|

시장보고서

상품코드

1906898

중동 및 아프리카(MEA)의 사이버 보안 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2026-2031년)MEA Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

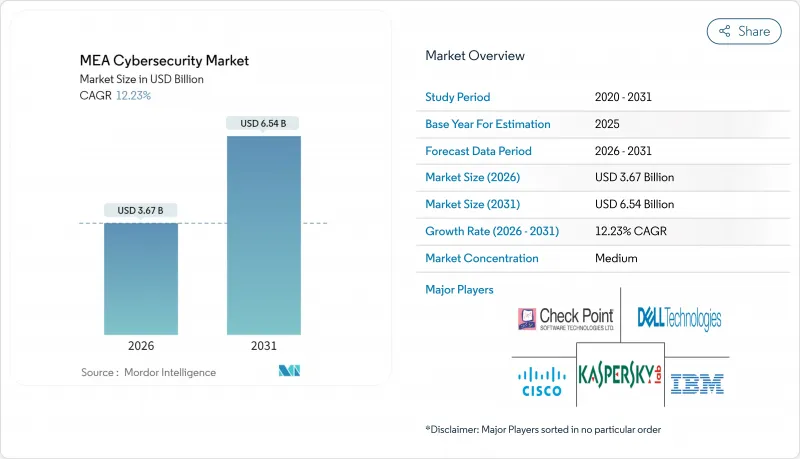

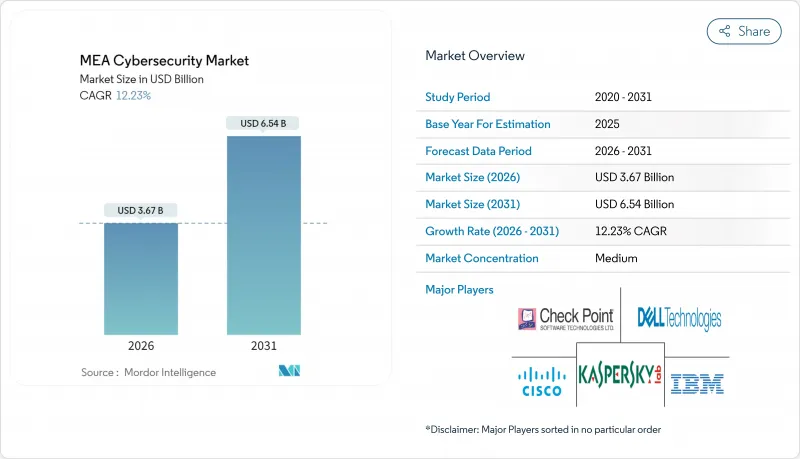

중동 및 아프리카의 사이버 보안 시장 규모는 2026년 36억 7,000만 달러로 추정되고, 2025년 32억 7,000만 달러에서 성장할 것으로 예상되며, 2031년 예측은 65억 4,000만 달러로, 2026-2031년 12.23%의 CAGR로 성장할 것으로 전망됩니다.

걸프 협력회의(GCC) 국가에서 소블린 클라우드의 급속한 전개, 지역의 석유 및 가스 자산에 대한 운영 기술(OT)의 위협 증가, 사하라 이남의 아프리카에 있어서 모바일 머니의 폭발적인 보급과 함께, 보안 지출은 증가 경향에 있습니다. 2030년 박람회와 NEOM 등의 메가 이벤트 개최로 중요한 국가 인프라의 강화가 진행되고 있는 한편, 조직이 제로 트러스트 아키텍처로의 현대화를 진행함에 따라 클라우드에 의한 보안의 채용이 확대되고 있습니다. 심각한 인력 부족과 단편적인 데이터 보호법에 의한 병행 비용 압력으로 관리형 보안 서비스 제공업체가 중동 및 아프리카 사이버 보안 시장에서 점유율을 얻는 기회가 탄생했습니다.

중동 및 아프리카(MEA) 사이버 보안 시장 동향 및 인사이트

GCC 국가의 소블린 클라우드 및 데이터 거주 의무가 SOC 투자 가속화

사우디아라비아의 '2024년 사이버 보안 기본 대책'과 UAE의 '국가 IoT 보안 정책'에 내장된 규제는 국내 데이터 처리를 의무화하고 조직은 현지 보안 운영 센터(SOC) 구축과 자국 인재 육성 파이프라인의 정비를 촉구하고 있습니다. 이 전략은 2027년까지 110억 달러 시장 규모를 목표로 하여 인력 부족을 보완하기 위해 관리 보안 서비스를 우선하는 카타르 '국가 사이버 보안 전략 2024-2030'에 의해 강화되고 있습니다. 그 결과, 현지 SOC의 구축과 매니지드 서비스의 채용이 중동 및 아프리카 사이버 보안 시장의 장기적인 성장을 지원할 것으로 예측됩니다.

사우디아라비아 및 아랍에미리트(UAE)에서 디지털 은행 라이선싱의 신속한 발행이 컴플라이언스 주도 보안 지출 촉진

사우디아라비아 규제 샌드박스 프로그램과 UAE의 개인정보보호법은 디지털 은행이 서비스를 시작하기 전에 견고한 리스크 관리 프레임워크를 증명하도록 요구합니다. 중앙 은행에서 상공부에 이르는 여러 규제 체크포인트는 지속적인 감사를 요구하며 컨설팅, 제3자 평가 및 자동화 플랫폼에 대한 수요를 촉진하고 있습니다. 라이선스 신청이 급증하는 가운데, 컴플라이언스 주도의 구입이 중동 및 아프리카 사이버 시큐리티 시장에 한층 더 기세를 더하고 있습니다.

사이버 보안 인력의 심각한 부족으로 서비스 비용 상승

UAE 기업의 87%가 컨설턴트 월급이 13,500 디르함을 넘어도 자격을 갖춘 채용에 어려움을 겪고 있습니다. 카타르에서는 주민 10만 명당 434.09개의 사이버보안직이 존재하지만, 수요는 공급을 상회하고 있으며, 조직은 모니터링 및 사고 대응을 외부 위탁할 수밖에 없습니다. 인건비 상승은 프로젝트 전체의 비용을 밀어 올리고 특히 중견 기업의 도입률을 억제하고 중동 및 아프리카 사이버 보안 시장을 제약하고 있습니다.

부문 분석

2025년에는 솔루션이 수익의 69.28%를 차지했으며 조직이 엔드포인트, 네트워크 및 클라우드 보안 제품군을 대량으로 조달했습니다. 이 이점은 중요한 환경을 위해 온프레미스 장비를 여전히 선호하는 대기업의 구매력을 보여줍니다. AI 기반 위협 감지 기술의 지속적인 혁신이 솔루션 지출을 뒷받침하고 있으며 SentinelOne과 같은 공급업체는 섀도우 AI 자산을 방어하기 위해 보안 태세 관리를 추가하고 있습니다. 그러나 중동 및 아프리카 사이버보안 시장에서는 심각한 인력 부족 및 컴플라이언스 부담을 배경으로 매니지드 서비스에 대한 수요가 높아지고 있으며 14.68%의 연평균 복합 성장률(CAGR) 전망이 나타났습니다.

전문 서비스는 통합업체가 주권 클라우드 환경을 가로지르는 복잡한 하이브리드 아키텍처를 커스터마이즈함에 따라 성장하고 있습니다. 특히 중소기업은 모니터링, 사고 대응, 규제 보고를 예측 가능한 요금 체계로 제공하는 Liquid C2와 같은 SOC-as-a-Service 솔루션에 기울고 있습니다. 이 전환은 중동 및 아프리카 사이버 보안 업계 내 점유율을 재분배하면서 대규모 리노베이션 프로젝트를 위한 솔루션 판매를 유지하고 있습니다.

2025년 시점에서 데이터 주권 규제 및 레거시 SCADA 시스템과의 연계를 통해 온프레미스형 아키텍처가 중동 및 아프리카 사이버 보안 시장 규모의 61.65%를 차지했습니다. 그러나 지역 제공업체가 거주 요건을 충족하는 로컬 PoP(연결 거점)를 확립함에 따라 클라우드 제공 보안은 15.43%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측되고 있습니다. 시스코 UAE용 Secure Service Edge 노드는 지연을 줄이고 GCC 규정을 준수하는 클라우드 현지화의 좋은 예입니다.

현재, 마이그레이션 로드맵에서는 하이브리드 모델이 주류가 되고 있습니다. 조직은 기밀성이 높은 워크로드를 국내에 유지하면서 분석 및 샌드박스 처리 작업을 지역 클라우드로 라우팅하고 있습니다. 가트너 정상 회담에서의 논의는 기업이 경계 방어로부터 정체성을 분리하는 동안 제로 트러스트 도입이 진행되고 있으며, 중동 및 아프리카 사이버 보안 시장에서 클라우드 채용을 더욱 촉진하는 것이 강조되었습니다.

중동 및 아프리카 사이버 보안 시장 보고서는 업계를 다음의 부문으로 분류하고 있습니다. 제공 형태별(솔루션, 서비스), 전개 모드별(온프레미스, 클라우드), 최종 사용자 업종별(은행 및 금융 및 보험, 의료, IT 및 통신, 산업 및 방위, 제조, 소매 및 전자상거래, 에너지 및 유틸리티, 기타), 최종 사용자 기업 규모별(중소기업), 지역별로 분석하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- GCC 국가의 소블린 클라우드 및 거주 의무화가 SOC 투자 가속

- 사우디아라비아 및 아랍에미리트(UAE)에서 디지털 은행 라이선싱의 신속한 발행이 컴플라이언스 주도의 보안 지출 촉진

- 석유 및 가스 자산에 대한 OT 사이버 공격의 격화가 ICS/SCADA 보안 도입 촉진

- 서브 사하라 아프리카에서 모바일 머니의 폭발적 보급이 엔드 포인트 보호 및 부정 방지를 필요로 하는 상황

- 메가 이벤트 계획(2030년 만박, 네옴, 두바이 항공 쇼)에 의한 중요 인프라 강화 가속

- 새로운 국가 사이버 규제(NCA ECC, UAE NESA, 이집트 DP법)에 의한 위협 인텔리전스 공유 의무화

- 시장 성장 억제요인

- 사이버 보안 인력의 심각한 부족이 서비스 비용 촉진

- 아프리카 국가에서의 단편화된 데이터 보호법이 컴플라이언스의 복잡화 초래

- 아프리카 중소기업의 예산 제약 : 보안보다 기본 디지털화 우선

- 지정학적 공급망 혼란에 노출되는 보안 기기에 대한 수입 의존도

- 중요 규제 프레임워크의 평가

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 주요 이용 사례와 사례 연구

- 시장의 거시 경제적 요인에 미치는 영향

- 투자분석

제5장 시장 세분화

- 제공별

- 솔루션

- 애플리케이션 보안

- 클라우드 보안

- 데이터 보안

- 아이덴티티 및 액세스 관리

- 인프라 보호

- 통합 리스크 관리

- 네트워크 보안 장비

- 엔드포인트 보안

- 기타 서비스

- 서비스

- 전문 서비스

- 매니지드 서비스

- 솔루션

- 전개 모드별

- 온프레미스

- 클라우드

- 최종 사용자 업계별

- BFSI

- 헬스케어

- IT 및 통신

- 산업 및 방위

- 제조업

- 소매 및 전자상거래

- 에너지 및 유틸리티

- 제조업

- 기타

- 최종 사용자 기업의 규모별

- 중소기업(SME)

- 대기업

- 지역별

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 바레인

- 쿠웨이트

- 오만

- 이스라엘

- 튀르키예

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 케냐

- 모로코

- 기타 아프리카

- 중동

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Inc.

- Broadcom(Symantec)

- Sophos Ltd.

- Kaspersky Lab

- Microsoft Corp.

- CrowdStrike Holdings Inc.

- Darktrace plc

- Rapid7 Inc.

- Mandiant

- McAfee Corp.

- Splunk Inc.

- LogRhythm Inc.

- Proofpoint Inc.

- BAE Systems Applied Intelligence

- Help AG

- StarLink DMCC

제7장 시장 기회 및 장래 전망

AJY 26.01.26Middle East and Africa cybersecurity market size in 2026 is estimated at USD 3.67 billion, growing from 2025 value of USD 3.27 billion with 2031 projections showing USD 6.54 billion, growing at 12.23% CAGR over 2026-2031.

Rapid sovereign-cloud rollouts across the Gulf Cooperation Council, mounting operational-technology (OT) threats to regional oil and gas assets, and explosive mobile-money adoption in Sub-Saharan Africa are converging to lift security spending. Mega-event pipelines such as Expo 2030 and NEOM drive hardening of critical national infrastructure, while cloud-delivered security gains traction as organizations modernize toward zero-trust architectures. Parallel cost pressures from an acute talent shortage and fragmented data-protection laws create openings for managed security service providers to capture share in the Middle East and Africa cybersecurity market.

MEA Cybersecurity Market Trends and Insights

Sovereign-cloud and residency mandates across GCC accelerating SOC investments

Mandates embedded in Saudi Arabia's Essential Cybersecurity Controls 2024 and the UAE National IoT Security Policy require in-country data processing, pushing organizations to build local security operations centers and indigenous talent pipelines. The strategy is reinforced by Qatar's National Cybersecurity Strategy 2024-2030, which targets USD 11 billion market value by 2027 and prioritizes managed security services to offset talent shortages. As a result, local SOC build-outs and managed services adoption are expected to anchor long-term growth in the Middle East and Africa cybersecurity market.

Rapid digital-banking license issuance in KSA and UAE boosting compliance-led security spend

Saudi Arabia's regulatory sandbox programs and the UAE's Personal Data Protection Law compel digital banks to demonstrate robust risk-management frameworks before launch. Multiple regulatory checkpoints-from central banks to commerce ministries-require continuous audits, driving demand for consulting, third-party assessments, and automation platforms. Compliance-driven purchases add momentum to the Middle East and Africa cybersecurity market as license applications surge.

Acute shortage of cybersecurity talent inflating service costs

Eighty-seven percent of UAE enterprises struggle to recruit qualified professionals despite monthly salaries exceeding AED 13,500 for consultants. Qatar records 434.09 cybersecurity roles per 100,000 residents, yet demand continues to outstrip supply, forcing organizations to outsource monitoring and incident response. Higher wage bills lift overall project costs and temper adoption rates, particularly among mid-tier enterprises, constraining the Middle East and Africa cybersecurity market.

Other drivers and restraints analyzed in the detailed report include:

- Escalating OT cyber-attacks on oil and gas assets driving ICS/SCADA security uptake

- Explosive mobile-money adoption in Sub-Saharan Africa requiring endpoint and fraud protection

- Fragmented data-protection laws across African nations raising compliance complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 69.28% of revenue in 2025 as organizations procured endpoint, network, and cloud-security suites in bulk. This dominance shows the purchasing power of large enterprises that still favor on-premise appliances for critical environments. Continued innovation in AI-driven threat detection reinforces solution spend, with vendors like SentinelOne adding security-posture management to defend shadow AI assets. The Middle East and Africa cybersecurity market nevertheless shows rising appetite for managed services, evident in a 14.68% CAGR outlook fueled by acute talent shortages and compliance burdens.

Professional services grow as integrators tailor complex hybrid architectures across sovereign-cloud environments. SMEs in particular gravitate toward SOC-as-a-Service offerings such as Liquid C2, which bundles monitoring, incident response, and regulatory reporting for a predictable fee structure. The shift reallocates share within the Middle East and Africa cybersecurity industry while preserving solution sales for large renovation projects.

On-premises architectures held 61.65% of the Middle East and Africa cybersecurity market size in 2025 due to data-sovereignty rules and legacy SCADA linkages. Yet cloud-delivered security is forecast to expand at 15.43% CAGR as regional providers establish local Points of Presence that meet residency mandates. Cisco's UAE Secure Service Edge node exemplifies cloud localization that lowers latency and aligns to GCC controls.

Hybrid models now dominate migration roadmaps. Organizations retain sensitive workloads in-country while routing analytics and sandboxing tasks to regional clouds. Gartner summit dialogues underscore zero-trust adoption as enterprises decouple identity from perimeter, further propelling cloud uptake within the Middle East and Africa cybersecurity market.

The Middle East and Africa Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and Geography.

List of Companies Covered in this Report:

- IBM Corporation

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Inc.

- Broadcom (Symantec)

- Sophos Ltd.

- Kaspersky Lab

- Microsoft Corp.

- CrowdStrike Holdings Inc.

- Darktrace plc

- Rapid7 Inc.

- Mandiant

- McAfee Corp.

- Splunk Inc.

- LogRhythm Inc.

- Proofpoint Inc.

- BAE Systems Applied Intelligence

- Help AG

- StarLink DMCC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sovereign-cloud and Residency Mandates across GCC Accelerating SOC Investments

- 4.2.2 Rapid Digital-Banking License Issuance in KSA and UAE Boosting Compliance-led Security Spend

- 4.2.3 Escalating OT Cyber-attacks on Oil and Gas Assets Driving ICS/SCADA Security Uptake

- 4.2.4 Explosive Mobile-Money Adoption in Sub-Saharan Africa Requiring Endpoint and Fraud Protection

- 4.2.5 Mega-Events Pipeline (Expo 2030, Neom, Dubai Airshow) Intensifying Critical-Infrastructure Hardening

- 4.2.6 New National Cyber Regulations (NCA ECC, UAE NESA, Egypt DP Law) Mandating Threat-Intel Sharing

- 4.3 Market Restraints

- 4.3.1 Acute Shortage of Cybersecurity Talent Inflating Service Costs

- 4.3.2 Fragmented Data-Protection Laws across African Nations Raising Compliance Complexity

- 4.3.3 Budget Constraints among African SMEs Prioritising Basic Digitisation over Security

- 4.3.4 Import Dependence on Security Appliances Exposed to Geopolitical Supply-Chain Disruptions

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 Middle East

- 5.5.1.1 Saudi Arabia

- 5.5.1.2 United Arab Emirates

- 5.5.1.3 Qatar

- 5.5.1.4 Bahrain

- 5.5.1.5 Kuwait

- 5.5.1.6 Oman

- 5.5.1.7 Israel

- 5.5.1.8 Turkey

- 5.5.2 Africa

- 5.5.2.1 South Africa

- 5.5.2.2 Egypt

- 5.5.2.3 Nigeria

- 5.5.2.4 Kenya

- 5.5.2.5 Morocco

- 5.5.2.6 Rest of Africa

- 5.5.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 IBM Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Palo Alto Networks Inc.

- 6.4.4 Fortinet Inc.

- 6.4.5 Check Point Software Technologies Ltd.

- 6.4.6 Trend Micro Inc.

- 6.4.7 Broadcom (Symantec)

- 6.4.8 Sophos Ltd.

- 6.4.9 Kaspersky Lab

- 6.4.10 Microsoft Corp.

- 6.4.11 CrowdStrike Holdings Inc.

- 6.4.12 Darktrace plc

- 6.4.13 Rapid7 Inc.

- 6.4.14 Mandiant

- 6.4.15 McAfee Corp.

- 6.4.16 Splunk Inc.

- 6.4.17 LogRhythm Inc.

- 6.4.18 Proofpoint Inc.

- 6.4.19 BAE Systems Applied Intelligence

- 6.4.20 Help AG

- 6.4.21 StarLink DMCC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment