|

시장보고서

상품코드

1851581

E-commerce 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)E-commerce Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

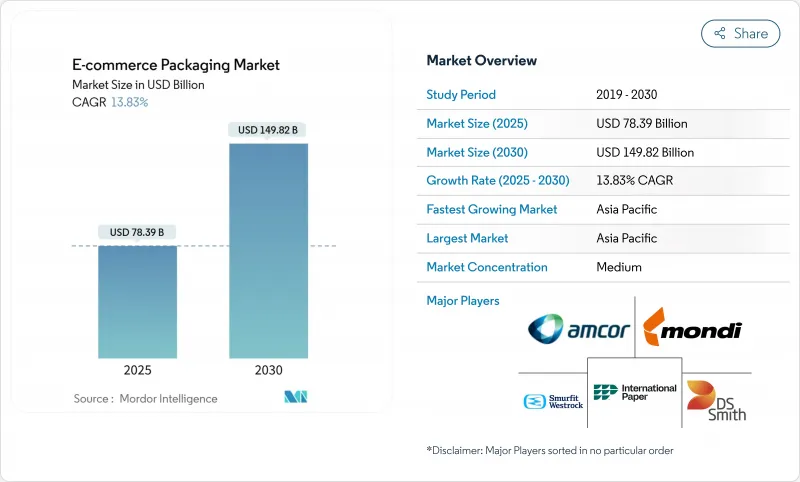

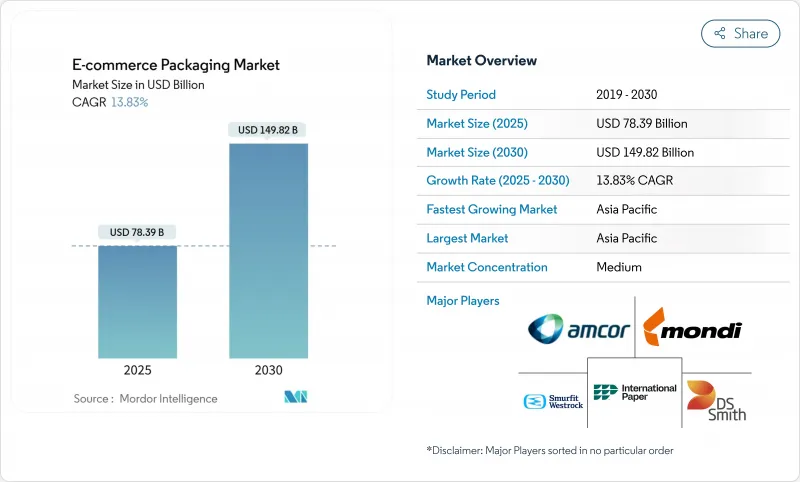

E-commerce 포장 시장 규모는 2025년에 783억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 13.83%로, 2030년에는 1,498억 2,000만 달러에 달할 것으로 예상됩니다.

취급량의 신장은 온라인 소매 거래의 급증에 기인하는 것으로, 과거에는 점포에서 정리해 배송하고 있던 것이, 소포 1개 마다의 배송에 대신해 받고 있습니다. 재활용 어려운 소재에 벌칙을 부과하는 규제의 의무화와 자동화와 제품 설계 소프트웨어의 급속한 진보가 더해져, 보다 스마트하고 경량, 지속 가능한 팩에 대한 수요가 계속 높아지고 있습니다. 종이, 바이오플라스틱, 단일 소재의 플렉서블 필름에 대한 소재 대체는 브랜드가 옴니채널의 물류 네트워크로 상품을 보호하면서 새로운 재활용 함량 할당에 맞추어 가속화하고 있습니다. 한편, 프리미엄의 개봉 체험을 요구하는 소비자의 기대에 의해 판매자는 미관과 사용한 상품의 순환성의 밸런스를 취하도록 강요되고, 패키지는 코스트 센터로부터 수익을 창출하는 브랜드 자산으로 승화하고 있습니다.

세계의 E-commerce 포장 시장 동향과 인사이트

온라인 소매 GMV의 폭발적인 성장

전자상거래의 총 상품 금액은 세계 2자리 성장을 계속하고 있으며, 주문이 늘어날 때마다 보호 팩에 포장되어 출하되기 때문에 패키지 수요는 소매 매출을 초과하는 속도로 증가하고 있습니다. 중국의 165개 경계 조종사 지역에서만 2024년에는 매일 2,000만 가까이의 수하물이 처리되어 국가 수준의 GMV 확대가 골판지와 메일러 소비를 직접 뒷받침하는 것으로 나타났습니다. 인도 도시의 퀵·커머스 사업자는 현재, 10-15분의 식료품 배달 시간을 목표로 내걸고 있어 깨지기 쉬운 신선 식품을 대량의 나무 상자가 아니라 개별적으로 발송하기 때문에 포장 비율이 높아지고 있습니다. 정기 배송은 매월 보충을 브랜드 판지에 넣어 전달하므로 구독 상거래는 더 많은 양을 늘립니다. 심천의 풀필먼트 허브부터 구미 소비자에 이르기까지 국경을 넘는 상거래에서의 트레이드 레인의 장기화는 플루트 등급을 두껍게 하고, 복수의 운송 수단에 의한 핸들링에 견딜 수 있는 완충재의 필요성을 높이고 있습니다. 이러한 수량과 성능의 변화는 세계 E-commerce 포장 시장의 성장 궤도를 지원합니다.

가볍고 유연한 형식으로 이동

택배 치수 무게 가격 설정은 중간 정도의 판지에 페널티를 부과하기 때문에 판매자는 적절한 크기의 메일러, 접을 수있는 파우치, 마치있는 가방을 채택하여 공수 공간과 운임을 절약 할 수 있습니다. 아마존의 온디맨드 포장 이니셔티브는 머신러닝 소프트웨어와 각 주문 주위에 필름을 밀봉하는 오토버거를 결합하여 출하 시 손상을 24% 줄이고 왕로 운임을 5% 줄였습니다. 빠른 패션과 같은 이익률이 낮은 카테고리는 포장 비용을 상품 가치의 5% 미만으로 줄이기 위해 유연한 폴리 메일러를 사용합니다. 초기 채용은 미국과 유럽에서 가장 강하지만, 마지막 원마일의 비용이 전체 물류비의 30%를 초과할 수 있는 아시아태평양에서는 이러한 추세가 가속화되고 있습니다. 택배업체가 판매량 가격을 강화함에 따라 경량 형식은 E-commerce 포장 시장에서 점점 더 많은 점유율을 얻게 될 것입니다.

엄격한 플라스틱 금지와 EPR 수수료가 비용을 밀어

확대 생산자 책임 제도(EPR)는 각 소재의 실제 재활용 가능성에 따라 수수료를 징수하기 때문에 EU의 일부 시장에서는 재활용이 어려운 다층 파우치 비용이 두 배로 늘고 있습니다. 캘리포니아의 플라스틱 오염방지법에서는 판매된 포장재 1킬로그램마다 일률 요금이 부과되므로, 브랜드는 포트폴리오의 재검토를 강요받거나 벌칙을 흡수해야 합니다. 규제 당국 직원이 없는 소규모 온라인 판매업체는 수수료 신고를 완료하는데 어려움을 겪고 있으며 경쟁 우위는 컴플라이언스 고정비를 더 많은 양으로 분산할 수 있는 종합적인 선수에 기울고 있습니다. 이러한 재정적 역풍은 향후 2년간의 E-commerce 포장 시장의 잠재적인 CAGR을 축소시킵니다.

부문 분석

골판지는 비용 효율성, 높은 스택 강도 및 보편적인 재활용 가능성으로 2024년 E-commerce 포장 시장의 51%를 차지했습니다. 이 분야는 국내 및 수출화물의 골판지 플루트 등급을 공식화한 중국 국가 익스프레스 포장 품질 표준의 혜택을 계속 받고 있습니다. 한편 바이오플라스틱은 2030년까지 연평균 복합 성장률(CAGR)이 14.97%로 가장 급성장하는 소재그룹으로 규제의 추풍과 소비자심리의 변화를 반영하고 있습니다. 컨버터는 PLA와 소비자 사용 후 재생 자원을 혼합하여 인장 성능을 저하시키지 않고 EU의 재생 자원 함량 30% 기준을 충족하는 우편물을 제조합니다. 동남아시아 각지의 확장 가능한 발효시설에 대한 투자로 바이오수지 프리미엄은 서서히 저하되어 고급화장품이나 유기농 식품 판매업자 이외에도 널리 보급될 수 있게 됩니다.

브랜드 소유자는 Scope 3 배출량을 줄이기 위해 골판지의 신뢰할 수 있는 보호 성능과 재생 가능한 대체품의 균형을 맞추고 있습니다. D2C의 전자 장비 판매자는 퇴비화 가능한 필름의 수축 슬리브를 눈에 보이는 지속가능성 업그레이드로 홍보하고 있습니다. 기존의 PE 및 PP 사업자는 기계 재활용에 대응하는 단일 소재의 제품을 설계함으로써 대응하여 점유율을 지키려고 합니다. 재생가능한 폴리머와 화석 유래 폴리머의 공존은 하룻밤 사이에 바뀌는 것이 아니라 전환을 나타내는 것으로, E-commerce 포장 시장에 있어서 양재료 클러스터가 불가결하다는 것을 보증하는 것입니다.

E-commerce 포장 시장 보고서는 소재별(플라스틱, 종이 및 판지, 골판지, 플렉서블 필름·메일러 등), 포장 형태별(상자·판지, 메일러·엔벨로프, 보호 포장 등), 최종 사용자별(패션 및 의류, 가전, 식품 및 음료, 퍼스널케어 및 화장품, 식료품·퀵 코머)로 구분됩니다.

지역 분석

아시아태평양은 2024년 매출 점유율 52%로 E-commerce 포장 시장을 선도했고, 2030년까지의 CAGR은 15.70%를 나타낼 전망입니다. 중국의 국가 표준 GB 43352-2023은 익스프레스 팩의 필수 성능 지표를 정의하고 있으며 600만 명의 활성 온라인 판매자 전체에서 통일된 품질에 대한 기대를 뒷받침하고 있습니다. 동시에 인도의 퀵커머스 매출은 2025년부터 2030년에 걸쳐 3배로 증가해 몬순의 습도에 대응하는 경량이고 내구성 있는 가방에 대한 수요가 높아집니다. 동남아시아의 마켓플레이스도 비슷한 규칙을 채택하고 종이제 쿠션을 활용하여 플라스틱 폐기물을 삭감하고 지역의 기세를 강화하고 있습니다.

북미는 2위입니다. 캘리포니아의 플라스틱 자원 삭감 목표와 캐나다 재활용 어려운 발포 스티롤의 금지로 인해 기판 이동이 가속화되고 있습니다. Fullfilment Center는 골판지 사용량을 12% 줄이는 AI 주도 상자 선택 도구에 투자하여 비용과 지속가능성 목표를 모두 지원합니다. 미국에서는 2025년에 온라인 식료품의 보급률이 16%에 달했으며, 식품과 의약품의 온도 안정 라이너 수요에 박차가 걸려 콜드체인의 혁신도 탄생하고 있습니다.

유럽은 PPWR의 재활용 컨텐츠와 재사용의 의무화를 통해 궁극적으로 전 세계적으로 확장되는 형식을 형성하고 있으며, 여전히 순환성의 세계적인 실험장이 되고 있습니다. 독일 소매업체는 도시의 밀집지역에서 일회용 팩을 80% 줄이는 리터너블 전자 식료품 상자를 시험적으로 도입하고 있습니다. 다른 지역에서는 중동 및 아프리카가 널리 보급되고 뒤쳐져 있지만, 국경을 넘어선 플랫폼이 물류 실적를 확대함에 따라 2자리 성장을 기록하고 있습니다. 인프라 격차와 세관의 복잡성이 물량을 억제하고 있지만, 스마트폰의 보급이 장기적인 상승을 이끌어내고, 신흥 지역이 E-commerce 포장 시장 전망 확대에 통합되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 온라인 소매 GMV의 폭발적 성장

- DIM-웨이트·코스트를 낮추기 위해, 경량으로 플렉서블한 포맷으로의 변화가 진행

- 제지와 바이오 베이스의 채용을 가속하는 지속가능성 규제

- 브랜드 인게이지먼트 채널로서의 개봉 체험

- AI를 활용한 제품에의 적합 자동화가 재료의 낭비를 생략

- 퀵커머스/구독·소매의 급속한 대두에 의한 출하 빈도의 상승

- 시장 성장 억제요인

- 엄격한 세계의 플라스틱 금지와 EPR 요금이 컴플라이언스 비용 상승 촉진

- 크래프트지와 수지의 가격 변동이 컨버터의 마진을 압박

- 크로스 보더·플루필먼트의 파손 및 반품율이 포장의 ROI를 저하

- 데이터와 지식의 갭 속에서 재설계를 강요받는 카본 실적 감사

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 기업 간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 재료 유형별 부문

- 플라스틱

- 종이 및 판지

- 골판지

- 유연 필름 및 메일러

- 바이오플라스틱

- 기타

- 포장 형태별 부문

- 박스 및 카톤

- 메일러 및 봉투

- 보호 포장(공극 충전재, 완충재, 라이너)

- 라벨, 테이프 및 밀봉재

- 특수/반환형 시스템

- 최종 사용자별 부문

- 패션 및 의류

- 소비자 일렉트로닉스

- 식음료

- 퍼스널케어 및 화장품

- 식료품 및 퀵커머스

- 가정 및 생활용품/가구

- 기타 온라인 소매업체

- 지역별 세분화

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(MandA, 능력, 기술)

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Mondi plc

- International Paper

- Smurfit Kappa Group

- DS Smith plc

- WestRock Company

- Georgia-Pacific LLC

- Sealed Air Corporation

- Ranpak Holdings Corp.

- Pregis LLC

- Klabin SA

- Rengo Co. Ltd

- Stora Enso Oyj

- Nippon Paper Industries

- Oji Holdings

- Ranpak Holdings Corp

- Packhelp SA

- Shorr Packaging Corp.

- Packsize Intl.

- Packsize International

제7장 시장 기회와 향후 전망

KTH 25.11.24The E-commerce Packaging Market size is estimated at USD 78.39 billion in 2025, and is expected to reach USD 149.82 billion by 2030, at a CAGR of 13.83% during the forecast period (2025-2030).

Volume growth stems from the surge in online retail transactions, where every single-parcel shipment replaces what was once a consolidated store delivery. Regulatory mandates that penalize difficult-to-recycle materials, coupled with rapid advances in automation and fit-to-product design software, continue to propel demand for smarter, lighter, and more sustainable packs. Material substitution toward paper, bioplastic, and mono-material flexible films is accelerating as brands align with new recycled-content quotas while still protecting goods in omnichannel logistics networks. Meanwhile, consumer expectations for premium unboxing experiences force sellers to balance aesthetics with end-of-life circularity, elevating packaging from a cost center to a revenue-generating brand asset.

Global E-commerce Packaging Market Trends and Insights

Explosive Online Retail GMV Growth

E-commerce gross merchandise value continues to climb in double digits worldwide, and every incremental order ships in its protective pack, multiplying packaging demand faster than headline retail sales. China's 165 cross-border pilot zones alone processed nearly 20 million packages daily in 2024, underscoring how country-level GMV expansion directly fuels corrugated and mailer consumption. Urban India's quick-commerce operators now target 10-to-15-minute grocery delivery windows, raising packaging-to-product ratios because fragile fresh items ship individually rather than in bulk crates. Subscription commerce further amplifies volumes as recurring shipments deliver monthly replenishments in branded cartons. Longer trade lanes in cross-border commerce, from Shenzhen fulfilment hubs to Western consumers, elevate the need for thicker flute grades and engineered cushioning that can withstand multi-modal handling. These volume and performance shifts anchor the growth trajectory of the global e-commerce packaging market.

Shift Toward Lightweight and Flexible Formats

Courier dimensional-weight pricing penalizes half-empty cartons, pushing sellers to adopt right-sized mailers, collapsible pouches, and gusseted bags that shave airspace and freight spend. Amazon's on-demand packaging initiative trimmed shipping damage 24% and cut outbound freight costs 5% by pairing machine-learning software with auto-baggers that seal film around each order. Lower-margin categories such as fast-fashion rely on flexible poly-mailers to keep packaging costs below 5% of product value, while mono-material films answer recyclability rules without sacrificing density gains. Early adoption is strongest in the United States and Europe, but the trend accelerates in Asia Pacific, where last-mile costs can exceed 30% of total logistics spend. As couriers tighten volumetric pricing, lightweight formats are likely to capture an increasing share of the e-commerce packaging market.

Stringent Plastics Bans and EPR Fees Inflate Costs

Extended Producer Responsibility schemes levy fees that vary with each material's real-world recyclability, doubling the cost of difficult-to-recycle multilayer pouches in some EU markets. California's Plastic Pollution Prevention Act tags flat fees on every kilogram of packaging sold, compelling brands to overhaul portfolios or absorb penalties. Smaller online sellers lacking regulatory staff struggle to complete fee filings, tilting competitive advantage toward integrated players that can spread compliance fixed costs across higher volumes. These financial headwinds pare back the potential CAGR of the e-commerce packaging market over the next two years.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Regulations Accelerating Paper and Bio-Based Adoption

- Unboxing Experience as a Brand Channel

- Kraft Paper and Resin Price Volatility Squeezes Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrugated board captured 51% of the e-commerce packaging market in 2024 thanks to cost efficiency, high stacking strength, and near-universal curbside recyclability. The segment continues to benefit from China's national express-packaging quality standard, which formalizes corrugate flute grades for domestic and export shipments. Meanwhile, bioplastics form the fastest-growing material group at a 14.97% CAGR through 2030, reflecting both regulatory tailwinds and shifting consumer sentiment. Converters blend PLA with post-consumer recyclate to create mailers that meet EU 30% recycled-content thresholds without compromising tensile performance. Investments in scalable fermentation facilities across Southeast Asia will gradually lower bio-resin premiums, enabling wider uptake beyond premium cosmetics and organic food sellers.

Brand owners balance corrugated's reliable protection with renewable alternatives to reduce Scope 3 emissions. Although corrugate commands volume, bioplastics bring differentiation; D2C electronics sellers tout compostable film shrink sleeves as a visible sustainability upgrade. Traditional PE and PP operators respond by designing mono-material variants compatible with mechanical recycling, seeking to defend their share. The coexistence of renewable and fossil-based polymers signals a transition, not an overnight swap, ensuring both material clusters remain essential to the e-commerce packaging market.

The E-Commerce Packaging Market Report is Segmented by Material (Plastic, Paper and Paperboard, Corrugated Board, Flexible Films and Mailers, and More), Packaging Format (Boxes and Cartons, Mailers and Envelopes, Protective Packaging, and More), End-User Vertical (Fashion and Apparel, Consumer Electronics, Food and Beverages, Personal Care and Cosmetics, Grocery and Quick-Commerce, and Other End Users), and Geography.

Geography Analysis

Asia Pacific led the e-commerce packaging market with a 52% revenue share in 2024 and is scaling at a 15.70% CAGR through 2030. China's national standard GB 43352-2023 defines mandatory performance metrics for express packs, driving uniform quality expectations across 6 million active online sellers. Concurrently, India's quick-commerce sales triple between 2025 and 2030, elevating demand for lightweight yet durable bags that perform in monsoon humidity. Southeast Asian marketplaces adopt similar rules, leveraging paper cushioning to cut plastic waste, reinforcing regional momentum.

North America ranks second. California's plastic-source-reduction targets and Canada's ban on difficult-to-recycle foam prompt accelerated substrate shifts. Fulfilment centers invest in AI-driven box-selection tools that trim corrugated usage by 12%, supporting both cost and sustainability goals. The United States also incubates cold-chain innovations as online grocery penetration touches 16% in 2025, spurring demand for temperature-stable liners across food and pharma.

Europe remains the global test bed for circularity, with the PPWR's recycled-content and reuse mandates shaping formats that eventually scale worldwide. Retailers in Germany pilot returnable e-grocery crates that cut single-use packs by 80% in dense urban districts. Elsewhere, the Middle East and Africa trail in adoption but record double-digit gains as cross-border platforms extend logistics footprints. Infrastructure gaps and customs complexities temper volume, yet rising smartphone penetration unlocks long-run upside, embedding emerging regions in future expansion of the e-commerce packaging market.

- Amcor plc

- Mondi plc

- International Paper

- Smurfit Kappa Group

- DS Smith plc

- WestRock Company

- Georgia-Pacific LLC

- Sealed Air Corporation

- Ranpak Holdings Corp.

- Pregis LLC

- Klabin SA

- Rengo Co. Ltd

- Stora Enso Oyj

- Nippon Paper Industries

- Oji Holdings

- Ranpak Holdings Corp

- Packhelp SA

- Shorr Packaging Corp.

- Packsize Intl.

- Packsize International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of online retail GMV

- 4.2.2 Shift toward lightweight and flexible formats to lower DIM-weight costs

- 4.2.3 Sustainability regulations accelerating paper and bio-based adoption

- 4.2.4 "Unboxing experience" as a brand-engagement channel

- 4.2.5 AI-enabled fit-to-product automation reducing material waste

- 4.2.6 Rapid rise of quick-commerce/subscription retail raising shipment frequency

- 4.3 Market Restraints

- 4.3.1 Stringent global plastics bans and EPR fees inflate compliance costs

- 4.3.2 Kraft paper and resin price volatility squeezes converter margins

- 4.3.3 Cross-border fulfilment damage/return rates erode ROI on packaging

- 4.3.4 Carbon-footprint audits forcing redesigns amid data-knowledge gaps

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Segmentation by Material Type

- 5.1.1 Plastic

- 5.1.2 Paper and Paperboard

- 5.1.3 Corrugated Board

- 5.1.4 Flexible Films and Mailers

- 5.1.5 Bioplastics

- 5.1.6 Others

- 5.2 Segmentation by Packaging Format

- 5.2.1 Boxes and Cartons

- 5.2.2 Mailers and Envelopes

- 5.2.3 Protective Packaging (void-fill, cushioning, liners)

- 5.2.4 Labels, Tapes and Closures

- 5.2.5 Specialty/Returnable Systems

- 5.3 Segmentation by End User

- 5.3.1 Fashion and Apparel

- 5.3.2 Consumer Electronics

- 5.3.3 Food and Beverage

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Grocery and Quick-Commerce

- 5.3.6 Home and Living/Furniture

- 5.3.7 Other Online Retailers

- 5.4 Segmentation by Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, capacity, tech)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 International Paper

- 6.4.4 Smurfit Kappa Group

- 6.4.5 DS Smith plc

- 6.4.6 WestRock Company

- 6.4.7 Georgia-Pacific LLC

- 6.4.8 Sealed Air Corporation

- 6.4.9 Ranpak Holdings Corp.

- 6.4.10 Pregis LLC

- 6.4.11 Klabin SA

- 6.4.12 Rengo Co. Ltd

- 6.4.13 Stora Enso Oyj

- 6.4.14 Nippon Paper Industries

- 6.4.15 Oji Holdings

- 6.4.16 Ranpak Holdings Corp

- 6.4.17 Packhelp SA

- 6.4.18 Shorr Packaging Corp.

- 6.4.19 Packsize Intl.

- 6.4.20 Packsize International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment