|

시장보고서

상품코드

1850402

스마트 TV 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart TV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

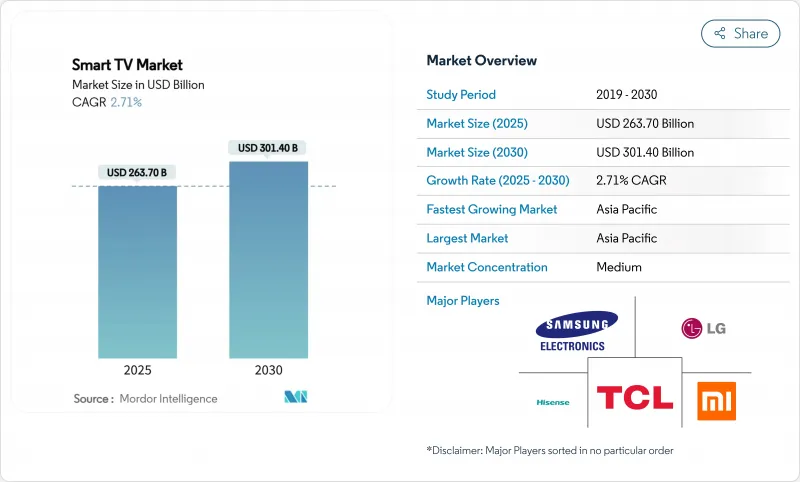

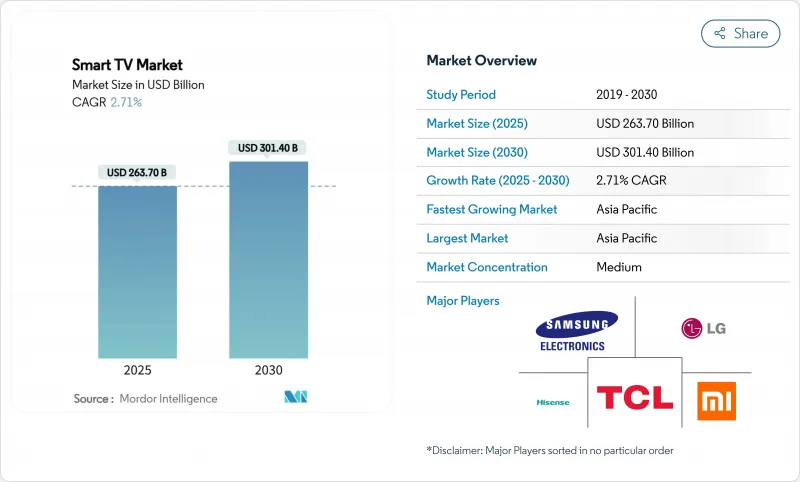

스마트 TV 시장 규모는 2025년 2,637억 달러로 추정되고, 2030년 3,014억 달러에 이를 전망이며, CAGR 2.71%로 확대될 것으로 예측됩니다.

현재의 기세는 최초 소유자의 급증에 의한 것이 아니라, AI를 활용한 이미지 처리, 통합된 클라우드 게임 기능, 금리를 유지하면서 비용을 압축하는 밸류체인 현지화 등의 단계적인 개선에 의한 것입니다. 인도 생산 연동 장려금의 확대와 베트남과 멕시코의 유사한 제조 공제는 리드 타임을 단축하고 평균 판매 가격을 낮추는 니어 소스 어셈블리 허브를 육성하고 있습니다. 디스플레이 제조업체는 OLED 공급 제약에 대항하기 위해 미니 LED 백라이트와 양자점 강화를 위한 연구개발에 방향타를 끊고 있으며, 통신사업자는 텔레비전을 파이버 플랜에 번들해 주소 가능 가구를 확대합니다. 플랫폼 경쟁은 광고 지원 컨텐츠 서비스 및 소프트웨어 지원 연장의 약속으로 전환하고 있으며 성숙한 지역에서도 프리미엄 구매를 촉구하고 있습니다.

세계의 스마트 TV 시장 동향 및 인사이트

55-65인치 4K 세트의 가격 하락이 인도와 브라질에서 대량 보급 가속

중국 OEM 각사는 한때 프리미엄층을 나타내는 임계값이었던 55인치 4K의 소매 가격을 2024년에는 400달러 이하로 밀었습니다. TCL이 98인치 모델을 5,999달러에서 1,999달러로 인하하는 등 적극적인 판촉을 실시함으로써, 라이벌 각사는 현지 조달로 마진을 확보하면서 엔트리 레벨 라인업을 확대할 수밖에 없었습니다. 삼성의 인도 부문은 디플레이션 하에서도 브랜드 주도의 AI 기능으로 가격대를 유지할 수 있다고 강조하며 2024년 TV 매출을 10,000캐롤 루피로 보고하고 있습니다.

텔레콤 주도의 광섬유 전개가 동남아시아 최초 보유 촉진

인도네시아, 태국, 말레이시아의 전국적인 광섬유 계획은 광대역 가입 비용을 절감하고 원활한 4K 스트리밍을 가능하게 합니다. 사업자는 현재 엔트리 레벨 43인치 TV를 100Mbps 계약에 번들어 기존 소매 채널을 통하지 않는 통합 서비스 제안을 하고 있습니다. 시청이 모바일 기기에서 거실 스크린으로 이동함에 따라 대응 가능한 수요는 도시 중심에서 Tier2 도시로 이동하여 2030년까지 세계의 스마트 TV 시장에 대한 아웃퍼폼을 유지합니다.

미니 LED 백라이트용 반도체 압박이 프리미엄 공급 제한

미니 LED 세트에는 수천 개의 드라이버 IC와 고밀도로 집적된 다이오드가 필요하지만, 이러한 부품의 웨이퍼 생산 능력은 2024년 수요 급증에 뒤처지고 있습니다. TrendForce의 예측에서 2024년 Mini-LED TV 출하량은 59% 증가한 640만 대에 이르렀으며, 사용 가능한 부품 공급량을 압도했습니다. 리드 타임은 30주를 넘어, 각 브랜드는 플래그쉽 라인을 우선해, 중위층의 채용을 지연시켰습니다. 공급 완화는 2026년 후반에 시작될 예정인 새로운 12인치 공장에 달려 있습니다.

부문 분석

HD 및 풀HD는 2024년에도 37.8%로 매출을 이끌어 신흥경제 국가의 비용에 민감한 구매층에 지지를 받고 있습니다. 반대로 8K UHD는 4.2%의 성장을 이루며 2030년까지 스마트 TV 시장 전체의 성장을 웃도는 것으로 예측됩니다. 2025년에 전개된 삼성 Vision AI 엔진은 저해상도 스트림을 네이티브에 가까운 8K 품질로 향상시켜 초고비트 레이트 컨텐츠의 부족을 완화합니다. 피크 휘도를 제한하는 EU의 에코 디자인 룰은 보다 효율적인 백라이트의 설계를 요구하는 압력이 되어, 브랜드는 고휘도 준거를 위해서 OLED보다 미니 LED에 방향타를 자릅니다.

엔트리 레벨 4K 세트는 가변 리프레시 레이트의 게이밍 모드 등의 프리미엄 기능을 계승해 중위층을 모호하게 해 총 스마트 TV 시장을 확대하고 있습니다. 컨텐츠 플랫폼은 카탈로그를 HDR10 및 Dolby Vision으로 업스케일링하여 동적 메타데이터를 정확하게 렌더링할 수 있는 고화소 밀도 패널에 대한 수요를 강화하고 있습니다.

2024년 스마트 TV 시장은 46-55인치 주류 모델이 32.1%를 차지했습니다. 이 카테고리의 평균 판매 가격은 인도와 멕시코에서 현지 조립이 축소되었기 때문에 전년 대비 9% 하락했습니다. 65인치 이상은 CAGR 3.8%로 예측되며, 120Hz 패널이나 오브젝트 추적 사운드 등 가장 프리미엄 기술 장착률을 견인합니다.

제조업체 각사는 공유 유리 기판 공장을 활용해 98인치 LCD를 2,000달러 이하로 밀어 내려, 중소득 가구에서도 벽걸이 사이즈의 시청이 가능하게 됩니다. 팬데믹 시대의 홈 시어터 업그레이드로 거실 레이아웃이 재구성되었지만 이러한 공간 변화로 인해 더 큰 화면이 선호되었습니다. 32인치 미만의 소형 스크린은 2차 방에서는 여전히 효과적이지만 수익 구성은 위쪽으로 이동하고 스마트 TV 시장의 헤드라인 성장은 완만함에도 불구하고 이익 풀을 지지하고 있습니다.

지역 분석

아시아태평양은 2024년 매출의 41.2%를 차지했으며, CAGR 3.2%로 성장을 이끌고 있습니다. 뉴델리의 인센티브 에코시스템은 10년간 현지 생산량을 9배로 끌어올려 ASEAN 수출 회랑에 파급하는 규모를 창출했습니다. 광섬유의 부설과 OTT 컨텐츠의 현지화로 인도네시아, 베트남, 필리핀의 최초 구매자가 스마트 TV 시장에 진입하여 농촌 지역으로의 보급이 확대됩니다.

북미는 성숙하고 있으며, 교체 수요는 AI를 활용한 업스케일링과 FAST 채널 통합에 달려 있습니다. 광고주가 자금을 제공하는 서비스가 프리미엄 세트를 지원하고 클라우드 게임 지연 개선이 새로 고침 속도 사양을 높입니다. 유럽에서는 대형 8K 모델의 휘도에 상한을 마련하는 엄격한 에너지 절약법 EC 2024/1781에 임하고 있습니다. 이 법의 준수에 의해 피크 휘도 레벨의 박형화가 강요되고, 미니 LED의 채용이 촉진되어 마이크로 렌즈 어레이의 연구 개발에 박차가 걸립니다.

중동 및 아프리카는 보급률이 1자리대로 낮지만 인프라 투자 및 가처분소득 증가로 선행 여지가 있습니다. 아랍어 FAST 채널을 전개하는 지역 방송국이 컨텐츠 장벽을 제거합니다. 라틴아메리카에서는 수요가 양극화되고 있습니다. 프리미엄 세트가 도시의 부유층에 팔리고 있는 한편, 저가의 스트리밍 동글은 가격에 민감한 가구의 패널의 업그레이드를 늦추고 있습니다. 전반적으로 환율 변동은 제조업체를 유연한 조달과 헤지 전략으로 향하게 하여 시장 경쟁력을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 55-65인치 4K TV의 가격 하락에 의해 인도와 브라질에서 보급 가속

- 통신회사 주도의 광섬유 전개가 동남아시아 최초의 오너십 촉진

- FAST 채널 통합으로 북미에서의 업그레이드 수요 증가

- 인도에서는 정부의 PLI와 현지화 인센티브가 ASP 저하 초래

- 클라우드 게임 파트너십(Xbox, GeForce Now)이 120Hz 프리미엄 TV의 매출 견인

- Matter 인증의 상호 운용성에 의해 EU에서 교환 사이클 가속

- 시장 성장 억제요인

- 미니 LED 백라이트용 반도체의 압박에 의해 프리미엄 공급 제한

- 단편화된 OS 에코시스템이 앱 개발 비용 상승 초래

- EU 제2차 에너지 규제, 8K TV의 밝기 및 보급률 억제

- 가격에 민감한 시장에서 교환 사이클을 연장하는 저가격 스트리밍 동글

- 업계 밸류체인 분석

- 규제 및 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 해상도별

- HD 및 풀 HD

- 4K UHD

- 8K UHD

- 스크린 사이즈(인치)별

- 32인치 미만

- 33-45인치

- 46-55인치

- 56-65인치

- 65인치 이상

- 패널 및 디스플레이 기술별

- LED 및 액정

- OLED

- QLED

- 미니 LED

- 마이크로 LED

- 화면 형상별

- 플랫

- 커브

- 운영 체제별

- Android TV

- 기타 및 OEM 독자 사양

- 유통 채널별

- 오프라인 소매(하이퍼마켓, 브랜드 스토어)

- 온라인(전자상거래, D2C)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- TCL Technology Group Corp.

- Hisense Group Co., Ltd.

- Xiaomi Corporation

- Sony Group Corporation

- Vizio Holding Corp.

- Panasonic Holdings Corporation

- Sharp Corporation

- TPV Technology Limited(Philips)

- Skyworth Group Ltd.

- Konka Group Co., Ltd.

- Haier Smart Home Co., Ltd.

- Changhong Electric Co., Ltd.

- Toshiba Corporation

- OnePlus Technology(Shenzhen) Co., Ltd.

- VU Technologies Pvt. Ltd.

제7장 시장 기회 및 향후 전망

AJY 25.11.19The smart TV market size stands at USD 263.7 billion in 2025 and is projected to reach USD 301.4 billion by 2030, expanding at a 2.71% CAGR.

Momentum now comes less from first-time ownership surges and more from incremental improvements such as AI-driven picture processing, integrated cloud-gaming features and value-chain localization that compresses costs while preserving margins. India's expanded production-linked incentives and similar manufacturing credits in Vietnam and Mexico are fostering near-source assembly hubs that shorten lead times and lower average selling prices Ministry of Commerce & Industry. Display makers are steering R&D toward Mini-LED backlighting and quantum-dot enhancements that counter OLED's supply constraints, while telecom operators bundle televisions with fiber plans to widen addressable households. Platform competition is shifting toward ad-supported content services and extended software-support promises, encouraging premium replacements even in mature regions.

Global Smart TV Market Trends and Insights

Price Erosion of 55-65" 4 K Sets Accelerating Mass Adoption in India and Brazil

Chinese OEMs pushed 55-inch 4 K retail pricing below USD 400 in 2024, a threshold that once signaled the premium tier. Aggressive promotions, such as TCL's drop on 98-inch models from USD 5,999 to USD 1,999, compelled rivals to broaden entry-level line-ups while preserving margins through localized sourcing . Samsung's Indian unit still reported INR 10,000 crore television revenue in 2024, underscoring that brand-led AI features can hold price points even amid deflation Lower barriers entice middle-income households into larger-screen categories and compress replacement cycles across value-sensitive markets.

Telecom-Led Fiber Roll-outs Catalyzing First-Time Ownership in Southeast Asia

Nationwide fiber plans in Indonesia, Thailand and Malaysia are shrinking broadband subscription costs and enabling seamless 4 K streaming. Operators now bundle entry-level 43-inch televisions with 100 Mbps contracts, creating integrated service propositions that sidestep traditional retail channels. As viewing shifts from mobile devices to living-room screens, addressable demand moves beyond urban cores into tier-2 cities, sustaining outperformance against the global smart TV market through 2030.

Semiconductor Tightness for Mini-LED Backlights Limiting Premium Supply

Mini-LED sets need thousands of driver ICs and densely packed diodes; wafer-fab capacity for these parts lagged surging demand in 2024. TrendForce estimates Mini-LED television shipments grew 59% to 6.4 million units in 2024, overwhelming available component supply. Lead times stretched beyond 30 weeks, prompting brands to prioritise flagship lines and delay mid-tier adopters. Supply relief hinges on new 12-inch fabs slated to ramp only in late 2026.

Other drivers and restraints analyzed in the detailed report include:

- Government PLI and Localization Incentives Lowering ASPs in India

- Integration of FAST Channels Spurring Upgrade Demand in North America

- Low-Cost Streaming Dongles Extending Replacement Cycles in Price-Sensitive Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HD/Full HD still led revenue with 37.8% in 2024, sustained by cost-sensitive buyers in developing economies. Conversely, 8 K UHD is projected to compound at 4.2% and outsprint overall smart TV market growth through 2030. Samsung's Vision AI engine, rolled out in 2025, enhances lower-resolution streams to near-native 8 K quality and mitigates the shortage of ultra-high-bitrate content . EU ecodesign rules that limit peak brightness add pressure to engineer more efficient backlights, nudging brands toward Mini-LED over OLED for high-nit compliance.

Entry-level 4 K sets inherit premium features such as variable-refresh-rate gaming modes, blurring the mid-tier and expanding the total smart TV market. Content platforms also upscale catalogues to HDR10+ and Dolby Vision, reinforcing demand for higher-pixel-density panels that can render dynamic metadata accurately.

Mainstream 46-55-inch models captured 32.1% of the smart TV market in 2024. Average selling prices in this category fell 9% year on year after local assembly scaled in India and Mexico. Sets above 65 inches are forecast for a 3.8% CAGR and pull most premium technology attach-rates, including 120 Hz panels and object-tracking sound.

Manufacturers leverage shared glass-substrate fabs to push 98-inch LCDs below USD 2,000, making wall-sized viewing accessible to middle-income households. Pandemic-era home-theatre upgrades reconfigured living-room layouts, and those spatial changes now lock in preference for larger screens. Smaller than 32 inch remains viable for secondary rooms, yet the revenue mix shifts upward, underpinning profit pools despite moderate headline growth for the smart TV market.

The Smart TV Market Report is Segmented by Resolution (HD/Full HD, 4K UHD, and 8K UHD), Screen Size (Up To 32 Inch, 33-45 Inch, 46-55 Inch, and More), Panel/Display Technology (LED/LCD, OLED, QLED, Mini-LED, and More), Screen Shape (Flat, and Curved), Operating System (Android TV, and Other/OEM Proprietary), Distribution Channel (Offline Retail, and Online), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 41.2% of 2024 revenue and leads growth at 3.2% CAGR as domestic panel fabs in China and assembly hubs in India lower regional landed costs. New Delhi's incentive ecosystem boosted local output nine-fold over a decade, creating scale that reverberates across ASEAN exporting corridors. Fiber roll-outs and OTT content localisation bring first-time buyers in Indonesia, Vietnam and the Philippines into the smart TV market, expanding rural penetration.

North America is mature; replacement demand hinges on AI-powered upscaling and FAST-channel integration. Advertiser-funded services subsidise premium sets, and cloud-gaming latency improvements elevate refresh-rate specifications. Europe wrestles with stringent energy-efficiency law EC 2024/1781 that caps brightness for large 8 K models. Compliance forces thinner peak-luminance levels, prompting Mini-LED adoption and spurring R&D into micro-lens arrays.

Middle East and Africa trail with low single-digit penetration, yet infrastructure investments and rising disposable incomes signal headroom. Regional broadcasters rolling out Arabic-language FAST channels remove content barriers. Latin America shows bifurcated demand: premium sets sell into affluent urban districts, while low-cost streaming dongles slow panel upgrades in price-sensitive households. Throughout, currency volatility steers manufacturers toward flexible sourcing and hedging strategies to keep the smart TV market competitive.

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- TCL Technology Group Corp.

- Hisense Group Co., Ltd.

- Xiaomi Corporation

- Sony Group Corporation

- Vizio Holding Corp.

- Panasonic Holdings Corporation

- Sharp Corporation

- TPV Technology Limited (Philips)

- Skyworth Group Ltd.

- Konka Group Co., Ltd.

- Haier Smart Home Co., Ltd.

- Changhong Electric Co., Ltd.

- Toshiba Corporation

- OnePlus Technology (Shenzhen) Co., Ltd.

- VU Technologies Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Price Erosion of 55-65" 4K Sets Accelerating Mass Adoption in India and Brazil

- 4.2.2 Telecom-Led Fiber Roll-outs Catalyzing First-Time Ownership in Southeast Asia

- 4.2.3 Integration of FAST Channels Spurring Upgrade Demand in North America

- 4.2.4 Government PLI and Localization Incentives Lowering ASPs in India

- 4.2.5 Cloud-Gaming Partnerships (Xbox, GeForce Now) Driving 120 Hz Premium TV Sales

- 4.2.6 Matter-Certified Interoperability Boosting Replacement Cycles in EU

- 4.3 Market Restraints

- 4.3.1 Semiconductor Tightness for MiniLED Backlights Limiting Premium Supply

- 4.3.2 Fragmented OS Ecosystem Raising App Development Costs

- 4.3.3 EU Tier-2 Energy Rules Curbing 8K TV Brightness and Adoption Rates

- 4.3.4 Low-Cost Streaming Dongles Extending Replacement Cycles in Price-Sensitive Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Resolution

- 5.1.1 HD/Full HD

- 5.1.2 4K UHD

- 5.1.3 8K UHD

- 5.2 By Screen Size (Inches)

- 5.2.1 Upto 32

- 5.2.2 33-45

- 5.2.3 46-55

- 5.2.4 56-65

- 5.2.5 Above 65

- 5.3 By Panel/Display Technology

- 5.3.1 LED/LCD

- 5.3.2 OLED

- 5.3.3 QLED

- 5.3.4 Mini-LED

- 5.3.5 Micro-LED

- 5.4 By Screen Shape

- 5.4.1 Flat

- 5.4.2 Curved

- 5.5 By Operating System

- 5.5.1 Android TV

- 5.5.2 Other/OEM Proprietary

- 5.6 By Distribution Channel

- 5.6.1 Offline Retail (Hypermarket, Brand Stores)

- 5.6.2 Online (E-commerce, D2C)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Nordics

- 5.7.2.5 Rest of Europe

- 5.7.3 South America

- 5.7.3.1 Brazil

- 5.7.3.2 Rest of South America

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South-East Asia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Gulf Cooperation Council Countries

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Electronics Inc.

- 6.4.3 TCL Technology Group Corp.

- 6.4.4 Hisense Group Co., Ltd.

- 6.4.5 Xiaomi Corporation

- 6.4.6 Sony Group Corporation

- 6.4.7 Vizio Holding Corp.

- 6.4.8 Panasonic Holdings Corporation

- 6.4.9 Sharp Corporation

- 6.4.10 TPV Technology Limited (Philips)

- 6.4.11 Skyworth Group Ltd.

- 6.4.12 Konka Group Co., Ltd.

- 6.4.13 Haier Smart Home Co., Ltd.

- 6.4.14 Changhong Electric Co., Ltd.

- 6.4.15 Toshiba Corporation

- 6.4.16 OnePlus Technology (Shenzhen) Co., Ltd.

- 6.4.17 VU Technologies Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment