|

시장보고서

상품코드

1911500

유럽의 HVAC 서비스 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe HVAC Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

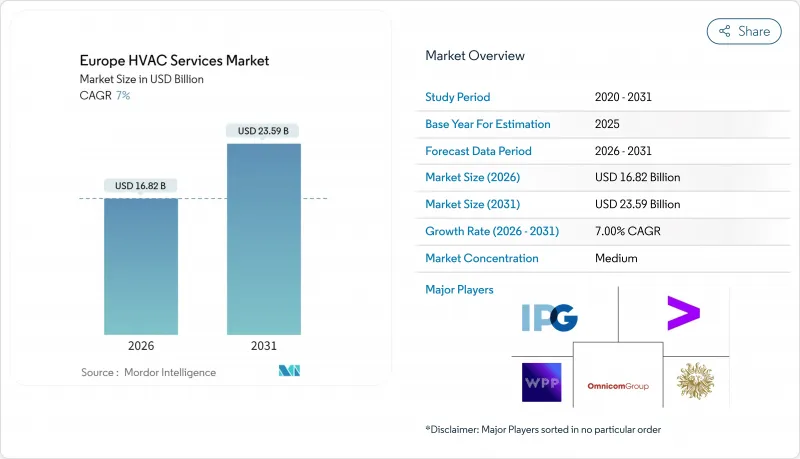

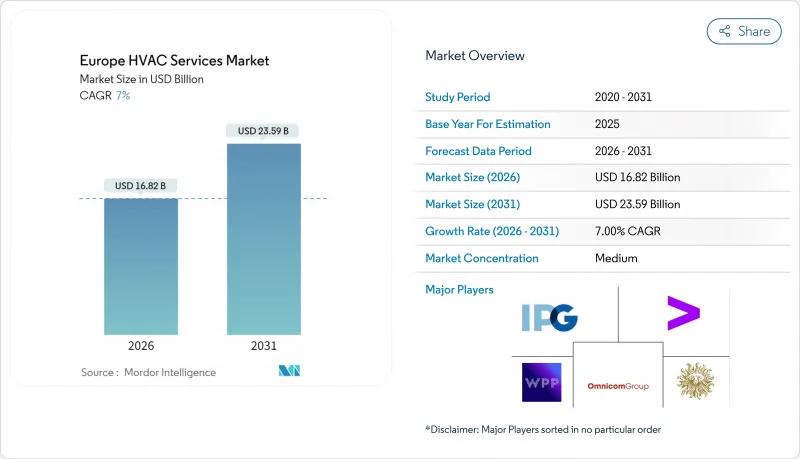

유럽의 HVAC 서비스 시장은 2025년 157억 2,000만 달러로 평가되었고, 2026년에는 168억 2,000만 달러로 성장할 전망이며, 2026-2031년 CAGR 7.0%로 성장을 지속하여, 2031년까지 235억 9,000만 달러에 달할 것으로 예측되고 있습니다.

이 성장세는 탈탄소화를 의무화하는 법규제 강화, 히트펌프의 보급 확대, 에너지 사용량 및 서비스 정지 시간 모두를 줄이는 예지보전에 대한 수요 증가에 기인하고 있습니다. 프론 규제 강화, 구리 가격 상승, 지역 노동력 부족이 비용 압력이 되는 한편, 자산 소유자가 운영 예산을 효율화하는 방법을 모색하면서 디지털 서비스 도입을 가속화하고 있습니다. 보쉬에 의한 존슨컨트롤스 및 히타치 합작회사(81억 달러 규모)의 인수 후, 경쟁은 계속하고 있습니다. 이 인수는 유럽 전역의 주택 및 소규모 상업 서비스 네트워크를 재편하는 것입니다. 성장 기회는 주로 EU 리노베이션 계획 'Renovation Wave'에 연동된 리노베이션 패키지, 북유럽 국가의 지역 난방 시스템 업데이트, 비용 최소화보다 가동 시간 보장을 중시하는 하이퍼스케일 데이터센터용 정밀 공조 계약에 집중하고 있습니다.

유럽의 HVAC 서비스 시장 동향 및 인사이트

EU 리노베이션 계획의 의무화가 서비스 수요 가속화 촉진

개수파 정책에 따라 회원국은 2030년까지 비주택 건축물 중 에너지 효율이 가장 낮은 16%의 개수를 의무화하고, 2024년 12월까지 290kW를 초과하는 시설에는 빌딩 자동화 제어 시스템 설치가 요구됩니다. 이 규제 대응에 의해 소유자는 사후 대응형의 보수로부터, 에너지 절약 효과를 보증하는 성과 연동형 서비스 계약에 대한 이행을 강요받고 있습니다. 에너지 감사, 자금 조달 지원, 디지털 성능 추적을 일상적인 HVAC 업무에 통합하는 계약 업체는 장기간 다년간 계약을 받았습니다. 독일과 네덜란드의 선행 도입 기업은 고객이 낮은 시간당 단가보다 턴키 방식의 컴플라이언스를 중시하기 때문에 더 높은 이익률을 보고합니다.

히트 펌프 교체 붐이 서비스 포트폴리오 요구 사항 재구성

유럽의 설치 대수는 2024년에 2,150만 대를 돌파했으며, 교환 공사마다 A2L 냉매나 스마트 홈 통합의 훈련을 받은 기술자가 필요하게 됩니다. 서비스 방문은 연소 안전 점검에서 냉매 누출 감지 및 펌웨어 업데이트로 전환하고 있습니다. 1990년대 이후, 스웨덴에서는 건축물 난방의 배출량을 95% 삭감하고 있어 히트 펌프의 보급이 수십년에 걸쳐서 서비스 형태를 어떻게 변화시킬 수 있는가를 나타내고 있습니다. 각 공급업체는 차별화를 위해 원격 모니터링 및 5년 보증을 제공하여 고객 1인당 평생 가치를 높이고 있습니다.

프론 가스 인정 기술자의 부족이 대응 능력 제약

2025년 시행의 신규제에 의해 R-454B 또는 R-32를 취급하는 현장 기술자는 모두, 갱신된 자격을 유지할 것이 의무지워집니다. 그러나 EU 역내에서는 8만 명의 기술자 부족이 해소되지 않았습니다. 이 부족으로 네덜란드 등 수요 집중 지역에서는 인건비가 15-20% 상승하여 유자격자 확보가 몇 주간 지연되는 프로젝트도 발생하고 있습니다. 보쉬를 비롯한 기업은 현재 단기 집중 코스 및 이동식 트레이닝 랩을 후원하고 있지만, 이 스킬 갭이 2027년까지 해소될 가능성은 낮다고 보여지고 있습니다.

부문 분석

2025년 시점에서 유럽 HVAC 서비스 시장의 53.55%를 차지한 보수 및 수리 분야는 규정 용량을 넘는 시스템에 대한 의무 검사가 기반이 되고 있습니다. 안정적인 설치 기반이 지속적인 수익을 제공하는 반면, 이익 소스는 소프트웨어 플랫폼으로 전환하고 있습니다. 센서 해석에 의한 성능 이상 검출 시에만 기술자를 파견하는 구조입니다. 스마트 접속형 운용 및 보수는 CAGR 10.38%로 확대되고 있으며, 고장을 며칠 전에 예측하는 엣지 디바이스를 활용하는 것으로, 기술자의 출장 횟수를 최대 25% 삭감합니다. 벤더 각사는 디지털 트윈 기술에 투자해, 기류나 에너지 부하를 가시화하는 것으로 가동률 보증을 제공합니다. 이에 따라 기존 서비스 요금을 크게 웃도는 이익률을 실현하고 있습니다. 기존의 유지 보수 수요는 여전히 규모가 크며 성장률은 인플레이션을 따라 잡지 못했으며 공급업체는 원격 모니터링, 부품 물류 및 컴플라이언스 보고서를 포장하는 방향으로 전환하고 있습니다.

예지보전은 노동력의 구성도 변혁합니다. 현장 팀에는 기계 전문가를 파견하기 전에 이상 경보를 분석하는 데이터 분석가가 참가했습니다. 이 새로운 모델은 소프트웨어 라이선스, 현지 방문 및 규제 서류를 중앙 집중화하여 고객당 수익 점유율을 증가시킵니다. 구독 계약이 심화됨에 따라 고객 이탈률이 떨어지고 수익원이 고정화되어 연결 기술을 습득한 서비스 기업의 기업 가치가 상승합니다. 한편, 고장 수리 모델을 고수하는 기업은 가격 침식에 직면하여 유럽 HVAC 서비스 시장의 통합을 서두르는 디지털 대응 경쟁사에 의한 인수 가능성에 노출됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EU 개수파 지령

- 히트 펌프 교환 붐

- 에너지 절약 개수에 대한 수요 증가

- 데이터센터의 냉각 수요 급증

- 카본 연동형 금융 스킴

- 디지털 트윈을 활용한 예지보전

- 시장 성장 억제요인

- 프론 가스 인정 기술자 부족

- 레거시 시스템용 IoT 리노베이션의 높은 비용

- 냉매 공급망의 변동성

- 접속형 HVAC에 있어서 사이버 보안상의 우려

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 분석

제5장 시장 규모 및 성장 예측

- 서비스 유형별

- 보수 및 수리

- 설치

- 스마트 접속형 운용 보수(OandM)

- 도입 형태별

- 신축

- 기존 건물 개수

- 최종 사용자 업계별

- 주택용

- 비주택

- 상업용

- 산업

- 공공 및 공공기관

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 덴마크

- 노르웨이

- 스웨덴

- 핀란드

- 아이슬란드

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Johnson Controls International PLC

- Carrier Corporation

- Daikin Industries Ltd

- Vaillant Group

- Aggreko PLC

- Aermec SpA

- Trane Technologies plc

- Bosch Thermotechnology GmbH

- Siemens Building Technologies

- Honeywell International Inc.

- BDR Thermea Group

- Ingersoll Rand PLC

- Crystal Air Holdings Limited

- Klima Venta

- IAC Vestcold AS

- Airedale International Air Conditioning Ltd

- Envirotec Limited

- Kospel SA

- Spectrum Engineering Limited

- Pentair Inc.

제7장 시장 기회 및 장래 전망

AJY 26.01.30The Europe HVAC services market is expected to grow from USD 15.72 billion in 2025 to USD 16.82 billion in 2026 and is forecast to reach USD 23.59 billion by 2031 at 7.0% CAGR over 2026-2031.

Momentum comes from binding decarbonization laws, widespread heat-pump rollouts, and growing demand for predictive maintenance that lowers both energy use and service downtime. Tightening F-gas regulations, record copper prices, and regional labour shortages add cost pressure, yet they simultaneously accelerate digital service uptake as asset owners look for ways to stretch operating budgets. Competitive intensity keeps rising after Bosch's USD 8.1 billion purchase of the Johnson Controls-Hitachi JV, which reshapes residential and light-commercial service networks across the continent. Growth opportunities concentrate in retrofit packages tied to the EU Renovation Wave, district-heating upgrades in the Nordics, and precision-cooling contracts for hyperscale data centers that value guaranteed uptime over cost minimization.

Europe HVAC Services Market Trends and Insights

EU Renovation Wave mandates drive service demand acceleration

The Renovation Wave compels member states to refurbish the worst-performing 16% of non-residential buildings by 2030 and to install building-automation controls in sites above 290 kW by December 2024. Compliance pushes owners to shift from reactive maintenance toward outcome-based service contracts that guarantee energy savings. Contractors that layer energy audits, financing support, and digital performance tracking onto routine HVAC tasks lock in long multiyear deals. Early adopters in Germany and the Netherlands report higher margins because clients value turnkey compliance more than low hourly rates.

Heat-pump replacement boom reshapes service portfolio requirements

Europe's installed base surpassed 21.5 million units in 2024, and each replacement calls for technicians trained on A2L refrigerants and smart-home integration. Service visits shift from combustion safety checks to refrigerant leak detection and firmware updates. Sweden's 95% cut in building-heating emissions since the 1990s shows how widespread heat-pump adoption can transform service patterns for decades. Vendors now bundle remote monitoring and five-year warranties to differentiate, raising per-customer lifetime value.

Shortage of F-gas-certified technicians constrains capacity

New 2025 rules force every field technician who handles R-454B or R-32 to carry updated certification, yet 80,000 vacancies remain unfilled across the bloc. Backlogs push labour rates up 15-20% in hot spots such as the Netherlands, and some projects stall for weeks until a licensed crew becomes available. Companies including Bosch now sponsor accelerated courses and mobile training labs, but the skills gap is unlikely to close before 2027.

Other drivers and restraints analyzed in the detailed report include:

- Growing demand for energy-efficient retrofits transforms business models

- Data-center cooling surge creates a specialized service niche

- High IoT retrofit costs limit smart-service adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Maintenance and repair held 53.55% of Europe HVAC services market share in 2025, anchored by mandatory inspections on systems above specified capacity thresholds. The stable installed base delivers recurring revenue, yet profit pools shift toward software-enabled platforms that dispatch technicians only when sensor analytics flag performance drift. Smart-connected operations and maintenance, expanding at 10.38% CAGR, leverages edge devices that predict faults days in advance and trims labour truck rolls by up to 25%. Vendors invest in digital twins to visualize airflow and energy loads so they can offer uptime guarantees that boost margins far above traditional service rates. While the legacy maintenance cohort remains sizable, its growth lags inflation, nudging providers to bundle remote monitoring, parts logistics, and compliance reporting.

Predictive maintenance also changes workforce composition. Field teams now include data analysts who interpret anomaly alerts before dispatching mechanical specialists. The new model increases wallet share per client because a single provider manages software licenses, on-site visits, and regulatory paperwork. As subscription arrangements deepen, customer churn rates fall, locking revenue streams and raising enterprise valuations for service firms that master connectivity. Conversely, companies that cling to break-fix models face eroding prices and potential acquisition by digitally enabled rivals eager to consolidate the Europe HVAC services market.

The Europe HVAC Services Market Report is Segmented by Type of Service (Maintenance and Repair, Installation, Smart-Connected OandM), Implementation Type (New Construction, Retrofit Buildings), End-User Industry (Residential, Non-Residential Including Commercial, Industrial, Public and Institutional), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Johnson Controls International PLC

- Carrier Corporation

- Daikin Industries Ltd

- Vaillant Group

- Aggreko PLC

- Aermec SpA

- Trane Technologies plc

- Bosch Thermotechnology GmbH

- Siemens Building Technologies

- Honeywell International Inc.

- BDR Thermea Group

- Ingersoll Rand PLC

- Crystal Air Holdings Limited

- Klima Venta

- IAC Vestcold AS

- Airedale International Air Conditioning Ltd

- Envirotec Limited

- Kospel SA

- Spectrum Engineering Limited

- Pentair Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Renovation Wave mandates

- 4.2.2 Heat-pump replacement boom

- 4.2.3 Growing demand for energy-efficient retrofits

- 4.2.4 Data-center cooling demand surge

- 4.2.5 Carbon-linked financing schemes

- 4.2.6 Digital twin-driven predictive maintenance

- 4.3 Market Restraints

- 4.3.1 Shortage of F-gas-certified technicians

- 4.3.2 High IoT retrofit costs for legacy systems

- 4.3.3 Refrigerant supply-chain volatility

- 4.3.4 Cyber-security concerns in connected HVAC

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type of Service

- 5.1.1 Maintenance and Repair

- 5.1.2 Installation

- 5.1.3 Smart-connected OandM

- 5.2 By Implementation Type

- 5.2.1 New Construction

- 5.2.2 Retrofit Buildings

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Non-residential

- 5.3.2.1 Commercial

- 5.3.2.2 Industrial

- 5.3.2.3 Public and Institutional

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Nordic

- 5.4.6.1 Denmark

- 5.4.6.2 Norway

- 5.4.6.3 Sweden

- 5.4.6.4 Finland

- 5.4.6.5 Iceland

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Johnson Controls International PLC

- 6.4.2 Carrier Corporation

- 6.4.3 Daikin Industries Ltd

- 6.4.4 Vaillant Group

- 6.4.5 Aggreko PLC

- 6.4.6 Aermec SpA

- 6.4.7 Trane Technologies plc

- 6.4.8 Bosch Thermotechnology GmbH

- 6.4.9 Siemens Building Technologies

- 6.4.10 Honeywell International Inc.

- 6.4.11 BDR Thermea Group

- 6.4.12 Ingersoll Rand PLC

- 6.4.13 Crystal Air Holdings Limited

- 6.4.14 Klima Venta

- 6.4.15 IAC Vestcold AS

- 6.4.16 Airedale International Air Conditioning Ltd

- 6.4.17 Envirotec Limited

- 6.4.18 Kospel SA

- 6.4.19 Spectrum Engineering Limited

- 6.4.20 Pentair Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment