|

시장보고서

상품코드

1850394

응급실 정보 시스템(EDIS) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Emergency Department Information System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

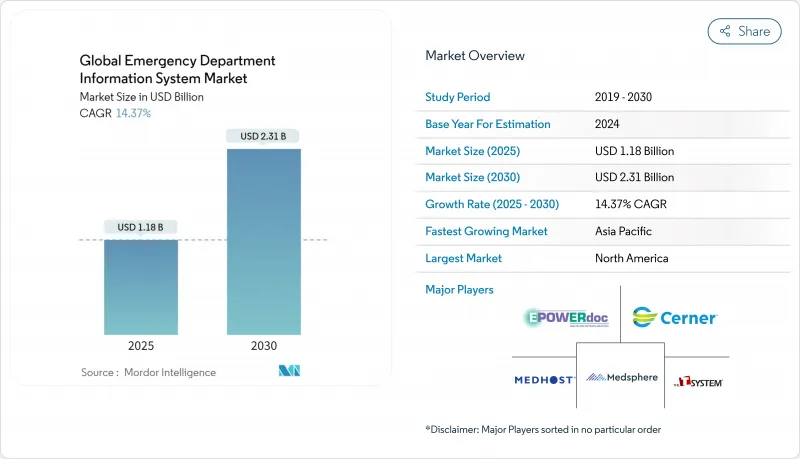

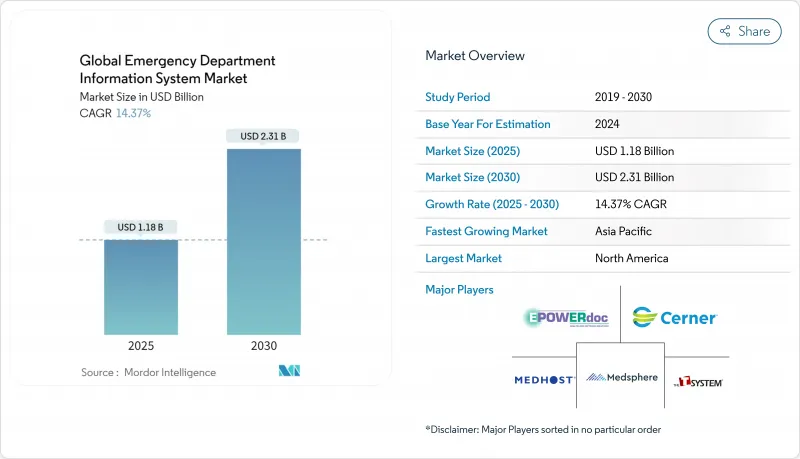

응급실 정보 시스템 시장 규모는 2025년 11억 8,000만 달러로 추정되고, 2030년 23억 1,000만 달러에 이를 전망이며, CAGR 14.37%로 성장할 것으로 예측됩니다.

보급의 원동력은 치료 시간 지표의 의무화, AI를 활용한 임상 판단 지원의 통합, 지역 병원에서 SaaS 전개로의 신속한 시프트입니다. 의료 기관은 과밀 상태를 제거하고 품질에 대한 의무를 준수하며 환자 중심 지표와 연계 된 상환을 보장하기 위해 이러한 시스템을 도입했습니다(cms.gov). 반면에 사이버 보안에 대한 기대가 높아지고 있으며, 공급업체는 임상 워크플로우를 정체하지 않고 제로 트러스트 아키텍처를 통합할 필요가 있습니다. Oracle의 Cerner 인수로 전문 공급업체에 빈 공간이 생겨 Epic의 설치 기반 리드가 확대된 후 경쟁 역학이 빠르게 진화하고 있습니다.

세계의 응급실 정보 시스템 시장 동향 및 인사이트

AI에 의한 임상 판단 지원 통합

AI 툴은 현재 인간의 예민도 분류 정밀도에 89%로 필적하고, 응급 심혈관계의 치료 시간을 205.4분 단축해, 실제의 트리아지에 있어서의 가치를 증명하고 있습니다. HCA 헬스케어와 같은 대규모 공급자는 184개의 진료과에서 앰비언트 문서를 실시하고 있으며, 99%의 환자가 수용하고 있습니다. 마찬가지로 중요한 것은 예측 모델이 전통적인 스코어링을 능가하고, AUROC는 0.92를 초과하며, AI는 결과와 업무 효율의 양면에서 차별화의 핵심입니다.

환자 중심의 품질 측정으로 상환 모델 증가

메디케어의 가치 기반 구매는 병원 진료비를 처리량과 경험 점수에 연결하여 응급실의 성과를 직접적인 수익 지렛대로 창출합니다. 또한 상업적 환급이 감소함에 따라 워크플로우 간소화의 시급성이 높아지며, 2024년에 발표된 새로운 형평성 조치는 사회적 결정 요인을 응급 지표에 포함시켰습니다. 조기에 적응하는 병원은 마진을 보호하고 2018-2022년 기록된 3.8%의 매출 침식을 완화할 수 있습니다.

사이버 보안 침해 부채 및 보험료

평균 침해 비용은 2024년 977만 달러로 상승했고, 병원은 공격 중에 매일 200만 달러를 잃을 수 있기 때문에 CFO는 불요불급의 IT 도입을 늦추도록 촉구하고 있습니다. 사이버 보험의 손해율은 상승하고 있으며, 특히 클라우드에 의존하는 워크플로우에서는 보험료가 상승하고 있습니다.

부문 분석

환자 추적 및 트리어지는, 병원이 실시간 병상 상황과 용태 대시보드를 선호했기 때문에, 2024년 응급실 정보 시스템 시장 점유율의 36.19%를 획득했습니다. 이 부문의 이점은 door-to-doctor 벤치마크에 대한 규제의 초점 및 수동 검사보다 빠르게 패혈증과 뇌졸중에 플래그를 지정하는 AI 도구에 의해 강화되었습니다. E-Prescribing은 CAGR 14.82%로 가장 급상승하고 있으며, 미국의 많은 주에서 전자 스크립트를 의무화하고 있는 오피오이드 리스크 감시가 뒷받침하고 있습니다. 대규모 공급자가 의사의 화면 표시 시간을 줄이기 위해 앰비언트 음성 캡처를 도입했기 때문에 임상 문서화는 큰 가중치를 차지합니다. CPOE의 채용은 투약 안전 프로토콜이 폐쇄 루프 주문을 요구하기 때문에 견조하게 변화하고 있습니다. 트리어지 모듈에 예측 민첩성 스코어링을 통합한 새로운 분석은 단일 워크플로우가 초기 평가부터 문서화까지 다루는 미래의 수렴을 시사합니다.

향후 환자 추적 모듈은 5G 텔레메트리와 통합되어 구급차 도착 전에 바이탈을 캡처하고, 트리어지 엔진은 머신러닝 권장사항에 자연어 질의를 거듭할 것으로 보입니다. 사일로화된 추적 보드를 계속 사용하는 병원은, AI가 몇 분 빨리 발견할 수 있는 용량 트리거를 놓칠 위험이 있습니다. 품질 지표의 상환이 깊어짐에 따라, 소규모 시설조차도 현재는 학술 센터에만 있는 고급 트리어지 대시보드를 채택하게 될 것으로 보입니다. 따라서 응급실 정보 시스템 시장에서는 추적, 처방, 문서화를 통합기록에 통합하는 멀티 모듈 스위트의 라이선스 보급률이 상승할 것으로 보입니다.

2024년 응급실 정보 시스템 시장 규모는 SaaS 제공이 65.27%의 점유율을 차지했습니다. 공급자는 초기 투자 감소, 신속한 운영 개시, 법규의 자동 갱신 등을 주요 이유로 꼽고 있습니다. IT 팀이 슬림한 지역 병원은 공급업체에 유지보수를 위탁하고 분석 애드온 예산을 확보하고 있습니다. 대규모 의료 시스템은 클라우드 풋 프린트를 확대하고 있지만 대기 시간에 민감한 이미지 처리를 위해 사내 구축형 클러스터를 유지하고 있으며, 이 부문의 CAGR 전망이 15.12%임을 설명합니다. 팬데믹 후 노동력 부족은 원격 업그레이드에 필요한 내부 엔지니어의 수를 줄이기 위해 클라우드 사용을 가속화합니다.

엣지 게이트웨이가 빈도가 높은 바이탈을 로컬로 처리하는 반면 요약 데이터를 중앙 클라우드에 아카이브하므로 하이브리드 패턴이 심화됩니다. 사이버 보험 규정은 현재 명확한 재해 복구 런북을 요구하고 있으며 감사된 중복성을 가진 SaaS 공급업체를 지원합니다. 국제적인 확장은 대역폭 문제를 부각하고 있지만, 멀티존 아키텍처와 오프라인 동기화는 기능정지를 완화하고 있습니다. 규제 당국의 감사는 로그 추적의 불변성이 점점 더 요구되고 있으며 실시간 컴플라이언스 대시 보드를 제공하는 클라우드 공급자가 점유율을 높이고 있습니다. 따라서 응급실 정보 시스템 시장의 성장은 클라우드의 경제성 및 병원 수준의 내결함성을 결합하는 벤더의 능력에 달려 있습니다.

응급실 정보 시스템 시장 보고서는 용도별(컴퓨터에 의한 의사 주문 엔트리(CPOE), 임상 기록, 환자 추적 및 트리어지 등), 도입 형태별(온프레미스 EDIS, SaaS), 소프트웨어 유형별(엔터프라이즈 솔루션, BOB) 솔루션, 최종 사용자별(소규모 병원, 중규모 병원, 대규모 병원), 지역별로 업계를 세분화합니다.

지역별 분석

북미는 2024년 응급실 정보 시스템 시장 수익의 45.25%를 유지했습니다. CMS의 품질보고 및 합동위원회의 인증은 병원에 입원 결정에서 퇴원까지의 지표를 문서화할 것을 의무화하고 있으며, 연간 1억 3,000만 건 이상의 ED 방문은 정확한 환자 추적의 필요성을 강화하고 있습니다. 2018-2022년 기록된 메디케어의 지불 감소는 효율화 추진에 재정적인 긴급성을 더합니다. TEFCA 배포 및 FHIR 인센티브는 실시간 상호 운용성을 보장하는 플랫폼 업그레이드를 더욱 촉구합니다. Providence Health & Service와 같은 대규모 네트워크는 적극적인 비용 억제를 추구하고 상환 스트레스를 상쇄하는 기술의 역할을 강조합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 15.94%로 가장 급성장하고 있는 지역입니다. 정부는 병원의 현대화에 자금을 제공하고 민간 체인은 디지털 확장으로 인한 높은 이익률을 예측합니다. 중국의 5G 의료 지침 센터는 구조 범위를 확대하고 지구를 가로 지르는 운송 시간을 단축하며 고급 연결성의 가치를 입증합니다. 그러나 중국 병원의 도산 건수는 증가하고 있으며, 재무의 건전성에 편차가 있음을 부각하고 있습니다. 동남아시아에서는 원장이 영상 진단과 1차 케어에 대한 투자를 우선하고 있어 구급부문의 디지털 툴과의 연동이 진행되고 있습니다.

유럽에서는 각국의 의료 서비스 구조와 상호 운용성 규제에 의해 꾸준히 도입이 진행되고 있습니다. 독일의 병원 미래법에서는 40억 유로 이상을 디지털 프로젝트에 투입하고 있으며, 병원은 인프라가 뛰어나지만 원격 의료의 보급에서는 늦어지고 있음이 감사에서 밝혀지고 있습니다. 유럽 의료 데이터 공간은 기록 형식을 표준화하고 국경을 넘어 환자의 흐름을 지원합니다. eCREAM과 같은 프로젝트는 응급 문서의 조화를 목표로 하는 것으로, 이탈리아의 조사에 따르면 대규모 교육 병원이 가장 빨리 디지털화하고, 특히 응급 치료실이 변혁의 앵커로서 기능하고 있습니다. 동유럽의 시스템은 성숙도의 격차를 메우기 위해 협조적인 자금 제공을 요구하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI를 활용한 임상 의사결정 지원의 통합

- 환자 중심의 품질 지표에 기초한 상환 모델 확대

- 지역 병원에서 SaaS 기반 EDIS의 급속한 성장

- 치료까지 시간의 필수 주요 성과 평가 지표

- 실시간 의료 데이터 교환 프레임워크(FHIR, TEFCA)의 급증

- 구급차로부터 구급 외래까지의 데이터 플로우에 있어서 엣지 분석 및 5G의 도입

- 시장 성장 억제요인

- 사이버 보안 침해의 배상 책임 및 보험료

- 복잡한 전자 의료 기록의 사용자 인터페이스와 관련된 임상의의 소진 증후군

- 디바이스 통합을 위한 단편화된 미들웨어 표준

- 팬데믹 후 공립 병원 예산 동결

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 용도별

- 의사 컴퓨터 주문 엔트리(CPOE)

- 임상 문서

- 환자 추적 및 트리아지

- 전자 처방

- 기타

- 전개별

- 온프레미스

- 서비스로서의 소프트웨어(SaaS)

- 소프트웨어 유형별

- 엔터프라이즈 솔루션

- 베스트 오브 블리드(BoB) 솔루션

- 최종 사용자별

- 소규모 병원(100 병상 이하)

- 중규모 병원(101-299 병상)

- 대규모 병원(300 병상 이상)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Oracle Health(Cerner)

- Epic Systems Corporation

- MEDHOST Inc.

- MEDITECH

- Allscripts Healthcare Solutions

- McKesson Corporation

- UnitedHealth Group(Optum Insight)

- EPOWERdoc Inc.

- T-Systems International

- Evident(CPSI)

- Logibec Inc.

- Medsphere Systems

- Picis Clinical Solutions

- Wellsoft Corporation

- Dedalus Group

- Philips Healthcare

- Ascom Holding AG

- Cantata Health

- VitalHub Corp.

- Global Health Ltd(MasterCare)

제7장 시장 기회 및 향후 전망

AJY 25.11.19The Emergency Department Information System market size stood at USD 1.18 billion in 2025 and is forecast to reach USD 2.31 billion by 2030, advancing at a 14.37% CAGR.

Wider adoption is driven by mandatory time-to-treatment indicators, the integration of AI-enabled clinical decision support, and a swift shift toward SaaS deployment in community hospitals. Providers are deploying these systems to cut overcrowding, comply with quality mandates, and secure reimbursement tied to patient-centric metrics cms.gov. Tighter cybersecurity expectations, meanwhile, push vendors to embed zero-trust architectures without slowing clinical workflows. Competitive dynamics are evolving quickly after Oracle's acquisition of Cerner, which opened white-space for specialist vendors and widened Epic's installed-base lead.

Global Emergency Department Information System Market Trends and Insights

AI-enabled clinical decision support integration

AI tools now match human acuity classification accuracy at 89% and have cut emergency cardiovascular time-to-treatment by 205.4 minutes, proving value in real-world triage . Large providers such as HCA Healthcare run ambient documentation across 184 departments with 99% patient acceptance. Equally important, predictive models outperform traditional scoring with AUROC readings above 0.92, positioning AI as a core differentiator in both outcomes and operational efficiency.

Increasing patient-centric quality-metric reimbursement models

Medicare's Value-Based Purchasing ties hospital payment to throughput and experience scores, making emergency department performance a direct revenue lever. Declining commercial reimbursements heighten the urgency to streamline workflows, while new equity measures rolling out in 2024 embed social determinants into emergency metrics. Hospitals that adapt early can safeguard margins and mitigate the 3.8% revenue erosion documented from 2018 to 2022.

Cyber-security breach liabilities and insurance premiums

Average breach cost climbed to USD 9.77 million in 2024 and hospitals can lose USD 2 million daily during attacks, prompting CFOs to delay non-essential IT rollouts. Rising cyber-insurance loss ratios are pushing premiums up, particularly for cloud-dependent workflows.

Other drivers and restraints analyzed in the detailed report include:

- Rapid growth of SaaS-based EDIS in community hospitals

- Mandatory time-to-treatment key performance indicators

- Surge in real-time health-data exchange frameworks (FHIR, TEFCA)

- Edge analytics & 5G deployment in ambulance-to-ED data flow

- Clinician burnout linked to complex EHR interfaces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Patient Tracking & Triage captured 36.19% of Emergency Department Information System market share in 2024 as hospitals prioritized real-time bed status and acuity dashboards. The segment's dominance is reinforced by regulatory focus on door-to-doctor benchmarks and by AI tools that flag sepsis and stroke earlier than manual checks. E-Prescribing is the fastest riser at a 14.82% CAGR, fueled by opioid-risk monitoring that mandates electronic scripts across many US states. Clinical Documentation holds significant weight as large providers deploy ambient voice capture to trim physician screen time. CPOE adoption remains steady because medication safety protocols demand closed-loop orders. Emerging analytics that fold predictive acuity scoring into triage modules hint at future convergence where a single workflow covers initial assessment through documentation.

Looking forward, patient-tracking modules will integrate with 5G telemetry to ingest ambulance vitals long before arrival, while triage engines will layer natural-language queries on top of machine-learning recommendations. Hospitals continuing to run siloed tracking boards risk missing capacity triggers that AI can surface minutes sooner. As quality-metric reimbursement deepens, even smaller facilities will adopt advanced triage dashboards that now sit only in academic centers. The Emergency Department Information System market will therefore see rising license penetration for multi-module suites that merge tracking, prescribing, and documentation into a unified record.

SaaS delivery held 65.27% share of the Emergency Department Information System market size in 2024. Providers cite lower up-front capital, faster go-live timelines, and automatic regulatory updates as key reasons. Community hospitals with lean IT teams offload maintenance to vendors, freeing budgets for analytics add-ons. Large health systems still expand cloud footprints but also maintain on-premise clusters for latency-sensitive imaging, which explains the segment's 15.12% CAGR outlook. The post-pandemic workforce crunch accelerates cloud uptake because remote upgrades need fewer in-house engineers.

Hybrid patterns will deepen as edge gateways process high-frequency vitals locally while archiving summary data to a central cloud. Cyber-insurance stipulations now require explicit disaster-recovery run-books, favoring SaaS vendors with audited redundancy. International expansion highlights bandwidth challenges yet multi-zone architectures and offline sync mitigate outages. As regulatory audits increasingly ask for immutable log trails, cloud providers offering real-time compliance dashboards gain mind-share. Growth in the Emergency Department Information System market will therefore pivot on vendor ability to mix cloud economics with hospital-grade resilience.

The Emergency Department Information System Market Report Segments the Industry Into by Application (Computerized Physician Order Entry (CPOE), Clinical Documentation, Patient Tracking & Triage, and More), by Deployment (On-Premise EDIS, Software-As-A-Services (SaaS)), by Software Type (Enterprise Solutions, Best of Breed (B. O. B. ) Solutions), by End User (Small Hospitals, Medium-Sized Hospitals, Large Hospitals), and Geography.

Geography Analysis

North America retained 45.25% of Emergency Department Information System market revenue in 2024. CMS quality reporting and Joint Commission accreditation oblige hospitals to document admit-decision-to-departure metrics, and over 130 million annual ED visits intensify the need for precise patient tracking. Medicare payment declines recorded between 2018 and 2022 add financial urgency to efficiency drives. TEFCA rollout and FHIR incentives further compel platform upgrades that guarantee real-time interoperability. Large networks such as Providence Health & Services pursue aggressive cost containment, underscoring technology's role in offsetting reimbursement stress.

Asia-Pacific is the fastest-growing region at a 15.94% CAGR to 2030. Governments fund hospital modernization and private chains forecast high profit margins from digital expansion. 5G medical command centers in China extend rescue reach and cut cross-district transfer times, proving the value of advanced connectivity. Yet rising bankruptcies among Chinese hospitals highlight uneven financial health, requiring modular pricing that scales with volume. In Southeast Asia, directors prioritize diagnostic imaging and primary care investments which naturally link to emergency-department digital tools.

Europe posts steady uptake shaped by national health-service structures and interoperability regulations. Germany's Hospital Future Act channels more than EUR 4 billion into digital projects, and audits reveal hospitals excel in infrastructure yet lag in telehealth penetration. The European Health Data Space will standardize record formats, aiding cross-border patient flows. Projects such as eCREAM aim to harmonize emergency documentation, while Italian studies show that larger, teaching hospitals digitize fastest, especially where emergency rooms act as transformation anchors. Eastern European systems seek coordinated funding to bridge their maturity gaps.

- Oracle Health (Cerner)

- Epic Systems

- MEDHOST Inc.

- Meditech

- Allscripts

- Mckesson

- UnitedHealth Group (Optum Insight)

- EPOWERdoc Inc.

- T-Systems International

- Evident (CPSI)

- Logibec Inc.

- Medsphere Systems

- Picis Clinical Solutions

- Wellsoft Corporation

- Dedalus Group

- Koninklijke Philips

- Ascom

- Cantata Health

- VitalHub Corp.

- Global Health Ltd (MasterCare)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-enabled clinical decision-support integration

- 4.2.2 Increasing patient-centric quality-metric reimbursement models

- 4.2.3 Rapid growth of SaaS-based EDIS in community hospitals

- 4.2.4 Mandatory time-to-treatment key performance indicators

- 4.2.5 Surge in real-time health-data exchange frameworks (FHIR, TEFCA)

- 4.2.6 Edge analytics & 5G deployment in ambulance-to-ED data flow

- 4.3 Market Restraints

- 4.3.1 Cyber-security breach liabilities & insurance premiums

- 4.3.2 Clinician burnout linked to complex EHR user-interfaces

- 4.3.3 Fragmented middleware standards for device integration

- 4.3.4 Budget freezes in public hospitals post-pandemic

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Application

- 5.1.1 Computerized Physician Order Entry (CPOE)

- 5.1.2 Clinical Documentation

- 5.1.3 Patient Tracking & Triage

- 5.1.4 E-Prescribing

- 5.1.5 Others

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Software-as-a-Service (SaaS)

- 5.3 By Software Type

- 5.3.1 Enterprise Solutions

- 5.3.2 Best-of-Breed (BoB) Solutions

- 5.4 By End User

- 5.4.1 Small Hospitals (<=100 beds)

- 5.4.2 Medium-Sized Hospitals (101-299 beds)

- 5.4.3 Large Hospitals (>=300 beds)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 APAC

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of APAC

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Oracle Health (Cerner)

- 6.3.2 Epic Systems Corporation

- 6.3.3 MEDHOST Inc.

- 6.3.4 MEDITECH

- 6.3.5 Allscripts Healthcare Solutions

- 6.3.6 McKesson Corporation

- 6.3.7 UnitedHealth Group (Optum Insight)

- 6.3.8 EPOWERdoc Inc.

- 6.3.9 T-Systems International

- 6.3.10 Evident (CPSI)

- 6.3.11 Logibec Inc.

- 6.3.12 Medsphere Systems

- 6.3.13 Picis Clinical Solutions

- 6.3.14 Wellsoft Corporation

- 6.3.15 Dedalus Group

- 6.3.16 Philips Healthcare

- 6.3.17 Ascom Holding AG

- 6.3.18 Cantata Health

- 6.3.19 VitalHub Corp.

- 6.3.20 Global Health Ltd (MasterCare)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment