술자 시각화의 요구

유틸리티 사업자 및 통신 사업자는 정전 시간을 단축하고 고객의 기대에 부응할 필요가 있습니다. 위치 정보, 작업 상태 및 자산 데이터를 실시간으로 전달하는 현장 플랫폼은 의사 결정주기를 단축하고 실시간 전개에서 30-40%의 시간을 절약합니다. IoT 지원 상태 모니터링은 실제 고장 위험에 우선순위를 부여하여 트랙 롤을 줄이고 통합 모바일 앱은 체크리스트, 회로도 및 부품 재고 상태를 현장에서 표시합니다. 송전망의 현대화 계획 및 광섬유 업그레이드는 서비스를 필요로 하는 자산 포인트를 증가시켜 보다 광범위한 전개를 강화할 것입니다.

현장의 복잡성을 높이는 대규모 5G 전개

5G의 매크로셀과 스몰셀의 고밀도화는 네트워크 요소를 증가시켜 루트 계획 및 예비 부품 관리를 더욱 복잡하게 만듭니다. 텔레콤의 현장 팀은 현재 설치하는 것과 동일한 5G 회선을 통해 고해상도 비디오 지원 및 AR 오버레이에 액세스하여 젊은 기술자가 원격 전문가의 지도를 받으면서 고급 작업을 처리할 수 있게 되었습니다. 커버리지가 가속됨에 따라 통신 사업자는 지역별로 수천 개의 사이트를 지휘하고 외주 승무원과 사내 직원의 균형을 맞출 수 있는 필드 서비스 관리 시장 솔루션을 찾고 있습니다.

공공 부문의 사이버 보안 및 데이터 주권 장벽

유틸리티, 운송기관, 의료 제공자는 업무 데이터를 국경 내에서 관리하며, 엄격한 위반 통지법을 준수해야 합니다. 유럽 데이터 거버넌스법(European Data Governance Act)과 같은 프레임워크에서는 현지화 및 관리 증명이 의무화되어 클라우드 FSM의 도입이 지연되는 경우가 많습니다. 지역 전문 호스팅, 세밀한 액세스 제어 및 인증된 암호화 기능을 갖춘 공급업체는 이러한 장애물을 가장 빠르게 극복할 수 있습니다.

부문 분석

2024년 필드 서비스 관리 시장의 57%는 온프레미스가 차지하며, 이는 대기업의 썬크 인프라와 엄격한 데이터 관리 정책을 반영합니다. 온프레미스 도입과 관련된 필드 서비스 관리 시장 규모는 기존 시설의 유지보수가 10년 내내 지속되기 때문에 완만하지만 여전히 확대될 것으로 보입니다.

그러나 클라우드 플랫폼은 CAGR 14.2%로 성장하고 있으며, 대부분의 새로운 프로젝트를 획득하고 있습니다. 시작 비용 절감, 신속한 프로비저닝 및 기능 자동 업데이트는 모바일 워크포스를 확장하는 조직에 매력적입니다. API가 풍부한 환경은 CRM, ERP, IoT 스택과의 통합을 간소화하고 점차 맞춤형 온프레미스 사용자 정의를 구축하고 있습니다.

대기업은 세계 서비스 거점과 복잡한 다중 브랜드 자산 포트폴리오를 보유하기 때문에 2024년 매출의 66%를 차지했습니다. 이러한 기업들은 기본적인 스케줄링 위에 필드 서비스 관리 시장 분석을 거듭하여 지역 전체에서 지속적인 개선을 추진하는 경우가 많습니다.

중소기업은 CAGR 13.5%에서 가장 급성장하고 있는 코호트입니다. 합리적인 가격의 SaaS 에디션과 가이드 온보딩이 도입을 용이하게 합니다. 핵심 작업 지시 흐름이 성숙하면 중견 기업은 IoT 원격 측정과 고객 포털을 추가하고 출장 감소 및 청구 주기를 가속화함으로써 ROI를 증명하면서 필드 서비스 관리 시장 규모를 확대합니다.

필드 서비스 관리 시장은 전개 모드별(온프레미스, 클라우드), 조직 규모별(대기업, 중소기업), FSM 솔루션 및 서비스 유형별(솔루션, 서비스), 최종 사용자 산업별(시설 관리(하드 FM 및 소프트 FM), IT 및 통신, 기타), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년 세계 매출의 34%를 차지했으며, 조기 도입 기업과 발달한 파트너 에코시스템에 지지를 받고 있습니다. 서비스 제공업체는 노동력 부족에 직면하고 있으며, 건설 직원의 4분의 1이 55세를 넘어서 AI 스케줄링과 계약자 마켓플레이스에 대한 수요가 증가하고 있습니다. 또한 북미에서 호스팅되는 SaaS 환경을 표준화하고 거버넌스를 중앙 집중화하는 기업이 늘어나면서 클라우드 채택도 증가하고 있습니다.

아시아태평양은 CAGR 15.2%로 확대되고 있습니다. 산업화가 진행되는 경제권에서는 임금 상승을 상쇄하기 위해 현장 작업이 디지털화되고 선진국에서는 원격지의 자산에 도달하기 위해 민간 5G와 드론이 도입됩니다. 홍콩에서는 5G-AR의 시험적 도입으로 작업 시간이 30-40% 단축되어 보다 광범위한 지역 전개를 위한 ROI가 증명되었습니다. 정부의 스마트 시티 보조금은 자산 중심의 필드 서비스 관리 시장 용도에 대한 지출을 더욱 가속화합니다.

유럽은 제조업과 유틸리티이 견인하여 큰 점유율을 차지하고 있습니다. GDPR(EU 개인정보보호규정)의 엄격한 규칙은 데이터 거주 및 암호화 요구를 증가시키고 일부 구매자를 로컬 또는 하이브리드 전개로 향하게 합니다. 또한 지속가능성의 의무화는 벤더 선정을 좌우하고 있으며, 차량의 배출량을 줄이기 위해 경로의 최적화가 중요시되고 있습니다. GAIA-X와 같은 이니셔티브는 소블린 클라우드 제공을 뒷받침하고 EU 국경을 넘어서는 필드 서비스 관리 시장의 컴플라이언스를 기반으로 확장을 가능하게 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유틸리티 및 통신 업계에서 기술자의 실시간 시각화 요구

- 대규모 5G 도입으로 현장의 복잡성 증가

- 탈탄소화의 추진으로 스마트 미터 및 EV 충전기 설치 촉진

- AI 지원 스케줄링을 가속화하는 고령화 인력

- 지속적인 수익원을 창출하는 OEM 서비스화 모델

- AR 기반의 원격 지원을 촉진하는 원격 근무의 안전 규칙

- 시장 성장 억제요인

- 공공 부문의 사이버 보안 및 데이터 주권의 장벽

- 브라운필드 플랜트에서의 레거시 ERP 및 OT 통합의 복잡성

- 중소기업용 초기 가입 및 변경 관리 비용

- 국경을 넘은 규제의 단편화가 AI의 도입 저해

- 규제 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시경제 충격의 영향(COVID-19와 공급망 포함)

- 현장 이용 사례의 진화(AR/VR, 예지 보전, 자동화)

- 구매자의 필수 사항 분석

제5장 시장 규모 및 성장 예측

- 전개 유형별

- 온프레미스

- 클라우드

- 조직 규모별

- 대기업

- 중소기업

- FSM 솔루션 및 서비스 유형별

- 솔루션

- 스케줄링, 디스패치, 루트 최적화

- 서비스 계약 관리

- 작업 지시 관리

- 고객 관리

- 재고 관리

- 기타 소프트웨어(과금, 청구서 발행, 보증)

- 서비스(통합, 구현, 지원)

- 솔루션

- 최종 사용자별

- 시설 관리(하드 FM 및 소프트 FM)

- IT 및 통신

- 헬스케어 및 생명과학

- 에너지 및 유틸리티

- 석유 및 가스

- 제조업

- 운송 및 물류

- 부동산 및 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 페루

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- Strategic Developments

- Vendor Positioning Analysis

- 기업 프로파일

- Oracle Corp.(Oracle Field Service)

- Salesforce Inc.(Field Service)

- Microsoft Corp.(Dynamics 365 Field Service)

- SAP SE(Coresystems)

- IFS AB

- ServiceMax Inc.(PTC)

- ServicePower PLC

- Trimble Inc.

- FieldAware US Inc.

- Accruent LLC(Fortive)

- Zinier Inc.

- simPRO Group Pty Ltd.

- OverIT SpA

- Praxedo SA

- KloudGin Inc.

- Jobber

- FieldEZ Technologies

- ProntoForms Corp.

- Zuper Inc.

- KloudGin Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.10The field service management market size is valued at USD 5.64 billion in 2025 and is forecast to expand to USD 9.68 billion by 2030, reflecting an 11.39% CAGR.

Growth stems from rapid adoption of AI-assisted scheduling, IoT-enabled predictive maintenance, and 5G-powered connectivity that jointly compress service cycle times and improve first-time fix rates. Organisations are shifting workloads to the cloud to secure flexibility, lower capital expense, and easier integrations, while advanced analytics reshape technician dispatch and inventory planning. Vendors are widening partner ecosystems to accelerate implementation services and industry-specific extensions, opening fresh revenue pools for both software and services providers. The field service management market also benefits from recurring revenue models such as Equipment-as-a-Service, which convert one-time product sales into long-life service contracts and lock in customer relationships.

Global Field Service Management (FSM) Market Trends and Insights

Real-time Technician Visibility Needs across Utilities And Telecom

Utilities and telecom operators are under pressure to cut outage durations and meet rising customer expectations. Field platforms that stream live location, job status, and asset data shorten decision cycles, delivering 30-40% time savings in live deployments . IoT-enabled condition monitoring reduces truck rolls by prioritising genuine failure risks, while integrated mobile apps surface checklists, schematics, and parts availability onsite. Broader roll-out is set to intensify as grid modernisation programmes and fibre upgrades multiply asset points needing service.

Large-scale 5G Roll-outs Raising Field Complexity

5G macro- and small-cell densification multiplies network elements, making route planning and spares management far more intricate. Telecom field teams now access high-definition video support and AR overlays via the same 5G links they install, letting junior technicians handle advanced tasks with remote expert guidance . As coverage accelerates, operators demand field service management market solutions that can orchestrate thousands of sites per region and balance outsourced crews with in-house staff.

Cyber-security & Data-sovereignty Barriers in Public Sector

Utilities, transport agencies, and healthcare providers must keep operational data inside national borders and comply with stringent breach-notification laws. Frameworks such as the European Data Governance Act mandate localisation and proof of control, often delaying cloud FSM deployments. Vendors with region-specific hosting, granular access controls, and certified encryption overcome these hurdles fastest.

Other drivers and restraints analyzed in the detailed report include:

- Decarbonisation Push Driving Smart-Meter & EV-Charger Installs

- Ageing Workforce Accelerating AI-assisted Scheduling

- Legacy ERP/OT Integration Complexity in Brownfield Plants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations held 57% of the field service management market in 2024, reflecting sunk infrastructure and tight data-control policies among large enterprises. The field service management market size linked to on-premise deployments will still expand, albeit slowly, as maintenance of existing estates persists through the decade.

Cloud platforms, however, are growing at a 14.2% CAGR and capture most net-new projects. Lower start-up costs, rapid provisioning, and automatic feature updates appeal to organisations scaling mobile workforces. API-rich environments simplify integration with CRM, ERP, and IoT stacks, gradually eclipsing bespoke on-premise customisations.

Large enterprises commanded 66% revenue in 2024 thanks to global service footprints and complex multi-brand asset portfolios. These accounts often layer field service management market analytics atop base scheduling to drive continuous improvement across regions.

SMEs are the fastest-growing cohort at 13.5% CAGR. Affordable SaaS editions and guided onboarding demystify adoption. Once core work-order flows mature, midsize firms add IoT telemetry and customer portals, widening the field service management market size while proving ROI through reduced travel and quicker invoice cycles.

Field Service Management Market is Segmented by Deployment Type (On-Premise, Cloud), Organization Size (Large Enterprises, Small and Medium Enterprises), FSM Solution and Service Type (Solutions, Services), End-User Vertical (Facilities Management (Hard-FM and Soft-FM), IT and Telecom, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 34% of global revenue in 2024, sustained by early adopter enterprises and well-developed partner ecosystems. Service providers face mounting labour shortages-one quarter of construction staff exceed 55 years of age, which intensifies demand for AI scheduling and contractor marketplaces. Cloud adoption also rises as enterprises standardise on North America-hosted SaaS environments to centralise governance.

Asia-Pacific is expanding at a 15.2% CAGR. Industrialising economies digitise field work to offset rising wages, while advanced nations deploy private 5G and drones to reach remote assets. In Hong Kong, a 5 G-AR pilot delivered 30-40% task-time reductions, proving ROI for broader regional roll-outs. Government smart-city grants further accelerate spending on asset-centric field service management market applications.

Europe holds a substantial share, driven by manufacturing and utilities. Strict GDPR rules elevate data-residency and encryption demands, nudging some buyers toward local or hybrid deployments. Sustainability mandates also shape vendor selection, with route optimisation prized for lowering fleet emissions. Initiatives such as GAIA-X boost sovereign-cloud offers, enabling compliant scaling of the field service management market across EU borders.

- Oracle Corp. (Oracle Field Service)

- Salesforce Inc. (Field Service)

- Microsoft Corp. (Dynamics 365 Field Service)

- SAP SE (Coresystems)

- IFS AB

- ServiceMax Inc. (PTC)

- ServicePower PLC

- Trimble Inc.

- FieldAware US Inc.

- Accruent LLC (Fortive)

- Zinier Inc.

- simPRO Group Pty Ltd.

- OverIT S.p.A.

- Praxedo SA

- KloudGin Inc.

- Jobber

- FieldEZ Technologies

- ProntoForms Corp.

- Zuper Inc.

- KloudGin Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real-time Technician Visibility Needs across Utilities and Telecom

- 4.2.2 Large-scale 5G Roll-outs Raising Field Complexity

- 4.2.3 Decarbonization Push Driving Smart-Meter and EV-Charger Installs

- 4.2.4 Ageing Workforce Accelerating AI-assisted Scheduling

- 4.2.5 OEM Servitization Models Creating Recurring Revenue Streams

- 4.2.6 Remote-work Safety Rules Fueling AR-based Remote Assistance

- 4.3 Market Restraints

- 4.3.1 Cyber-security and Data-sovereignty Barriers in Public Sector

- 4.3.2 Legacy ERP/OT Integration Complexity in Brownfield Plants

- 4.3.3 Up-front Subscription and Change-management Costs for SMEs

- 4.3.4 Cross-border Regulatory Fragmentation Hindering AI Dispatch

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Macroeconomic Shocks (incl. COVID-19 and Supply Chain)

- 4.7 Field Use-Case Evolution (AR/VR, Predictive Maintenance, Automation)

- 4.8 Buyer Imperatives Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By FSM Solution and Service Type

- 5.3.1 Solutions

- 5.3.1.1 Scheduling, Dispatch and Route Optimization

- 5.3.1.2 Service Contract Management

- 5.3.1.3 Work-order Management

- 5.3.1.4 Customer Management

- 5.3.1.5 Inventory Management

- 5.3.1.6 Other Software (Billing, Invoicing, Warranty)

- 5.3.2 Services (Integration, Implementation, Support)

- 5.3.1 Solutions

- 5.4 By End-User Vertical

- 5.4.1 Facilities Management (Hard-FM and Soft-FM)

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Energy and Utilities

- 5.4.5 Oil and Gas

- 5.4.6 Manufacturing

- 5.4.7 Transportation and Logistics

- 5.4.8 Real Estate and Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Oracle Corp. (Oracle Field Service)

- 6.3.2 Salesforce Inc. (Field Service)

- 6.3.3 Microsoft Corp. (Dynamics 365 Field Service)

- 6.3.4 SAP SE (Coresystems)

- 6.3.5 IFS AB

- 6.3.6 ServiceMax Inc. (PTC)

- 6.3.7 ServicePower PLC

- 6.3.8 Trimble Inc.

- 6.3.9 FieldAware US Inc.

- 6.3.10 Accruent LLC (Fortive)

- 6.3.11 Zinier Inc.

- 6.3.12 simPRO Group Pty Ltd.

- 6.3.13 OverIT S.p.A.

- 6.3.14 Praxedo SA

- 6.3.15 KloudGin Inc.

- 6.3.16 Jobber

- 6.3.17 FieldEZ Technologies

- 6.3.18 ProntoForms Corp.

- 6.3.19 Zuper Inc.

- 6.3.20 KloudGin Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment