|

시장보고서

상품코드

1639514

라틴아메리카의 무균 포장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Latin America Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

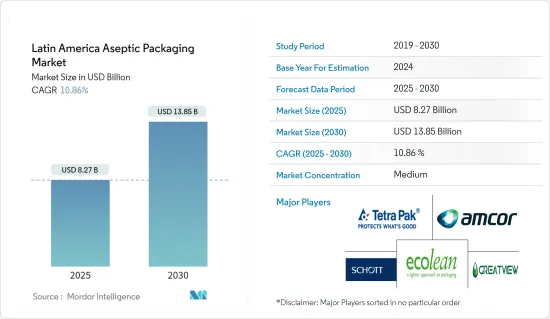

라틴아메리카의 무균 포장 시장 규모는 2025년 82억 7,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 10.86%의 CAGR로 2030년에는 138억 5,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 라틴아메리카는 많은 원자재와 식품을 생산하는 지역이기 때문에 시장 조사에서 뛰어난 잠재력을 제공합니다. 브라질, 아르헨티나, 콜롬비아, 멕시코 등의 국가에서 급속한 산업화가 경제 성장을 주도하고 있습니다. 다른 대륙과 마찬가지로, 환경 친화적인 신기술의 사용은 책임감 있고 의식적인 소비의 증가 추세에 대한 식품 체인 전반에 걸쳐 반응과 해결책을 제공할 수 있는 길을 열어주고 있습니다. 이러한 발전은 품질과 안전을 보장하고 식품의 유통기한을 연장하는 가공 및 보존 단계에서 가장 두드러지게 나타납니다. 무균 포장은 더 안전하고 수익성 높은 식품 포장 옵션으로 점점 더 인기를 얻고 있습니다.

- 건강한 대체 식품에 대한 소비자의 선호는 무균 포장에 대한 잠재적인 기술적, 비용적 문제에도 불구하고 무균 포장에 대한 투자 증가로 이어지고 있습니다. 더 건강한 대안을 찾는 소비자의 선호로 인해 무균 포장의 인기가 높아짐에 따라 제조업체들은 이러한 수요에 대응하기 위해 포장 및 충전 기술에 투자하고 있습니다. 브라질에서는 기능적이고 건강한 대안에 대한 소비자의 선호가 제품 개발의 원동력이 되고 있습니다. 유제품 제조업체들은 유제품 기반 제품에 대한 수요 증가에 대응하기 위해 무균 충전기를 도입하는 데 주력하고 있습니다.

- 이에 따라 브라질 유제품 회사 Shefa와 Lider Alimentos는 무균 충전 기계 및 포장 솔루션 공급 및 설치의 우선 파트너로 SIG를 선택했으며, SIG는 브라질에서 첨단 무균 충전 기술을 제공하고 있습니다. 상파울루와 파라나에 위치한 생산 기지에 9대의 무균 충전기를 설치하여 이미 가동에 들어갔습니다.

- Ball Corporation은 남미 지역에서의 사업 확장을 발표하며 페루 치르카에 제조 공장을 신설했습니다. 확장 후 이 공장은 연간 10억 개 이상의 음료수 캔을 생산할 수 있는 능력을 갖추게 됩니다. 소비자들이 신선하고 새로운 맛과 고급스러운 포장을 계속 추구함에 따라 프리미엄화는 주류 부문 기업들에게 중요한 촉진제가 되고 있습니다. 업계 기업들은 세계 브랜드와 특수 프리미엄 브랜드의 다양한 포트폴리오를 구축하기 위한 투자에 집중하고 있습니다.

- 또한, 멕시코에서는 청량음료 및 기타 무알콜 음료에 대한 수요가 증가하고 있으며, 예측 기간 동안 무균 포장에 대한 수요가 증가할 것으로 예상됩니다. 예를 들어, National Institute of Statistics and Geography(INEGI)에 따르면, 멕시코의 가향 청량음료 생산액은 2023년 2월 28억 1,106만 MXN(1억 6,751만 달러)에서 2023년 4월에는 34억 7,000만 MXN(2억 7,000만 달러)로 증가할 것으로 예상됩니다. 4억 7,100만 MXN(2억 7,055만 달러)를 넘어섰습니다.

- 그러나 무균 상자에는 알루미늄과 폴리에틸렌 성분이 포함되어 있기 때문에 포장재에서이 물질을 제거하기가 어렵습니다. 정확한 재활용(재료가 품질 손실없이 생산주기의 이전 단계로 재활용되는 것)을 달성하기 위해서는 테트라 팩의 모든 층을 분리하고 더 많은 테트라 팩을 생산하기 위해 재사용해야합니다. 또한, 이러한 기계를 사용할 수 있는 것은 특정 진입 기업에 국한되어 있습니다. 재활용에는 많은 장비와 물, 에너지와 같은 투입물이 필요하며, 많은 재활용 센터가 이를 갖추지 못하고 있습니다. 이러한 요인들이 시장 성장의 걸림돌이 될 수 있습니다.

라틴아메리카 무균 포장 시장 동향

무균 상자는 조사 대상 시장에서 수요 증가를 확인합니다.

- 무균 상자는 특히 오렌지 주스나 수프와 같은 액체를 위해 다층 포장으로 만들어진 식품 용기입니다. 이 용기는 종이, 플라스틱, 금속의 층으로 만들어집니다. 깨끗한 흐름으로 처리되면 재료는 재활용이 가능합니다. 무균 상자는 약 70%가 종이(경도와 강도를 위해), 약 24%가 폴리에틸렌(포장을 밀봉하기 위해 4겹으로 사용), 약 6%가 알루미늄 포일(공기와 빛에 대한 장벽으로 사용)로 만들어집니다. 이 상자는 냉장보관 없이도 1년 이상 액체를 안전하게 보관할 수 있습니다.

- 그 결과, 음료 및 식품 공급업체들은 비용 및 환경적 측면, 특히 상온 운송 및 보관의 이점을 고려하여 무균 포장을 선호하고 있습니다. 또한, 무균 포장은 재활용이 가능하고 친환경적인 파우치 포장을 지원하기 때문에 소량을 선호하고 구매 빈도가 높은 소비자를 대상으로 하는 경우가 많기 때문에 이러한 제품에 대한 수요가 상당히 높습니다.

- 이러한 성장은 주로 간편하고 바로 먹을 수 있는 제품의 인기 증가와 보존 기술의 향상에 기인합니다. 또한, 유기농 및 건강식품에 대한 수요 증가는 브라질에서 무균 포장의 사용 증가로 이어지고 있으며, Tetra Pak, Amcor, SIG Combibloc과 같은 주요 무균 포장 제조업체들은 브라질에 많은 투자를 하고 있으며, 앞으로도 계속될 것으로 예상됩니다.

- 라이프스타일의 변화와 이에 따른 소비자의 가공식품, 포장식품, 즉석조리식품 및 음료에 대한 의존도가 높아지면서 무균 포장 솔루션에 대한 수요가 증가하고 있습니다. 슈퍼마켓 문화의 출현은 쇼핑 환경을 변화시켰으며, 특히 식음료에 대한 포장의 필요성을 증가시켰습니다. 사람들의 라이프스타일의 변화는 바로 먹을 수 있는 제품으로의 전환을 가져왔습니다. 또한, 이러한 제품은 무균 포장으로 포장되어 제품이 오염되지 않고 변조되지 않고 안전하게 소비될 수 있도록 보장합니다.

- 우유용 무균 상자는 매우 높은 온도에서 처리되어 우유에 포함된 모든 유해한 박테리아가 파괴됩니다. 그 후, 우유는 즉시 무균 환경에서 공기의 침입을 막는 특수 포장재로 포장됩니다. 이 과정을 통해 우유의 유통기한이 훨씬 더 길어집니다. 우유용 무균 카톤은 빛과 주변 산소로부터 제품을 보호하기 때문에 전 세계적으로 수요가 증가하고 있습니다.

- 미국 농무부에 따르면, 멕시코의 낙농 산업은 2023년 1,342만 리터의 우유를 생산할 것으로 예상되며, 이는 2018년의 약 1,254만 톤에서 증가할 것으로 예상됩니다. 이러한 생산량 증가는 예측 기간 동안 시장 성장을 뒷받침할 것으로 예상됩니다.

브라질이 큰 비중을 차지할 것으로 예상

- 브라질 식품 산업은 무균 포장의 주요 소비자 중 하나이며, 식품의 유통기한을 연장하고 오염을 줄입니다. 무균 포장은 의약품 및 의료 분야에서도 부패를 최소화하고 제품 안전성을 향상시키며, 멸균 및 기타 포장 기술과 함께 사용되어 제품 안전을 보장합니다.

- 시장 개척자들은 신흥국 산업을 앞서 나가기 위해 연구개발에 투자하고 있습니다. 신제품 출시 동향이 시장 수요를 뒷받침하고 있습니다. 특히 제약 산업의 무균 포장에 대한 수요도 증가하고 있습니다. 각국 정부는 무균 포장 시장의 성장을 촉진하기 위해 의료 부문에 대한 규제를 강화하고 있습니다.

- 브라질 보건부는 무균 포장을 규제하고, 브라질의 우수의약품 제조 및 품질 관리기준(GMP) 규정 준수를 보장하고 있습니다. 또한, 브라질 정부는 2019년에 실무 그룹을 설립하여 브라질에서 무균 포장을 사용하기 위한 전략을 논의하고 개발하기 위해 노력하고 있습니다.

- 무균 포장 시장은 향후 몇 년 동안 인도에서 비약적으로 성장할 것으로 예상됩니다. Organic Trade Association에 따르면, 브라질의 유기농 포장 식품 소비량은 2020년 7,400만 달러에서 2025년 1억 5,000만 달러로 증가할 것으로 예상됩니다. 2025년에는 1억 5천만 달러로 증가할 것으로 예상됩니다.

- 새로운 기술과 혁신으로 제조업체가 보다 효율적이고 지속가능한 무균 포장 솔루션을 구축할 수 있게 됨에 따라 향후 몇 년 동안 시장이 성장할 것으로 예상됩니다. 이 지역에서는 알코올 음료의 소비가 증가하고 있으며, 와인 포장에는 백 인 박스, 맥주에는 캔, 증류주에는 병이 사용될 것으로 예상됩니다. 예를 들어, Banco do Nordeste가 발표한 기사에 따르면, 브라질의 알코올 음료 소비량은 2021년 110억 9,000만 리터에서 2024년 122억 9,000만 리터에 달할 것으로 예상됩니다.

라틴아메리카 무균 포장 산업 개요

라틴아메리카의 무균 포장 시장은 반고정적이며, 소수의 업체들이 국내외 시장에서 사업을 전개하고 있습니다. 시장은 중간 정도 통합된 것으로 보이며, 진입 기업들은 제품 혁신, 합병, 인수 등 다양한 전략을 채택하여 진입 범위를 확장하고 경쟁을 유지하고 있습니다. 주요 시장 진입 기업으로는 Bemis Company Incorporation, DS Smith PLC, SIG Combibloc Group AG, Tetra Pak International 등이 있습니다.

- 2023년 3월, 칠레에 본사를 둔 식품 기술 유니콘 NotCo는 SIG와 파트너십을 맺어 NotCo는 동물성 식품을 대체할 수 있는 식물성 대체 식품 NotCreme을 SIG의 카톤 포장으로 출시할 수 있게 되었습니다. 이번 제휴를 통해 NotCo는 식물성 식품에 대한 전문성과 적응력을 더욱 강화할 수 있게 되었습니다. 노트밀크 오리지널, 제로슈가, 세미슈가, 초콜릿 밀크 제품도 SIG의 무균 카톤 팩으로 출시될 예정입니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 역학

- 시장 성장 촉진요인

- 식품 및 음료 산업의 무균 포장 수요 확대

- 시장 과제

- 포장 재료 재활용 어려움

제6장 시장 세분화

- 제품별

- 카톤

- 백·파우치

- 캔

- 보틀

- 용도별

- 음료

- RTD(Ready to Drink)

- 유음료

- 식품

- 가공식품

- 과일·야채

- 유제품

- 의약품

- 음료

- 국가별

- 브라질

- 아르헨티나

- 멕시코

제7장 경쟁 구도

- 기업 개요

- Amcor PLC

- Bemis Company Inc.

- DS Smith PLC

- Elopak AS

- Mondi PLC

- Reynold Group Holdings PLC

- Sonoco Products Company

- Smurfit Kappa Group PLC

- SIG Combibloc Group AG

- Stora Enso Oyj

제8장 투자 분석

제9장 시장 전망

ksm 25.02.10The Latin America Aseptic Packaging Market size is estimated at USD 8.27 billion in 2025, and is expected to reach USD 13.85 billion by 2030, at a CAGR of 10.86% during the forecast period (2025-2030).

Key Highlights

- Latin America offers excellent potential in the market studied as a region that produces a lot of raw resources and food products. Rapid industrialization in countries like Brazil, Argentina, Columbia, and Mexico is driving economic growth. As in other continents, the use of new, more environmentally friendly technology is paving the way for the provision of reactions and solutions along the whole food chain to the trend of rising responsible and conscious consumption. These developments are most apparent throughout the processing and preservation stages when they assure quality and safety and extend the food's shelf life. Aseptic packaging is becoming increasingly popular as a safer and more profitable food packaging option.

- Consumers' preference for healthier alternatives is leading to a surge in investment in aseptic packaging despite the potential technical and cost issues associated with the formats. As aseptic designs become increasingly popular due to consumer preference for healthier alternatives, manufacturers are investing in packaging and fill technologies to meet this demand. In Brazil, product development is being driven by consumer preference for functional and healthier options. Dairy companies are focusing on installing aseptic fill machines to cater to the increasing demand for dairy-based products.

- In line with this, Shefa and Lider Alimentos, two Brazilian dairy companies, selected SIG as their preferred partner for supplying and installing aseptic fillers and packaging solutions. SIG is the provider of advanced aseptic fill technology in Brazil. It installed nine aseptic fill machines at production sites in Sao Paulo and Parana, where the systems have already started operating.

- Ball Corporation announced it was expanding its operations in South America, landing in Peru with a new manufacturing plant in Chilca. After expansion, the plant will have a production capacity of over 1 billion beverage cans annually. Premiumization has been a critical growth driver for players in the alcohol space due to consumers' continued desire for refreshing and newer tastes and premium packaging. The companies in the industry have been focused on investing in crafting a diverse portfolio of global and specialty premium brands.

- Additionally, the growing demand for soft drinks and other non-alcoholic beverages in Mexico is expected to support the need for aseptic packaging in the forecast timeframe. For instance, according to the National Institute of Statistics and Geography (INEGI), the production value of flavored soft drinks in Mexico amounted to over MXN 3474.71 million (USD 207.05 million) in April 2023, compared to MXN 2811.06 million (USD 167.51 million) in February 2023.

- However, it is difficult to remove this material from packaging due to the presence of aluminum and polyethylene components in aseptic cartooning. To achieve accurate recycling (where materials are recycled to a previous stage of the production cycle without loss of quality), all the layers of Tetra Pak would need to be separated and reused to produce more Tetra Pak. Additionally, the availability of such machines is limited to certain players. Recycling requires a lot of equipment and inputs, such as water and energy, and many recycling centers do not have these. Such factors might hinder market growth.

Latin America Aseptic Packaging Market Trends

Aseptic Cartons to Witness Increased Demand in the Market Studied

- Aseptic cartons are food containers built from multi-layer packing, particularly for liquids like orange juice and soups. These containers are made of layers of paper, plastic, and metal. Once processed into a clean stream, the material is recyclable. Aseptic cartons are made up of approximately 70% paper (for stiffness and strength), roughly 24% polyethylene (used in four layers to seal the package hermetically), and nearly 6% aluminum foil (used as a barrier against air and light). The boxes keep liquids safe for a year or longer without refrigeration.

- As a result, food and beverage vendors are inclining toward aseptic packaging, considering cost and environmental benefits, especially in terms of ambient shipping and storage. Also, as aseptic packaging supports packaging through recyclable and eco-friendly pouches, which often target consumers who prefer small quantities and make purchases more frequently, the demand for such products is considerably high.

- This growth has been primarily driven by the increasing popularity of convenience and ready-to-eat products and the improvement in preservation technologies. In addition, the rising demand for organic and healthy foods has also led to the increased use of aseptic packaging in Brazil. Major aseptic packaging manufacturers, such as Tetra Pak, Amcor, and SIG Combibloc, have invested heavily in Brazil and are expected to continue in the coming years.

- Changing lifestyles and the consequent dependence of consumers on processed, packaged, and pre-cooked food and beverages are increasing the demand for aseptic packaging solutions. The advent of the supermarket culture has also altered the shopping landscape and has increased the need for packaging, especially in food and beverage products. The altering lifestyle of people has resulted in the shift to ready-to-eat products. In addition, these products are packed in aseptic packaging to ensure that the products remain uncontaminated, tamper-proof, and safe for consumption.

- Aseptic cartons for milk are processed at extremely high temperatures, which destroy any harmful bacteria in the milk. The milk is then instantly cartooned in a sterile environment into specialized packaging that prevents air from penetrating. The shelf-life of the milk becomes much longer after this operation. The demand for aseptic cartons for milk is increasing globally, as they protect the product from light and ambient oxygen, resulting in increased shelf life.

- According to the US Department of Agriculture, the Mexican dairy industry produced 13.42 million liters of milk in 2023, up from around 12.54 million metric tons in 2018. Such production growth is expected to support the market growth during the forecast period.

Brazil is Expected to Hold a Significant Share

- The Brazilian food industry is one of the primary consumers of aseptic packing, which extends the shelf life of food products and reduces contamination. Packaging is also employed in the pharmaceutical and medical sectors to minimize spoilage, improve product safety, and ensure product safety when used with sterilization or other packaging technologies.

- Market players invest in research and development to stay ahead of developing industries. Market trends in new product launches support market demand. Notably, the pharmaceutical industry's demand for aseptic packaging is also increasing. Governments across the country are increasing regulations on the healthcare sector to boost the growth of the aseptic packaging market.

- The Ministry of Health in Brazil regulates aseptic packing and ensures that it complies with the country's Good Manufacturing Practices regulations. Additionally, the Brazilian government established a Working Group in 2019 to discuss and develop strategies for using aseptic packing in Brazil.

- The aseptic packaging market is expected to expand in the country exponentially over the next couple of years. The growth rates included ready meals, breakfast cereals, baby food, sauces, dressings and condiments, processed meat, seafood, and soup. According to the Organic Trade Association, the consumption of organic packaged food and beverages in Brazil is expected to increase from USD 74 million in 2020 to USD 105 million in 2025.

- The market is expected to grow in the coming years as new technologies and innovations enable manufacturers to create more efficient and sustainable aseptic packaging solutions. Increasing consumption of alcoholic beverages in the region will boost the use of the bag in the box for wine packaging, cans for beers, and bottles for spirits. For instance, according to an article published by Banco do Nordeste, the consumption of alcoholic beverages in Brazil is expected to reach 12.29 billion liters by 2024 from 11.09 billion liters in 2021.

Latin America Aseptic Packaging Industry Overview

The Latin American aseptic packaging market is semi-consolidated, as a few vendors operate in the domestic and international markets. The market appears to be moderately consolidated, with the players adopting various strategies, such as product innovation, mergers, and acquisitions, to expand their reach and stay competitive. Some of the major players in the market are Bemis Company Incorporation, DS Smith PLC, SIG Combibloc Group AG, and Tetra Pak International.

- In March 2023, Chile-based NotCo, a food-tech unicorn, partnered with SIG, enabling NotCo to launch NotCreme, a plant-based alternative to animal-derived food products, in SIG's carton packaging. This partnership further strengthens NotCo's expertise and adaptability in plant-based foods. NotMilk Originals, zero-sugar, semi-sugar, and chocolate milk products will also be available in aseptic carton packs from SIG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Aseptic Packaging in the Food and Beverage Industry

- 5.2 Market Challenges

- 5.2.1 Difficulty in Recycling the Packaging Material

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Cartons

- 6.1.2 Bags and Pouches

- 6.1.3 Cans

- 6.1.4 Bottles

- 6.2 By Application

- 6.2.1 Beverages

- 6.2.1.1 Ready-to-Drink

- 6.2.1.2 Dairy-based Beverages

- 6.2.2 Food

- 6.2.2.1 Processed Food

- 6.2.2.2 Fruits and Vegetables

- 6.2.2.3 Dairy Food

- 6.2.3 Pharmaceutical

- 6.2.1 Beverages

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Argentina

- 6.3.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Bemis Company Inc.

- 7.1.3 DS Smith PLC

- 7.1.4 Elopak AS

- 7.1.5 Mondi PLC

- 7.1.6 Reynold Group Holdings PLC

- 7.1.7 Sonoco Products Company

- 7.1.8 Smurfit Kappa Group PLC

- 7.1.9 SIG Combibloc Group AG

- 7.1.10 Stora Enso Oyj