|

시장보고서

상품코드

1851543

LED 패키징 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

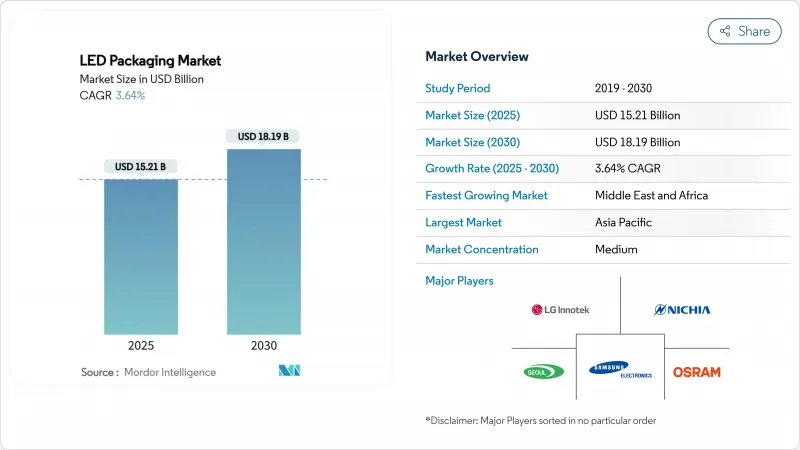

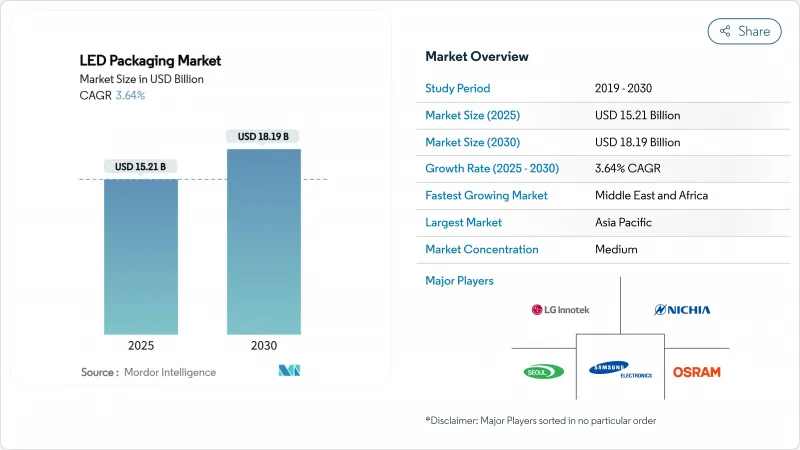

LED 패키징 시장 규모는 2025년에 152억 1,000만 달러, 2030년에는 181억 9,000만 달러에 이를 것으로 예측되며, CAGR은 3.64%를 나타낼 전망입니다.

가치 증가는 상품화된 램프가 아니라 자동차용 적응형 헤드램프, UV-C 살균 모듈, 미니 LED 디스플레이 백라이트 등의 프리미엄 틈새에서 비롯됩니다. 자동차 제조업체나 패널 제조업체가 보다 엄격한 열공차와 박형화를 요구하는 가운데, 칩 스케일 패키지(CSP)나 선진 세라믹 기판을 비롯한 성능 중시의 패키지 아키텍처가 점유율을 늘리고 있습니다. 정책 주도의 형광등 금지와 화합물 반도체의 생산 능력에 대한 정부 자금 원조가 LED 패키징 시장에 더욱 탄력을 주는 한편, 지정학적 공급망의 현지화가 투자 결정을 형성합니다. 동시에 지적재산권 분쟁과 기판 비용의 변동은 진입 장벽을 높이고 자본 요건을 증대시킴으로써 성장 궤도를 약화시키고 있습니다.

세계의 LED 패키징 시장 동향과 인사이트

TV 및 IT 패널에서 미니/마이크로 LED 백라이트로 전환

각 브랜드가 100-200μm 칩을 활용해, 2,000을 넘는 로컬 조광 존과 2,000니트를 넘는 피크 휘도를 실현하는 것으로, 미니 LED 백라이트의 채용이 프리미엄 TV나 모니터의 카테고리를 재구축하고 있습니다. 패키지 온보드 방식은 재료비의 경쟁력을 유지하면서도 초박형의 산업용 디자인용으로 칩 온 유리가 대두하고 있습니다. 차량용 조종석 디스플레이는 태양광의 읽기 편의성과 라이프사이클의 견고성이 OLED보다 Mini-LED에 유리하기 때문에 어드레싱 가능한 볼륨을 확대하고 있습니다. 고밀도로 장착된 어레이는 높은 열 부하를 유발하므로 두께를 희생하지 않고 효율적으로 방열하는 세라믹 기판 및 CSP 솔루션에 대한 수요가 증가하고 있습니다. 가전 제조업체가 Mini-LED의 로드맵을 공표하는 가운데, 가와카미의 패키징 기업은 수년 단위의 패널 교환 사이클에 대응할 수 있는 용량을 확보해, LED 패키징 시장을 확대하고 있습니다.

유럽과 한국에서 자동차용 헤드램프에 CSP가 급속히 보급

칩 스케일 패키지는 와이어 본드를 제거하고 광학 높이를 크게 줄임으로써 150°C 이상의 접합 온도에 대응하면서 에너지 소비를 20% 절감합니다. ams 오스람의 EVIYOS 2.0과 같은 주요 적응형 빔 시스템은 2만 5,600개의 개별 주소 지정 가능 픽셀을 통합하여 CSP가 얼마나 세밀한 배광 제어를 가능하게 하는지를 보여줍니다. 눈부심과 에너지 효율에 관한 유럽 규정이 전환을 가속화하고 있으며, 한국공급업체는 제약이 있는 실내 앰비언트 조명 모듈에 CSP를 사용합니다. 헤드램프 Tier-1은 10만 시간의 수명을 규정하고 있으며, 패키지 하우스는 세라믹 캐비티와 고열 전도 다이 부착의 인정을 받고 있습니다. 이 기세는 프리미엄 자동차 조명이 안전 크리티컬 조명기구의 참조 아키텍처로 CSP를 채택한다는 LED 패키징 시장의 전략적 변절을 강조합니다.

사파이어 웨이퍼 가격 변동성

사파이어 웨이퍼는 패키지 비용의 최대 20%를 차지하지만 분기별 가격 변동은 30% 이상의 경우가 많으며 계약 패키지 제조업체의 조익을 압박하고 있습니다. 결정 성장은 APAC의 소수공급업체에 집중되어 있기 때문에 지정학적 마찰과 전력 부족은 즉시 스팟 공급 부족으로 이어집니다. 선도적 인 제조업체는 기판을 재사용하기 위해 레이저 리프트 오프를 고려하고 있지만, 설비 투자 부담으로 인해 채용은 일류 제조업체로 제한됩니다. 이 때문에 중소기업은 재활용 헷지 없이 원재료 위험을 견디고 생산량을 확대하는 능력을 약화시키고 LED 패키징 시장 전체의 탄력성을 억제하고 있습니다.

부문 분석

CSP의 출하량은 자동차의 헤드라이트나 초박형 디스플레이의 백라이트에 채용되고 있는 것을 반영해, CAGR 5.4%를 나타낼 전망입니다. 금액 기준으로 CSP는 LED 패키징 시장 규모에서 차지하는 비율이 증가하고 있습니다. SMD는 2024년 출하량의 43%를 차지했는데, 이는 단가가 소형화의 이점을 웃도는 개조 조명 수요를 유지하기 때문입니다. 플립칩형은 3W 이상의 틈새 시장을 타겟으로 하고 있으며 로열티는 높지만 적응형 빔 규제에 따른 컴팩트한 광학계가 가능하기 때문에 LED 패키징 시장에서 차별화된 점유율을 유지하고 있습니다. 하이브리드 및 패키지 프리 구조는 픽 앤 플레이스의 사이클 타임과 재작업의 과제에 제약을 받으며 실험적인 단계에 머물고 있습니다.

웨이퍼 레벨 밀봉에 대한 끊임없는 혁신은 칩 제조와 패키지 조립의 경계를 모호하게 만듭니다. 대만의 반도체 조립 테스트(OSAT) 아웃소싱 제공업체는 텔레비전 및 스마트폰 백라이트 제조업체의 급한 주문에 대응하기 위해 팬아웃 CSP 라인을 확장하고 있습니다. 반대로 유럽 자동차 제조업체 Tier-1은 엄격한 AEC-Q102 신뢰성 테스트를 의무화하여 듀얼 소싱을 보장하고 신흥 공급업체를 효과적으로 마무리하고 있습니다. 이 이분화는 LED 패키징 시장에서 비용 최적화 레인과 성능 최적화 레인이 어떻게 공존하고 있는지를 두드러지게 합니다.

리드프레임 아키텍처는 2024년에도 출하의 34%를 차지했지만, 설계자가 150W/mK를 넘는 열전도율을 추구하는 가운데, 질화알루미늄 기반의 세라믹 캐비티는 4.3%로 성장했습니다. 자동차, UV-C, 원예용 조명기구는 유기 기판이 조기에 열화되는 접합부 온도를 밀어 올리기 때문에 세라믹이 필수품이 됩니다. 따라서 세라믹 기판의 LED 패키징 시장 규모는 출하 톤수가 아니라 전력 밀도에 비례하여 확대됩니다.

밀봉재의 화학적 진화는 보조를 맞추어 진행됩니다. 아웃 가스 특성을 향상시킨 UV 내성 실리콘 겔은 멸균 사이클 동안 변색을 방지하고 은동 합금 본딩 와이어는 금 비용 노출을 상쇄합니다. 원격 형광체와 유리 형광체 솔루션은 컬러 변화의 안정성을 약속하지만, 중견 기업은 자본 집약에 의한 CAGR-0.5%의 영향을 경계하여 투자를 앞두고 있습니다. 따라서 재료 선택은 전략적 헤지가 되었습니다. 열 마진을 요구하는 세라믹, 비용을 요구하는 유기물, 스펙트럼의 균일성을 요구하는 유리 내장 형광체, 이들 모두가 LED 패키징 시장 내에서 배분을 다투고 있습니다.

지역 분석

아시아태평양은 LED 패키징 시장의 68%를 차지하고 있으며, 그 우위성은 수직 통합된 일렉트로닉스공급망과 국내 소비에 뿌리를 두고 있습니다. 중국 인프라 정비와 에너지 효율화 지령이 판매량을 견인하는 한편, ASE 등 대만의 OSAT 대기업은 AI 하드웨어 수주를 배경으로 2025년 2분기에 11%의 전분기 대비 증수를 기록했습니다. 일본은 자동차 등급의 신뢰성 노하우를 활용하고 한국의 패널 제조업체는 CSP 헤드 램프 모듈을 추진하고 있습니다. 또한 높은 CRI 세라믹 패키지를 필요로 하는 데이터센터 건설도 이 지역의 성장으로 이어집니다.

북미의 성장 궤도는 유기적인 리노베이션 사이클보다는 오히려 규제에 의한 촉매에 달려 있습니다. 형광등의 사용 금지와 DOE의 효율 규칙은 2030년까지 LED의 대체 시장을 확보하고, 거시적인 변동에 관계없이 기준선 출하를 확보합니다. 월프 스피드 실리콘 카바이드 라인에 대한 7억 5,000만 달러를 포함한 미국 CHIPS 법의 우대 조치는 화합물 반도체 공급망에 대한 정책 지원을 보여줍니다.

유럽 시장은 프리미엄 자동차 수요와 까다로운 환경 설계 규범을 기울입니다. 독일의 OEM은 CSP 및 플립칩 패키지를 선호하는 적응형 헤드램프의 전개를 개척하고, 보다 엄격한 눈부심 규제는 픽셀 레벨 제어를 필요로 합니다. 동시에, 지속가능성의 틀은 서비스 수명의 루멘 유지를 선호하기 때문에 세라믹 기판에 대한 선호를 강화하고 있습니다. 중동 및 아프리카는 현재 규모는 작지만 걸프 협력 회의 인프라 프로젝트가 이산화탄소 감축 로드맵 아래 스마트하고 에너지 효율적인 조명을 통합하기 때문에 CAGR 5.2%를 나타낼 것으로 예측됩니다. 남미는 점유율로 후진을 숭배하고 있지만, 교통회랑의 업그레이드나 전기요금의 상승에 의해 LED의 개수가 재정적으로 설득력을 가지게 되어, 상승 여지가 있습니다. 이러한 지역 벡터는 규제 의도와 인프라 투자가 LED 패키징 시장 전체 수요를 어떻게 재조정하는지를 명확하게 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- TV와 IT 패널에서 미니/마이크로 LED 백라이트로의 전환

- 유럽과 한국에서 자동차용 헤드램프에 CSP가 급속히 채용

- 북미의 정책 주도의 형광등 단계적 폐지

- 데이터센터 붐이 아시아의 높은 CRI 조명을 견인

- 포인트 오브 유스 소독용 UV-C LED 수요의 급증

- 대만과 중국에서 아웃소싱 LED 패키징(OSAT) 성장

- 시장 성장 억제요인

- 사파이어 웨이퍼 가격의 변동성

- 플립 칩 설계에서 IP 크로스 라이선스 장벽

- 자본 집약적인 형광체 유리로의 이행

- 3W 패키지 이상의 전력 밀도 열 관리 한계

- 생태계 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 패키징 유형별

- 표면 실장 소자(SMD)

- 칩 온 보드(COB)

- 칩 스케일 패키지(CSP)

- 플립 칩

- 하이브리드/패키지 프리 설계

- 패키지 소재별

- 리드 프레임 및 기판

- 세라믹 기판

- 본딩 와이어/다이어 부착

- 캡슐 수지 및 실리콘 렌즈

- 형광체 및 원격 형광체 필름

- 전력 범위별

- 저·중전력(1W 미만)

- 고전력(1-3W)

- 초고전력(3W 이상)

- 용도별

- 일반 조명

- 주택용

- 상업 및 산업용

- 자동차 조명

- 외부(헤드 램프, 주간주행등)

- 내부

- 백라이트

- TV 및 모니터

- 모바일 및 태블릿

- 플래시 및 사이니지

- 모바일 카메라 플래시

- 디지털 사이니지 및 빌보드

- 특수 및 UV/IR

- 원예

- UV-C 살균

- 일반 조명

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Everlight Electronics Co., Ltd.

- Cree LED(Smart Global Holdings)

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- TT Electronics plc

- Bridgelux, Inc.

- Epistar Corp.(Ennostar)

- Lite-On Technology Corp.

- Lextar Electronics Corp.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn Bhd

- NationStar Optoelectronics Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

제7장 시장 기회와 향후 전망

KTH 25.11.13The LED packaging market size stands at USD 15.21 billion in 2025 and is forecast to touch USD 18.19 billion by 2030, registering a 3.64% CAGR.

Incremental value is coming less from commoditized lamps and more from premium niches such as adaptive automotive headlamps, UV-C disinfection modules and Mini-LED display backlights. Performance-oriented package architectures, notably chip-scale package (CSP) and advanced ceramic substrates, are gaining share as carmakers and panel makers demand tighter thermal tolerances and thinner form factors. Policy-driven fluorescent lamp bans and government funding for compound-semiconductor capacity add further impetus to the LED packaging market, while geopolitical supply-chain localization shapes investment decisions. Simultaneously, intellectual-property disputes and substrate cost volatility temper the growth trajectory by raising barriers to entry and amplifying capital requirements.

Global LED Packaging Market Trends and Insights

Transition to Mini/Micro-LED Backlighting in TVs and IT Panels

Mini-LED backlight adoption is reshaping premium TV and monitor categories as brands leverage 100-200 µm chips to unlock >2,000 local-dimming zones and >2,000-nit peak brightness. Package-on-Board formats keep the bill-of-materials competitive, yet Chip-on-Glass is emerging for ultra-slim industrial designs. Automotive cockpit displays extend the addressable volume because sunlight readability and life-cycle robustness favor Mini-LED over OLED. Densely packed arrays trigger higher thermal loads, directing demand toward ceramic-substrate and CSP solutions that dissipate heat efficiently without sacrificing thickness. As consumer-electronics makers publicize Mini-LED roadmaps, upstream packaging houses position capacity to catch a multi-year panel-replacement cycle, thereby widening the LED packaging market.

Rapid CSP Adoption in Automotive Headlamps across Europe and Korea

Chip-scale packages eliminate wire bonds and significantly shrink optical height, reducing energy draw by 20% while handling junction temperatures beyond 150 °C. Flagship adaptive-beam systems such as ams OSRAM's EVIYOS 2.0 integrate 25,600 individually addressable pixels, demonstrating how CSP enables finer light distribution control. European regulations on glare and energy efficiency accelerate the switch, and Korean suppliers use CSP for constrained interior ambient lighting modules. Headlamp Tier-1s stipulate 100,000-hour lifetimes, compelling package houses to qualify ceramic cavity and high-thermal-conductivity die attach. The momentum underscores a strategic inflection where premium automotive lighting steers the LED packaging market toward CSP as the reference architecture for safety-critical luminaires.

Volatility of Sapphire Wafer Pricing

Sapphire wafers contribute up to 20% of package cost, yet quarterly price swings often top 30%, squeezing gross margins for contract packagers. Because crystal growth is clustered in a handful of APAC vendors, geopolitical friction or power rationing quickly feeds into spot shortages. Large manufacturers explore Laser Lift-Off to reclaim substrates for reuse, but the capex burden confines adoption to top-tier producers. Smaller firms thus endure raw-material risk without the hedge of recycling, dampening their ability to scale output and constraining the LED packaging market's overall elasticity.

Other drivers and restraints analyzed in the detailed report include:

- Policy-Led Phase-Out of Fluorescent Lamps in North America

- Data-Centre Boom Driving High-CRI Lighting in Asia

- IP Cross-Licensing Barriers for Flip-Chip Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CSP shipments climb at a 5.4% CAGR, reflecting their rising acceptance in automotive headlights and ultra-thin display backlights. In value terms, CSP contributes a growing slice of the LED packaging market size as lamp makers pay premiums for thermal headroom and pixel-level control. SMD formats still anchor 43% of shipments in 2024, sustaining refurb-lighting demand where unit cost outweighs miniaturization benefits. Flip-chip variants target >3 W niches, and while their royalty load is high, they enable compact optics aligned with adaptive-beam regulations, thereby sustaining a differentiated share of the LED packaging market. Hybrid and package-free constructs stay experimental, constrained by pick-and-place cycle-times and rework challenges.

Continuous innovation around wafer-level encapsulation blurs the boundary between chip fabrication and package assembly. Outsourced semiconductor assembly and test (OSAT) providers in Taiwan scale fan-out CSP lines to satisfy surge orders from TV and smartphone backlight makers. Conversely, European automotive Tier-1s secure dual sourcing by mandating stringent AEC-Q102 reliability tests, effectively locking out nascent vendors. The bifurcation accentuates how cost-optimized versus performance-optimized lanes coexist in the LED packaging market.

Lead-frame architectures still represented 34% of shipments in 2024, yet ceramic cavities based on aluminum nitride grow at 4.3% as designers chase thermal conductivity >150 W/mK. Automotive, UV-C and horticulture luminaires push junction temperatures where organic boards degrade prematurely, making ceramics a necessity. The LED packaging market size for ceramic substrates thus scales alongside power densities instead of shipment tonnage.

Encapsulation chemistries evolve in lockstep. UV-resistant silicone gels with improved outgassing properties prevent discoloration during sterilization cycles, while silver-copper alloy bonding wires offset gold cost exposure. Although remote-phosphor and phosphor-in-glass solutions promise color-shift stability, mid-tier players defer the investment, wary of -0.5% CAGR drag from capital intensity. Hence, material choice has become a strategic hedge: ceramics for thermal margin, organics for cost, and glass-embedded phosphors for spectral uniformity-all vying for allocation within the LED packaging market.

The LED Packaging Market Report is Segmented by Packaging Type (Surface-Mount Device, Chip-On-Board, Chip-Scale Package, and More), Package Material (Lead-Frame and Substrate, Ceramic Substrate, and More), Power Range (Low and Mid-Power (Less Than 1 W), High-Power (1-3 W), and More), Application (General Lighting, Automotive Lighting, Backlighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 68% of the LED packaging market, a dominance rooted in its vertically integrated electronics supply chain and domestic consumption. China's infrastructure rollouts and energy-efficiency mandates drive volume, while Taiwan's OSAT giants such as ASE posted 11% sequential revenue growth in Q2 2025 on the back of AI-hardware orders. Japan leans on auto-grade reliability know-how, and South Korea's panel makers advance CSP headlamp modules. Regional growth also leverages data-centre build-outs that require high-CRI ceramic packages.

North America's trajectory hinges on regulatory catalysts rather than organic renovation cycles. The fluorescent lamp ban and DOE efficacy rules create a captive LED replacement window to 2030, ensuring baseline shipments regardless of macro swings. US CHIPS Act incentives, including USD 750 million for Wolfspeed's silicon-carbide line, illustrate policy support for compound-semiconductor supply chains.

Europe's market tilts toward premium automotive demand and strict eco-design codes. German OEMs pioneer adaptive headlamp rollouts that favor CSP and flip-chip packages, while stricter glare regulations necessitate pixel-level control. Simultaneously, sustainability frameworks prioritize lifetime lumen maintenance, reinforcing the preference for ceramic substrates. Middle East & Africa, though smaller today, is forecast to expand at a 5.2% CAGR as Gulf Cooperation Council infrastructure projects integrate smart, energy-efficient lighting under carbon-reduction roadmaps. South America trails in share but holds upside from transportation-corridor upgrades and rising electricity tariffs that make LED retrofits financially compelling. Together, these regional vectors underscore how regulatory intent and infrastructure investment recalibrate demand across the LED packaging market.

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Everlight Electronics Co., Ltd.

- Cree LED (Smart Global Holdings)

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- TT Electronics plc

- Bridgelux, Inc.

- Epistar Corp. (Ennostar)

- Lite-On Technology Corp.

- Lextar Electronics Corp.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn Bhd

- NationStar Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transition to Mini/Micro-LED Backlighting in TVs and IT Panels

- 4.2.2 Rapid CSP Adoption in Automotive Headlamps across Europe and Korea

- 4.2.3 Policy-Led Phase-Out of Fluorescent Lamps in North America

- 4.2.4 Data-Centre Boom Driving High-CRI Lighting in Asia

- 4.2.5 Surge in UV-C LED Demand for Point-of-Use Disinfection

- 4.2.6 Outsourced LED Packaging (OSAT) Growth in Taiwan and China

- 4.3 Market Restraints

- 4.3.1 Volatility of Sapphire Wafer Pricing

- 4.3.2 IP Cross-Licensing Barriers for Flip-Chip Designs

- 4.3.3 Capital-Intensive Transition to Phosphor-in-Glass

- 4.3.4 Power Density Heat-Management Limitations Above 3 W Packages

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Packaging Type

- 5.1.1 Surface-Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip-Scale Package (CSP)

- 5.1.4 Flip-Chip

- 5.1.5 Hybrid/Package-Free Designs

- 5.2 By Package Material

- 5.2.1 Lead-Frame and Substrate

- 5.2.2 Ceramic Substrate

- 5.2.3 Bonding Wire/Die-Attach

- 5.2.4 Encapsulation Resin and Silicone Lens

- 5.2.5 Phosphor and Remote Phosphor Films

- 5.3 By Power Range

- 5.3.1 Low and Mid-Power (Less than 1 W)

- 5.3.2 High-Power (1-3 W)

- 5.3.3 Ultra-High-Power (Above 3 W)

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.1.1 Residential

- 5.4.1.2 Commercial and Industrial

- 5.4.2 Automotive Lighting

- 5.4.2.1 Exterior (Headlamp, DRL)

- 5.4.2.2 Interior

- 5.4.3 Backlighting

- 5.4.3.1 TV and Monitor

- 5.4.3.2 Mobile and Tablet

- 5.4.4 Flash and Signage

- 5.4.4.1 Mobile Camera Flash

- 5.4.4.2 Digital Signage and Billboards

- 5.4.5 Specialty and UV/IR

- 5.4.5.1 Horticulture

- 5.4.5.2 UV-C Disinfection

- 5.4.1 General Lighting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Nichia Corporation

- 6.4.3 OSRAM Opto Semiconductors GmbH

- 6.4.4 LG Innotek Co., Ltd.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 Cree LED (Smart Global Holdings)

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Citizen Electronics Co., Ltd.

- 6.4.12 TT Electronics plc

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Epistar Corp. (Ennostar)

- 6.4.15 Lite-On Technology Corp.

- 6.4.16 Lextar Electronics Corp.

- 6.4.17 Edison Opto Corp.

- 6.4.18 Dominant Opto Technologies Sdn Bhd

- 6.4.19 NationStar Optoelectronics Co., Ltd.

- 6.4.20 MLS Co., Ltd. (Forest Lighting)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment