|

시장보고서

상품코드

1850397

AaaS 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automation-as-a-Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

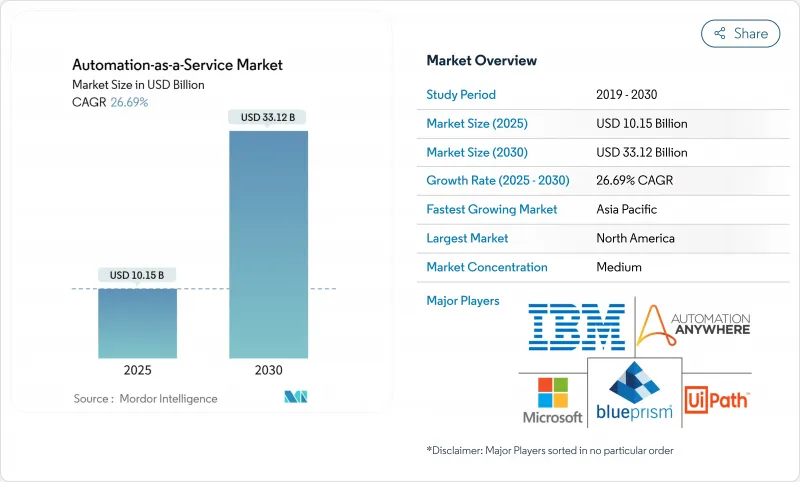

AaaS 시장 규모는 2025년에 101억 5,000만 달러, 2030년에는 331억 2,000만 달러에 이르고, CAGR 26.7%로 성장할 것으로 예상됩니다.

기업이 기존의 로봇 프로세스 자동화 투자에 생성형 AI 기능을 통합하는 한편, 구독 과금에 의해 자본 지출을 억제함으로써 도입이 가속화되고 있습니다. 강력한 클라우드 에코시스템, 로우코드 디자인 스튜디오의 출현, 기성품 봇의 도메인 마켓플레이스의 출현으로 대응 가능한 고객층이 확대되고 있습니다. 프로세스 마이닝 진단과 이벤트 중심 오케스트레이션을 결합한 통합은 실시간 최적화를 가능하게 하고 자동화 프로그램을 작업 수준 개선에서 엔드 투 엔드 워크플로 재설계로 끌어 올립니다. 발견, 구축 및 실행의 각 단계에 걸쳐 수직으로 통합된 스택을 가진 공급업체는 특히 통일된 거버넌스를 필요로 하는 규제 산업에서 포인트 솔루션을 대체하는 존재로 남아 있습니다.

세계 AaaS 시장 동향과 통찰

비즈니스 프로세스 자동화에 대한 수요 증가

현재 새롭게 자동화된 워크플로우의 44%는 비즈니스 부서가 만들었으며 시민 개발자가 중앙 IT 팀을 보완하고 있음을 보여줍니다. 수익 사업 프로젝트가 자동화된 워크플로의 절반에 가깝고 고객을 위한 사용 사례로의 전환을 강조합니다. 크로스펑션 팀이 핸드오프를 리엔지니어링함에 따라 로우코드 합성을 가능하게 하면서 세분화된 퍼미션을 관리할 수 있는 플랫폼에 대한 수요가 높아지고 있습니다. 복잡성도 증가하고 있습니다. 활성 봇의 61%는 단일 작업 매크로가 아닌 다중 단계 로직을 실행합니다. 고객 지원 프로세스는 3자리 성장을 보여주고 자동화가 비용 제약이 있는 경제 주기에서 유지 보수 전략에 단단히 연결되어 있음을 보여줍니다.

AaaS 배포를 가속화하는 클라우드 퍼스트 IT 전략

다중 테넌트 아키텍처를 통해 공급자는 예정된 다운타임 없이 모든 클라이언트 인스턴스에 새로운 기능을 배포하여 혁신 주기를 단축할 수 있습니다. Infrastructure-as-Code 템플릿은 테스트, 스테이징 및 프로덕션 계층에서 환경 프로비저닝을 표준화하여 마찰을 더욱 줄여줍니다. 중소기업에서는 종량 과금제를 통해 자동화를 위한 지출을 운영 예산에 돌려 서버 유지 보수 오버헤드를 없앨 수 있습니다. 하이브리드 실적가 있는 기업은 대기 시간에 민감한 워크로드를 가장자리에 배치하면서 클라우드에서 중앙 집중식으로 정책을 오케스트레이션하고 주권 규칙과 탄력적인 규모의 균형을 유지합니다. 그 결과 클라우드 중심의 배포가 AaaS 시장 전체의 성장을 능가하고 있습니다.

멀티 테넌트 클라우드에서 데이터 보안 및 개인 정보 보호에 대한 우려

공유 인프라 모델은 분리 제어가 실패할 경우 수평 이동 위험을 증가시켜 금융 서비스 및 건강 관리 구매자에게 가장 큰 우려 사항이 되었습니다. 이 문제는 AI 코 파일럿이 광범위한 OAuth 범위를 상속하고 프롬프트 주입으로 기밀 컨텐츠가 노출될 수 있는 경우 증폭됩니다. 유럽 규제 당국은 엄격한 레지던시 및 자동 판단 공개 규칙을 시행하고 공급자에게 암호화 표준 인증 및 로그 분리를 의무화합니다. 공급업체는 고객이 관리하는 키, 지역별로 고정된 데이터스토어 및 지속적인 규정 준수 대시보드를 지원합니다. 도입의 기세는 견고하지만, 규제가 엄격한 섹터의 바이어는 리스크가 낮은 프로세스로부터 단계적으로 도입을 진행하고 있습니다.

부문 분석

2024년 AaaS 시장에서는 On-Premise형이 68.4%의 점유율을 유지하고 있습니다. 이는 금융 및 공공 부문에서 엄격한 소블린 의무와 하드웨어에 대한 투자를 반영합니다. 하지만 클라우드 기반은 CAGR 28.4%로 확대되고 있습니다. 이는 조직이 인프라 유지 관리를 완화하기 위해 중요하지 않은 워크플로우 및 개발 샌드박스를 마이그레이션하기 때문입니다. 공급업체는 현재 탄력적인 확장성과 자동 패치 적용을 유지하면서 감사 요구 사항을 충족하는 단일 테넌트 VPC 옵션을 제공합니다. 에지 배포는 대기 시간에 영향을 받기 쉬운 작업의 데이터를 로컬로 처리한 다음 풍부한 페이로드를 중앙 애널리틱스로 라우팅하여 성능과 거버넌스 간의 균형을 이루는 하이브리드 토폴로지를 구축합니다. 관리자는 비용 및 규정 준수 트리거를 기반으로 워크로드를 동적으로 이동할 수 있습니다. 이러한 유연성을 통해 클라우드 모델은 AaaS 시장의 장기 성장 엔진으로 자리매김하고 있으며, 특히 데이터센터 자산을 소유하지 않은 그린필드 디지털 비즈니스에 중요한 역할을 합니다.

플랫폼 라이선스와 봇 제작 스튜디오가 대부분의 구매자를 위한 진입점이 되었기 때문에 2024년 판매는 솔루션이 66.8%를 차지합니다. 그러나 기업이 디자인 사고, 변경 관리, 지속적인 개선의 전문 지식을 요구함에 따라 2030년까지의 CAGR은 28.1%가 되어 서비스 부문이 소프트웨어 매출을 상회할 것으로 예측됩니다. 관리형 서비스 제공업체는 런북 관리, 봇 상태 모니터링, 보안 패치를 적용하여 고객이 핵심 혁신에 집중할 수 있도록 합니다. 공급업체 생태계의 권고 팜은 프로세스 마이닝 진단 및 초자동화 설계도를 패키징하여 인력을 늘리지 않고도 가치 실현까지의 시간을 단축합니다. 복잡성이 증가함에 따라 서비스 품질이 중요한 차별화 요인이 되어 에코시스템의 록인이 강화되고, AaaS 시장 전체의 평생계약 가치가 높아집니다.

Automation As A Service 시장 보고서는 배포 유형(On-Premise 및 클라우드), 구성 요소(솔루션 및 서비스), 비즈니스 기능(정보 기술, 재무 및 회계 등), 기업 규모(대기업 및 중소기업(SME)), 최종 사용자 업계별(은행, 금융서비스 및 보험(BFSI), 통신 및 IT, 소매 및 소비재 등) 및 지역별로 분류됩니다.

지역 분석

북미는 성숙한 하이퍼스케일 데이터센터, 치밀한 파트너 네트워크, 금융, 헬스케어, 공공 서비스에 걸친 플랫폼의 조기 도입에 힘입어 2024년 매출 38.6%로 주도권을 잡는다. 미국 기업은 ERP, CRM, 가상 클라우드에 걸친 데이터를 조정하는 인지 봇을 도입하여 플랫폼 이용률을 세계 평균 이상으로 끌어 올리고 있습니다. 캐나다에서는 공공 부문에서의 이용이 가속화되고 멕시코에서는 자동화를 활용하여 제조업의 니어쇼어링 경쟁력을 강화하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 27.3%로 가장 빠른 성장을 기록했습니다. ASEAN 디지털 마스터 플랜 2025는 국경을 넘어 디지털 서비스의 표준화를 촉진하고 공공 부문의 자동화에 박차를 가해 민간 기업에도 급속히 침투합니다. 중국은 공장의 로봇과 시정 봇의 규모를 확대하고, 인도는 IT 서비스 워크플로우를 근대화하고, 일본은 노인 간호를 위한 대화 요원으로 노동력 부족을 다룹니다. 한국은 5G 대응 에지 자동화를 시험적으로 도입하고 호주는 광업 부문의 공정 효율화에 주력하고 있습니다.

유럽은 혁신과 엄격한 데이터 보호 감시의 균형을 잡는 신중한 자세를 취하고 있습니다. GDPR(EU 개인정보보호규정)과 AI 거버넌스 법의 제안은 설명 가능한 워크플로우와 감사 로그의 통합을 요구합니다. 스위스, 스웨덴, 독일이 가장 높은 보급률을 보이고 있으며, 은행과 제조업체가 AI 코파일럿을 중요한 업무에 통합하고 있습니다. 남유럽 국가의 경제는 디지털화를 위한 EU의 자금 지원에 의존하고 있으며, platform-as-a-service 계약의 새로운 입찰을 창출하고 있습니다. 이러한 역학을 통해 AaaS 시장은 다양한 거시 경제적 배경 중에서도 탄력성을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비즈니스 프로세스 자동화 수요 증가

- AaaS 도입을 가속화하는 클라우드 퍼스트의 IT 전략

- 하이퍼 오토메이션을 위한 RPA와 Gen-AI의 융합

- 구독과 사용량 기반의 가격 설정에 의해 중소기업의 진입 장벽을 낮추기

- 도메인 특화형 봇 마켓플레이스의 출현

- 프로세스 마이닝의 통찰을 통합하여 엔드 투 엔드의 자동화를 추진

- 시장 성장 억제요인

- 멀티 테넌트 클라우드에서의 데이터 보안 및 프라이버시 우려

- 레거시/On-Premise 시스템과의 통합 복잡성

- 알고리즘 투명성 및 윤리에 대한 규제 조사

- 로우 코드 자동화 거버넌스 인력 부족

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 전개 유형별

- On-Premise

- 클라우드

- 컴포넌트별

- 솔루션

- 서비스

- 업무 기능별

- 정보기술

- 재무와 회계

- 인사

- 영업과 마케팅

- 오퍼레이션/서플라이 체인

- 기업 규모별

- 대기업

- 중소기업

- 최종 사용자별

- BFSI

- 통신 및 IT

- 소매 및 소비재

- 헬스케어 및 생명과학

- 제조업

- 정부 및 공공 부문

- 기타 최종 사용자 분야

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Automation Anywhere

- UiPath

- Blue Prism

- IBM

- Microsoft

- HCLTech

- Hewlett Packard Enterprise

- Kofax

- NICE

- Pegasystems

- ServiceNow

- Appian

- SAP

- Oracle

- Salesforce(MuleSoft/RPA)

- WorkFusion

- Celonis

- Nintex

- Workato

- AutomationEdge

제7장 시장 기회와 장래의 전망

SHW 25.11.11The Automation-as-a-Service market size stands at USD 10.15 billion in 2025 and is forecast to reach USD 33.12 billion by 2030, advancing at a 26.7% CAGR.

Adoption is accelerating as enterprises embed generative-AI features into existing robotic-process-automation investments while containing capital outlays through subscription billing. Robust cloud ecosystems, the rise of low-code design studios, and the emergence of domain marketplaces for ready-made bots are widening the addressable customer base. Integrations that combine process-mining diagnostics with event-driven orchestration allow real-time optimization, pushing automation programs from task level gains to end-to-end workflow redesign. Vendors with vertically integrated stacks that span discovery, build and run phases continue to displace point solutions, especially in regulated industries that demand unified governance.

Global Automation-as-a-Service Market Trends and Insights

Rising Demand for Business-Process Automation

Business units now originate 44% of all newly automated workflows, signalling that citizen developers are complementing central IT teams. Revenue-operations projects account for nearly half of live automations, underscoring a pivot toward customer-facing use cases. As cross-functional teams re-engineer hand-offs, demand rises for platforms that can manage granular permissions while enabling low-code composition. Complexity is also increasing: 61% of active bots execute multistep logic rather than single-task macros. Customer support processes experienced triple-digit growth, showing that automation is firmly linked to retention strategies during cost-constrained economic cycles.

Cloud-First IT Strategies Accelerating AaaS Adoption

Multi-tenant architectures let providers roll out new capabilities to every client instance without scheduled downtime, shortening innovation cycles. Infrastructure-as-Code templates further reduce friction by standardising environment provisioning across testing, staging and production tiers. For SMEs, pay-as-you-go consumption shifts automation spending to operating budgets and removes server maintenance overhead. Enterprises with hybrid footprints place latency-sensitive workloads at the edge while orchestrating policies centrally in the cloud, balancing sovereignty rules with elastic scale. As a result, cloud-centric deployments are outpacing overall Automation-as-a-Service market growth.

Data-Security and Privacy Concerns in Multi-Tenant Clouds

Shared-infrastructure models increase lateral-movement risk if isolation controls fail, a top worry for financial-services and healthcare buyers. The issue is amplified when AI copilots inherit broad OAuth scopes, potentially exposing confidential content through prompt injections. European regulators enforce strict residency and automated-decision disclosure rules, forcing providers to certify encryption standards and segregate logs. Vendors respond with customer-managed keys, regionally pinned data stores and continuous compliance dashboards. Adoption momentum remains solid but buyers in highly regulated sectors proceed with staged rollouts that start with low-risk processes.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of RPA with Generative AI for Hyper-Automation

- Subscription and Usage-Based Pricing Lowering SME Entry Barriers

- Integration Complexity with Legacy/On-Prem Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations retained 68.4% share of the Automation-as-a-Service market in 2024, reflecting strict sovereignty mandates and sunk hardware investments within finance and public-sector domains. Nevertheless, cloud variants are expanding at a 28.4% CAGR as organisations migrate non-critical workflows and development sandboxes to reduce infrastructure upkeep. Vendors now provide single-tenant VPC options that satisfy audit requirements while preserving elastic scale and automated patching. Edge deployments process data locally for latency-sensitive tasks before routing enriched payloads to central analytics, creating a hybrid topology that balances performance with governance. Contracts increasingly bundle both operating modes under unified dashboards, enabling administrators to shift workloads dynamically based on cost or compliance triggers. This flexibility positions cloud models as the long-run growth engine of the Automation-as-a-Service market, particularly for green-field digital businesses that never owned data-centre assets.

Solutions accounted for 66.8% revenue in 2024 as platform licences and bot-authoring studios formed the entry point for most buyers. The services segment, however, is forecast to outpace software sales at 28.1% CAGR through 2030 as enterprises seek design thinking, change management and continuous-improvement expertise. Managed-service providers curate runbooks, monitor bot health and apply security patches, letting customers focus on core innovation. Advisory firms within the vendor ecosystem package process-mining diagnostics with hyper-automation blueprints, accelerating time to value without ballooning headcount. As complexity rises, service quality becomes a key differentiator, reinforcing ecosystem lock-in and boosting lifetime contract values across the Automation-as-a-Service market.

The Automation As A Service Market Report is Segmented by Deployment Type (On-Premise and Cloud), Component (Solution and Services), Business Function (Information Technology, Finance and Accounting, and More), Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (BFSI, Telecom and IT, Retail and Consumer Goods, and More), and Geography.

Geography Analysis

North America holds leadership with 38.6% revenue in 2024, supported by mature hyperscale data centres, a dense partner network and early platform adoption that spans finance, healthcare and public services. United States corporations deploy cognitive bots that reconcile data across ERP, CRM and vertical clouds, pushing platform utilisation rates above global averages. Canada accelerates public-sector use, while Mexico leverages automation to enhance near-shoring competitiveness in manufacturing.

Asia-Pacific registers the fastest growth at 27.3% CAGR through 2030. The ASEAN Digital Masterplan 2025 catalyses cross-border digital-service standards, spurring public-sector automation that quickly permeates private enterprises. China scales factory-floor robotics and city-administration bots, India modernises IT-service workflows, and Japan addresses labour shortages with conversational agents for elder-care. South Korea pilots 5G-enabled edge automations, while Australia focuses on mining-sector process efficiency.

Europe adopts a measured stance that balances innovation with rigorous data-protection oversight. GDPR and proposed AI-governance acts prompt demand for explainable workflows and built-in audit logs. Switzerland, Sweden and Germany exhibit the highest penetration rates, with banks and manufacturers integrating AI copilots into critical operations. Southern-European economies rely on EU funding for digitalisation, creating fresh bids for platform-as-a-service contracts. These dynamics keep the Automation-as-a-Service market resilient across varying macro-economic backdrops.

- Automation Anywhere

- UiPath

- Blue Prism

- IBM

- Microsoft

- HCLTech

- Hewlett Packard Enterprise

- Kofax

- NICE

- Pegasystems

- ServiceNow

- Appian

- SAP

- Oracle

- Salesforce (MuleSoft/RPA)

- WorkFusion

- Celonis

- Nintex

- Workato

- AutomationEdge

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for business-process automation

- 4.2.2 Cloud-first IT strategies accelerating AaaS adoption

- 4.2.3 Convergence of RPA with Gen-AI for hyper-automation

- 4.2.4 Subscription and usage-based pricing lowering SME entry barriers

- 4.2.5 Emergence of domain-specific bot marketplaces

- 4.2.6 Integration of process-mining insights to drive end-to-end automation

- 4.3 Market Restraints

- 4.3.1 Data-security and privacy concerns in multi-tenant clouds

- 4.3.2 Integration complexity with legacy/on-prem systems

- 4.3.3 Regulatory scrutiny over algorithmic transparency and ethics

- 4.3.4 Scarcity of low-code automation governance talent

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Component

- 5.2.1 Solution

- 5.2.2 Services

- 5.3 By Business Function

- 5.3.1 Information Technology

- 5.3.2 Finance and Accounting

- 5.3.3 Human Resources

- 5.3.4 Sales and Marketing

- 5.3.5 Operations / Supply-Chain

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-user Vertical

- 5.5.1 BFSI

- 5.5.2 Telecom and IT

- 5.5.3 Retail and Consumer Goods

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Verticals

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Automation Anywhere

- 6.4.2 UiPath

- 6.4.3 Blue Prism

- 6.4.4 IBM

- 6.4.5 Microsoft

- 6.4.6 HCLTech

- 6.4.7 Hewlett Packard Enterprise

- 6.4.8 Kofax

- 6.4.9 NICE

- 6.4.10 Pegasystems

- 6.4.11 ServiceNow

- 6.4.12 Appian

- 6.4.13 SAP

- 6.4.14 Oracle

- 6.4.15 Salesforce (MuleSoft/RPA)

- 6.4.16 WorkFusion

- 6.4.17 Celonis

- 6.4.18 Nintex

- 6.4.19 Workato

- 6.4.20 AutomationEdge

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment