|

시장보고서

상품코드

1851024

항공 사이버 보안 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aviation Cyber Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

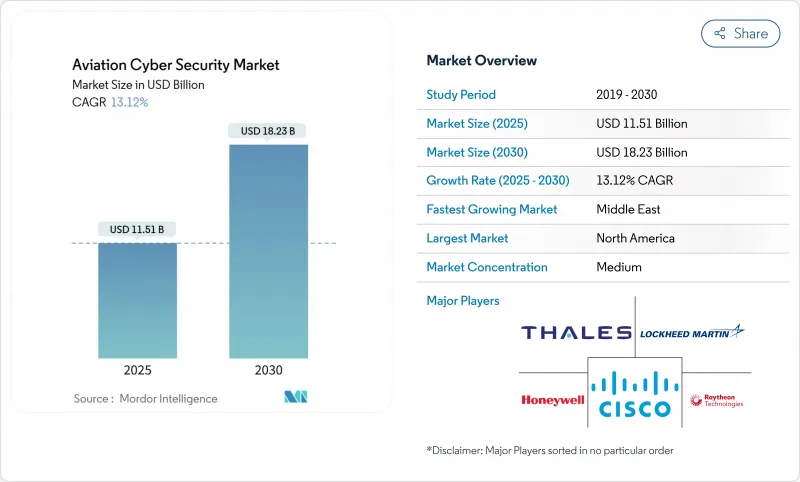

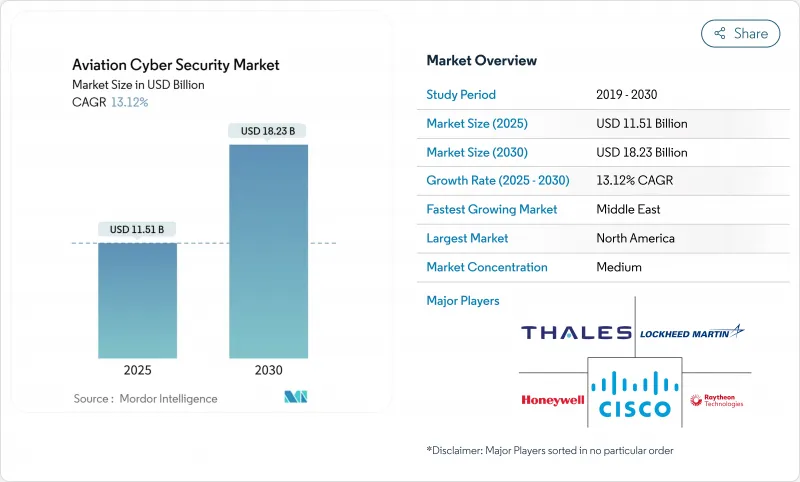

항공 사이버 보안 시장 규모는 2025년 115억 1,000만 달러, 2030년 182억 3,000만 달러에 이르고, 예측 기간 중 CAGR은 13.12%를 나타낼 전망입니다.

2020년 이후 사이버 공격 빈도 상승, 클라우드로의 급속한 전환, 공항, 항공기, 항공 관제(ATC) 시스템에 걸친 연결 자산의 급증이 이 확대를 뒷받침하고 있습니다. 북미의 규제 자금 조달, 유럽의 규칙 조화, 중동의 인프라 정비가 총체적으로 지출 수준을 올리고 있습니다. 기술 우선순위는 제로 트러스트 아키텍처, 관리형 감지 및 응답 서비스, 양자 안전 암호화로 이동하는 반면, 항공 분야의 보안 인력 부족이 계속되는 이 분야를 해결하기 위해 운영자는 아웃소싱을 추구하고 있습니다. 기존 벤더와 틈새 벤더의 합병이 활발해지고, 항공 사이버 보안 시장 전체의 운영 기술(OT) 보호, 위협 인텔리전스, 컴플라이언스 자동화에 있어서의 능력 격차의 해소를 목표로 하고 있습니다.

세계 항공 사이버 보안 시장 동향 및 통찰

통합 디지털 항공 생태계 급증으로 사이버 공격 대상 확대

승객 서비스, 공항 OT, 항공기 데이터 링크 및 제3자물류의 융합은 항공 사이버 보안 시장을 재정의합니다. 2024년 8월, 시애틀 항구의 정보 유출이 주변 시스템을 다운시키고 비행의 안전이 유지되고 있어도 옆의 움직임이 어떻게 업무를 혼란시키는지를 입증했습니다. 미국 운수 보안청은 2025년도를 기준으로 1억 3,617만 달러를 항공에 특화된 사이버 방어에 할당해, 경계 중심의 전략이 더 이상 충분하지 않다는 신호를 보냈습니다. 이해관계자들은 현재 항공사이버 보안 시장 전체의 상호 의존성을 매핑하고 안전성을 보장하는 전반적인 아키텍처를 선호하고 있습니다.

항공기에서 개방형 아키텍처 어비오닉스 및 IoT 센서의 신속한 채택

개방형 표준은 라이프사이클 비용을 절감하고 플러그 앤 플레이 업그레이드를 가능하게 하지만 플릿 전체에 동일한 취약점을 전파합니다. FAA의 2024년 8월 제안은 유지보수용 노트북, 공항 Wi-Fi, 비행 크리티컬한 영역으로 전환할 수 있는 Bluetooth 센서에 의한 위험을 강조하고 있습니다. 충돌 회피 트랜스폰더의 결함을 노출시킨 CISA 권고는 긴급성을 높이고 있습니다. 따라서 항공사와 OEM은 보안 코딩 실천과 런타임 모니터링을 융합시켜 항공 사이버 보안 시장의 시스템 노출을 줄여야 합니다.

통합 보안 거버넌스를 방해하는 단편화된 레거시 시스템

국방산업기반 조사에 따르면 항공사의 98%는 사이버 인시던트에 휩싸인 공급망 파트너십을 유지하고 있으며 수십년전의 ATC와 수하물 네트워크에 위험이 전파되고 있습니다. 암호화, 다중 요소 인증 및 중앙 집중식 로깅은 많은 레거시 노드에 존재하지 않으므로 항공사는 심각한 격차를 유지하면서 비용을 증가시키는 중복 관리를 수행해야합니다.

부문 분석

위협 인텔리전스 및 응답 솔루션은 2024년 매출의 28%를 차지했으며, 이 분야가 능동적인 감시로 전환되고 있음을 보여줍니다. 관리형 보안 서비스는 2030년까지 13.8%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다. 이 기세는 항공 리터러시가 높은 분석가의 수가 제한되어 있고 사내 인력을 늘리지 않고도 24시간 365일의 규제 로깅 의무에 대응할 필요가 있기 때문입니다.

OEM과 항공사는 SIEM, OT 이상 감지, 컴플라이언스 대시보드를 번들한 매니지드 서비스에 주목하고 있습니다. 매니지드 서비스의 항공 사이버 보안 시장 규모는 인시던트 보고 의무의 타임라인 및 제로 트러스트 배포와 연계하여 확대될 것으로 예측됩니다. 벤더 차별화의 중심은 일반 SOC 인력 배치 모델보다 아비오닉스 및 ATC 워크플로우와 통합할 수 있는 비행 인증 엔지니어의 보유에 있습니다.

네트워크 보안은 2024년 지출액의 32%를 유지하며 경계 방화벽에 대한 의존도가 여전히 높다는 것을 뒷받침합니다. 그러나 클라우드 보안은 멀티클라우드, 컨테이너화된 워크로드를 통해 승객 체크인, 승무원 로스터링, 예지 보전 등이 On-Premise로 전환되기 때문에 CAGR 15.1%로 성장을 이끌고 있습니다. 클라우드 제어 항공 사이버 보안 시장 규모는 공유 책임 교육 캠페인과 규제 부문에 맞춘 주권 클라우드 지역의 전개로부터 혜택을 받습니다.

엔드포인트 보호는 크루 태블릿에서 엔진 헬스 센서에 이르기까지 확장되며, 공급업체는 서로 다른 하드웨어간에 정책 엔진을 통합해야 합니다. 용도 수준의 방화벽, API 게이트웨이, 런타임 코드 스캔도 SaaS 비행 계획 도구가 항공 사이버 보안 시장에서 출시되기 전에 사이버 및 안전 감사를 모두 통과해야 하므로 가속화됩니다.

지역 분석

북미는 항공 사이버 보안 시장을 선도하고 2024년 매출은 40%에 달했습니다. 2026년 FAA의 3,500만 달러 사이버 보안 항목과 TSA의 1억 3,617만 달러의 공항 강화를 위한 할당이 지원되고 있습니다. 미국의 주요 항공사는 모두 AI에 의한 위협 감지를 도입하고 있으며 캐나다의 ANSP인 NAV CANADA는 연방 정부의 모범 사례를 반영한 제로 트러스트 설계도를 채택하고 있습니다. 이 지역의 벤더 생태계는 방어 프라임이 하드화된 솔루션을 민간 항공기로 교차 판매함으로써 이익을 얻고 있습니다.

유럽에서는 EASA Part-IS와 EUROCONTROL CERT의 조정을 통해 견고한 채택이 유지되고 있습니다. 일반 EU 조화는 중복을 줄이고 풀링된 정보 공유를 증가시킵니다. 방어를 위한 신뢰할 수 있는 GenAI 개발을 위한 탈레스와 CEA와의 3년간의 AI 파트너십은 감지와 대응 가속을 목표로 하는 지역의 혁신을 강조하고 있습니다. GDPR(EU 개인정보보호규정)은 새로운 컴플라이언스 차원을 추가하여 항공 사이버 보안 시장에서 프라이버시 바이 디자인의 암호화와 토큰화 노력을 촉진합니다.

중동에서는 걸프 국가의 허브 공항 확대와 2024년 1분기에 183%의 DDoS 급증이 기록됨에 따라 CAGR이 12.5%에 달하여 사업자는 여러 공항 포트폴리오를 신속하게 보호해야 합니다. 이 지역의 플래그 캐리어는 현재 지상 시스템의 관리형 SOC 커버리지를 의무화하고 있으며, 스푸핑에 대응하기 위해 위성 경로의 다양성을 전개하고 있습니다. 중국, 일본, 인도가 주도하는 아시아태평양은 대규모 항공기 증비, 정부의 스마트 에어포트 보조금, 2024년 9월 델리에서 개최되는 이 지역 최초의 각료급 항공·사이버 정상 회담을 통해 바로 뒤를 이어가고 있습니다. 다양한 규제 기준은 국제 공급업체와 지역 전문가 모두에게 다양한 인증 제도를 지원하는 제품의 현지화를 촉구합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 통합된 디지털 항공 생태계의 급증으로 사이버 공격 대상이 확대

- 항공기의 오픈 아키텍처 어비오닉스와 IoT 센서의 급속한 채택

- 클라우드 기반 공항 운영 플랫폼과 SaaS 형 비행 용도의 성장

- 제로 신뢰 보안이 요구되는 ATC 네트워크에서 5G와 위성 연결의 통합

- 시큐리티 바이 디자인을 도입하는 eVTOL과 도시형 에어 모빌리티 사업자의 대두

- 시장 성장 억제요인

- 통합된 보안 거버넌스를 막는 분산된 레거시 시스템

- 신흥 시장에 있어서의 항공 분야의 사이버 시큐리티 전문가의 부족

- 높은 인증 및 내공성 검증 비용으로 배치 지연

- 지역 공항과 일반 공항의 한정된 예산 배분

- 산업 밸류체인 분석

- 규제와 컴플라이언스의 전망

- 기술 스냅샷(신흥 툴, AI/ML, 양자 내성 암호)

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장에 주는 거시경제 동향의 평가

제5장 시장 규모와 성장 예측 수치

- 솔루션별

- 위협 인텔리전스 및 응답

- 아이덴티티와 액세스 관리

- 데이터 유출 방지

- 보안 및 취약성 관리

- 관리 보안

- 보안 유형별

- 네트워크 보안

- 엔드포인트 보안

- 용도 보안

- 클라우드 보안

- 무선 및 위성 링크의 보안

- 전개 모드별

- On-Premise

- 클라우드 배포

- 용도별

- 항공사 경영

- 항공화물 관리

- 공항 관리

- 항공교통관제관리

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향(MandA, JV, 제품 출시)

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- Cisco Systems Inc.

- Thales Group

- Raytheon Technologies Corporation

- BAE Systems plc

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Collins Aerospace

- Unisys Corporation

- Palo Alto Networks Inc.

- SITA SC

- Leidos Holdings Inc.

- IBM Corporation

- Airbus CyberSecurity

- The Boeing Company

- Darktrace plc

- Fortinet Inc.

- Trend Micro Inc.

- Telespazio SpA

- Rohde and Schwarz GmbH and Co KG

- Cyberbit Ltd.

제7장 시장 기회와 장래의 전망

SHW 25.11.11The aviation cyber security market size is valued at USD 11.51 billion in 2025 and is projected to reach USD 18.23 billion by 2030, reflecting a solid 13.12% CAGR during the forecast window.

Rising cyber-attack frequency since 2020, rapid cloud migration, and the surge of connected assets across airports, aircraft, and air traffic control (ATC) systems underpin this expansion. North American regulatory funding, European harmonized rules, and Middle-Eastern infrastructure build-outs collectively elevate spending levels. Technology priorities are shifting toward zero-trust architectures, managed detection-and-response services, and quantum-safe encryption, while operators pursue outsourcing to address the sector's persistent shortage of aviation-domain security talent. Intensifying merger activity among incumbents and niche vendors aims to close capability gaps in operational-technology (OT) protection, threat intelligence, and compliance automation across the aviation cyber security market.

Global Aviation Cyber Security Market Trends and Insights

Surge in Integrated Digital Aviation Ecosystems Expanding Cyber-Attack Surface

The convergence of passenger services, airport OT, aircraft data links, and third-party logistics is redefining the aviation cyber security market. In August 2024 a Port of Seattle breach brought down peripheral systems, demonstrating how lateral movement can disrupt operations even when flight safety is maintained. US Transportation Security Administration allocated USD 136.17 million toward aviation-focused cyber defenses for FY 2025, signaling that perimeter-centric strategies are no longer sufficient. Stakeholders now prioritize holistic architectures that map and secure interdependencies across the entire aviation cyber security market.

Rapid Adoption of Open-Architecture Avionics & IoT Sensors in Aircraft Fleets

Open standards cut lifecycle costs and enable plug-and-play upgrades, yet they propagate identical vulnerabilities across fleets. The FAA's August 2024 proposal underscores risks from maintenance laptops, airport Wi-Fi, and Bluetooth sensors that can pivot to flight-critical domains. CISA advisories exposing flaws in collision-avoidance transponders add urgency. Airlines and OEMs thus must blend secure-coding practices with runtime monitoring to mitigate systemic exposure within the aviation cyber security market.

Fragmented Legacy Systems Hindering Unified Security Governance

Defense Industrial Base studies find that 98% of aviation organizations sustain supply-chain partnerships hit by cyber incidents, propagating risk across decades-old ATC and baggage networks. Encryption, multifactor authentication, and centralized logging remain absent from many legacy nodes, forcing airlines to juggle redundant controls that inflate cost while leaving material gaps.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Cloud-Based Airport Operations Platforms & SaaS Flight Applications

- Integration of 5G & Satellite Connectivity in ATC Networks Requiring Zero-Trust Security

- High Certification & Air-Worthiness Validation Costs Delaying Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Threat Intelligence & Response solutions captured 28% of 2024 revenue within the aviation cyber security market share, evidencing the sector's pivot to proactive monitoring. Managed Security Services exhibit a 13.8% CAGR through 2030. This momentum stems from a limited pool of aviation-literate analysts and the need to meet 24X7 regulatory logging mandates without inflating internal headcount.

OEMs and airlines turn to managed offerings that bundle SIEM, OT anomaly detection, and compliance dashboards. The aviation cyber security market size for managed services is forecast to increase in tandem with mandatory incident-reporting timelines and zero-trust rollouts. Vendor differentiation now centers on possessing flight-certified engineers able to integrate with avionics and ATC workflows rather than generic SOC staffing models.

Network Security retained 32% of 2024 spend, underlining residual reliance on perimeter firewalls. Yet Cloud Security leads growth at a 15.1% CAGR as multi-cloud, containerized workloads move passenger check-in, crew rostering, and predictive maintenance off-premise. The aviation cyber security market size for cloud controls benefits from shared-responsibility education campaigns and the rollout of sovereign-cloud regions tailored for regulated sectors.

Endpoint protection stretches from crew tablets to engine-health sensors, compelling vendors to unify policy engines across distinct hardware. Application-level firewalls, API gateways, and runtime code-scanning also accelerate because SaaS flight-planning tools must pass both cyber and safety audits before release in the aviation cyber security market.

The Aviation Cyber Security Market is Segmented by Solution (Threat Intelligence and Response, Identity and Access Management, Data Loss Prevention, and More), Security Type (Network Security, Endpoint Security, Application Security, and More), Deployment Mode (On-Premise, Cloud-Deployed), Application (Airline Management, Air Cargo Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads the aviation cyber security market with 40% revenue in 2024, underpinned by the FAA's USD 35 million cybersecurity line item for FY 2026 and TSA's USD 136.17 million allocation to harden airports. All major U.S. carriers now embed AI-driven threat detection, and Canadian ANSP NAV CANADA adopts zero-trust blueprints mirroring federal best practices. The region's vendor ecosystem also benefits from defense primes cross-selling hardened solutions into commercial fleets.

Europe maintains robust adoption through EASA Part-IS and EUROCONTROL CERT coordination. Pan-EU harmonization reduces duplication and increases pooled intelligence sharing. Thales' three-year AI partnership with CEA to develop trusted GenAI for defense highlights regional innovation targeted at detection-and-response acceleration. GDPR adds another compliance dimension, prompting privacy-by-design encryption and tokenization efforts inside the aviation cyber security market.

The Middle East posts a 12.5% CAGR driven by Gulf hub expansion and a documented 183% DDoS spike during Q1 2024, pushing operators to secure multi-airport portfolios rapidly. Flag carriers in the region now mandate managed SOC coverage for ground systems and deploy satellite-route diversity to counter spoofing attempts. Asia-Pacific, led by China, Japan, and India, follows close behind through large-scale fleet additions, government smart-airport grants, and the region's first ministerial aviation-cyber summit hosted in Delhi in September 2024. Diverse regulatory baselines encourage both international vendors and regional specialists to localize offerings for different certification regimes.

- Honeywell International Inc.

- Cisco Systems Inc.

- Thales Group

- Raytheon Technologies Corporation

- BAE Systems plc

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Collins Aerospace

- Unisys Corporation

- Palo Alto Networks Inc.

- SITA SC

- Leidos Holdings Inc.

- IBM Corporation

- Airbus CyberSecurity

- The Boeing Company

- Darktrace plc

- Fortinet Inc.

- Trend Micro Inc.

- Telespazio S.p.A.

- Rohde and Schwarz GmbH and Co KG

- Cyberbit Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Integrated Digital Aviation Ecosystems Expanding Cyber-Attack Surface

- 4.2.2 Rapid Adoption of Open Architecture Avionics and IoT Sensors in Aircraft Fleets

- 4.2.3 Growth in Cloud-Based Airport Operations Platforms and SaaS Flight Applications

- 4.2.4 Integration of 5G and Satellite Connectivity in ATC Networks Requiring Zero-Trust Security

- 4.2.5 Rise of eVTOL and Urban Air Mobility Operators Implementing Security-by-Design

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy Systems Hindering Unified Security Governance

- 4.3.2 Shortage of Aviation-Domain Cyber-Security Specialists in Emerging Markets

- 4.3.3 High Certification and Air-Worthiness Validation Costs Delaying Deployments

- 4.3.4 Limited Budget Allocation Among Regional and General Aviation Airports

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory and Compliance Outlook

- 4.6 Technology Snapshot (Emerging Tools, AI/ML, Quantum-Resistant Crypto)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Solution

- 5.1.1 Threat Intelligence and Response

- 5.1.2 Identity and Access Management

- 5.1.3 Data Loss Prevention

- 5.1.4 Security and Vulnerability Management

- 5.1.5 Managed Security

- 5.2 By Security Type

- 5.2.1 Network Security

- 5.2.2 Endpoint Security

- 5.2.3 Application Security

- 5.2.4 Cloud Security

- 5.2.5 Wireless and Satellite Link Security

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud-Deployed

- 5.4 By Application

- 5.4.1 Airline Management

- 5.4.2 Air Cargo Management

- 5.4.3 Airport Management

- 5.4.4 Air Traffic Control Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, JV, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Honeywell International Inc.

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Thales Group

- 6.4.4 Raytheon Technologies Corporation

- 6.4.5 BAE Systems plc

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 Collins Aerospace

- 6.4.9 Unisys Corporation

- 6.4.10 Palo Alto Networks Inc.

- 6.4.11 SITA SC

- 6.4.12 Leidos Holdings Inc.

- 6.4.13 IBM Corporation

- 6.4.14 Airbus CyberSecurity

- 6.4.15 The Boeing Company

- 6.4.16 Darktrace plc

- 6.4.17 Fortinet Inc.

- 6.4.18 Trend Micro Inc.

- 6.4.19 Telespazio S.p.A.

- 6.4.20 Rohde and Schwarz GmbH and Co KG

- 6.4.21 Cyberbit Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment