|

시장보고서

상품코드

1851064

지적재산 관리 소프트웨어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Intellectual Property Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

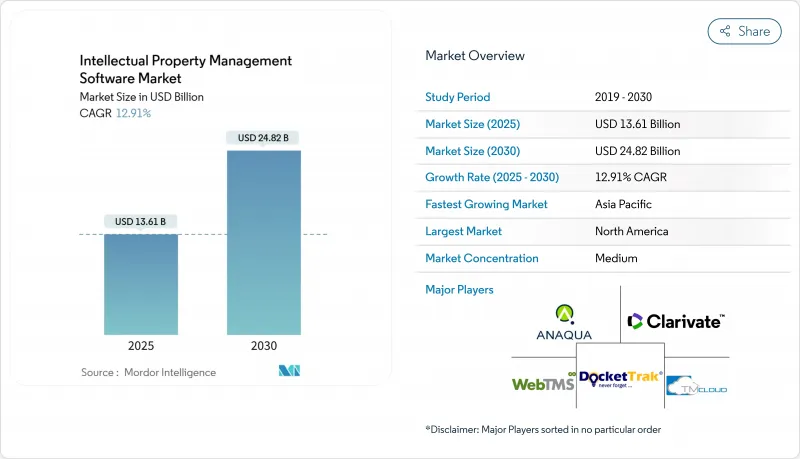

지적재산 관리 소프트웨어 시장 규모는 2025년에 136억 1,000만 달러, 2030년에는 248억 2,000만 달러로 확대되어 CAGR 12.91%를 나타낼 것으로 예측됩니다.

AI를 활용한 특허 분석, ESG와 연동한 지재 평가 툴, 크로스보더 감시 모듈에 대한 수요 증가가 플랫폼의 기능 로드맵을 재구축하고 있습니다. 이 새로운 기능은 독일 특허상표청이 2024년에 기록한 국내 특허 출원 건수의 4% 증가와 일치하고 있으며, 핵심 기술 부문 전체에서 혁신 의욕이 지속되고 있음을 보여줍니다. 미국과 중국의 반도체 소송, 인도의 조기 심사 프로그램 등의 정책적인센티브, WIPO의 중소기업용 지재 관리 클리닉 등이 지적재산 관리 소프트웨어 시장의 대응 가능한 밑단을 넓히고 있습니다. 공급업체의 통합은 여전히 완만하지만, 대규모 전략적 구매자와 개인 자금 펀드는 기업 사용자에게 가치 실현까지의 시간을 단축할 수 있는 분석에 중점을 둔 자산을 획득하기 위해 새로운 자본을 투입하고 있습니다.

세계의 지적재산 관리 소프트웨어 시장 동향과 인사이트

AI를 활용한 특허 분석의 채용이 북미 전역에서 스위트 업그레이드를 촉진

북미 기업은 도킹에 머무르지 않고 대규모 언어 모델 검색, 자동 제도 및 구현 자유 검사를 포함한 예측 특허 랜드스케이프 매핑으로 전환하고 있습니다. 특허 문서에서 책임있는 AI 사용에 관한 USPTO의 2024년 가이드라인은 준비 시간을 최대 60% 단축하는 AI 드래프팅 어시스턴트의 채용을 법무팀에 장려했습니다. Lucinity와 같은 공급업체가 보유한 연계 학습 특허는 연합 분석이 데이터 주권을 손상시킬 필요가 없음을 입증합니다. 이에 따라 포춘 500의 기술 기업 내에서의 교체 사이클이 가속화되고 지적재산 관리 소프트웨어 시장이 확대되고 있습니다.

아시아의 D2C 브랜드 상표의 급증이 SaaS IP의 채용을 가속

아시아태평양의 전자상거래 경제는 2025년까지 세계 온라인 소매 매출의 61%에 이를 것으로 예상되며, 자동화된 여러 법역에서 워크플로우가 필요한 D2C 브랜드 상표 출원에 박차를 가하고 있습니다. 플랫폼 수요는 사내에 변호사가 없었던 중소기업에서 가장 강하며 구독 기반 상표 모듈의 사용자 수는 4자리 증가를 나타냅니다. 지적재산 관리 소프트웨어 시장은 온보딩 전에 유효한 IP 포트폴리오를 유지하도록 판매자에게 의무화하는 시장에서 이익을 얻고 있습니다.

세분화된 EU 데이터 표준이 포트폴리오 통합을 방해

통일특허재판소의 출시에도 불구하고 상표와 디자인은 여전히 각국의 출원 시스템에 의존하고 있으며, 기업은 자동화된 워크플로우 중 적어도 14개의 유연성 카테고리를 다루어야 합니다. 컴플라이언스 팀은 지역 전반에 걸쳐 30-40%의 설정 시간이 소요된다고 보고했으며 지적재산 관리 소프트웨어 시장의 단기 성장에 물을 공급하고 있습니다.

부문 분석

프라이빗 클라우드 솔루션은 2030년까지 연평균 복합 성장률(CAGR)이 18.6%를 나타낼 전망입니다. 프라이빗 클라우드 솔루션과 관련된 지적재산 관리 소프트웨어 시장 규모는 퍼블릭 클라우드 수익을 초과할 것으로 예측됩니다. 지적재산 관리 소프트웨어 시장에서 프라이빗 클라우드 관련 시장 규모는 퍼블릭 클라우드 관련 수익을 상회할 것으로 예측됩니다. 다만 2024년 기준에서는 퍼블릭 클라우드가 시장 점유율의 58%를 차지했습니다. 항공우주와 방어를 포함한 대규모 규제 산업은 에어 갭이 있는 On-Premise 노드에 대한 의존을 계속하고 있지만, 분석 엔진은 클라우드의 샌드박스에서 실행하고, 마스터 데이터는 방화벽 안에 머무르는 하이브리드 철학이 법역을 넘어서는 입찰을 이겨내고 있습니다. 싱크로노스 테크놀로지스와 같은 공급업체들은 이러한 아키텍처의 기술적 기반을 보호하는 특허 포트폴리오를 보유하고 있으며 시장 진입 장벽을 강조하고 있습니다.

이 변화는 IP 데이터가 지정학적 위험을 수반한다는 인식 증가를 반영합니다. 다국적 기업의 법무팀은 현재 데이터베이스 계층에 통합된 세분화된 상주 관리 및 자동 삭제 정책을 요구하고 있습니다. 그 결과 RFP는 라이선스 할인보다는 정지시 암호화, 지역별 페일오버 기능, 제로 트러스트 액세스 모델을 중시하게 되었습니다. 컴플라이언스 부담이 증가함에 따라 프라이빗 클라우드 제공업체는 보안 인증을 수익화하고 지적재산 관리 소프트웨어 시장의 가치를 높이고 있습니다.

2024년 판매 점유율은 소프트웨어가 60.1%로 계속 우위를 차지했지만 컨설팅 및 분석 서비스는 CAGR 19.3%로 가속화되고 있습니다. 기업은 레거시 도킹 워크플로와 AI 주도의 시맨틱 검색 및 자동 드래프팅과의 조정에 고민하고 있습니다. 시행 부대는 CFO 대시보드에 포트폴리오 인사이트를 표시하기 위해 IP 제품군을 ERP, 전자 송장 및 계약 수명 주기 시스템과 통합합니다. SaaS 라이선싱이 예측 가능한 수익을 제공하는 반면 서비스 라인은 비용이 많이 드는 청구율을 얻고 솔루션 통합자의 지적재산 관리 소프트웨어 시장 규모를 전반적으로 확대합니다.

또한 지적재산 관리 소프트웨어 시장에서 틈새 마이크로 서비스(선행 기술 자동 요약, 클레임 매핑 엔진, 녹색 특허 스크리너)가 API를 통해 번들되어 소프트웨어 공급자를 마켓플레이스 모델로 밀어 올리고 있습니다. 공급업체가 고객을 둘러싸는 데이터 네트워크 효과를 즐기는 반면, 최종 사용자는 맞춤형 스택을 구성하는 자유를 얻습니다. 이 모듈화로 인해 핵심 도킹 시트 가격 경쟁이 치열해지면서 독자적인 AI 교육 데이터를 보유한 기존 기업의 경우 보다 수익성이 높은 분석 레인이 열립니다.

지역 분석

북미는 2024년 지적재산 관리 소프트웨어 시장에서 39.1%의 점유율을 유지하고 견조한 특허소송 인프라와 포춘 500기업의 프리미엄 분석에 대한 지불 경향에 의해 지원되었습니다. USPTO의 GUI와 자동차 부품에 관한 의장 특허 발행 건수가 40% 급증해 대응 가능한 워크로드가 더욱 확대됩니다. 사이버 보험료가 상승함에 따라 프라이빗 클라우드의 선호도가 높아지며, 각 지역공급업체는 SOC-2 컴플라이언스와 제로 트러스트 아키텍처를 번들로 제공합니다.

아시아태평양은 기록상표출원, 인도의 신속한 심사, 중국의 지속적인 연구개발비로 2030년까지 연평균 복합 성장률(CAGR) 18.9%로 성장을 이끌어 갈 것입니다. 상표 체류가 신흥 기업을 SaaS 기반 자동 분류와 실시간 상태 추적으로 향하게 합니다. 일본에서는 지재 분석의 인력 부족으로 특허 텍스트를 비즈니스에 적합한 비주얼로 변환하는 자동 대시보드가 주목을 받고 이 지역의 지적재산 관리 소프트웨어 시장 규모가 확대되었습니다.

단편적인 데이터 표준에도 불구하고, 유럽의 궤도는 안정적입니다. 통일특허법원은 유럽 전역의 특허권 행사를 간소화했지만 상표 워크플로우는 여전히 국가마다 다르기 때문에 기업의 IP 스위트는 멀티테넌트 아키텍처를 강요하고 있습니다. 독일에서는 특허 출원 건수가 4% 증가하고 자동차 기술 혁신이 진행되고 있기 때문에 현지 수요는 유지되고 있지만 기업이 EU 데이터 거버넌스법의 의무에 적응하는 동안 롤아웃 사이클이 길어집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI를 활용한 특허 분석의 채용이 북미 전역에서 스위트 업그레이드를 촉진

- 아시아에 있어서 D2C 브랜드 상표의 급증이 SaaS IP의 도입을 가속

- 미·중 반도체 특허 전쟁이 국경을 넘은 모니터링 수요 촉진

- 통합 스위트에 투자자를 유치하는 ESG 연동 IP 평가 의무

- 인도와 브라질의 패스트 트랙 검찰 제도가 중소기업의 이용을 촉진

- 시장 성장 억제요인

- 세분화된 EU 데이터 표준이 포트폴리오의 통합을 방해

- 사이버 보험료 상승이 클라우드의 TCO 수요 촉진

- IP 애널리틱스 인재 부족이 일본의 서비스 용량 감소

- 블록체인 레지스트리 도입 지연으로 상호 운용성 투자 지연

- 밸류체인 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 동향의 영향 평가

제5장 시장 규모와 성장 예측(가치)

- 배포별

- On-Premise

- 클라우드

- 구성 요소별

- 소프트웨어

- IP 포트폴리오 관리 제품군

- 특허 및 상표 검색 데이터베이스

- IP 분석 대시보드

- 도킹 및 워크플로우 자동화

- 서비스

- 구현 및 통합

- 컨설팅 및 애널리틱스

- 지원 및 유지보수

- 소프트웨어

- IP 유형별

- 특허

- 상표

- 저작권

- 디자인

- 영업비밀

- 조직 규모별

- 대기업(직원 수 1,000명 이상)

- 중소기업(직원 수 1,000명 미만)

- 최종 사용자 업계별

- BFSI

- 헬스케어 및 생명과학

- 자동차 및 모빌리티

- IT 및 텔레콤

- 가전 및 반도체

- 정부 및 공공 부문

- 학술 및 연구 기관

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가(덴마크, 스웨덴, 노르웨이, 핀란드)

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 멕시코

- 기타 남미

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Anaqua Inc.

- Clarivate PLC

- DoketTrak

- WebTMS Ltd.

- TM Cloud Inc.

- CPA Global Ltd.

- Alt Legal Inc.

- Questel SAS

- Gridlogics Technologies Pvt. Ltd

- AppColl Inc.

- Patrix AB

- Patsnap Pte Ltd

- MaxVal Group Inc.

- LexisNexis IP(RELX)

- Inteum Company LLC

- IPfolio(Zenith IP)

- Minesoft Ltd.

- TechInsights Inc.

- Ambercite Pty Ltd.

- Dennemeyer Group

- Dolcera Corp.

제7장 시장 기회와 향후 전망

KTH 25.11.20The intellectual property management software market size is valued at USD 13.61 billion in 2025 and is projected to advance to USD 24.82 billion by 2030, registering a 12.91% CAGR.

Rising demand for AI-powered patent analytics, ESG-linked IP valuation tools, and cross-border monitoring modules is reshaping platform feature roadmaps. The new functionality coincides with a 4% rise in domestic patent applications recorded by the German Patent and Trade Mark Office in 2024, signaling sustained innovation appetite across core technology sectors. Semiconductor litigation between the United States and China, policy incentives such as India's fast-track prosecution program, and WIPO's SME-focused IP Management Clinics together widen the addressable base for the intellectual property management software market. Vendor consolidation remains moderate, yet large strategic buyers and private-equity funds are allocating fresh capital to acquire analytics-heavy assets that can shorten time-to-value for corporate users.

Global Intellectual Property Management Software Market Trends and Insights

Adoption of AI-Powered Patent Analytics Driving Suite Upgrades Across North America

Enterprises across North America are moving beyond docketing toward predictive patent-landscape mapping that embeds large-language-model search, automated drafting, and freedom-to-operate checks. The USPTO's 2024 guidelines on responsible AI use in patent documents encouraged legal teams to adopt AI drafting assistants that cut preparation time by up to 60%. Federated-learning patents held by vendors such as Lucinity prove that collaborative analytics does not have to compromise data sovereignty. Replacement cycles inside Fortune 500 technology firms are therefore accelerating, expanding the intellectual property management software market.

D2C Brand Trademark Surge in Asia Accelerating SaaS IP Adoption

Asia-Pacific's e-commerce economy, forecast to reach 61% of global online retail sales by 2025, is fueling trademark filings among D2C brands that require automated, multi-jurisdictional workflows. Platform demand is strongest among SMEs that previously lacked in-house counsel, driving quadruple-digit user growth for subscription-based trademark modules. The intellectual property management software market benefits from marketplace mandates that sellers maintain validated IP portfolios before onboarding.

Fragmented EU Data Standards Hindering Portfolio Consolidation

Despite the Unified Patent Court launch, trademarks and designs still depend on national filing systems, forcing corporates to juggle at least 14 flexibility categories inside automated workflows. Compliance teams report 30-40% extra configuration time when rolling out region-wide deployments, dampening near-term growth for the intellectual property management software market.

Other drivers and restraints analyzed in the detailed report include:

- U.S.-China Semiconductor Patent Wars Spurring Cross-Border Monitoring Demand

- ESG-Linked IP Valuation Mandates Attracting Investors to Integrated Suites

- Rising Cyber-Insurance Premiums Inflating Cloud TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Private-cloud solutions are registering 18.6% CAGR to 2030 as firms seek scalability without relinquishing data sovereignty. The intellectual property management software market size attached to private-cloud offerings is forecast to outpace public-cloud revenues even though public configurations held 58% market share in 2024. Large regulated industries, including aerospace and defense, continue relying on air-gapped on-premise nodes, but hybrid philosophies-where analytics engines run in cloud sandboxes while master data stays inside firewalls-are winning cross-jurisdictional bids. Vendors such as Synchronoss Technologies hold patent portfolios that protect the technical underpinnings of these architectures, emphasizing market entry barriers.

The shift reflects growing awareness that IP data carries geopolitical risk. Multinational legal teams now require granular residency controls and automated deletion policies embedded at the database layer. Consequently, RFPs increasingly weight encryption-at-rest, regional failover capabilities, and zero-trust access models over marginal license discounts. As compliance burdens rise, private-cloud providers monetize security certifications, contributing incremental value to the intellectual property management software market.

Software continued to dominate with 60.1% revenue share in 2024, yet consulting and analytics services are accelerating at 19.3% CAGR. Enterprises struggle to reconcile legacy docketing workflows with AI-driven semantic search and automated drafting; advisory engagements thus balloon in scope. Implementation squads integrate IP suites with ERP, e-billing, and contract-lifecycle systems to surface portfolio insights inside CFO dashboards. Where SaaS licensing yields predictable revenue, services lines earn premium bill rates, enlarging the overall intellectual property management software market size for solution integrators.

The intellectual property management software market also sees niche micro-services-prior-art auto-summarizers, claim-mapping engines, and green-patent screeners-bundled through APIs, pushing software providers toward marketplace models. End-users gain the freedom to compose bespoke stacks, while vendors enjoy data network effects that lock in customers. This modularity intensifies price competition for core docketing seats yet opens higher-margin analytics lanes for incumbents with proprietary AI training data.

The IP Management Software Market Report is Segmented by Deployment (On-Premise, Cloud), Component (Software, Service), IP Type (Patent, Trademark, Copyright, and More), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Healthcare and Lifesciences, Automotive and Mobility, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 39.1% share of the intellectual property management software market in 2024, anchored by robust patent litigation infrastructure and Fortune 500 propensity to pay for premium analytics. The USPTO's 40% jump in design patent issuances across GUI and automotive components further expands addressable workloads. Private-cloud preferences grow as cyber-insurance costs inflate, driving regional vendors to bundle SOC-2 compliance and zero-trust architectures.

Asia-Pacific leads growth at 18.9% CAGR through 2030, thanks to record trademark filings, India's fast-track prosecution, and China's sustained R&D spending. Trademark backlogs push startups toward SaaS-based auto-classification and real-time status tracking. Japan's talent shortage in IP analytics creates pull for automated dashboards that translate patent texts into business-ready visuals, widening the intellectual property management software market size within the region.

Europe's trajectory remains steady despite fragmented data standards. The Unified Patent Court simplifies enforcement for pan-European patents, yet trademark workflows still differ by country, forcing multi-tenant architecture within enterprise IP suites. Germany's 4% rise in patent applications and ongoing automotive innovations preserve local demand, although rollout cycles lengthen while firms adapt to EU Data Governance Act obligations.

- Anaqua Inc.

- Clarivate PLC

- DoketTrak

- WebTMS Ltd.

- TM Cloud Inc.

- CPA Global Ltd.

- Alt Legal Inc.

- Questel SAS

- Gridlogics Technologies Pvt. Ltd

- AppColl Inc.

- Patrix AB

- Patsnap Pte Ltd

- MaxVal Group Inc.

- LexisNexis IP (RELX)

- Inteum Company LLC

- IPfolio (Zenith IP)

- Minesoft Ltd.

- TechInsights Inc.

- Ambercite Pty Ltd.

- Dennemeyer Group

- Dolcera Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of AI-Powered Patent-Analytics Driving Suite Upgrades Across North America

- 4.2.2 D2C Brand Trademark Surge in Asia Accelerating SaaS IP Adoption

- 4.2.3 U.S.-China Semiconductor Patent Wars Spurring Cross-Border Monitoring Demand

- 4.2.4 ESG-Linked IP Valuation Mandates Attracting Investors to Integrated Suites

- 4.2.5 India and Brazil Fast-Track Prosecution Schemes Unlocking SME Uptake Potentially

- 4.3 Market Restraints

- 4.3.1 Fragmented EU Data Standards Hindering Portfolio Consolidation

- 4.3.2 Rising Cyber-Insurance Premiums Inflating Cloud TCO

- 4.3.3 IP-Analytics Talent Shortage Capping Services Capacity in Japan

- 4.3.4 Slow Blockchain Registry Adoption Delaying Inter-operability Investments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Component

- 5.2.1 Software

- 5.2.1.1 IP Portfolio Management Suites

- 5.2.1.2 Patent and Trademark Search Databases

- 5.2.1.3 IP Analytics Dashboards

- 5.2.1.4 Docketing and Workflow Automation

- 5.2.2 Services

- 5.2.2.1 Implementation and Integration

- 5.2.2.2 Consulting and Analytics

- 5.2.2.3 Support and Maintenance

- 5.2.1 Software

- 5.3 By IP Type

- 5.3.1 Patent

- 5.3.2 Trademark

- 5.3.3 Copyright

- 5.3.4 Design

- 5.3.5 Trade Secret

- 5.4 By Organization Size

- 5.4.1 Large Enterprises (>=1 000 Emp.)

- 5.4.2 Small and Medium Enterprises ( <1 000 Emp.)

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Lifesciences

- 5.5.3 Automotive and Mobility

- 5.5.4 IT and Telecom

- 5.5.5 Consumer Electronics and Semiconductor

- 5.5.6 Government and Public Sector

- 5.5.7 Academia and Research Institutes

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 South-East Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Mexico

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC

- 5.6.5.2 Turkey

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)}

- 6.4.1 Anaqua Inc.

- 6.4.2 Clarivate PLC

- 6.4.3 DoketTrak

- 6.4.4 WebTMS Ltd.

- 6.4.5 TM Cloud Inc.

- 6.4.6 CPA Global Ltd.

- 6.4.7 Alt Legal Inc.

- 6.4.8 Questel SAS

- 6.4.9 Gridlogics Technologies Pvt. Ltd

- 6.4.10 AppColl Inc.

- 6.4.11 Patrix AB

- 6.4.12 Patsnap Pte Ltd

- 6.4.13 MaxVal Group Inc.

- 6.4.14 LexisNexis IP (RELX)

- 6.4.15 Inteum Company LLC

- 6.4.16 IPfolio (Zenith IP)

- 6.4.17 Minesoft Ltd.

- 6.4.18 TechInsights Inc.

- 6.4.19 Ambercite Pty Ltd.

- 6.4.20 Dennemeyer Group

- 6.4.21 Dolcera Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment