|

시장보고서

상품코드

1851258

무균 포장 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

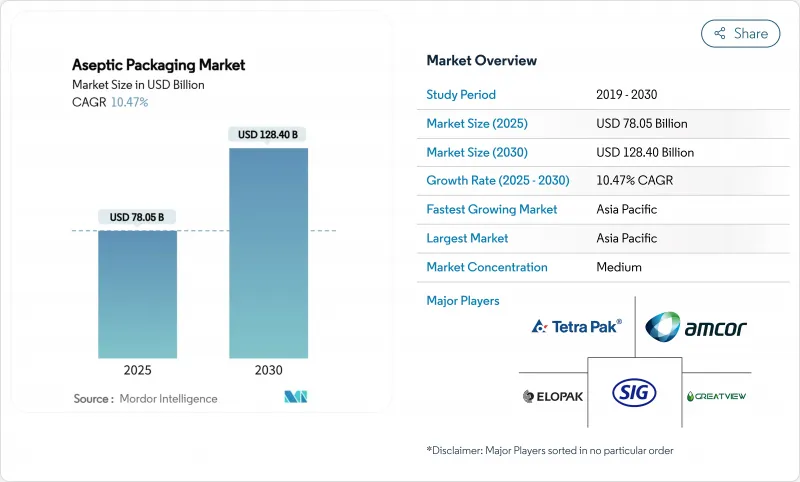

무균 포장 시장 규모는 2025년에 780억 5,000만 달러로 추정되고, 2030년에는 1,284억 달러에 이를 전망이며, CAGR 10.47%로 확대될 것으로 예측됩니다.

보존 가능한 식품 및 음료에 대한 수요 증가, 식품 안전 규칙의 엄격화 및 콜드체인 비용 절감의 필요성은 무균 상온 유통 형태의 매력을 강화하고 있습니다. 브랜드 소유자는 냉장 인프라가 아직 불완전한 지역에서 즉시 마실 수 있는(RTD) 기능성 음료 및 저장 가능한 유제품 수요 증가에 대응하기 위해 무균 라인을 확대하고 있습니다. 동시에, 생물 제제의 제조 및 맞춤형 치료가 무균 포장 시장의 의약품 수익 기반을 확대하고 있습니다. 알루미늄이 없는 하이 배리어 판지와 PFAS가 없는 코팅제와 같은 재료 과학의 혁신은 제조업체가 무균성을 희생하지 않고 새로운 지속가능성 의무를 준수하는 데 도움이 됩니다. 컨버터와 수지 제조업체의 통합은 불안정한 고분자 시장에서 구매력을 강화하고 디지털 인쇄는 급증하는 재고 관리 단위에 적합한 비용 효율적인 소량 생산을 가능하게 합니다.

세계의 무균 포장 시장 동향 및 인사이트

RTD 기능성 음료의 급성장

기능성 RTD 음료는 현재 민감한 미량 영양소, 프로바이오틱스, 식물 성분을 상온에서 최대 12개월간 가두는 무균 솔루션이 요구되고 있습니다. 각 브랜드는 편의점에서 라스트 원 마일의 유통을 촉진하면서 산소, 빛, 자외선 보호를 제공하는 하이 배리어 판지와 다층 병을 선택합니다. 미국, 중국, 태국의 음료 충전업체는 스포츠 중립, 에너지 차, 식물성 단백질의 출시에 대응하기 위해 시간당 48,000개 이상의 정격을 가진 새로운 고속 무균 라인을 도입했습니다. 식음료 등급의 무균성 및 의약품 등급 검증의 중복은 좁아지고 있으며, 바이알 및 앰풀 공급업체는 프리미엄 포지셔닝을 요구하는 음료 제조업체에 진입하도록 촉구하고 있습니다. 성분 공급자는 무균 처리에 의해 얻어지는 긴 보존 기간에 의해 더 적은 방부제와 더 많은 활성 화합물의 배합이 가능해지고, 보다 깨끗한 라벨 및 더 높은 소매 가격이 가능하게 된다고 지적합니다.

신흥아시아에서 유제품 유통 확대

인도, 베트남, 인도네시아에서는 완만하게 관리되는 냉장 공급망에서 무균 저장 가능한 우유와 요구르트로 업그레이드가 급속히 진행되고 있습니다. 도시의 유제품 가공업자는 송전망이 불안정하고 냉장 비용이 상승하는 농촌에 공급하기 위해 UHT 살균기나 브릭팩 충전기에 투자하고 있습니다. 중국에서는 2024년에 보존 가능한 음료에 대한 조제 분유의 사용이 금지되는 것으로 결정했기 때문에 순유 무균 라인에 대한 설비 투자가 잇따라, 135℃의 살균에 견디는 저산성 카톤 라미네이트에 대한 수요가 높아지고 있습니다. 다국적 브랜드는 현지 협동조합과 합작회사를 설립하여 원유를 확보하고 농장 근처에 모듈식 무균 마이크로플랜트를 배치하여 운송 비용을 절감하고 부패를 경감하고 있습니다. 그 결과, 무균 포장 시장은 아시아 신흥국 정부의 장기적인 식량 안보 과제에 필수적이 되고 있습니다.

다층 폴리머 가격의 난고하

폴리에틸렌과 폴리프로필렌의 가격은 2024년 파운드당 5센트 상승했으며, 컨버터의 마진을 단축하고 분기별로 충전을 촉진했습니다. 나프타와 에탄 원료 시장의 변동은 카톤 주입구, 캡 및 장벽 필름의 예산 조직을 복잡하게 만듭니다. 선도적인 구매자는 수년간 수지 계약으로 헤지하고 있지만 소규모 충전업자는 스팟 가격의 고통을 겪었으며 핫 필 라인을 무균 시설로 대체하기 위한 설비 프로젝트가 지연되었습니다. 크래커 콤플렉스에서의 계획 외 운영 정지 및 선적 병목 현상과 같은 세계적인 수지 공급의 구조적 제약은 가격 불안정성이 당분간 지속됨을 시사합니다.

부문 분석

유제품, 주스 및 RTD 커피에 침투하여 카톤 시장은 2024년 수익의 64%를 확보했습니다. 직사각형 풋 프린트는 팔레트 효율성과 선반의 외관을 극대화하고 새로운 스트로리스 클로저는 플라스틱 감소 목표에 호소합니다. 한편, 바이알과 앰풀은 주사용 생물제제, 백신, 세포 요법의 보급에 따라 2030년까지 연평균 복합 성장률(CAGR) 13.2%로 확대됩니다. 바이알 및 앰풀의 무균 포장 시장 규모는 인간 의료 및 동물 의료 모두 채용을 반영하여 2030년까지 97억 달러에 이를 것으로 예측됩니다. 병은 스무디와 같은 점도가 높은 음료와 더 큰 리실러블 형식이 소비 편의성을 높이는 향미 우유에게 여전히 중요합니다. 캔은 UHT 코코넛 워터와 고산성 과일 퓌레에서 견고한 내펑크성에 의해 틈새 위치를 유지하고 있지만, 알루미늄 가격의 변동과 젊은 소비자의 종이 기반 팩에 대한 기호에 의해 성장은 억제되고 있습니다. 파우치 기반의 백 인 박스 시스템은 컴팩트한 운송과 개봉 후 유통기한 연장을 요구하는 식음료 사업자를 매료하고 있습니다. 1회분의 파우치가 달린 파우치는 유아용 음료 및 스포츠 영양 젤에 휴대성을 제공합니다.

탄소 실적 감소 추구는 제품 수준의 혁신을 자극하고 있습니다. SIG사가 2025년에 발매한, 12개월의 상온 보존이 가능한 완전하게 리사이클 가능한 알루미늄 프리의 1L 카톤은 유럽의 대기업 유제품 브랜드로부터 재빨리 채용되었습니다. 이와는 별도로, 유리병 제조업체는 불활성 접촉면을 유지하면서 무게를 30% 줄이는 고분자와 유리 하이브리드 용기를 개발하여 세계적인 백신 캠페인에서 운임 배출을 완화하고 있습니다. 신소재의 출현과 함께 장벽 성능, 재활용성 및 충전 속도에서 제품 수준의 차별화는 시장 경쟁에서 우위를 형성할 것입니다.

지역 분석

아시아태평양은 중국, 인도, 인도네시아가 견인하여 2024년 매출의 38.4%를 차지했습니다. 인도의 국가 영양 프로그램은 2027년까지 팩 우유의 보급률을 15% 이상으로 끌어올리는 것을 목표로 하고 있으며, 무균 처리 능력에 대한 관민 투자를 촉진하고 있습니다. 구자라트에 있는 SIG의 9,000만 유로의 새로운 공장은 현지 유제품과 마시는 요구르트에 연간 40억 팩의 생산량을 추가합니다. UHT 카톤 들이 분유를 금지하는 중국 정책으로 가공업자는 보다 무결성이 높은 업체에게 밀려, 가격 규율이 강화되고 이폭이 확대되고 있습니다. 동남아시아의 신흥기업은 비타민 강화차를 250mL의 슬림한 판지로 출시해 외출처에서의 소비를 섭취하려고 합니다.

남미는 가장 급성장하고 있는 지역으로, 2030년까지의 CAGR은 14.21%로 예측되고 있습니다. 브라질의 포장 식품 시장은 2024년에 1,136억 달러에 이르렀고, 인플레이션 압력이 소비자에게 대형으로 보존되는 상품의 구입을 촉구했기 때문입니다. 디젤 연료와 전기 요금이 높기 때문에 내륙 지역의 유통 센터에 대한 투자는 상온 제품을 선호합니다. 아르헨티나 유제품 수출업체는 유연한 파우치 라인을 활용하여 냉장 없이 유당이 없는 우유를 칠레와 페루에 출하합니다.

북미와 유럽은 한자릿수 중반의 성장을 나타내고 있지만, 이는 수량 확대보다 지속가능성을 중시한 소재 교환이 뒷받침하고 있습니다. EU의 PFAS 금지령은 산화규소 기반 판지 장벽의 상업화를 자극하며, 미국 필러는 노동력 부족을 보완하기 위해 간호도가 높은 구역에서 로봇을 채택합니다. 중동 및 아프리카는 금액적으로 작은 반면, 인구 역학의 성장과 정부의 식량 안보 전략에 연결되는 장기적인 상승 여지가 있습니다. 이집트의 산업 지역에는 지역 공급을 목적으로 하는 UFlex의 2억 달러의 라미네이트 보드 복합물이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- RTD 기능성 음료의 급성장

- 신흥 아시아의 상온 유제품 유통 확대

- 엄격한 식품 안전 규제가 무균 포장의 채용 뒷받침

- 콜드체인에서 선반 스테이블 물류로의 인플레이션 연동 시프트

- 지속 가능한 경량 포장으로의 시프트 의무화됨

- D2C 브랜드에 있어서의 디지털 및 인쇄 대응 쇼트 SKU의 대두

- 시장 성장 억제요인

- 다층 폴리머 가격의 변동

- 아셉틱 충전 라인의 높은 초기 CAPEX

- 알루미늄박 라미네이트의 한정된 재활용 인프라

- PFAS 배리어 코팅을 둘러싼 규제의 불확실성

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 가격 분석

- 음료의 무균 포장-수요 인사이트

제5장 시장 규모 및 성장 예측

- 제품별

- 판지

- 병

- 캔

- 가방 및 파우치

- 바이알 및 앰풀

- 재료 구성별

- 종이 및 판지

- 플라스틱(PP, PE, PET)

- 유리

- 금속(알루미늄, 스틸)

- 복합 라미네이트

- 용도별

- 음료

- RTD 음료

- 우유 음료

- 식품

- 가공 식품

- 과일 및 채소

- 유제품

- 의약품

- 퍼스널케어 및 화장품

- 음료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Tetra Pak International SA

- SIG Combibloc Group

- Amcor PLC

- Elopak ASA

- IPI SRL(Coesia Group)

- DS Smith PLC

- Smurfit Kappa Group

- Mondi PLC

- Uflex Limited

- Schott AG

- Gerresheimer AG

- Toyo Seikan Group

- CDF Corporation

- BIBP Sp. z oo

- Nampak Ltd

- Greatview Aseptic Packaging

- Liqui-Box(Graphic Packaging)

- OPLATEK Group

- Sealed Air Corporation

- ProAmpac

제7장 시장 기회 및 향후 전망

AJY 25.11.21The aseptic packaging market size is valued at USD 78.05 billion in 2025 and is projected to reach USD 128.40 billion by 2030, expanding at a 10.47% CAGR.

Growing demand for shelf-stable foods and beverages, stricter food-safety rules, and the need to trim cold-chain costs are reinforcing the appeal of sterile, ambient-distribution formats. Brand owners are scaling aseptic lines to meet rising demand for ready-to-drink (RTD) functional beverages and for shelf-stable dairy in regions where refrigeration infrastructures remain patchy. At the same time, biologics manufacturing and personalized therapies are widening the pharmaceutical revenue base for the aseptic packaging market. Material science breakthroughs-such as aluminum-free high-barrier cartons and PFAS-free coatings-help manufacturers comply with new sustainability mandates without sacrificing sterility. Consolidation among converters and resin producers is bolstering purchasing leverage in a volatile polymer market, while digital printing is enabling cost-effective short runs that suit proliferating stock-keeping units.

Global Aseptic Packaging Market Trends and Insights

Rapid Growth of RTD Functional Beverages

Functional RTD drinks now demand aseptic solutions that lock in sensitive micronutrients, probiotics, and botanicals for up to 12 months at ambient temperatures. Brands are selecting high-barrier cartons and multilayer bottles that offer oxygen, light, and UV protection while easing last-mile distribution in convenience stores. Beverage fillers in the United States, China, and Thailand have installed new high-speed aseptic lines rated above 48,000 bottles per hour to serve sports-nutrition, energy-tea, and plant-based protein launches. The overlap between food-grade sterility and pharmaceutical-grade validation is narrowing, encouraging suppliers of vials & ampoules to court beverage customers seeking premium positioning. Ingredient suppliers note that the longer shelf life afforded by aseptic processing allows them to blend less preservative and more active compounds, supporting cleaner labels and higher retail prices.

Expansion of Ambient Dairy Distribution in Emerging Asia

India, Vietnam, and Indonesia are rapidly upgrading from loosely supervised chilled supply chains to aseptic shelf-stable milk and yogurt. Urban dairy processors are investing in UHT sterilizers and brick-pack fillers to reach rural districts where grid instability inflates refrigeration costs. In China, the 2024 decision to prohibit reconstituted milk powder in shelf-stable beverages elicited a wave of capex for pure-milk aseptic lines, driving demand for low-acid carton laminates that can withstand 135 °C sterilization. Multinational brands are forming joint ventures with local cooperatives to secure raw milk and deploy modular aseptic micro-plants close to farms, slashing road-haul costs and mitigating spoilage. As a result, the aseptic packaging market is becoming integral to the long-term food-security agendas of emerging Asian governments.

Volatility in Multilayer Polymer Prices

Polyethylene and polypropylene prices rose by 5 cents per pound in 2024, tightening converter margins and prompting quarterly surcharges. Fluctuating naphtha and ethane feedstock markets complicate budgeting for carton spouts, caps, and barrier films. While large purchasers hedge through multi-year resin contracts, small fillers experience spot-price pain that slows capital projects aimed at replacing hot-fill lines with aseptic equipment. Structural constraints in global resin supply, including unplanned outages at cracker complexes and shipping bottlenecks, signal that price volatility will persist for the near term.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Food-Safety Regulations Pushing Sterile Packaging Adoption

- Inflation-Linked Shift From Cold-Chain to Shelf-Stable Logistics

- High Initial CAPEX for Aseptic Filling Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cartons secured 64% of 2024 revenue within the aseptic packaging market thanks to deep penetration in dairy, juice, and RTD coffee. Their rectangular footprint maximizes pallet efficiency and shelf facings, and new straw-less closures appeal to plastic-reduction goals. Meanwhile, vials & ampoules are expanding at a 13.2% CAGR through 2030 as injectable biologics, vaccines, and cell therapies proliferate. The aseptic packaging market size for vials & ampoules is projected to reach USD 9.7 billion by 2030, reflecting adoption in both human and veterinary medicine. Bottles remain important for high-viscosity drinks such as smoothies and for flavored milk where larger resealable formats enhance consumption convenience. Cans hold niche positions in UHT coconut water and high-acid fruit purees due to their robust puncture resistance, though growth is tempered by aluminum price swings and by younger consumers' preference for paper-based packs. Pouch-based bag-in-box systems attract food-service operators seeking compact shipping and extended post-opening shelf life; single-serve spouted pouches offer portability for early-childhood beverages and sports nutrition gels.

The pursuit of carbon-footprint cuts is stimulating product-level innovation. SIG's 2025 launch of a fully recyclable, aluminum-free 1 L carton that maintains a 12-month ambient shelf life won early adoption from leading European dairy brands. Separately, glass vial manufacturers have developed polymer-over-glass hybrid containers that reduce weight by 30% while retaining inert contact surfaces, easing freight emissions in global vaccine campaigns. As new materials emerge, product-level differentiation in barrier performance, recyclability, and filling speed will continue to shape competitive advantage within the aseptic packaging market.

Aseptic Packaging Market Report is Segmented by Product (Cartons, Bottles, Cans, Bags and Pouches, and More), Material Composition (Paper and Paperboard, Plastics, Glass, Metal, Composite Laminates), Application (Beverage, Food, Pharmaceuticals, Personal Care and Cosmetics), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.4% of revenues in 2024, driven by China, India, and Indonesia. National nutrition programs in India aim to increase packaged milk penetration above 15% by 2027, catalyzing public-private investment in aseptic capacity. SIG's EUR 90 million green-field plant in Gujarat adds 4 billion pack annual output devoted to local dairy and drinkable yogurt. China's policy forbidding reconstituted milk powder in UHT cartons is pushing processors toward higher-integrity manufacturers, reinforcing price discipline and lifting margins. Southeast Asian start-ups are launching vitamin-fortified teas in 250 mL slim cartons to capture on-the-go consumption.

South America is the fastest growing region, projected to rise at 14.21% CAGR through 2030. Brazil's packaged-food market reached USD 113.6 billion in 2024 as inflationary pressures encouraged consumers to favor large-format, shelf-stable purchases. Investments in inland distribution centers favor ambient products due to high diesel and electricity costs. Argentina's dairy exporters are leveraging flexible pouch lines to ship lactose-free milk to Chile and Peru without refrigeration.

North America and Europe show mid-single-digit growth, propelled by sustainability-driven material swaps rather than volume expansion. The EU PFAS ban stimulates the commercialization of silicon-oxide-based carton barriers, while US fillers adopt robotics in high-care zones to offset labor shortages. The Middle East and Africa, although smaller in value, present long-term upside tied to demographic growth and government food-security strategies. Egypt's industrial zones host UFlex's USD 200 million laminated-board complex aimed at regional supply

- Tetra Pak International SA

- SIG Combibloc Group

- Amcor PLC

- Elopak ASA

- IPI SRL (Coesia Group)

- DS Smith PLC

- Smurfit Kappa Group

- Mondi PLC

- Uflex Limited

- Schott AG

- Gerresheimer AG

- Toyo Seikan Group

- CDF Corporation

- BIBP Sp. z o.o.

- Nampak Ltd

- Greatview Aseptic Packaging

- Liqui-Box (Graphic Packaging)

- OPLATEK Group

- Sealed Air Corporation

- ProAmpac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of RTD functional beverages

- 4.2.2 Expansion of ambient dairy distribution in emerging Asia

- 4.2.3 Stringent food-safety regulations pushing sterile packaging adoption

- 4.2.4 Inflation-linked shift from cold-chain to shelf-stable logistics (under-reported)

- 4.2.5 Shift toward sustainable, lightweight packaging mandates

- 4.2.6 Rise of digital?print-enabled short SKUs for D2C brands (under-reported)

- 4.3 Market Restraints

- 4.3.1 Volatility in multilayer polymer prices

- 4.3.2 High initial CAPEX for aseptic filling lines

- 4.3.3 Limited recycling infrastructure for aluminum-foil laminates (under-reported)

- 4.3.4 Regulatory uncertainty around PFAS barrier coatings (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Aseptic Packaging for Beverages - Demand Insights

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Cartons

- 5.1.2 Bottles

- 5.1.3 Cans

- 5.1.4 Bags and Pouches

- 5.1.5 Vials and Ampoules

- 5.2 By Material Composition

- 5.2.1 Paper and Paperboard

- 5.2.2 Plastics (PP, PE, PET)

- 5.2.3 Glass

- 5.2.4 Metal (Aluminum, Steel)

- 5.2.5 Composite Laminates

- 5.3 By Application

- 5.3.1 Beverage

- 5.3.1.1 Ready-to-drink (RTD) Beverages

- 5.3.1.2 Dairy-based Beverages

- 5.3.2 Food

- 5.3.2.1 Processed Food

- 5.3.2.2 Fruits and Vegetables

- 5.3.2.3 Dairy Food

- 5.3.3 Pharmaceuticals

- 5.3.4 Personal Care and Cosmetics

- 5.3.1 Beverage

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Tetra Pak International SA

- 6.4.2 SIG Combibloc Group

- 6.4.3 Amcor PLC

- 6.4.4 Elopak ASA

- 6.4.5 IPI SRL (Coesia Group)

- 6.4.6 DS Smith PLC

- 6.4.7 Smurfit Kappa Group

- 6.4.8 Mondi PLC

- 6.4.9 Uflex Limited

- 6.4.10 Schott AG

- 6.4.11 Gerresheimer AG

- 6.4.12 Toyo Seikan Group

- 6.4.13 CDF Corporation

- 6.4.14 BIBP Sp. z o.o.

- 6.4.15 Nampak Ltd

- 6.4.16 Greatview Aseptic Packaging

- 6.4.17 Liqui-Box (Graphic Packaging)

- 6.4.18 OPLATEK Group

- 6.4.19 Sealed Air Corporation

- 6.4.20 ProAmpac

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment