|

시장보고서

상품코드

1850949

항공기 통신 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aircraft Communication Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

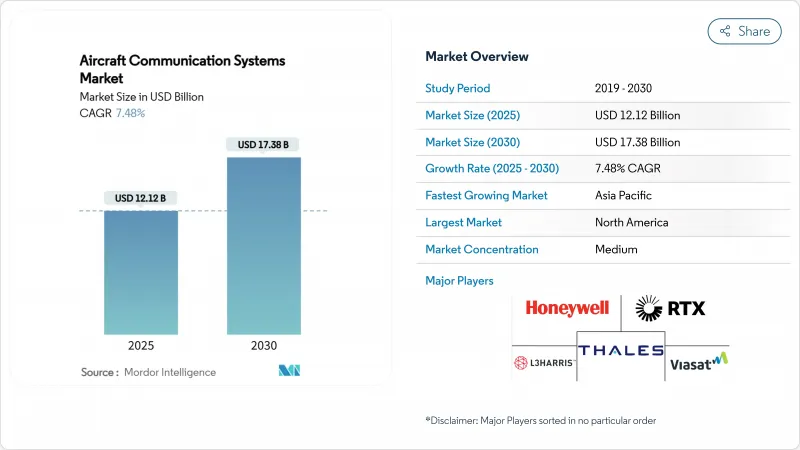

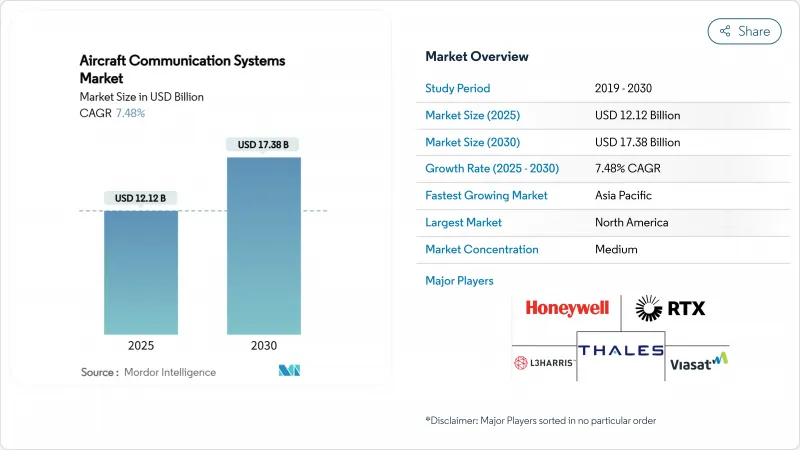

항공기 통신 시스템 시장 규모는 2025년 121억 2,000만 달러, 2030년에는 CAGR 7.48%로 성장하여 173억 8,000만 달러 규모에 이를 것으로 예측됩니다.

주요 성장 요인은 상업용, 방어용 및 신흥 도시형 에어 모빌리티 기계에서 중단 없는 안전한 다중 궤도 연결에 대한 수요가 증가하고 있다는 것입니다. 항공사는 연결성을 비용 센터에서 수익 서비스로 재지정하고 있는 반면, 방어 프로그램은 분쟁 환경을 위해 전술 데이터 링크와 위성 단말기를 계속 업그레이드하고 있습니다. 조종실 어비오닉스의 급속한 디지털화, CPDLC 및 ADS-B Out과 같은 규제의 의무화, AI 주도의 스펙트럼 관리는 모든 항공기 클래스에서 투자를 자극하고 있습니다. Gogo의 Satcom Direct 인수에서 볼 수 있는 연결 공급업체 간의 통합과 아시아태평양의 항공기의 지속적인 성장은 항공기 통신 시스템 시장의 기세를 더욱 강화하고 있습니다.

세계 항공기 통신 시스템 시장 동향과 통찰

SATCOM으로 기내 연결 급증

항공 아키텍처는 LEO, MEO, GEO의 각 용량을 결합한 멀티오비트 아키텍처로 전환하고 있으며 세계 리치를 유지하면서 지연 갭을 해소하고 있습니다. 델타 항공은 광대역 연결을 전략적 인프라로 간주하는 패러다임 시프트를 반영하여 400대 이상의 항공기에 퓨즈의 다중 궤도 솔루션을 선택했습니다. ThinKom의 Ka2517 안테나는 1,550대의 항공기로 1,700만 비행 시간을 기록하여 98%의 가용성을 나타내며 상호 운용성과 신뢰성을 증명하고 있습니다. 이러한 서비스 업그레이드는 높은 처리량 링크를 전체 함대에 채택하는 것을 촉진하는 레비뉴 공유 비즈니스 모델을 지원하고 항공기 통신 시스템 시장의 최상위 성장을 강화합니다.

ADS-B Out 및 CPDLC 의무화 일정

미국 공역에서는 ADS-B Out과 국내 CPDLC가 의무화되어 항공사는 VDL 모드 2 라디오와 통신 관리 유닛의 개조를 강요하고 있습니다. 병행하여 유럽에서는 2025년 1월부터 27,000kg 이상의 항공기의 자율 조난 추적이 의무화됩니다. 하니웰의 PM-CPDLC 보충 형식 인증서는 VHF 데이터 링크 라디오와 CMU를 사용하여 컴플라이언스에 대한 길을 제공합니다. 강제적인 일정은 단기적인 채택주기를 가속화하고 항공기 통신 시스템 수요를 높입니다.

인증 및 DO-178/DO-254 비용 부담

DO-178C 및 DO-254의 검증 비용은 멀티코어 및 AI 지원 어비오닉스에서 급증합니다. 콜린스 에어로스페이스의 모사르크 아키텍처(최근 FAA에 의해 승인됨)는 인증 비용에 비례하지 않고 75%의 처리 능력 향상을 보여주지만, 전체 비용은 여전히 역풍이 되고 있습니다. 소규모 OEM은 자원 제약에 직면하고 있으며 항공기 통신 시스템 시장의 중기 성장을 부분적으로 억제하고 있습니다.

부문 분석

안테나는 2024년 항공기 통신 시스템 시장 점유율의 39.89%를 차지하며, 멀티 궤도 위성을 위해 설계된 전자 제어 어레이가 견인하고 있습니다. Satcom Direct의 Plane Simple Ka-band ESA는 장거리 플릿에서 선호되는 고이득, 얇은 설계의 대표적인 예입니다. 디스플레이 및 프로세서 카테고리는 2030년까지 연평균 복합 성장률(CAGR) 9.67%로 성장할 것으로 예측되며, 조종석의 컴퓨팅 능력을 75% 늘리는 Collins Aerospace사의 FAA 인증 멀티 코어 칩이 지원합니다. 디스플레이 및 프로세서 항공기 통신 시스템 시장 규모는 레거시 하드웨어보다 가파른 경사입니다. 트랜스폰더는 후발기가 ADS-B의 의무에 대응함에 따라 안정적인 수요를 유지하고, 통신 관리 유닛(CMU)은 CPDLC의 전개에 의해 이익을 올리고 있습니다. 군용 대책 라디오와 SWaP 최적화 SDR 모듈은 컴포넌트 수요를 마무리하고 항공기 통신 시스템 시장의 폭을 넓히고 있습니다.

역사적으로 볼 때 하드웨어 중심의 성장은 소프트웨어 정의 기능에 대한 길을 옮겼습니다. Thales의 FlytX 햅틱 디스플레이는 크기와 전력 소비를 30% 줄이고 증분 인증을 지원하며 모듈화가 업그레이드 사이클을 재구성하는 방법을 보여줍니다. 모듈형 어비오닉스가 보급됨에 따라 조달량은 고정 안테나에서 프로세싱 플랫폼으로 이동하고 라이프사이클 수익은 항공기 통신 시스템 시장 전반에 걸쳐 균형을 유지하고 있습니다.

민간 제트기는 항공사가 광대역 연결 및 규정 준수를 선호했기 때문에 2024년 수익의 53.67%를 창출했습니다. 보잉사의 스피릿 에어로시스템즈 인수계획은 에비오닉스 통합의 수직통합을 강화하는 것을 시사하고 있으며, 이로써 내로우 바디기의 생산라인 전체에 있어서의 통신시스템의 설치가 간소화될 것입니다. 도시-항공 기동성(UAM) 프로그램은 하니웰의 Anthem 비행 데크가 Vertical Aerospace의 VX4에 탑재됨으로써 항공기 통신 시스템 시장에서 가장 빠른 CAGR 11.45%를 보일 것으로 예측됩니다. 군용기의 자금 조달은 E-130J TACAMO와 Link-16의 현대화 계약에 상징되는 것처럼 여전히 중요합니다. 비즈니스 항공기는 봄바르디아 하니웰과의 다년 계약을 포함한 장거리 캐빈 SATCOM 업그레이드를 통해 수량을 늘리고 있습니다. 지역 제트는 확장되는 APAC 플릿 전반에 걸쳐 수요를 유지하며, 무인 시스템은 고급 SDR과 AI 프로세서를 통합하여 항공기 통신 시스템 시장에서 전술 이용 사례를 심화시키고 있습니다.

지역 분석

북미는 FAA의 근대화 프로그램과 지속적인 군사비로 2024년 매출의 35.85%를 유지했습니다. FAA에 의한 4,600개의 ATC 시설에 걸친 통신 인프라의 오버홀은 계속되고 있으며, 무선기, 데이터 링크, 스펙트럼 관리의 업그레이드를 위한 견고한 국내 시장을 제공합니다. 미국 방어 계약(2억 6,900만 달러의 BACN 작업 주문 포함)은 2027년까지 조달 전망을 강화합니다.

아시아태평양은 가장 성장하는 지역이며 2030년까지 연평균 복합 성장률(CAGR)은 8.42%를 나타낼 전망입니다. 항공기 통신 시스템 시장에 대한 투자는 중국, 인도, 동남아시아의 함대 증가를 반영합니다. 중국 텔레콤은 1,000 미만의 타워에서 전국적인 5G 공대지 통신을 시험적으로 실시하고 있으며, 인도는 확대하는 전투기 재고에 Vayulink 보안 무선 네트워크를 탑재하고 있습니다. 태국 항공과 같은 지역 항공사는 SES의 다중 궤도 연결을 채택하고 첨단 SATCOM에 대한 상업적 인계를 강조합니다.

유럽은 엄격한 규제 리더십으로 확고한 지위를 유지하고 있습니다. ICAO가 갱신한 미래의 항공항법규격은 사이버에 강한 데이터 교환을 의무화하고 있으며, 암호화 링크 관리의 채택에 박차를 가하고 있습니다. 탈레스와 스파이어 세계은 우주 기반의 ADS-B 모니터링을 제공하기 위해 100개 이상의 위성을 배치하고 있으며, 2027년 서비스를 시작할 예정입니다. Airbus HBCplus는 공기 저항과 연료 소비를 줄이는 통합 멀티 궤도 터미널을 제공하며 항공기 통신 시스템 시장에 OEM 수준의 영향력을 강조합니다.

남미, 중동 및 아프리카는 함대의 갱신이나 전략적 방어 프로젝트에 추진되어 완만하지만 수요 증가에 기여하고 있습니다. 지상 인프라가 드물기 때문에 이러한 지역에서는 하이브리드 ATG/SATCOM 솔루션이 매력적이며, 항공기 통신 시스템 시장은 세계적으로 다양한 성장 패턴을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- SATCOM 기반 기내 연결성 급증

- ADS-B Out 및 CPDLC 규정 준수의 필수 타임라인

- APAC 내로우 바디 기군의 확대

- 보안 통신을 위한 군용 함대 개조 프로그램

- 항공전자기기 전체에 걸친 소프트웨어 정의 무선의 통합

- 동적 스펙트럼 이용을 위한 AI 구동형 인지 무선

- 시장 성장 억제요인

- 인증과 DO-178/DO-254의 비용 부담

- IP 기반 항공 전자 기기 네트워크의 사이버 취약성

- RF 스펙트럼의 혼잡과 간섭 위험

- RF 칩셋용 반도체 공급 부족

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 구성요소별

- 트랜스폰더

- SATCOM 터미널

- 안테나

- 디스플레이와 프로세서

- 통신 관리 유닛

- 기타 컴포넌트

- 항공기유형별

- 민간 항공기

- 내로우 바디

- 와이드 바디

- 지역 제트

- 비즈니스 제트

- 군용기

- 파이터

- 수송

- 특별 임무

- 무인 항공기(UAV)

- 도시형 항공 모빌리티/eVTOL

- 민간 항공기

- 시스템별

- 무선 통신 시스템

- 인터폰 통신 시스템

- 승객 주소 시스템

- 디지털 라디오 및 오디오 통합 관리 시스템

- 항공기 통신 주소 및 보고 시스템(ACARS)

- 커넥티비티 테크놀로지별

- SATCOM(L/Ku/Ka 밴드)

- VHF/HF 음성

- 공대지(ATG/5G-ATG)

- 전술 데이터 링크(Link-16, MADL)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- Northrop Grumman Corporation

- THALES Group

- RTX Corporation

- L3Harris Technologies, Inc.

- General Dynamics Corporation

- Iridium Satellite LLC

- Kratos Defense & Security Solutions, Inc.

- ViaSat Inc.

- Rohde & Schwarz GmbH & Co. KG

- Gogo Inc.

- Elbit Systems Ltd.

- BAE Systems plc

- Garmin Ltd.

- Orbit Communication Systems Ltd.

- Astronics Corporation

- Safran Electronics & Defense(Safran SA)

제7장 시장 기회와 장래의 전망

SHW 25.11.11The aircraft communication systems market size reached a value of USD 12.12 billion in 2025 and is projected to achieve a market size of USD 17.38 billion by 2030, reflecting a 7.48% CAGR.

The main growth catalyst is increasing demand for uninterrupted, secure, and multi-orbit connectivity across commercial, defense, and emerging urban-air-mobility fleets. Airlines are re-positioning connectivity from a cost center to a revenue service, while defense programs continue to upgrade tactical datalinks and satellite terminals for contested environments. Rapid digitalization of cockpit avionics, regulatory mandates such as CPDLC and ADS-B Out, and AI-driven spectrum management are stimulating investment across all aircraft classes. Consolidation among connectivity suppliers-seen in Gogo's Satcom Direct purchase-and sustained fleet growth in Asia-Pacific further reinforce momentum for the aircraft communication systems market.

Global Aircraft Communication Systems Market Trends and Insights

SATCOM-enabled in-flight connectivity surge

Airlines are transitioning to multi-orbit architectures that combine LEO, MEO, and GEO capacity to eliminate latency gaps while preserving global reach. Delta Air Lines selected a Hughes multi-orbit solution for more than 400 aircraft, reflecting a paradigm shift toward viewing broadband connectivity as strategic infrastructure. ThinKom's Ka2517 antennas have logged 17 million flight hours with 98% availability across 1,550 aircraft, proving interoperability and reliability. These service upgrades underpin revenue-sharing business models that encourage fleet-wide adoption of high-throughput links, reinforcing top-line growth for the aircraft communication systems market.

Mandatory ADS-B Out and CPDLC compliance timelines

ADS-B Out and domestic CPDLC are now required across US airspace, compelling airlines to retrofit VDL Mode 2 radios and communication management units. Parallel European mandates extend to autonomous distress tracking for aircraft above 27,000 kg from January 2025. Honeywell's PM-CPDLC Supplemental Type Certificate offers a ready pathway to compliance using VHF Data Link radios and CMUs. Compulsory timelines accelerate near-term adoption cycles, lifting the demand for aircraft communication systems.

Certification and DO-178/DO-254 cost burden

DO-178C and DO-254 verification costs rise sharply for multi-core and AI-enabled avionics. Collins Aerospace's Mosarc architecture-recently cleared by the FAA-shows a 75% processing uplift without proportional certification costs, yet overall expense remains a headwind. Smaller OEMs face resource constraints, partially tempering the aircraft communication systems market in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of APAC narrowbody aircraft fleet

- Military fleet retrofit programs for secure communications

- Cyber-vulnerabilities in IP-based avionics networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Antennas captured 39.89% of the aircraft communication systems market share in 2024, led by electronically steered arrays designed for multi-orbit satellites. Satcom Direct's Plane Simple Ka-band ESA exemplifies a high-gain, low-profile design favored on long-haul fleets. The displays and processors category is forecasted to grow at a 9.67% CAGR through 2030, underpinned by Collins Aerospace's FAA-certified multi-core chips that lift cockpit computing capacity by 75%. The aircraft communication systems market size for displays and processors is on a steeper trajectory than legacy hardware. Transponders maintain steady demand as late-adopters meet ADS-B mandates, while communication management units (CMUs) gain from CPDLC roll-outs. Military counter-measure radios and SWaP-optimized SDR modules round out component demand, extending the breadth of the aircraft communication systems market.

A historical look shows hardware-centric growth, which has given way to software-defined functionality. Thales' FlytX tactile display reduces size and power by 30% and supports incremental certification, illustrating how modularity reshapes upgrade cycles. As modular avionics proliferate, procurement volumes migrate from fixed antennas toward processing platforms, keeping lifecycle revenues balanced across the aircraft communication systems market.

Commercial jets generated 53.67% of 2024 revenue as airlines prioritized broadband connectivity and regulatory compliance. Boeing's plan to acquire Spirit AeroSystems signals greater vertical control of avionics integration, which should streamline communication-system fit-outs across narrowbody production lines. Urban-air-mobility (UAM) programs are projected to post an 11.45% CAGR, the fastest in the aircraft communication systems market, driven by Honeywell's Anthem flight deck on Vertical Aerospace's VX4. Military aircraft funding remains significant, illustrated by the E-130J TACAMO and Link-16 modernization contracts. Business aviation adds incremental volume through long-range cabin SATCOM upgrades, such as Bombardier's multi-year agreement with Honeywell. Regional jets sustain demand across the expanding APAC fleet, while unmanned systems integrate advanced SDRs and AI processors, deepening tactical use cases within the aircraft communication systems market.

The Aircraft Communication Systems Market is Segmented by Components (Transponder, Display and Processors, Antennas, and More), Aircraft Type (Commercial Aircraft, Military Aircraft, and More), System (Radio Communication System, and More), Connectivity Technology (SATCOM, Tactical Data Links, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 35.85% of 2024 revenue thanks to FAA modernization programs and sustained military spending. The FAA's telecommunication infrastructure overhaul across 4,600 ATC facilities continues, providing a robust domestic market for radios, datalinks, and spectrum-management upgrades. US defense contracts-including a USD 269 million BACN task order-reinforce procurement visibility through 2027.

Asia-Pacific is the fastest-growing region, increasing at an 8.42% CAGR through 2030. Aircraft communication systems market investments mirror rising fleets in China, India, and Southeast Asia. China Telecom is piloting nationwide 5G air-to-ground coverage with fewer than 1,000 towers, while India is fitting Vayulink secure radio networks onto its expanding fighter inventory. Regional carriers like Thai Airways have adopted SES multi-orbit connectivity, highlighting commercial pull for advanced SATCOM.

Europe maintains a solid position owing to stringent regulatory leadership. ICAO's updated future air navigation standards mandate cyber-resilient data exchange, spurring adoption of encrypted link management. Thales and Spire Global are deploying 100+ satellites to deliver space-based ADS-B surveillance, slated for 2027 service entry. Airbus HBCplus offers integrated multi-orbit terminals that reduce drag and fuel burn, underlining OEM-level influence on the aircraft communication systems market.

South America, the Middle East, and Africa contribute moderate but growing demand, leveraged by fleet renewals and strategic defense projects. Owing to sparse terrestrial infrastructure, hybrid ATG/SATCOM solutions appeal in these geographies, sustaining a globally diversified growth pattern for the aircraft communication systems market.

- Honeywell International Inc.

- Northrop Grumman Corporation

- THALES Group

- RTX Corporation

- L3Harris Technologies, Inc.

- General Dynamics Corporation

- Iridium Satellite LLC

- Kratos Defense & Security Solutions, Inc.

- ViaSat Inc.

- Rohde & Schwarz GmbH & Co. KG

- Gogo Inc.

- Elbit Systems Ltd.

- BAE Systems plc

- Garmin Ltd.

- Orbit Communication Systems Ltd.

- Astronics Corporation

- Safran Electronics & Defense (Safran SA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 SATCOM-enabled in-flight connectivity surge

- 4.2.2 Mandatory ADS-B Out and CPDLC compliance timelines

- 4.2.3 Expansion of APAC narrowbody aircraft fleet

- 4.2.4 Military fleet retrofit programs for secure comms

- 4.2.5 Software-defined radio integration across avionics

- 4.2.6 AI-driven cognitive radios for dynamic spectrum use

- 4.3 Market Restraints

- 4.3.1 Certification and DO-178/DO-254 cost burden

- 4.3.2 Cyber-vulnerabilities in IP-based avionics networks

- 4.3.3 RF spectrum congestion and interference risk

- 4.3.4 Semiconductor supply shortages for RF chipsets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Transponders

- 5.1.2 SATCOM Terminals

- 5.1.3 Antennas

- 5.1.4 Displays and Processors

- 5.1.5 Communication Management Units

- 5.1.6 Other Components

- 5.2 By Aircraft Type

- 5.2.1 Commercial Aircraft

- 5.2.1.1 Narrowbody

- 5.2.1.2 Widebody

- 5.2.1.3 Regional Jets

- 5.2.1.4 Business Jets

- 5.2.2 Military Aircraft

- 5.2.2.1 Fighter

- 5.2.2.2 Transport

- 5.2.2.3 Special-mission

- 5.2.3 Unmanned Aerial Vehicles (UAVs)

- 5.2.4 Urban Air Mobility/eVTOL

- 5.2.1 Commercial Aircraft

- 5.3 By System

- 5.3.1 Radio Communication System

- 5.3.2 Interphone Communication System

- 5.3.3 Passenger Address System

- 5.3.4 Digital Radio and Audio Integrating Management System

- 5.3.5 Aircraft Communications Addressing and Reporting System (ACARS)

- 5.4 By Connectivity Technology

- 5.4.1 SATCOM (L/Ku/Ka-band)

- 5.4.2 VHF/HF Voice

- 5.4.3 Air-to-Ground (ATG/5G-ATG)

- 5.4.4 Tactical Data Links (Link-16, MADL)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Honeywell International Inc.

- 6.4.2 Northrop Grumman Corporation

- 6.4.3 THALES Group

- 6.4.4 RTX Corporation

- 6.4.5 L3Harris Technologies, Inc.

- 6.4.6 General Dynamics Corporation

- 6.4.7 Iridium Satellite LLC

- 6.4.8 Kratos Defense & Security Solutions, Inc.

- 6.4.9 ViaSat Inc.

- 6.4.10 Rohde & Schwarz GmbH & Co. KG

- 6.4.11 Gogo Inc.

- 6.4.12 Elbit Systems Ltd.

- 6.4.13 BAE Systems plc

- 6.4.14 Garmin Ltd.

- 6.4.15 Orbit Communication Systems Ltd.

- 6.4.16 Astronics Corporation

- 6.4.17 Safran Electronics & Defense (Safran SA)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment