|

시장보고서

상품코드

1851199

미국의 HVAC 서비스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)US HVAC Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

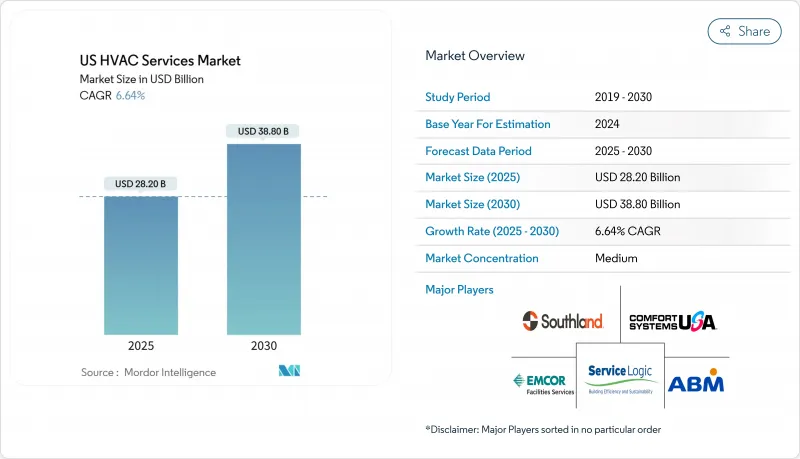

미국의 HVAC 서비스 시장 규모는 2025년 282억 달러에 이르고, 2030년까지 CAGR 6.6%로 388억 달러로 확대될 것으로 예측됩니다.

이 확장은 노후화된 시설의 갱신에 대한 근본적인 수요, 견조한 건설 파이프라인, 에너지 효율적인 업그레이드 비용을 낮추는 지속적인 정책 인센티브를 반영합니다. 2025년 4월 착공건수는 전월 대비 9.9% 증가하여 상업용, 주택용, 산업용 프로젝트를 통해 설치 계약의 견조한 흐름이 강화되었습니다. 인플레이션 억제법에 근거한 연방 정부의 리베이트와 주 수준의 인센티브는 주택 소유자 개조와 히트 펌프 채택을 계속 자극하고 있습니다. 스마트 빌딩 제어와 낮은 GWP 냉매로의 병렬 이동은 경상 수익 구성을 끌어올리는 컴플라이언스 중심의 서비스 기회를 창출합니다. 동시에 숙련된 기술자의 지속적인 부족은 노동공급을 박박시키고 임금을 상승시키고 소규모 계약자를 압박하고 있습니다.

미국 HVAC 서비스 시장 동향과 통찰

건설 활동의 성장

2025년 4월 비주택 착공건수가 9.9% 급증한 것은 재료비 상승이 특히 데이터센터, 헬스케어, 교육시설 등의 프로젝트 파이프라인을 좌절시키지 않았음을 나타냅니다. 이 확장은 꾸준한 설치와 시운전 작업을 미국 HVAC 서비스 시장으로 이끌고 운영 시작 후 롱테일 유지 보수 수입으로 전환합니다. 공공시설의 건설이 민간의 건설을 웃도는 가운데, 서비스 제공업체는 관공청의 개수가 급증하고 있는 것에 주목하고 있습니다. 멀티 트레이드 능력을 활용하는 계약자는 기계 + 제어 번들 범위에 위치하여 HVAC 서비스 시장에서 크로스 셀 잠재력을 높이고 있습니다.

노후화된 HVAC 장비의 대규모 설치 기반

미국 가정의 90% 이상이 일반적인 15-20년 라이프사이클이 끝나가는 기기에 의존하고 있어 예측 가능한 리노베이션 작업의 흐름을 만들어 내고 있습니다. 업무용 기기에서는 R-410A의 단계적 폐지가 가까이 다가오고 있기 때문에 업그레이드의 앞으로의 이송은 더욱 심각하고, 유지 보수 비용이 상승하고, 교환의 결정을 가속화하고 있습니다. 냉매 전환 전문 지식과 에너지 성과 계약을 결합한 서비스 제공 업체는 다년간 계약을 보장합니다. 결과적으로 이러한 계약은 정기적인 수익을 보장하고 미국의 HVAC 서비스 시장에서 점유율을 확대합니다.

공인 HVAC 기술자 부족

매년 약 4만 2,500명의 모집이 있지만, 졸업 파이프라인은 신축 및 개수의 요구보다 늦어지고 있습니다. 임금의 중앙값은 2023년 5만 7,300달러에 달하며, 특히 중소기업의 경우 영업비용이 상승하고 이익이 악화됩니다. 공공 부문의 기술 실습 제도는 이 격차를 메우기 위한 것이지만, 필요한 리드 타임은 10년 내내 고용이 전략적 병목 상태로 남아 있음을 의미합니다. 사내 아카데미와 명확한 경력 사다리를 구축하고 있는 기업은 높은 정착률을 누리고 미국의 HVAC 서비스 시장에 대한 이 발판을 경감하고 있습니다.

부문 분석

예방 유지보수 계약은 2024년 매출의 39%를 차지했으며, 예측 가능한 비용 관리와 가동 시간 보호를 소유자가 선호하는 것으로 나타났습니다. 상업용 포트폴리오는 현재 캘린더 간격이 아닌 실시간 가동 시간 데이터를 기반으로 서비스 방문을 예약하는 장비 분석을 통합하여 계약 갱신률을 높이고 단위당 평균 수익을 높이고 있습니다. 에너지 관리 및 모니터링 서비스는 컴플라이언스에 대한 압력과 동적 전력 요금 체계 하에서 부하 프로파일을 최적화할 필요성에 힘입어 CAGR 8.2%로 확대되고 있습니다. 모니터링과 성능 보증을 결합한 계약자는 미국 HVAC 서비스 시장 내에서 지갑 점유율을 확대하고 있습니다.

설치 공사 계약은 건설 지출과의 상관 관계를 유지하는 한편, 긴급 수리 서비스는 피크 부하 이벤트나 이상 기상시에 활황을 나타냅니다. 설계 엔지니어링의 범위는 탈탄소화 로드맵 및 라이프사이클 비용 분석을 포함할 때까지 확장되었습니다. 소유자는 기계, 제어 및 지속가능성 감사를 단일 공급자에게 번들로 늘어나고 있으며, 풀 서비스 기업의 전략적 관련성을 높이고 있습니다. 이러한 계약은 일반적으로 3-5년이므로 현금 흐름을 안정화하고 고객의 봉쇄를 강화하며 시장 경쟁력을 강화합니다.

빌딩 관리 시스템(BMS) 및 자동화 서비스는 고장 감지 및 데이터 중심 최적화에 대한 수요가 증가함에 따라 CAGR 9.1%로 가장 빠르게 성장하는 분야가 될 것입니다. 난방 서비스는 지역 차이가 현저하고, 히트 펌프의 채용은 전기 우대 조치로 비용 프리미엄이 축소되는 북부 주에서 가장 빠르게 성장하고 있습니다.

환기 및 실내 공기 품질(IAQ) 분야는 학교와 상업 사무실 거주자의 건강 지향에서 혜택을 받습니다. 냉동 서비스는 A2L 냉매로의 전환으로 인한 컴플라이언스 비용 증가에 직면하여 특수 도구에 대한 투자를 촉진하고 있습니다. 13%의 절감과 46%의 피크 부하 시프트를 달성한 캘리포니아의 실증 실험에 의해 검증된 축열식 리노베이션은 성능 지향 계약자의 보조 수익원으로 상승하고 있습니다. 제어 장치가 기계 시스템에 수렴함에 따라 서비스 제공업체는 통합 수수료 증분을 얻고 미국 HVAC 서비스 시장 내에서 차별화된 번들을 생성합니다.

미국의 HVAC 서비스 시장은 서비스 카테고리별(설계 및 엔지니어링, 설치 계약, 기타), 대상 시스템 유형별(난방, 서비스, 냉방 및 공조 서비스, 기타), 최종 사용자별(주택, 상업시설, 기타), 계약 모델별(프로젝트 기반(단발), 기타)으로 분류되어 있습니다. 시장 규모 및 예측은 금액(달러)으로 제공됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건설 활동의 성장

- 노후화된 HVAC 기기의 대규모 설치 기반

- 연방 및 주 에너지 효율 기준의 엄격화

- 스마트 및 IoT를 활용한 서비스 모델 확대

- 인플레이션 억제법에 의한 전기 인센티브

- 원 스톱 서비스 네트워크를 구축하는 프라이빗 에퀴티 롤업

- 시장 성장 억제요인

- 높은 초기 도입 및 레트로핏 비용

- 공인 HVAC 기술자 부족

- 냉매 전환 및 컴플라이언스 비용 상승

- 뒤섞인 주의 라이선싱 및 허가 규칙

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 서비스 카테고리별

- 디자인 및 엔지니어링

- 설치 계약

- 예방 보수 계약

- 긴급 수리 서비스

- 에너지 관리 및 감시 서비스

- 대상 시스템 유형별

- 난방(퍼니스, 보일러, 히트 펌프) 서비스

- 냉방 및 공조 서비스

- 환기 및 IAQ 서비스

- 냉동 서비스

- 제어, BMS, 자동화 서비스

- 최종 사용자별

- 주택

- 상업

- 상업

- 시설(교육, 헬스케어, 정부 기관)

- 계약 모델별

- 프로젝트 기반(단발)

- 정기 서비스 계약

- 지역별(미국 인구 조사 지역)

- 북동부

- 중서부

- 남부

- 서부

제6장 경쟁 구도

- 시장 집중도 분석

- 전략적 이동과 M&A

- 시장 점유율 분석

- 기업 프로파일

- EMCOR Services

- Comfort Systems USA

- Service Logic

- Southland Industries

- ACCO Engineered Systems

- TDIndustries

- ABM Technical Solutions

- United Mechanical

- J&J Air Conditioning

- National HVAC Services

- Lennox International

- Nortek Global HVAC

- Carrier Corporation

- Goodman Manufacturing

- Trane Technologies

- Johnson Controls

- Daikin Applied Americas

- Mechanical Services of America

- One Hour Heating and Air Conditioning

- ARS/Rescue Rooter

- McKinstry

제7장 시장 기회와 장래의 전망

JHS 25.11.21The US HVAC services market size reached USD 28.2 billion in 2025 and is projected to climb to USD 38.8 billion by 2030, advancing at a 6.6% CAGR.

The expansion reflects persistent demand for replacement of aging equipment, a robust construction pipeline, and sustained policy incentives that lower the cost of energy-efficient upgrades. Construction starts rose 9.9% month-over-month in April 2025, reinforcing a solid flow of installation contracts across commercial, residential, and industrial projects. Federal rebates under the Inflation Reduction Act, paired with state-level incentives, continue to stimulate homeowner retrofits and heat-pump adoption . Parallel shifts toward smart building controls and lower-GWP refrigerants are creating compliance-driven service opportunities that lift the recurring revenue mix. At the same time, a persistent shortage of skilled technicians tightens labor supply, lifts wages, and pressures small contractors, a dynamic that supports consolidation plays by capital-rich operators.

US HVAC Services Market Trends and Insights

Growth in Construction Activity

A 9.9% jump in nonresidential starts during April 2025 demonstrates that elevated materials costs have not derailed project pipelines, particularly in data centers, health care, and education facilities. The expansion funnels steady installation and commissioning work into the US HVAC services market, then converts into long-tail maintenance revenue once operations commence. As public construction outpaces private builds, service providers note a surge in government office retrofits, while data-center investment pushes premium demand for precision cooling. Contractors leveraging multi-trade capabilities position themselves for bundled mechanical-plus-controls scopes, reinforcing cross-sell potential in the US HVAC services market.

Large Installed Base of Aging HVAC Equipment

More than 90% of US households rely on equipment approaching the end of typical 15-20 year life cycles, creating predictable retrofit workstreams. On the commercial side, deferred upgrades are compounded by the impending phase-down of R-410A, which raises maintenance costs and accelerates replacement decisions. Service providers that combine refrigerant conversion expertise with energy-performance contracting secure multi-year engagements. In turn, those agreements lock in recurring revenue and boost wallet share within the US HVAC services market.

Shortage of Certified HVAC Technicians

Roughly 42,500 openings emerge each year, yet graduation pipelines lag the needs of new construction and retrofit workloads. Median wages hit USD 57,300 in 2023, lifting operating costs and eroding margins, especially for small businesses. Public-sector apprenticeship programs aim to fill the gap, but required lead times mean hiring remains a strategic bottleneck through the decade. Firms that build in-house academies and defined career ladders enjoy higher retention and mitigate this drag on the US HVAC services market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Federal & State Energy-Efficiency Standards

- Expansion of Smart/IoT-Enabled Service Models

- Rising Refrigerant Transition & Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Preventive maintenance contracts held 39% of 2024 revenue, underscoring owner preference for predictable cost management and uptime protection. Commercial portfolios now embed equipment analytics that schedule service visits based on real-time runtime data rather than calendar intervals, which increases contract renewal rates and raises average revenue per unit. Energy-management and monitoring services are expanding at an 8.2% CAGR, fueled by compliance pressures and the need to optimize load profiles under dynamic utility tariffs. Contractors that couple monitoring with performance guarantees deepen wallet share inside the US HVAC services market.

Installation contracting remains correlated with construction spending, while emergency repair services thrive during peak-load events and extreme weather. Design engineering scopes are broadening to include decarbonization road-mapping and lifecycle cost analysis. Owners increasingly bundle mechanical, controls, and sustainability audits under a single provider, elevating the strategic relevance of full-service firms. As those contracts typically span three to five years, they stabilize cash flow and reinforce client captivity, which strengthens competitive positions across the US HVAC services market.

Cooling services accounted for 41% revenue in 2024, a figure that continues to climb as cooling-degree days trend upward in nearly all US climate zones.[3] Building-management system (BMS) and automation services compose the fastest-growing slice at a 9.1% CAGR, aligned with rising demand for fault detection and data-driven optimization. Heating services exhibit pronounced regional differences; heat-pump adoption is growing fastest in northern states where electrification incentives narrow the cost premium.

Ventilation and indoor-air-quality (IAQ) scopes benefit from occupant-health imperatives in schools and commercial offices. Refrigeration services face higher compliance spend due to the switch to A2L refrigerants, which is prompting specialized tool investments. Thermal-energy-storage retrofits, validated by California demonstrations that achieved 13% savings and 46% peak-load shifting, are emerging as ancillary revenue streams for performance-oriented contractors.As controls converge with mechanical systems, service providers capture incremental integration fees and create differentiated bundles within the US HVAC services market.

US HVAC Services Market is Segmented by Service Category (Design and Engineering, Installation Contracting and More), by System Type Served (Heating, Services, Cooling / Air-Conditioning Services and More ), by End User (Residential, and Commercial, and More), by Contract Model (Project-Based (One-Off), and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- EMCOR Services

- Comfort Systems USA

- Service Logic

- Southland Industries

- ACCO Engineered Systems

- TDIndustries

- ABM Technical Solutions

- United Mechanical

- J&J Air Conditioning

- National HVAC Services

- Lennox International

- Nortek Global HVAC

- Carrier Corporation

- Goodman Manufacturing

- Trane Technologies

- Johnson Controls

- Daikin Applied Americas

- Mechanical Services of America

- One Hour Heating and Air Conditioning

- ARS/Rescue Rooter

- McKinstry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Construction Activity

- 4.2.2 Large Installed Base of Aging HVAC Equipment

- 4.2.3 Stricter Federal & State Energy-Efficiency Standards

- 4.2.4 Expansion of Smart/IoT-Enabled Service Models

- 4.2.5 Inflation Reduction Act Incentives for Electrification

- 4.2.6 Private-Equity Roll-ups Creating One-Stop Service Networks

- 4.3 Market Restraints

- 4.3.1 High Up-Front Installation & Retrofit Costs

- 4.3.2 Shortage of Certified HVAC Technicians

- 4.3.3 Rising Refrigerant Transition & Compliance Costs

- 4.3.4 Patchwork State Licensing & Permitting Rules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Service Category

- 5.1.1 Design and Engineering

- 5.1.2 Installation Contracting

- 5.1.3 Preventive Maintenance Contracts

- 5.1.4 Emergency Repair Services

- 5.1.5 Energy-Management and Monitoring Services

- 5.2 By System Type Served

- 5.2.1 Heating (Furnace, Boiler, Heat Pump) Services

- 5.2.2 Cooling / Air-Conditioning Services

- 5.2.3 Ventilation and IAQ Services

- 5.2.4 Refrigeration Services

- 5.2.5 Controls, BMS and Automation Services

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional (Education, Healthcare, Govt)

- 5.4 By Contract Model

- 5.4.1 Project-Based (One-off)

- 5.4.2 Recurring Service Agreements

- 5.5 By Geography (US Census Regions)

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves and M&A

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 EMCOR Services

- 6.4.2 Comfort Systems USA

- 6.4.3 Service Logic

- 6.4.4 Southland Industries

- 6.4.5 ACCO Engineered Systems

- 6.4.6 TDIndustries

- 6.4.7 ABM Technical Solutions

- 6.4.8 United Mechanical

- 6.4.9 J&J Air Conditioning

- 6.4.10 National HVAC Services

- 6.4.11 Lennox International

- 6.4.12 Nortek Global HVAC

- 6.4.13 Carrier Corporation

- 6.4.14 Goodman Manufacturing

- 6.4.15 Trane Technologies

- 6.4.16 Johnson Controls

- 6.4.17 Daikin Applied Americas

- 6.4.18 Mechanical Services of America

- 6.4.19 One Hour Heating and Air Conditioning

- 6.4.20 ARS/Rescue Rooter

- 6.4.21 McKinstry

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment