|

시장보고서

상품코드

1851365

열화상 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Thermal Imaging Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

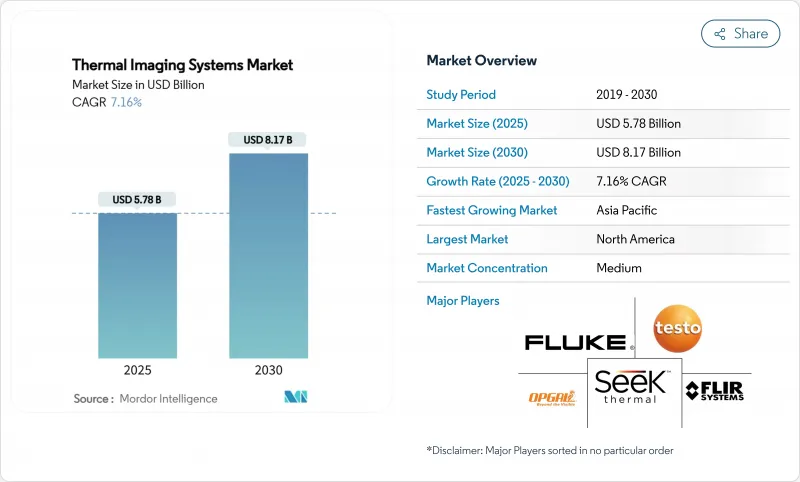

세계의 열화상 시스템 시장 규모는 2025년 57억 8,000만 달러, 2030년에는 81억 7,000만 달러에 이르고, CAGR 7.16%로 확대될 것으로 예측됩니다.

가속화하는 방위 근대화, 확대하는 산업 자동화, 의무화된 자동차 안전 기능 등이 수요 증가에 박차를 가하고 있습니다. NFPA-70B 서모그래피의 표준화는 제조 및 유틸리티에서 안정적인 조달 사이클을 자극하고 비냉각 장파장 적외선(LWIR)의 가격 하락은 가용성을 넓히고 있습니다. 이와 병행하여 자동차 제조업체는 보행자 보호 규정을 준수하기 위해 ADAS(첨단 운전 지원 시스템)에 야간 투시경 카메라를 통합하려고 합니다. 이 기세는 인도와 태평양 지역의 ISR 예산으로 미국과 호주 군사 프로그램이 차세대 후리어 센서를 다년간 주문하는 등 더욱 강해지고 있습니다.

세계 열화상 시스템 시장 동향과 통찰

비냉각 마이크로 볼로미터 가격 하락

비냉각 검출기의 코스트 커브는 계속 떨어지고, 방위나 중공업 이외에도 대응 가능한 기회가 퍼지고 있습니다. LightPath와 같은 기업에 의한 규모의 경제, 제조 간소화, 대체 칼코게나이드 광학계가 역사적인 게르마늄 병목 현상을 완화하고 있습니다. 스마트폰 OEM은 열 애드온을 시험적으로 도입하고 있으며, 차량 운행 회사는 기업의 ESG 프로그램 하에서 서모그래피 검사를 지정하고 있습니다. 이러한 상업적 확산은 원시 이미지를 실용적인 통찰력으로 변환하는 분석 소프트웨어의 가격 결정력을 높이고 있습니다.

인도 태평양 지역에서 방어 ISR 예산 증가

지역 안보 경쟁은 장거리 정찰기 조달을 자극합니다. 미국의 태평양 억제 구상에서는 첨단 센서에 99억 달러가 할당되고, 호주 국방 로드맵에서는 500억 호주 달러(347억 달러)의 자금이 다중 스펙트럼 이미지 플랫폼에 할당됩니다. 듀얼 밴드 FLIR 어레이를 지원하는 SBIR 보조금과 함께, 이 파이프라인은 검출기 파운드리 및 광학 부품 공급업체에 수년간 수량을 확보할 수 있습니다.

수출관리제도(ITAR 및 EAR)

미국의 수출 규제는 진화하고 있으며 많은 듀얼 유스 포컬 플레인 어레이 및 광학 키트에 라이선스가 의무화되어 판매주기가 장기화되고 국제 수익이 제한되고 있습니다. 최근의 제안에서는 지금까지 규제 대상외였던 상업용 이미저가 라이선스의 범주에 들어가게 되고, OEM은 미국 이외 공급망의 현지화를 가속화하게 됩니다. 정책 불확실성은 특히 소량 생산의 틈새 혁신자에게 부담을 주는 컴플라이언스 비용을 초래합니다.

부문 분석

보안 및 모니터링은 2024년 매출의 38.2%를 차지했으며 열화상 시스템 시장에서 경계 보호의 기본 역할이 강화되었습니다. 국경 관리 지출 증가와 중요 인프라 강화가 고정 카메라와 펀틸트 줌 카메라의 조달을 지원하는 반면, AI 주도 분석은 운영자의 작업 부담을 줄여줍니다. CAGR 7.8%로 가장 급성장하는 자동차 ADAS는 보행자 안전과 자동 긴급 브레이크에 관한 규제의 뒷받침을 활용하고 있습니다. 한때 적외선을 옵션으로 지정했던 OEM의 설계 사이클은 현재는 더 많은 양의 트림에 소형 모듈을 통합하게 되어 연간 출하 기준선이 확대되고 있습니다.

서모그래피 서비스는 공장이 NFPA-70B에 준거하고 수요의 다양화가 현저해지면서 연금 형식의 검사 수입이 창출되었습니다. 소방기관은 최전선에서 활동하는 대원에게 서모그래피 단안경을 장비시켜 위성에 의한 핫스팟 경보를 활용하여 신속한 배치를 도모하고 있습니다. 스마트폰과 클립온 마이크로 볼로미터를 결합한 모바일 앱의 출현은 열화상 시스템 시장의 소비자화 단계의 도래를 알리는 것입니다.

핸드헬드형 이미저는 2024년 매출의 46.4%를 차지했으며, 예방보수, 법집행, 긴급 대응 등의 장면에서 범용성이 지지되고 있습니다. 배터리 구동 장치의 편의성은 특히 검출기의 해상도가 향상됨에 따라 큰 교체 수요를 지원합니다. 그러나 통합 OEM 모듈은 CAGR 7.2% 이상으로 자동차, 드론, 스마트 가전 내부에서 열화상 시스템 시장 규모 확대를 지원합니다. 고정 마운트 솔루션은 24시간 365일 모니터링이 필수적인 주변 보안 및 프로세스 모니터링에 필수적인 것은 아닙니다.

군사 조달은 크기, 무게, 전력 소비 및 비용(SWaP-C)을 중시하며, 페이로드 실적을 압축하기 위해 독자적인 셔터리스 교정과 에지 AI를 추진하고 있습니다. 개발 중인 플렉서블 적외선 센서는 미래의 웨어러블화를 약속하지만, 실용화는 아직 몇 차례 미래의 이야기입니다.

지역 분석

북미는 2024년 지출액의 41.5%를 차지했으며, 미국 육군의 3세대 FLIR 센서에 1억 1,750만 달러의 발주 등 방위 관련 할당을 반영하고 있습니다. NFPA-70B 준수는 산업 분야에서의 채용을 더욱 뒷받침하고 있으며, 자동차 업계에서는 Tier-1이 2027년 모델을 향해 나이트 비전 프로그램을 시험적으로 도입하고 있습니다. CISA의 사이버 보안 지침은 하드화된 펌웨어에 대한 프리미엄 수요를 촉진하고 미국 공급업체는 가격 규율을 유지할 수 있습니다.

일본, 한국, 인도, 호주가 ISR 함대를 다양화하고 차량 수출을 확대함에 따라 아시아태평양의 CAGR은 8.3%로 가장 높을 것으로 예측됩니다. 2019년부터 2020년까지 중국의 서모그래피 점유율은 15%에서 63%로 상승했습니다. 국산 센서의 생태계는 성숙해지고 있지만, 수출 규제가 미국의 최첨단 기술에 대한 접근을 제한하고 있으며, 지역의 R&D 투자에 박차를 가하고 있습니다.

유럽은 국방 옵트로닉스 수주 및 자동차 안전 규정에 힘입어 견고한 성장을 보여줍니다. HENSOLDT의 옵트로닉스 부문의 수익이 34% 급증하여 조달의 견조함을 강조했습니다. 중동 및 아프리카에서는 사우디아라비아를 위해 멀티 센서 포드를 출하하는 등 주변 감시 수요가 견조하게 추이하고 있습니다. 남미는 여전히 신흥 시장이지만 산업 보수와 공공 안전 예산이 증가하는 경향이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비냉각 마이크로 볼로미터의 가격 하락

- 인도 태평양 지역의 방어 ISR 예산 증가

- 전기 안전을 위한 NFPA-70B 서모그래피 의무화

- 비용 효율적인 ADAS 나이트 비전을 요구하는 자동차 OEM의 움직임

- 스마트 공장에서 AI를 활용한 예지보전

- 기후에 좌우되는 산불 모니터링 수요

- 시장 성장 억제요인

- 수출규제(ITAR 및 EAR)

- 냉각형 MWIR 카메라의 높은 설비 투자액

- 게르마늄 광학 공급망 초크 포인트

- 네트워크 카메라의 사이버 보안 위험

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

- 가격 분석(용도별 및 기술별)

제5장 시장 규모와 성장 예측

- 용도별

- 보안 및 모니터링

- 군 및 방위

- 서모그래피 및 검사

- 소방

- 퍼스널 비전 시스템

- 스마트폰 및 태블릿

- 자동차용 ADAS

- 해상 및 항공우주

- 폼 팩터별

- 핸드 헬드 이미징 장치

- 고정식(회전식 및 비회전식)

- 통합 OEM 모듈

- 기술별

- 비냉각 LWIR

- 냉각 MWIR

- SWIR 및 멀티스펙트럼

- 컴포넌트별

- 검출기 및 코어

- 카메라

- 광학 부품 및 렌즈 세트

- 소프트웨어 및 애널리틱스

- 최종 사용자 업계별

- 방위 및 국토 안보

- 산업용

- 상업용

- 의료용

- 공공안전

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주 및 NZ

- ASEAN(분할)

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Teledyne FLIR

- Opgal Optronic Industries

- Fluke Corporation

- Seek Thermal

- Axis Communications

- Leonardo DRS

- Raytheon Technologies

- L3Harris Technologies

- Lockheed Martin

- Testo SE and Co. KGaA

- Bullard

- Hikmicro(Hikvision)

- Guide Sensmart

- Excelitas(Xenics)

- BAE Systems

- HT Italia

- Trijicon

- Zhejiang Dali

- Pelco

- Yantai IRay

제7장 시장 기회와 장래의 전망

JHS 25.11.13The thermal imaging systems market size is valued at USD 5.78 billion in 2025 and is forecast to reach USD 8.17 billion by 2030, expanding at a 7.16% CAGR.

Accelerating defense modernization, expanding industrial automation, and mandated automotive safety features are converging to keep demand elevated. Standardization around NFPA-70B thermography is stimulating steady procurement cycles in manufacturing and utilities, while uncooled long-wave infrared (LWIR) price declines are widening accessibility. In parallel, vehicle makers are integrating night-vision cameras into Advanced Driver-Assistance Systems (ADAS) to comply with pending pedestrian-protection rules. The momentum is reinforced by Indo-Pacific ISR budgets, with military programs in the United States and Australia placing multi-year orders for next-generation FLIR sensors.

Global Thermal Imaging Systems Market Trends and Insights

Falling Price of Uncooled Micro-Bolometers

Cost curves for uncooled detectors continue to decline, enlarging addressable opportunities beyond defense and heavy industry. Scale economies, simplified fabrication, and alternative chalcogenide optics from firms such as LightPath are mitigating historic germanium bottlenecks. Smartphone OEMs are piloting thermal add-ons, and fleet operators are specifying thermographic inspections under corporate ESG programs. The broader commercial reach strengthens pricing power for analytics software that converts raw images into actionable insights.

Growing Defense ISR Budgets in Indo-Pacific

Regional security competition is stimulating long-range surveillance procurements. The United States' Pacific Deterrence Initiative allocates USD 9.9 billion for advanced sensors, while Australia's AUD 50 billion (USD 34.7 billion) defense roadmap earmarks funds for multispectral imaging platforms. Combined with SBIR grants supporting dual-band FLIR arrays, the pipeline sustains multi-year volume visibility for detector foundries and optics suppliers.

Export-Control Regimes (ITAR & EAR)

Evolving US export rules mandate licenses for many dual-use focal-plane arrays and optics kits, elongating sales cycles and limiting addressable international revenue. Recent proposals would pull previously uncontrolled commercial imagers into license categories, prompting OEMs to accelerate non-US supply-chain localization. The policy uncertainty introduces compliance costs that particularly burden small-volume niche innovators.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory NFPA-70B Thermography for Electrical Safety

- Vehicle OEM Push for Cost-Effective ADAS Night-Vision

- High Cap-Ex for Cooled MWIR Cameras

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security and surveillance held 38.2% of 2024 revenue, reinforcing the foundational role of perimeter protection in the thermal imaging systems market. Increasing border-control spending and critical infrastructure hardening sustain procurement of fixed and pan-tilt-zoom cameras, while AI-driven analytics cut operator workload. Automotive ADAS, the fastest-growing application at a 7.8% CAGR, capitalizes on regulatory nudges for pedestrian safety and automated emergency braking. OEM design cycles that once specified infrared as optional are now embedding compact modules into higher-volume trims, broadening annual shipment baselines.

Demand diversification is evident in thermography services as factories comply with NFPA-70B, creating annuity-style inspection revenue. Firefighting agencies are equipping frontline responders with thermal monoculars, leveraging satellite-driven hotspot alerts for rapid deployment. Emerging mobile apps pairing smartphones with clip-on micro-bolometers signal the consumerization phase of the thermal imaging systems market.

Hand-held imagers captured 46.4% of 2024 revenue, favored for versatility across preventive maintenance, law enforcement, and first-responder scenarios. The convenience of battery-operated units sustains significant replacement demand, especially as detector resolution improves. Integrated OEM modules, however, are set to outpace at a 7.2% CAGR, underpinning the expansion of the thermal imaging systems market size inside vehicles, drones, and smart appliances. Fixed-mount solutions remain indispensable in perimeter security and process monitoring where 24/7 coverage is mandatory.

Military procurement emphasizes Size, Weight, Power, and Cost (SWaP-C) gains, driving proprietary shutterless calibration and edge AI to compress payload footprints. Flexible infrared sensors in development promise future wearables, although commercialization is still several design iterations away.

The Thermal Imaging Systems Market Report is Segmented by Application (Security and Surveillance, Military and Defense, and More), Form Factor (Hand-Held Imaging Devices, Fixed-Mount, and More), Technology (Uncooled LWIR, Cooled MWIR, and More), Component (Detectors/Cores, and More), End-User Industry (Defense and Homeland Security, Industrial, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 41.5% of 2024 spending, reflecting defense allocations such as the US Army's USD 117.5 million order for third-generation FLIR sensors. NFPA-70B compliance further bolsters industrial uptake, and automotive Tier-1s are piloting night-vision programs for 2027 model years. Cybersecurity directives from CISA drive premium demand for hardened firmware, enabling US-based vendors to maintain pricing discipline.

Asia-Pacific is projected to log the highest 8.3% CAGR as Japan, South Korea, India, and Australia diversify ISR fleets and expand vehicle exports. China's share shift from 15% to 63% in thermography during 2019-2020 illustrates the manufacturing scale at play. Indigenous sensor ecosystems are maturing, yet export controls restrict access to state-of-the-art US technology, fueling regional R&D investment.

Europe posts steady growth, buoyed by defense optronics orders and automotive safety regulations. HENSOLDT's 34% revenue surge in its Optronics segment underscores resilient procurement. Middle East and Africa register firm demand for perimeter surveillance, with Teledyne FLIR shipping multi-sensor pods to Saudi Arabia. South America remains emergent, but industrial maintenance and public-safety budgets point to incremental upside.

- Teledyne FLIR

- Opgal Optronic Industries

- Fluke Corporation

- Seek Thermal

- Axis Communications

- Leonardo DRS

- Raytheon Technologies

- L3Harris Technologies

- Lockheed Martin

- Testo SE and Co. KGaA

- Bullard

- Hikmicro (Hikvision)

- Guide Sensmart

- Excelitas (Xenics)

- BAE Systems

- HT Italia

- Trijicon

- Zhejiang Dali

- Pelco

- Yantai IRay

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Falling price of uncooled micro-bolometers

- 4.2.2 Growing defense ISR budgets in Indo-Pacific

- 4.2.3 Mandatory NFPA-70B thermography for electrical safety

- 4.2.4 Vehicle OEM push for cost-effective ADAS night-vision

- 4.2.5 AI-enabled predictive maintenance in smart factories

- 4.2.6 Climate-driven wildfire monitoring demand

- 4.3 Market Restraints

- 4.3.1 Export-control regimes (ITAR and EAR)

- 4.3.2 High cap-ex for cooled MWIR cameras

- 4.3.3 Supply-chain choke points in germanium optics

- 4.3.4 Cyber-security risks in networked cameras

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Pricing Analysis (by Application and Technology)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Security and Surveillance

- 5.1.2 Military and Defense

- 5.1.3 Thermography / Inspection

- 5.1.4 Firefighting

- 5.1.5 Personal Vision Systems

- 5.1.6 Smartphones and Tablets

- 5.1.7 Automotive ADAS

- 5.1.8 Maritime and Aerospace

- 5.2 By Form Factor

- 5.2.1 Hand-held Imaging Devices

- 5.2.2 Fixed-mount (Rotary / Non-rotary)

- 5.2.3 Integrated OEM Modules

- 5.3 By Technology

- 5.3.1 Uncooled LWIR

- 5.3.2 Cooled MWIR

- 5.3.3 SWIR and Multispectral

- 5.4 By Component

- 5.4.1 Detectors / Cores

- 5.4.2 Complete Cameras

- 5.4.3 Optics and Lens Sets

- 5.4.4 Software and Analytics

- 5.5 By End-user Industry

- 5.5.1 Defense and Homeland Security

- 5.5.2 Industrial

- 5.5.3 Commercial

- 5.5.4 Medical

- 5.5.5 Public Safety

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia and NZ

- 5.6.4.6 ASEAN (Break-up)

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Teledyne FLIR

- 6.4.2 Opgal Optronic Industries

- 6.4.3 Fluke Corporation

- 6.4.4 Seek Thermal

- 6.4.5 Axis Communications

- 6.4.6 Leonardo DRS

- 6.4.7 Raytheon Technologies

- 6.4.8 L3Harris Technologies

- 6.4.9 Lockheed Martin

- 6.4.10 Testo SE and Co. KGaA

- 6.4.11 Bullard

- 6.4.12 Hikmicro (Hikvision)

- 6.4.13 Guide Sensmart

- 6.4.14 Excelitas (Xenics)

- 6.4.15 BAE Systems

- 6.4.16 HT Italia

- 6.4.17 Trijicon

- 6.4.18 Zhejiang Dali

- 6.4.19 Pelco

- 6.4.20 Yantai IRay

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment