|

시장보고서

상품코드

1851661

인메모리 데이터베이스 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)In-Memory Database - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

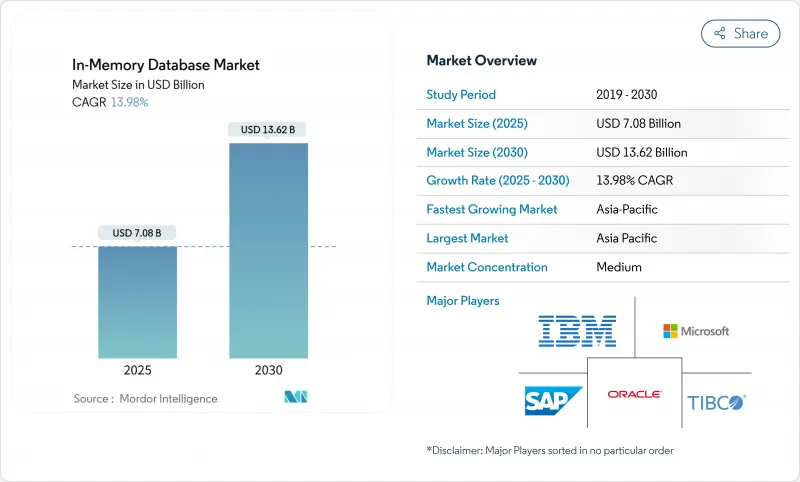

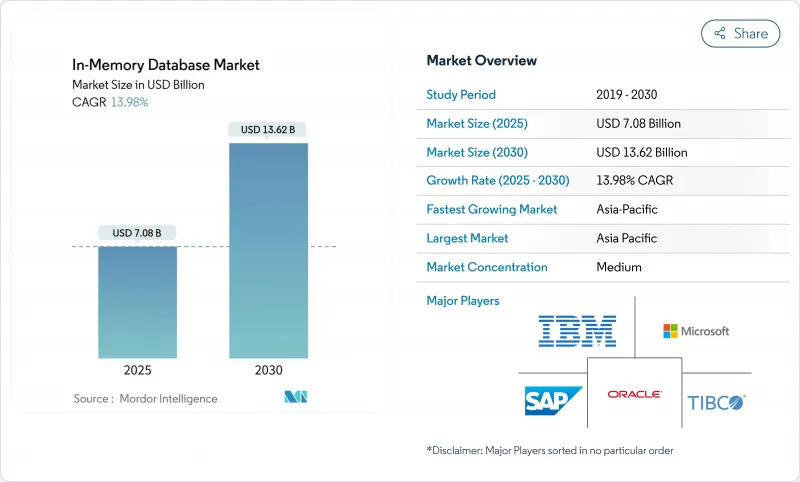

세계의 인메모리 데이터베이스 시장 규모는 2025년에 70억 8,000만 달러로 추정되고, 2030년에는 136억 2,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 13.98%로 추이할 것으로 전망됩니다.

클라우드 네이티브 마이크로서비스, AI 추론 엔진, 스트리밍 분석 플랫폼을 통한 서브밀리초 단위의 성능 요구 사항은 기업을 메모리 중심 아키텍처로 밀어 올리고 있습니다. DRAM 가격 저하와 CXL 기반 영구 메모리 모듈의 출현으로 총 소유 비용이 절감되고 더 많은 워크로드가 디스크 백업 시스템에서 마이그레이션됩니다. 커넥티드 차량 및 산업용 IoT 플랜트에서의 엣지 도입은 로컬 처리에 의해 네트워크 지연의 페널티를 회피할 수 있기 때문에 수요를 더욱 확대했습니다. 기존의 벤더가 하이퍼스케일 클라우드와의 통합을 깊게 하는 한편, 오픈소스 포크가 기세를 늘리고 벤더 록인을 회피하는 새로운 길을 구매자에게 제공했기 때문에 경쟁 역학은 유동적인 채로 있었습니다.

세계의 인메모리 데이터베이스 시장 동향 및 인사이트

서브밀리초의 대기 시간을 요구하는 클라우드 네이티브 마이크로 서비스

클라우드 네이티브를 사용하면 컨테이너화된 마이크로서비스가 마이크로초 단위로 데이터 액세스를 필요로 하고 성능 기준을 재구성했습니다. 세션 스토어, 개인화 엔진, 고주파 거래 플랫폼은 밀리초 단위의 지연이 전환율과 거래 이익을 낮추기 때문에 디스크 백업 데이터베이스에서 메모리 중심 저장소로 이동했습니다. Dragonfly는 AWS Graviton3E 실리콘에서 643만 작업/초를 입증하여 데이터베이스 계층에서 예상되는 상한을 강조했습니다. 모놀리스를 분산 시스템으로 전환한 금융기관 및 디지털 상거래 사업자는 응답 시간의 개선이 구체적인 수익 증가로 이어졌다는 것을 목격하고 이 드라이버의 단기적인 중요성을 강조했습니다.

DRAM 및 퍼시스턴트 메모리의 비용 하락이 TCO 갭 확대

DDR4 및 DDR5 모듈의 세계 스팟 가격은 계속 하락하는 반면 삼성의 CXL 메모리 모듈 하이브리드 프로토타입은 DRAM 클래스의 레이턴시와 퍼시스턴스를 보여 매력적인 비용 프로파일을 실현했습니다. 하이퍼스케일 운영자는 랙 전체에서 메모리를 풀링하여 스트랜드 용량과 백업 사이클을 줄였습니다. 특히 SLA 윈도우가 엄격한 애널리틱스 워크로드에서는 SSD 어레이에 대한 프리미엄이 축소되었기 때문에 기업은 로드맵을 인메모리 도입으로 전환했습니다. 이 효과는 아시아태평양의 제조 기지에서 대규모 히스토리안 데이터 세트를 실시간 디지털 트윈 분석을 위해 메모리로 마이그레이션함으로써 나타납니다.

독자적인 형식을 둘러싼 벤더 락인의 우려

Redis 라이선스가 2024년으로 변경됨에 따라 AWS, Google, Oracle은 Linux Foundation에서 Valkey 포크를 지원하게 되었습니다. 여러 해에 걸친 데이터베이스 프로젝트 예산을 맺고 있던 기업은 종료 비용을 짜고 구매 사이클을 늦추었습니다. 위험을 줄이기 위해 일부 기업은 다중 데이터베이스 오케스트레이션 계층을 채택했지만 이러한 추상화로 인해 대기 시간 패널티가 발생하여 메모리 속도 향상이 부분적으로 상쇄되었습니다.

부문 분석

OLTP 부문은 2024년 인메모리 데이터베이스 시장 점유율의 45.3%를 차지했으며, 은행, 전자상거래, ERP 시스템 등의 신뢰성 있는 트랜잭션 워크로드에 대한 지속적인 의존성을 강조했습니다. 미션 크리티컬 레코드는 여전히 ACID 컴플라이언스를 요구하고 있으며, 기업은 밀리초 이하의 커밋에 대해 성능 프리미엄을 지불하기 때문에 수요가 지속되고 있습니다. OLAP의 도입은 확립된 비즈니스 인텔리전스 프론트엔드를 지원했지만 애널리틱스가 보다 유연한 엔진으로 이동함에 따라 성장이 완만해졌습니다.

HTAP는 단일 플랫폼으로 단순성을 요구하는 기업에 의해 2025-2030년 CAGR 예측이 21.1%로 상승할 전망입니다. GridGain의 플랫폼은 ANSI SQL-99 지원을 유지하면서 디스크 기반 시스템에 비해 최대 1,000배의 속도 향상을 보여주었습니다. 실시간 위험 계산과 공급망 트윈은 동시 읽기 및 쓰기 액세스가 필요하기 때문에 HTAP이 바람직한 아키텍처가 되었습니다. 이 컨버전스는 이전에는 운영과 분석 사이에서 사일로화된 부서의 예산을 증가시켜 인메모리 데이터베이스 시장을 통합 설계로 밀어 올렸습니다.

2024년 매출의 55.4%를 온프레미스가 차지한 이유는 규제 부서가 데이터 레지던시를 완벽하게 관리하고 맞춤형 HA 아키텍처를 필요로 했기 때문입니다. 레거시 기업 소프트웨어 스택은 온프레미스 데이터베이스와 긴밀하게 통합되어 퍼블릭 클라우드가 성숙해도 지출을 지원합니다. 그럼에도 불구하고 디지털 네이티브 기업이 인프라 관리를 피하기 위해 관리 서비스를 채택하여 클라우드 전개가 진행되었습니다.

엣지 및 임베디드 장비의 도입은 커넥티드카와 IIoT 게이트웨이를 뒷받침하여 CAGR 23.2% 전망을 보였습니다. 최신 자동차는 연간 약 300TB를 생산하고 있으며, 자율 주행 기능을 위한 차량 탑재 처리가 요구되고 있습니다. TDengine은 스마트카 텔레메트리에서 Elasticsearch의 10배 압축을 달성하여 업스트림 전송 대역폭을 줄였습니다. 제조업체 각사는 유사한 전략을 생산 라인에도 적용하여 결함을 즉시 검출할 수 있도록 했습니다. 이 시프트는 한때 데이터센터에만 유보된 성능 향상이 이제 엣지에서도 필수적임을 보여주고 메모리 내 데이터베이스 시장 실적를 확대했습니다.

인메모리 데이터베이스 시장은 처리 유형별(OLTP, OLAP, HTAP), 전개 모드별(온프레미스, 기타), 데이터 모델별(SQL, Nosql, 멀티 모델), 조직 규모별(중소기업, 대기업), 용도별(실시간 트랜잭션 처리, 기타), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 시장 세분화, IT 및 통신, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 구분됩니다.

지역 분석

아시아태평양은 2024년 32.2%로 최대 수익을 기록했으며, 17.1%의 연평균 복합 성장률(CAGR) 전망을 유지했습니다. 중국, 일본, 인도의 국가 인더스트리 4.0 프로그램이 공장 자동화에 박차를 가했으며, 서브초 단위의 MES 피드백 루프에 메모리 내 히스토리언 데이터베이스가 필요했습니다. General Motors는 MES 4.0 전개에서 100,000개 이상의 운영 기술을 연결하여 엣지 전개 규모를 보여주었습니다. Nautilus Technologies와 같은 지역 공급업체는 해외 IP에 대한 의존도를 줄이면서 자체 관계형 엔진을 개발했습니다.

북미에서는 금융서비스, 하이퍼스케일 클라우드, 자율주행차의 연구개발을 중심으로 성숙하면서도 혁신이 풍부한 시장이 형성되었습니다. Oracle과 구글은 제휴를 깊게 하고 Oracle 데이터베이스 서비스를 구글 클라우드에서 네이티브로 가동시켜 엔터프라이즈 SQL 기능과 AI 가속기를 융합시켰습니다. 이 지역의 벤처 자금 조달은 드래곤플리와 같은 신흥 기업을 지원하여 경쟁의 난립을 격화시켰습니다.

유럽에서는 GDPR(EU 개인정보보호규정)을 기반으로 하는 데이터 주권 컴플라이언스가 선호되었고, 하이브리드 클라우드의 도입이 가속화되었으며, 온프레미스 클러스터와 로컬 데이터센터에서 관리되는 서비스의 조합이 지원되었습니다. Oracle은 거주 규칙을 충족하기 위해 Database@Azure 제공 지역을 EU의 추가 지역으로 확대했습니다. 또한 이 대륙에서는 엄격한 프라이버시의 틀에 따라 AI 진단을 강화하기 위한 HTAP 데이터베이스의 도입이 헬스케어로 진행되었습니다.

중동 및 아프리카에서는 스마트 시티의 광섬유 및 5G 백본에 투자하여 실시간 분석을 필요로 하는 IIoT의 시험적 도입으로 이어졌습니다. 남미에서는 채굴 사업 및 디지털 뱅킹이 견인역이 되어 저지연의 부정 검출이 프리미엄 메모리 중심의 시스템을 정당화했습니다. 이 두 지역의 절대 지출은 소폭에 머물렀고, 2자리대의 성장으로 인메모리 데이터베이스 시장의 세계 다양성이 확대되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 서브밀리초의 레이턴시를 요구하는 클라우드 네이티브인 마이크로서비스

- DRAM과 영구 메모리의 GB당 단가의 하락에 의해 디스크와의 TCO 격차 확대

- 부정 행위와 네트워크 QoS를 위한 BFSI와 통신에 스트리밍 분석 채택

- 헬스케어에서 AI/ML 모델 서비스를 가속하는 HTAP 아키텍처

- 내장형 IMDB를 필요로 하는 엣지 컴퓨팅의 이용 사례(커넥티드카, IIoT)

- 시장 성장 억제요인

- 독자적인 인메모리 포맷을 둘러싼 벤더의 락인 우려

- 40TB 이상의 클러스터에 대한 고가용성 설계의 복잡성

- 세계 복제를 제한하는 데이터 주권법(예 : 중국 CSL, EU GDPR(EU 개인정보보호규정))

- 밸류체인 분석

- 규제 및 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모 및 성장 예측

- 처리 유형별

- OLTP

- OLAP

- 하이브리드 트랜잭션 및 분석 처리(HTAP)

- 전개 모드별

- 온프레미스

- 클라우드

- 엣지 및 임베디드

- 데이터 모델별

- 관계형(SQL)

- NoSQL(키 밸류, 문서, 그래프)

- 멀티 모델

- 조직 규모별

- 중소기업

- 대기업

- 용도별

- 실시간 트랜잭션 처리

- 운영 분석 및 BI 대시보드

- AI/ML 모델 서빙

- 캐시 및 세션 스토어

- 최종 사용자 업계별

- BFSI

- IT 및 통신

- 소매 및 전자상거래

- 헬스케어 및 생명과학

- 제조업 및 산업용 IoT

- 미디어 및 엔터테인먼트

- 정부 및 방위

- 기타(에너지, 교육 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 대만

- 한국

- 일본

- 인도

- 기타 아시아태평양

- 남미

- 브라질

- 멕시코

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SAP SE

- Oracle Corp.

- Microsoft Corp.

- IBM Corp.

- Redis Ltd.(Redis Enterprise)

- Aerospike Inc.

- VoltDB Inc.

- Couchbase Inc.

- DataStax Inc.

- Hazelcast Inc.

- MemVerge Inc.

- Altibase Corp.

- GridGain Systems Inc.

- Raima Inc.

- McObject LLC

- Pivotal(VMware Tanzu GemFire)

- Amazon Web Services(Amazon ElastiCache & MemoryDB)

- Google Cloud(AlloyDB, Memorystore)

- Alibaba Cloud(ApsaraDB Tair)

- Huawei Cloud(GaussDB IM)

- Tencent Cloud(Tendis)

제7장 시장 기회 및 향후 전망

AJY 25.11.24The global In-Memory Database market size stood at USD 7.08 billion in 2025 and is expected to reach USD 13.62 billion by 2030, advancing at a 13.98% CAGR over the forecast period.

Sub-millisecond performance requirements from cloud-native microservices, AI inference engines, and streaming analytics platforms continued to push enterprises toward memory-centric architectures. Lower DRAM prices and the arrival of CXL-based persistent memory modules have reduced the total cost of ownership, encouraging more workloads to migrate from disk-backed systems. Edge deployments in connected vehicles and Industrial IoT plants further expanded demand because local processing avoids network latency penalties. Competitive dynamics remained fluid as traditional vendors deepened integrations with hyperscale clouds while open-source forks gained momentum, giving buyers new paths to avoid vendor lock-in.

Global In-Memory Database Market Trends and Insights

Cloud-Native Microservices Demanding Sub-Millisecond Latency

Cloud-native adoption reshaped performance baselines as containerized microservices needed data access in microseconds. Session stores, personalization engines, and high-frequency trading platforms shifted from disk-backed databases to memory-centric stores because every millisecond of delay reduced conversion rates or trading profit. Dragonfly demonstrated 6.43 million operations per second on AWS Graviton3E silicon, highlighting the ceiling now expected from database tiers. Financial institutions and digital commerce operators that migrated monoliths to distributed systems saw response-time improvements translate into tangible revenue gains, reinforcing the driver's near-term importance.

Falling DRAM and Persistent Memory Costs Widening TCO Gap

Global spot pricing of DDR4 and DDR5 modules continued to slide, while Samsung's CXL Memory Module Hybrid prototype showed DRAM-class latency with persistence, creating a compelling cost profile. Hyperscale operators pooled memory across racks, reducing stranded capacity and backup cycles. Enterprises pivoted roadmaps toward in-memory deployment because the premium over SSD arrays narrowed, especially for analytics workloads with tight SLA windows. The effect is visible in Asia-Pacific manufacturing hubs where large historian datasets are moved into memory for real-time digital-twin analytics.

Vendor Lock-in Concerns Around Proprietary Formats

Redis's license change in 2024 heightened buyer wariness of proprietary formats, spurring AWS, Google, and Oracle to back the Valkey fork under the Linux Foundation. Enterprises budgeting multi-year database projects factored in exit costs, slowing purchase cycles. To mitigate risk, some adopted multi-database orchestration layers, but those abstractions introduced latency penalties that partially offset memory-speed gains.

Other drivers and restraints analyzed in the detailed report include:

- Streaming Analytics Adoption in BFSI and Telecom

- HTAP Architectures Accelerating AI/ML Model Serving

- High-Availability Design Complexity for Large Clusters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The OLTP segment held 45.3% of the In-Memory Database market share in 2024, underscoring continued reliance on high-integrity transactional workloads across banking, e-commerce, and ERP systems. Demand persisted because mission-critical records still required ACID compliance, with enterprises paying a performance premium for sub-millisecond commits. OLAP deployments addressed established business-intelligence front ends but grew slowly as analytics shifted toward more flexible engines.

HTAP climbed with a 21.1% CAGR forecast from 2025 to 2030 as firms sought single-platform simplicity. GridGain's platform showed up to 1,000X speed-ups over disk-based systems while retaining ANSI SQL-99 support. Real-time risk calculations and supply-chain twins needed simultaneous read-write access, making HTAP the preferred architecture. The convergence unlocked incremental budget from departments earlier siloed between operations and analytics, pushing the In-Memory Database market toward unified designs.

On-premise installations captured 55.4% of 2024 revenue because regulated sectors required full control over data residency and tailored HA architectures. Legacy enterprise software stacks tightly integrated with on-premise databases, anchoring spending even as public clouds mature. Cloud deployments, nonetheless, have advanced as digital-native firms adopted managed services to avoid infrastructure administration.

Edge and embedded deployments displayed a 23.2% CAGR outlook, fueled by connected cars and IIoT gateways. Modern vehicles generate around 300 TB annually, which demands in-vehicle processing for autonomous features. TDengine achieved 10X compression over Elasticsearch in smart-vehicle telemetry, cutting bandwidth for upstream transfers. Manufacturers applied similar strategies on production lines to detect defects instantly. The shift signaled that performance gains once reserved for data centers were now indispensable at the edge, expanding the In-Memory Database market footprint.

In-Memory Database Market is Segmented by Processing Type (OLTP, OLAP, and HTAP), Deployment Mode (On-Premise, and More), Data Model (SQL, Nosql, and Multi-Model), Organization Size (SMEs, and Large Enterprises), Application (Real-Time Transaction Processing, and More), End-User Industry (BFSI, Telecommunications and IT, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific recorded the largest regional revenue at 32.2% in 2024 and maintained a 17.1% CAGR outlook. National Industry 4.0 programs in China, Japan, and India spurred factory automation that required in-memory historian databases for sub-second MES feedback loops. General Motors linked more than 100,000 operational technology connections in its MES 4.0 rollout, illustrating the scale of edge deployments. Local vendors such as Nautilus Technologies' advanced indigenous relational engines, reducing reliance on foreign IP.

North America formed a mature but innovation-rich market centered on financial services, hyperscale clouds, and autonomous-vehicle R&D. Oracle and Google deepened their partnership to run Oracle Database services natively on Google Cloud, marrying enterprise SQL capabilities with AI accelerators. The region's venture funding supported emerging players such as Dragonfly, intensifying competitive churn.

Europe prioritized data-sovereignty compliance under GDPR, driving hybrid cloud adoption and favoring on-premise clusters combined with managed services in local data centers. Oracle expanded Database@Azure coverage to additional EU regions to satisfy residency rules. The continent also saw healthcare deployments of HTAP databases to power AI diagnostics under strict privacy frameworks.

The Middle East and Africa invested in smart-city fiber and 5G backbones, leading to pilot IIoT deployments that require real-time analytics. South America gained traction in mining operations and digital banking, where low-latency fraud detection justified premium memory-centric systems. Though absolute spend in these two regions remained modest, double-digit growth expanded the In-Memory Database market's global diversity.

- SAP SE

- Oracle Corp.

- Microsoft Corp.

- IBM Corp.

- Redis Ltd. (Redis Enterprise)

- Aerospike Inc.

- VoltDB Inc.

- Couchbase Inc.

- DataStax Inc.

- Hazelcast Inc.

- MemVerge Inc.

- Altibase Corp.

- GridGain Systems Inc.

- Raima Inc.

- McObject LLC

- Pivotal (VMware Tanzu GemFire)

- Amazon Web Services (Amazon ElastiCache & MemoryDB)

- Google Cloud (AlloyDB, Memorystore)

- Alibaba Cloud (ApsaraDB Tair)

- Huawei Cloud (GaussDB IM)

- Tencent Cloud (Tendis)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native micro-services demanding sub-millisecond latency

- 4.2.2 Falling DRAM and persistent-memory USD/GB widening TCO gap vs. disk

- 4.2.3 Streaming analytics adoption in BFSI and telecom for fraud and network QoS

- 4.2.4 HTAP architectures accelerating AI/ML model-serving in healthcare

- 4.2.5 Edge-compute use-cases (connected vehicles, IIoT) requiring embedded IMDB

- 4.3 Market Restraints

- 4.3.1 Vendor lock-in concerns around proprietary in-memory formats

- 4.3.2 High-availability design complexity for >40 TB clusters

- 4.3.3 Data-sovereignty laws (e.g., China CSL, EU GDPR) limiting global replication

- 4.4 Value Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of macroeconomoic factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Processing Type

- 5.1.1 OLTP

- 5.1.2 OLAP

- 5.1.3 Hybrid Transactional/Analytical Processing (HTAP)

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Edge/Embedded

- 5.3 By Data Model

- 5.3.1 Relational (SQL)

- 5.3.2 NoSQL (Key-Value, Document, Graph)

- 5.3.3 Multi-model

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Application

- 5.5.1 Real-time Transaction Processing

- 5.5.2 Operational Analytics and BI Dashboards

- 5.5.3 AI/ML Model Serving

- 5.5.4 Caching and Session Stores

- 5.6 By End-user Industry

- 5.6.1 BFSI

- 5.6.2 Telecommunications and IT

- 5.6.3 Retail and E-commerce

- 5.6.4 Healthcare and Life Sciences

- 5.6.5 Manufacturing and Industrial IoT

- 5.6.6 Media and Entertainment

- 5.6.7 Government and Defense

- 5.6.8 Others (Energy, Education, etc.)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 France

- 5.7.2.3 United Kingdom

- 5.7.2.4 Nordics

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Taiwan

- 5.7.3.3 South Korea

- 5.7.3.4 Japan

- 5.7.3.5 India

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Mexico

- 5.7.4.3 Argentina

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corp.

- 6.4.3 Microsoft Corp.

- 6.4.4 IBM Corp.

- 6.4.5 Redis Ltd. (Redis Enterprise)

- 6.4.6 Aerospike Inc.

- 6.4.7 VoltDB Inc.

- 6.4.8 Couchbase Inc.

- 6.4.9 DataStax Inc.

- 6.4.10 Hazelcast Inc.

- 6.4.11 MemVerge Inc.

- 6.4.12 Altibase Corp.

- 6.4.13 GridGain Systems Inc.

- 6.4.14 Raima Inc.

- 6.4.15 McObject LLC

- 6.4.16 Pivotal (VMware Tanzu GemFire)

- 6.4.17 Amazon Web Services (Amazon ElastiCache & MemoryDB)

- 6.4.18 Google Cloud (AlloyDB, Memorystore)

- 6.4.19 Alibaba Cloud (ApsaraDB Tair)

- 6.4.20 Huawei Cloud (GaussDB IM)

- 6.4.21 Tencent Cloud (Tendis)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment