|

시장보고서

상품코드

1907351

안내 렌즈: 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026년-2031년)Intraocular Lens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

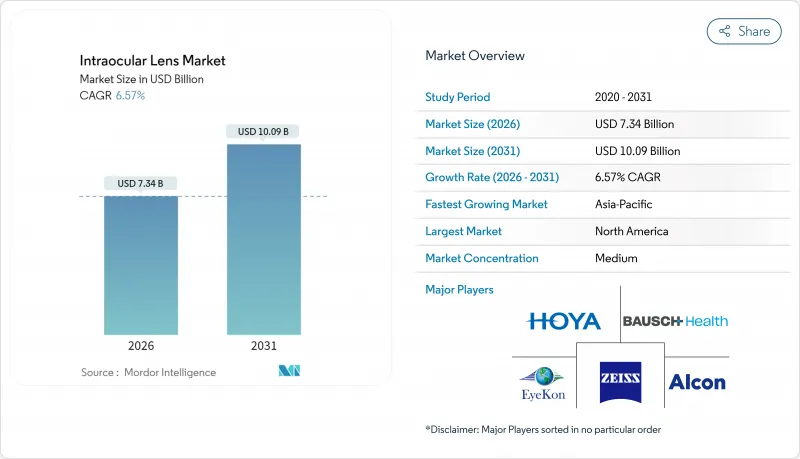

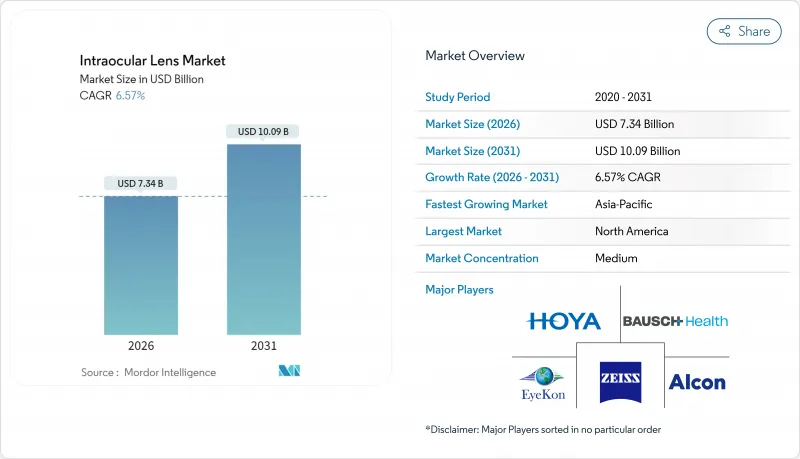

2026년 안내 렌즈 시장 규모는 73억 4,000만 달러로 추정되며, 2025년 68억 9,000만 달러에서 성장한 수치입니다. 2031년에는 100억 9,000만 달러에 이르고 2026년부터 2031년까지 CAGR 6.57%로 성장할 전망됩니다.

프리미엄 렌즈의 혁신, 노인 증가, 외래 수술 모델로의 전환이 이러한 확대를 지원합니다. 65세 이상의 인구 증가는 안정된 백내장 사례를 가져오고, 노안 교정이나 광조정 가능한 설계에 의해 안경 불필요라는 높아지는 생활양식에 대한 기대에 부응할 수 있습니다. 실리콘과 차세대 소수성 아크릴 소재는 염증 반응을 완화하고 의사가보다 자신있게 프리미엄 렌즈로 업그레이드를 제안하는 것을 뒷받침하고 있습니다. 아시아태평양의 의료 관광 루트 확대에 의해 첨단 렌즈에의 액세스가 확대되고, 진료소 내 수술실의 정비가 의료 제공업체의 경제성을 향상시켜, 새로운 수술 용량을 창출하고 있습니다. 시각 품질 향상과 시각 이상 저감을 실현하는 제품 사이클이 의사의 선호를 신속하게 쇄신하기 때문에 경쟁의 격렬함은 고수준으로 지속되고 있습니다.

세계 안내 렌즈 시장 동향과 인사이트

고령화에 따른 세계 백내장 수술 건수 증가

백내장의 발생률은 인구의 장수화와 병행하여 증가하고 있습니다. 80세 이상의 사람들의 70%가 수정체 혼탁을 일으킬 수 있으며, 많은 사람들이 디지털 기기의 지속적인 이용과 고령기 취업을 위해 고품질의 시력을 기대하고 있습니다. 외래수술센터에서는 이미 백내장수술이 최대의 증례유형을 차지하고 있으며, 2024년에는 ASC(외래수술센터) 수술건수의 19%를 차지했습니다. 아시아태평양에서는 인구의 고령화가 진료소의 확충을 상회하기 때문에 수용 능력의 압박이 현저합니다. 따라서 의료 제공업체는 Faco Unit과 프리로드 렌즈 시스템을 결합한 높은 처리량 모델을 점차 채택하고 있습니다.

프리미엄/노안 교정용 안내 렌즈의 채택 급증

상환 갭이 있음에도 불구하고 프리미엄 렌즈의 보급률은 2019년의 15.5%에서 2021년에는 18.5%로 상승했습니다. 광조정형 광학계에 의해 수술 후의 굴절력을 미세 조정할 수 있기 때문에 잔존 굴절 이상의 리스크가 저감됩니다. 알콘은 PanOptix 및 Vivity 시리즈를 주력으로 이 분야에서 60% 이상의 점유율을 차지하고 있습니다. Tecnis Eyhance와 같은 개선된 단초점 설계는 회절 링에 의한 광륜 현상의 문제 없이 심도를 확대하고, 광륜과 눈부심을 우려하는 환자의 적응 범위를 넓히고 있습니다.

프리미엄 안내 렌즈의 고액의 자기 부담과 불균일한 상환

CMS가 신기술 IOL코드를 등록하지 않았기 때문에 환자는 2계층 액세스 모델이 만들어지기 때문에 환자는 안당 1,500-3,000달러를 지불하는 경우가 많습니다. 진단용 아벨로메트리 검사나 수술 후 조정 비용도 부담에 가해 가격에 민감한 후보자의 진입을 막고 있습니다. 해외에서의 시술은 비용을 억제할 수 있습니다만, 시설에 의해 품질 보증에 편차가 보입니다.

부문 분석

단초점 렌즈는 2025년 시점에서 안내 렌즈 시장 점유율 62.68%를 차지했고 수량 기준으로 선두를 유지했습니다. 삼초점, 토릭, EDOF, 조절 기능이 있는 설계를 포함한 프리미엄 카테고리는 백내장 치료의 기준선 성장률을 넘는 CAGR 7.16%로 성장을 지속하고 있습니다. 이 수요는 교정 없이 근시 시력을 중시하는 환자와 백내장 치료의 일환으로 굴절 교정 효과를 추진하는 외과의사로부터 발생하고 있습니다. PanOptix와 같은 다초점 렌즈는 초기 이중 초점 모델에 비해 안경 의존도가 높고 후광 현상이 적다는 이점이 있습니다. 토릭 단초점 렌즈는 최대 4D의 각막 난시를 교정했으며 1D 이상의 난시를 가진 눈에서는 표준 옵션이 되었습니다. Tecnis Symfony 등의 EDOF 광학계는 근시 시력을 약간 희생하는 것으로 광학적 부작용을 저감해, 회절 링에 우려를 가지는 환자에게의 적응이 가능합니다. Juvene을 포함한 조절 기능이 있는 프로토타입은 3.5D 이상의 조절 폭을 목표로 하여 생리적인 초점 변화의 재현을 목표로 하고 있습니다. 시장 관계자는 이 기술이 프리미엄 렌즈로의 전환을 가속시키는 획기적인 진전이라고 예측했습니다.

수술센터에서는 노시 교정 렌즈를 펨토초 레이저 보조 낭 절개술과 결합하여 중심 위치 정밀도를 높입니다. 한편, 토포그래피 장치는 수술 전 계획을 정밀하게 하여 토릭 축의 정확한 위치를 가능하게 합니다. 임상의에 따르면, 굴절 교정 수술 후 환자는 광조정 기술이 잔존 오차를 미세 조정할 수 있기 때문에 프리미엄 솔루션을 선호하는 경향이 강하다고 합니다. 프리미엄층의 확대는 시술당 수익을 증대시켜 클리닉의 상환압력 완화에 기여함과 동시에 진보된 진단기술에 대한 투자촉진으로 이어집니다.

소수성 아크릴은 접이식, 낭내 생체 적합성 및 그리센 저항성 배합으로 인공 렌즈 시장 규모의 거의 절반을 지원합니다. 클레어온 등의 표면가공형은 투명성을 높이기 위해 수분함량을 증가시키면서 저석회화 리스크를 유지합니다. 실리콘의 CAGR 7.05%는 부흥을 나타내고 있으며, 고순도 등급은 염증세포 부착을 최소화하기 위해 포도막염안에서 이러한 렌즈가 매력적입니다. 신형 실리콘 광학계는 자외선 차단성 크로모포어를 짜넣어, 이식 후의 펨토초 레이저에 의한 파워 조정이 가능합니다. 친수성 아크릴은 현재 28.90%의 점유율을 차지하며, 가교 폴리머와 항석회화 코팅에 의해 당뇨병성 유리체 환경하에서도 투명성을 유지하는 특성으로 재평가되고 있습니다. PMMA의 사용은 강성 안정성이 이점이 되는 외상 사례를 제외하고 감소 경향이 있습니다.

재료 조사는 에지 디자인에 의한 미세 텍스처링에 의한 후낭 혼탁의 감소와 낭포 섬유화에 의한 광학부의 고정 후에 사라지는 생체 흡수성 햅틱스의 탐색에 초점을 맞추었습니다. 공급업체는 유통에 의한 공급망의 혼란이 소수성 아크릴 사슬에 대한 의존 위험을 드러내기 때문에 원료 단량체의 이중 조달을 강조합니다.

지역별 분석

2025년 북미는 안내 렌즈 시장에서 41.76%의 수익 점유율을 차지해 선두가 되었습니다. 메디케어가 기본 백내장 수술을 커버하고 환자가 자기 부담으로 고급 렌즈를 선택할 수 있기 때문입니다. 미국에서는 프리미엄 제품의 보급률이 21.80%를 넘어 안과 진료소는 RLE(재수정체 삽입술) 후보자를 유치하기 위해 적극적인 광고를 전개하고 있습니다. 이 지역의 안내 렌즈 시장 규모는 클리닉 수술실의 급속한 보급과 조정가능한 렌즈 플랫폼의 지지를 받아 2031년까지 연평균 복합 성장률(CAGR) 5.55%로 41억 8,000만 달러 이상에 달할 것으로 예측되고 있습니다.

아시아태평양은 고령화, 확대되는 중산계급 구매력, 의료관광 클러스터 성장으로 7.22%라는 가장 빠른 CAGR을 기록하고 있습니다. 태국과 싱가포르에서는 3일간의 회복 체류를 패키징한 프리미엄 안구 렌즈 수술을 제공하고 있으며, 해외 환자 수를 불러들여 평균 판매 가격을 끌어 올리고 있습니다. 중국에서는 백내장 수술의 진찰 체제가 확대를 계속하고 있지만, 프리미엄 제품의 보급률은 여전히 9.75% 미만으로 소득 수준과 보험 상환액이 상승하면 큰 성장 여지가 있음을 보여주고 있습니다. 인도의 고 볼륨 기지에서는 효율성과 모듈식 가격 설정을 결합한 아라빈드 모델이 재현되어 도시의 소비자에게 프리미엄 제품의 채택이 현실적인 선택이 되고 있습니다.

유럽은 상환제도가 성숙하고 있는 한편, 지속가능성에 대한 규범이 강하게 요구되고 있습니다. 규제 당국은 플라스틱 삭감형 전달 시스템을 권장하고 있으며, 렌즈 제조업체는 바이오 유래 카트리지 폴리머의 시험 도입을 진행하고 있습니다. 독일과 스페인에서는 프리미엄 침투율이 19.70% 가까이에 달하고 있습니다만, 영국은 국민보건서비스(NHS)의 예산 제약에 의해 보수적인 자세를 유지하고 있습니다. 2025년에 CE 마크를 취득한 클레어온 비비티 등의 제품이 시장 투입되어 노안 교정의 선택사항이 외과의사에게 퍼집니다.

중동 및 아프리카은 걸프 국가와 북아프리카에서 관민 연계를 통한 전문 안과 병원의 건설로 인해 낮은베이스에서 확대되고 있습니다. 부유층 환자는 프리미엄 수술을 위해 유럽과 아시아로 여행하는 경우가 많은 것, 두바이와 리야드에 신설된 센터는 이 해외 유출 경향의 역전을 목표로 하고 있습니다.

남미에서는 북미로부터의 가격차를 이용한 환자 유입이 추풍이 되고, 브라질에서는 민간보험사가 특정 EDOF렌즈의 보험 적용을 개시한 것으로, 지역 수요를 늘리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 노화에 따른 세계의 백내장 수술 건수 증가

- 프리미엄 및 노안 교정용 안내 렌즈의 채택 급증

- 신속한 제품 교체 주기 : 빛 조절 가능 렌즈(LAL) 및 AI 설계 렌즈

- 40-60세 연령층에 있어서의 굴절 교정 렌즈 교환술(RLE)의 성장

- 의료 관광 거점에 의한 시술 비용의 저감

- 수술실(OR) 병목 현상을 완화하는 프리로디드(Pre-loaded) 일회용 IOL 시스템

- 시장 성장 억제요인

- 프리미엄 안내 렌즈의 고액의 자기 부담 비용과 불충분한 보험 적용 범위

- 수술 후 이상광시증(Dysphotopsia) 우려로 인한 의료진 채택 제한

- 특수 소수성 아크릴 수지에 대한 공급망 의존도

- 렌즈 삽입 기구 내 일회용 플라스틱 사용에 대한 지속가능성 압박

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 단초점 안내 렌즈

- 프리미엄 안내 렌즈

- 다초점

- 난시 교정용 (Toric)

- 조절 기능

- 안내 삽입 렌즈(PIOL)

- 기타

- 소재별

- 소수성 아크릴

- 친수성 아크릴

- 실리콘

- 폴리메틸메타크릴레이트(PMMA)

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 안과 클리닉

- 기타

- 용도별

- 백내장

- 노안

- 각막 질환

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Alcon Inc.

- Johnson & Johnson Vision

- Bausch Lomb Corp.

- Carl Zeiss Meditec AG

- Hoya Corp.

- Staar Surgical Co.

- Rayner Group

- HumanOptics Holding AG

- Lenstec Inc.

- PhysIOL(BVI)

- Ophtec BV

- SAV-IOL SA

- Aurolab

- Medicontur Medical Engineering

- Santen Pharmaceutical Co.

- Biotech Healthcare

- Eyekon Medical

- Rodenstock Group

- Visioncare Ophthalmic Technologies

- Hanita Lenses

제7장 시장 기회와 장래의 전망

SHW 26.01.26The intraocular lens market size in 2026 is estimated at USD 7.34 billion, growing from 2025 value of USD 6.89 billion with 2031 projections showing USD 10.09 billion, growing at 6.57% CAGR over 2026-2031.

Premium lens innovations, the growing pool of older adults, and a shift toward outpatient surgical models anchor this expansion. An enlarging 65+ demographic brings a steady cataract case flow, while presbyopia-correcting and light-adjustable designs let surgeons match rising lifestyle expectations for spectacle independence. Silicone and next-generation hydrophobic acrylic materials reduce inflammatory events, encouraging surgeons to discuss premium upgrades more confidently. Asia-Pacific's medical-tourism corridors widen access to advanced lenses, and office-based suites improve provider economics, creating new procedure capacity. Competitive intensity stays high because every product cycle that lifts visual quality or lowers dysphotopsia quickly resets surgeon preferences.

Global Intraocular Lens Market Trends and Insights

Aging-linked rise in global cataract procedures

Cataract incidence parallels population longevity. Individuals over 80 have a 70% likelihood of developing lenticular opacity, and many expect high-quality vision for continued digital engagement and later-life employment. Ambulatory surgery centers already log cataract as their largest case type, representing 19% of ASC volume in 2024. Capacity pressure in Asia-Pacific magnifies because demographic aging outpaces clinic build-out, so providers increasingly adopt high-throughput models that pair phaco units with preloaded lens systems.

Surge in adoption of premium / presbyopia-correcting IOLs

Premium penetration rose from 15.5% in 2019 to 18.5% in 2021 despite reimbursement gaps. Light-adjustable optics let surgeons refine power post-op, shrinking the risk of residual refractive error. Alcon holds more than 60% of this segment on the strength of PanOptix and Vivity families. Enhanced monofocal designs such as Tecnis Eyhance extend depth without the photic issues of diffractive rings, broadening eligibility for patients wary of halo or glare.

High out-of-pocket cost and uneven reimbursement for premium IOLs

Patients often pay USD 1,500-3,000 per eye because CMS lists no New Technology IOL codes, creating a two-tier access model. The financial load includes diagnostic aberrometry and follow-up adjustments, deterring price-sensitive candidates. International travel can lower the bill, yet quality assurance varies across facilities.

Other drivers and restraints analyzed in the detailed report include:

- Rapid product cycles: light-adjustable and AI-designed lenses

- Growth of refractive lens exchange in the 40-60 age cohort

- Post-operative dysphotopsia concerns limiting surgeon uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monofocal lenses retained volume leadership with 62.68% intraocular lens market share in 2025. Premium categories, spanning trifocal, toric, EDOF, and accommodating designs, post a 7.16% CAGR that surpasses baseline cataract growth. Demand stems from patients who prioritize uncorrected near vision and from surgeons promoting refractive outcomes as part of cataract management. Multifocal options like PanOptix yield high spectacle independence and fewer halos than early bifocal models. Toric monofocals correct up to 4 D of corneal cylinder and have become routine in eyes with >=1 D astigmatism. EDOF optics such as Tecnis Symfony trade some near acuity for reduced photic side effects, fitting patients skeptical about diffractive rings. Accommodating prototypes including Juvene target >=3.5 D amplitude, aiming to replicate physiologic focus change, a milestone market observers expect to unlock accelerated premium conversion.

Surgical centers bundle presbyopia-correcting lenses with femtosecond assisted capsulotomy to enhance centration, while topographers refine pre-op planning for toric axis alignment. Clinicians report that post-refractive-surgery patients often prefer premium solutions because light-adjustable technology can fine-tune residual error. The premium tier extends revenue per procedure, helping clinics offset reimbursement headwinds and encouraging investment in advanced diagnostics.

Hydrophobic acrylic continues to underpin almost half of the intraocular lens market size thanks to foldability, capsular biocompatibility, and glistening-resistant formulations. Surface-engineered variants like Clareon boost water content to aid clarity yet maintain low calcification risk. Silicone's 7.05% CAGR signals a renaissance; higher purity grades minimize inflammatory cell adhesion, making these lenses attractive in uveitic eyes. Newer silicone optics incorporate UV-blocking chromophores and can accept femtosecond power refinement post-implant. Hydrophilic acrylic now represents 28.90% of units, rehabilitated by cross-linked polymers and anti-calc coatings that preserve clarity in diabetic vitreous environments. PMMA use declines except in trauma cases that benefit from rigid stability.

Material research focuses on reducing posterior capsule opacification through edge-design micro-texturing and exploring bioresorbable haptics that vanish after capsular fibrosis secures the optic. Suppliers stress dual-sourcing of raw monomers because pandemic disruptions revealed dependency risks in hydrophobic acrylic chains.

The Intraocular Lens Market is Segmented by Product Type (Monofocal IOL, Premium IOL [Multifocal, Toric, and More], and More), Material (Hydrophobic Acrylic and More), End User (Hospitals, Ambulatory Surgery Centers, and More), Application (Cataract, Presbyopia, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the intraocular lens market in 2025 with 41.76% revenue because Medicare covers baseline cataract surgery and patients can self-fund upgrades. Premium penetration tops 21.80% in the United States, and ophthalmology practices deploy heavy advertising to attract RLE candidates. The intraocular lens market size for the region is projected to surpass USD 4.18 billion by 2031 at 5.55% CAGR, supported by rapid adoption of office-based surgical suites and adjustable-lens platforms.

Asia-Pacific records the fastest 7.22% CAGR thanks to demographic aging, expanding middle-class spending power, and thriving medical-tourism clusters. Thailand and Singapore package premium IOL surgery with three-day recovery stays, drawing inbound volumes that lift average selling prices. China continues to scale cataract capacity, yet premium uptake remains below 9.75%, signaling sizable headroom for growth once income and reimbursement levels rise. India's high-volume hubs replicate the Aravind model that combines efficiency with modular pricing, bringing premium adoption into reach for urban consumers.

Europe features mature reimbursement but strong sustainability norms. Regulators encourage reduced-plastic delivery systems, prompting lens makers to trial bio-derived cartridge polymers. Germany and Spain report premium penetration near 19.70%, while the United Kingdom remains conservative amid National Health Service budget constraints. CE-marked launches such as Clareon Vivity in 2025 widen presbyopia-correction choice for surgeons.

The Middle East and Africa expand from a lower base as public-private partnerships build specialty eye hospitals in Gulf states and North Africa. Wealthy patients often fly to Europe or Asia for premium surgery, but new centers in Dubai and Riyadh aim to reverse outbound flow.

South America benefits from price-arbitrage seekers from North America; Brazil's private insurers now reimburse certain EDOF lenses, lifting regional demand.

- Alcon

- Johnson & Johnson

- Bausch + Lomb Corp.

- Carl Zeiss

- Hoya Corp.

- Staar Surgical Co.

- Rayner Group

- HumanOptics Holding AG

- Lenstec

- PhysIOL (BVI)

- Ophtec BV

- SAV-IOL SA

- Aurolab

- Medicontur Medical Engineering

- Santen Pharmaceutical Co.

- Biotech Healthcare

- EyeKon Medical

- Rodenstock Group

- Visioncare Ophthalmic Technologies

- Hanita Lenses

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-Linked Rise in Global Cataract Procedures

- 4.2.2 Surge In Adoption of Premium / Presbyopia-Correcting IOLs

- 4.2.3 Rapid Product Cycles: Light-Adjustable & AI-Designed Lenses

- 4.2.4 Growth Of Refractive-Lens-Exchange (RLE) In the 40-60 Age Cohort

- 4.2.5 Medical-Tourism Hubs Lowering Procedure Costs

- 4.2.6 Pre-Loaded, Single-Use IOL Systems Easing OR Bottlenecks

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Cost & Patchy Reimbursement for Premium IOLs

- 4.3.2 Post-Operative Dysphotopsia Concerns Limiting Surgeon Uptake

- 4.3.3 Supply-Chain Dependence on Specialty Hydrophobic Acrylics

- 4.3.4 Sustainability Pressures on Single-Use Plastics in Lens Delivery

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Monofocal IOL

- 5.1.2 Premium IOL

- 5.1.2.1 Multifocal

- 5.1.2.2 Toric

- 5.1.2.3 Accommodating

- 5.1.3 Phakic Intraocular Lens (PIOL)

- 5.1.4 Others

- 5.2 By Material

- 5.2.1 Hydrophobic Acrylic

- 5.2.2 Hydrophilic Acrylic

- 5.2.3 Silicone

- 5.2.4 Polymethyl-methacrylate (PMMA)

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Ophthalmology Clinics

- 5.3.4 Others

- 5.4 By Application

- 5.4.1 Cataract

- 5.4.2 Presbyopia

- 5.4.3 Corneal Disorders

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Johnson & Johnson Vision

- 6.3.3 Bausch + Lomb Corp.

- 6.3.4 Carl Zeiss Meditec AG

- 6.3.5 Hoya Corp.

- 6.3.6 Staar Surgical Co.

- 6.3.7 Rayner Group

- 6.3.8 HumanOptics Holding AG

- 6.3.9 Lenstec Inc.

- 6.3.10 PhysIOL (BVI)

- 6.3.11 Ophtec BV

- 6.3.12 SAV-IOL SA

- 6.3.13 Aurolab

- 6.3.14 Medicontur Medical Engineering

- 6.3.15 Santen Pharmaceutical Co.

- 6.3.16 Biotech Healthcare

- 6.3.17 Eyekon Medical

- 6.3.18 Rodenstock Group

- 6.3.19 Visioncare Ophthalmic Technologies

- 6.3.20 Hanita Lenses

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment