|

시장보고서

상품코드

1851595

자동차 유압 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Hydraulic Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

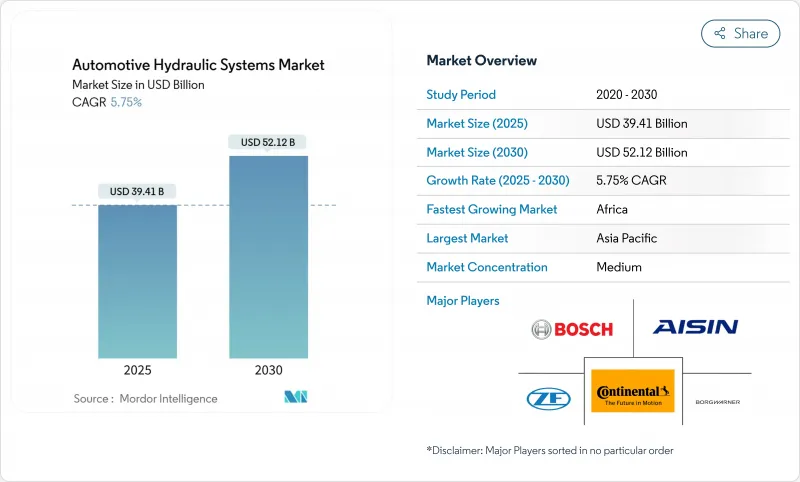

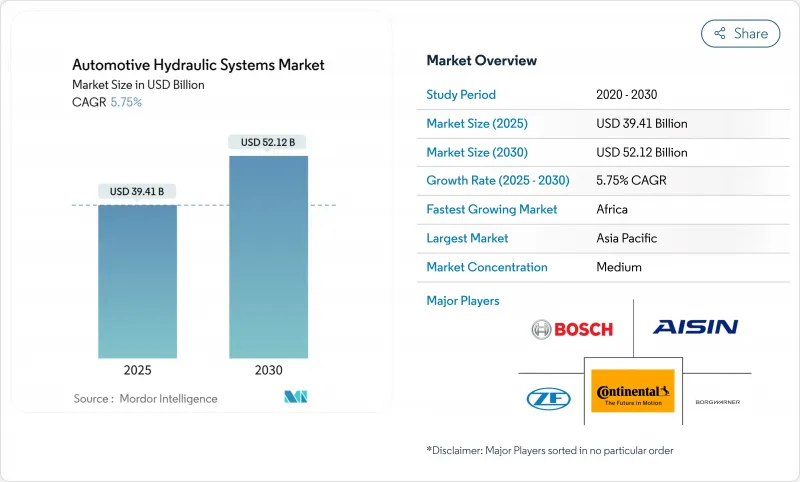

자동차 유압 시스템 시장의 2025년 시장 규모는 394억 1,000만 달러에 달하고, CAGR 5.75%를 나타내 2030년에는 521억 2,000만 달러로 확대될 것으로 예측되고 있습니다.

전동화에도 불구하고 꾸준히 전진하고 있는 것은 이 분야가 핵심 브레이크, 스티어링, 서스펜션의 역할을 유지할 수 있다는 것을 반영하고 있습니다. 세계적인 브레이크 안전 규제 강화, 상용차 생산 대수 증가, 레벨 3 자율 주행 플랫폼에 전동 유압 모듈의 보급이 계속해서 수요를 밀어 올리고 있습니다. 중국의 생산 성장과 인도의 생산 능력 증대 덕분에 아시아태평양은 여전히 제조의 중심이며 아프리카는 인프라 지출의 견인 역할로 새로운 비즈니스 기회가되고 있습니다. 동시에 럭셔리 자동차 제조업체는 승차감을 차별화하기 위해 유압 서스펜션에 의존하며, 상용차는 실험적 대안보다 시행 착오를 거친 유압의 신뢰성을 우선합니다.

세계의 자동차 유압 시스템 시장 동향 및 인사이트

세계 상용차 생산 및 판매 증가

트럭과 버스의 생산량이 급증하고 있어 브레이크, 스티어링, 보조 구동용으로 여러 개의 고압 회로가 필요하기 때문에 1대당 유압 부품이 증가하고 있습니다. 인도 산업은 2024년에 3,060만 대의 차량을 생산하여 국내 및 수출 시장 전체에서 유압 수요를 강화했습니다. 미국의 함대 사업자는 섀시 부족에 직면하고 있으며 정기적인 유압 유지 보수가 필요한 트럭 이용률이 높아지고 있습니다. 제로 방출 트럭의 전동 파워트레인은 유압 상태로 여분의 열 관리 루프를 도입하여 부품 양을 더욱 유지합니다. 운영자는 입증된 내구성을 평가하고 있으며, 이는 전동화가 확산되어도 자동차 유압 시스템 시장을 지원합니다.

브레이크 안전규제 강화(ABS, ESC, EBS)

새로운 규칙에 따라 자동차 제조업체는 정확한 유압 조절에 의존하는 자동 비상 브레이크와 강화된 안정성 제어를 설치해야 합니다. NHTSA의 FMVSS 127은 2029년 9월부터 미국의 모든 경차를 대상으로 하며 충돌 회피 속도 목표를 시속 62마일로 설정합니다. EU의 차기 Euro7 기준에서는 브레이크 입자 규제가 도입되어 낮은 먼지 유압 부품의 채용이 추진됩니다. 이러한 요구 사항은 자동차 유압 시스템 시장에서 고급 밸브, 부스터 및 마이크로펌프에 대한 대응 가능한 수요를 확대합니다.

완전 전동 브레이크 및 스티어링 시스템으로의 급속한 변화

배터리 EV 플랫폼은 경량화와 정확한 제어를 목표로 하며, 유체 라인을 생략한 전기기계식 유닛이 지지되어 있습니다. 미국에서는 EPA(환경보호국)의 여러 오염물질 규제가 이러한 전환을 가속화하고 있습니다. 독일 공급업체는 전기 모델이 유압 부품을 줄이면서 생산 실적를 재구성합니다. 상용 트럭은 더 큰 힘이 요구되기 때문에 움직임이 둔하고 장기적인 대체 위험이 자동차 유압 시스템 시장에 무겁게 걸립니다.

부문 분석

브레이크는 2024년 매출의 45.12%를 차지하며 자동차 유압 시스템 시장에서 가장 큰 점유율을 차지했습니다. NHTSA의 긴급 브레이크 규칙 등의 규제 의무화에 의해 탄력적인 수요가 확보되어 순수한 EV조차도 유압 백업 회로를 보유하고 있습니다. 한편, 파워 스티어링 어시스트는 전동 유압 랙이 에너지 효율과 스티어링 느낌의 균형을 맞추면서 CAGR 6.52%를 나타낼 전망입니다. 이는 자동차 유압 시스템 시장 규모가 전동화 플랫폼 내에서 계속 상승하는 방식을 보여줍니다.

충돌 회피 시스템이 고압 변조를 필요로 하기 때문에 브레이크는 안정적입니다. 스티어링 어시스트는 유압의 신속한 반응에 의존하는 액티브 레인 기술을 배경으로 증가하고 있습니다. 서스펜션 용도는 승차감에 대한 프리미엄 자동차 수요로 인해 혜택을 누리지만, 클러치 및 팬 드라이브의 사용은 엔진의 전동화에 따라 쇠퇴합니다. 상용차의 회생 유압 에너지 저장은 소폭이면서도 꾸준히 기여하는 신흥 하위 부문입니다.

마스터 실린더는 2024년 부품 매출의 35.26%를 차지하며 전체 차량 클래스에 대한 보편적인 적합성을 강조했습니다. 유압 펌프는 고급 운전 지원 기능이 온디맨드 압력을 필요로 하기 때문에 CAGR이 7.46%로 가장 높습니다. 이 수치는 자동차 유압 시스템 시장 점유율의 일부를 펌프가 차지하고 있음을 의미하며 패시브에서 활성 제어 아키텍처로의 축 발을 나타냅니다.

저장소, 호스 및 매니폴드는 복합 라인을 사용한 경량 설계로 증가했습니다. 밸브와 액추에이터는 통합 센서가 폐쇄 루프 제어를 허용하므로 가치가 상승합니다. 어큐뮬레이터는 PFAS 프리 유체 솔루션이 개발될 때까지 다양한 전망에 직면하게 되지만, 하이브리드 서스펜션 에너지 저장에 장기적인 관련성이 기대됩니다.

자동차 유압 시스템 시장은 용도별(브레이크, 클러치, 서스펜션 등), 부품별(마스터 실린더, 슬레이브 실린더 등), 차종별(승용차, 소형 상용차 등), 판매 채널별(OEM, 애프터마켓 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)과 수량(단위)으로 제공됩니다.

지역 분석

아시아태평양은 2024년 세계 매출의 48.89%를 차지하며 자동차 유압 시스템 시장의 중심임을 강조했습니다. 중국의 2024년 5월 자동차 생산 대수는 235만 3,000대로 전년대비 7.6% 증가, 신에너지 모델은 33.6% 증가했습니다. 인도의 2024년 생산 대수는 3,060만 대로, 이 지역의 자동차 유압 시스템 시장 규모를 확대해, 장기 수요를 지원했습니다. 일본 보조금에 의한 EV 보급은 파워트레인 유압 용도의 일부를 삭감하는 한편, 브레이크와 서스펜션의 요구를 유지해, 공급자에게 포트폴리오의 재조정을 촉구하고 있습니다. 깊은 공급망과 풍부한 노동력으로 아시아태평양은 대량 판매 부품의 기본 옵션이지만, PFAS 및 누출 규제로 공장은 유체 처리 공정을 업그레이드해야 합니다.

북미에서는 엄격한 안전규제와 급속한 전동화가 혼재하고 있어 유압 수요에 이중파가 밀려들고 있습니다. NHTSA의 새로운 평가 프로토콜과 FMVSS 127은 브레이크 유압의 기술적 복잡성을 유지하는 반면 EPA의 배기 가스 규제는 미래의 수를 줄일 수 있는 EV의 채택을 가속화합니다. 미국은 여전히 레벨 3 자동화 허브이며 전동 유압 모듈 전문가에게 개발 이점을 제공합니다. 캐나다와 멕시코는 USMCA 하에서 통합 회랑을 통해 지역 규모를 강화하고 정책 전환에도 불구하고 북미의 조립 제조업체에 공급을 안정시키고 있습니다.

유럽은 유로 7의 입자 규제와 PFAS 규제에 의해 자금력 있는 기업만 흡수할 수 있는 고가의 재설계를 강요하기 때문에 비용 경쟁력의 저하와의 싸움에 직면하면서도 규칙 책정에서 리드하고 있습니다. 아프리카는 나이지리아, 케냐, 이집트의 인프라 투자가 오프 하이웨이 유압 수요를 끌어 올려 저 수준에서 2030년까지 가장 빠른 CAGR 7.57%를 나타낼 전망입니다. 남미는 거시경제의 불안정성이 시야를 흐리게 하는 것, 광산기계와 농업기계에 결합된 꾸준한 성장을 보여줍니다. 중동 시장은 기존의 파워트레인 선호도와 현지 유압 조립을 촉진할 수 있는 산업 정책상의 인센티브를 겸비하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 상용차 생산·판매 증가

- 브레이크 안전규제 강화(ABS, ESC, EBS)

- 유압 서스펜션에 대한 고급차 수요 증가

- 레벨 3 AD 시스템용 전기 유압 모듈

- 신흥 시장에서의 엔트리 EV용 저가격 유압 팩

- 하이브리드 서스펜션의 회생 유압 에너지 저장

- 시장 성장 억제요인

- 완전 전동 브레이크 및 스티어링 시스템으로의 급속한 변화

- 작동유 누출에 대한 환경 문제

- 엘라스토머 씰의 원재료 부족이 비용 상승 촉진

- 로봇 택시에서 OEM 드라이브 레이크 바이 와이어 선호

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 브레이크

- 클러치

- 서스펜션

- 파워 스티어링 보조 장치

- 팬 구동 시스템

- 밸브 트레인(태핏/액추에이터)

- 기타

- 구성 요소별

- 마스터 실린더

- 슬레이브/휠 실린더

- 리저버

- 호스 및 튜빙

- 유압 펌프

- 밸브 및 매니폴드

- 액추에이터/부스터

- 어큐뮬레이터 및 씰

- 차량 유형별

- 승용차

- 소형 상용차

- 중대형 상용차

- 비도로용 차량(농업 및 건설)

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Continental AG

- Aisin Corporation

- BorgWarner Inc.

- Valeo SA

- Eaton Corporation plc

- Schaeffler AG

- KYB Corporation

- WABCO(ZF CVCS)

- JTEKT Corporation

- GKN Automotive

- Denso Corporation

- Nexteer Automotive Group

- Nissin Kogyo Co. Ltd

- Hitachi Astemo Ltd

- Brembo SpA

- Mando Corp

제7장 시장 기회와 향후 전망

KTH 25.11.24The Automotive Hydraulics Systems Market is valued at USD 39.41 billion in 2025 and is forecast to expand to USD 52.12 billion by 2030, registering a 5.75% CAGR.

Despite electrification, the steady advance reflects the sector's ability to preserve its core braking, steering, and suspension roles. Stricter global brake-safety mandates, rising commercial-vehicle output, and the spread of electro-hydraulic modules into Level 3+ autonomous driving platforms continue to lift demand. Thanks to China's production growth and India's capacity additions, Asia-Pacific remains the manufacturing hub, while Africa represents an emerging opportunity as infrastructure spending gains traction. At the same time, premium-vehicle makers rely on hydraulic suspension to differentiate ride quality, and commercial fleets prioritize tried-and-tested hydraulic reliability over experimental alternatives.

Global Automotive Hydraulic Systems Market Trends and Insights

Rising Global Commercial Vehicle Production & Sales

Surging truck and bus output increases hydraulic content per unit because heavy platforms need multiple high-pressure circuits for braking, steering, and auxiliary drives. India's industry produced 30.6 million vehicles in 2024, reinforcing hydraulic demand across domestic and export markets. U.S. fleet operators face chassis shortages, prompting higher utilisation of trucks requiring regular hydraulic upkeep. Electric powertrains in zero-emission trucks introduce extra thermal management loops that remain hydraulic, further sustaining component volumes. Operators value proven durability, which supports the automotive hydraulics systems market even as electrification spreads.

Stricter Brake-Safety Mandates (ABS, ESC, EBS)

New rules oblige carmakers to install automatic emergency braking and enhanced stability control that rely on precise hydraulic modulation. NHTSA's FMVSS 127 covers all U.S. light vehicles from September 2029 and sets collision-avoidance speed targets of 62 mph. The EU's upcoming Euro 7 standards bring brake particle limits, driving the adoption of low-dust hydraulic components. These requirements enlarge the addressable demand for advanced valves, boosters, and micro-pumps within the automotive hydraulics systems market

Rapid Shift to Fully-Electric Brake & Steering Systems

Battery EV platforms target weight savings and precise control, favouring electromechanical units that omit fluid lines. EPA multi-pollutant standards accelerate this transition in the United States. German suppliers reorganise production footprints as electric models trim hydraulic content. Commercial trucks move more slowly because of higher force requirements, yet long-term substitution risk weighs on the automotive hydraulics systems market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Premium-Vehicle Demand for Hydraulic Suspension

- Electro-Hydraulic Modules for Level-3+ AD Systems

- Environmental Concerns Over Hydraulic-Fluid Leakage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brakes generated 45.12% of 2024 revenue, giving this segment the largest stake in the automotive hydraulics systems market. Regulatory mandates such as NHTSA's emergency braking rule lock in resilient demand, and even pure EVs retain hydraulic backup circuits. Meanwhile, power-steering assist expands at a 6.52% CAGR as electro-hydraulic racks balance energy efficiency with steering feel. This illustrates how the automotive hydraulics systems market size can keep climbing inside electrified platforms.

Brake content remains stable because collision-avoidance systems need high-pressure modulation. Steering assist rises on the back of active-lane technologies that depend on fast hydraulic response. Suspension applications benefit from premium-car demand for ride comfort, while clutch and fan-drive uses fade in line with engine electrification. Regenerative hydraulic energy storage in commercial vehicles marks an emerging sub-segment with modest but steady contributions

Master cylinders constituted 35.26% of component sales in 2024, underscoring their universal fit across vehicle classes. Their dominance ensures stable volume, while hydraulic pumps post the highest 7.46% CAGR as advanced driver assistance features require on-demand pressure. These figures translate into a portion of the automotive hydraulics systems market share for pumps, signalling a pivot from passive to active control architectures.

Reservoirs, hoses, and manifolds record incremental gains driven by lightweight designs using composite lines. Valves and actuators climb in value because integrated sensors enable closed-loop control. Accumulators face mixed prospects pending PFAS-free fluid solutions, yet research promises long-term relevance in hybrid suspension energy storage.

The Automotive Hydraulic Systems Market is Segmented by Application (Brakes, Clutch, Suspension, and More), Component (Master Cylinder, Slave Cylinder, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific commands 48.89% of global revenue in 2024, underscoring its status as the centre of gravity for the automotive hydraulics systems market. China produced 2.353 million vehicles in May 2024, a 7.6% year-on-year rise, while new-energy models jumped 33.6%. India's 2024 output of 30.6 million units enlarges the regional automotive hydraulics systems market size and anchors long-term demand. Japan's subsidy-backed EV rollout reduces some power-train hydraulic applications yet preserves brake and suspension needs, prompting suppliers to recalibrate portfolios. Deep supply chains and abundant labour make Asia-Pacific the default choice for volume components, though PFAS and leakage regulations force factories to upgrade fluid-handling processes.

North America mixes rigorous safety regulations with fast-tracking electrification, creating a dual pull on hydraulic demand. NHTSA's new assessment protocols and FMVSS 127 sustain technical complexity in brake hydraulics, while EPA emissions rules accelerate EV adoption that can trim future volumes. The United States remains a Level 3 automation hub, giving electro-hydraulic module specialists a development advantage. Canada and Mexico buttress regional scale through integrated corridors under USMCA, stabilising supply for North American assemblers despite policy shifts.

Europe leads on rule-making yet battles eroding cost competitiveness, as Euro 7 particle limits and PFAS curbs force costly redesigns that only well-funded firms can absorb. Africa delivers the fastest 7.57% CAGR through 2030 from a low base, with infrastructure spending in Nigeria, Kenya and Egypt lifting off-highway hydraulic demand. South America shows steady growth tied to mining and agriculture machinery, though macroeconomic volatility clouds visibility. Middle Eastern markets combine legacy power-train preferences with industrial-policy incentives that could seed local hydraulic assembly.

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Continental AG

- Aisin Corporation

- BorgWarner Inc.

- Valeo SA

- Eaton Corporation plc

- Schaeffler AG

- KYB Corporation

- WABCO (ZF CVCS)

- JTEKT Corporation

- GKN Automotive

- Denso Corporation

- Nexteer Automotive Group

- Nissin Kogyo Co. Ltd

- Hitachi Astemo Ltd

- Brembo SpA

- Mando Corp

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global commercial?vehicle production & sales

- 4.2.2 Stricter brake-safety mandates (ABS, ESC, EBS)

- 4.2.3 Growing premium-vehicle demand for hydraulic suspension

- 4.2.4 Electro-hydraulic modules for Level-3+ AD systems

- 4.2.5 Low-cost hydraulic packs for entry-level EVs in emerging markets

- 4.2.6 Regenerative hydraulic energy-storage in hybrid suspensions

- 4.3 Market Restraints

- 4.3.1 Rapid shift to fully-electric brake & steering systems

- 4.3.2 Environmental concerns over hydraulic?fluid leakage

- 4.3.3 Elastomer-seal raw-material shortages inflating costs

- 4.3.4 OEM preference for dry brake-by-wire in robotaxi fleets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Application

- 5.1.1 Brakes

- 5.1.2 Clutch

- 5.1.3 Suspension

- 5.1.4 Power-steering Assist

- 5.1.5 Fan-drive Systems

- 5.1.6 Valve-train (Tappets/Actuators)

- 5.1.7 Others

- 5.2 By Component

- 5.2.1 Master Cylinder

- 5.2.2 Slave / Wheel Cylinder

- 5.2.3 Reservoir

- 5.2.4 Hose & Tubing

- 5.2.5 Hydraulic Pump

- 5.2.6 Valve & Manifold

- 5.2.7 Actuator / Booster

- 5.2.8 Accumulator & Seals

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium & Heavy-duty Commercial Vehicles

- 5.3.4 Off-highway Vehicles (Ag & Construction)

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Continental AG

- 6.4.4 Aisin Corporation

- 6.4.5 BorgWarner Inc.

- 6.4.6 Valeo SA

- 6.4.7 Eaton Corporation plc

- 6.4.8 Schaeffler AG

- 6.4.9 KYB Corporation

- 6.4.10 WABCO (ZF CVCS)

- 6.4.11 JTEKT Corporation

- 6.4.12 GKN Automotive

- 6.4.13 Denso Corporation

- 6.4.14 Nexteer Automotive Group

- 6.4.15 Nissin Kogyo Co. Ltd

- 6.4.16 Hitachi Astemo Ltd

- 6.4.17 Brembo SpA

- 6.4.18 Mando Corp

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessmen