|

시장보고서

상품코드

1851711

인력 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Workforce Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

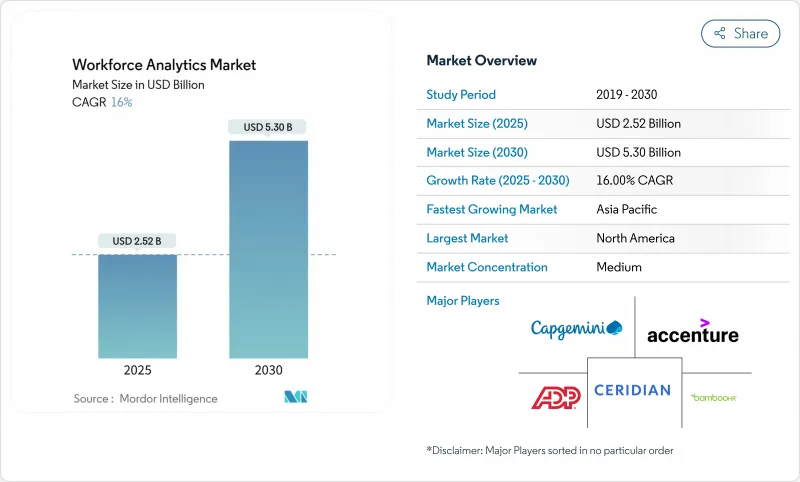

인력 분석 시장은 2025년에 25억 2,000만 달러로 평가되었고 CAGR은 16.0%를 나타낼 것으로 예측되며 2030년에는 53억 달러에 달할 전망입니다.

성장은 조직들이 데이터 기반 인재 결정, 하이브리드 업무 최적화, AI 기반 분석으로 빠르게 전환함에 따라 발생합니다. 예측 계획, 실시간 인사이트, 비용 최적화에 대한 집중도가 높아지면서 신중한 경제 환경 속에서도 수요는 견조하게 유지됩니다. 클라우드 기반 전개는 HCM 제품군과의 통합으로 데이터 양이 증가하고 활용 사례가 확대되면서 빠르게 확산되며, 의료 및 제조업 분야의 특정 요구사항이 도입을 가속화합니다. 지역별 동향은 주목할 만합니다. 북미가 초기 기업 도입을 주도하지만, 아시아태평양 지역의 디지털 전환 프로그램이 가장 빠른 확장 경로를 창출합니다. HCM 플랫폼 선도 기업들이 분석 기능을 핵심 서비스에 통합하고, 순수 플레이 벤더들이 규모 확대를 위해 전략적 자금 조달, 인수합병, 파트너십을 추구함에 따라 경쟁 역학은 적정 수준의 강도를 유지합니다.

세계의 인력 분석 시장 동향 및 인사이트

AI를 활용한 예측 분석이 인력 의사결정 변화

기업의 머신러닝 모델 도입으로 HR 팀은 인재 격차를 예측하고, 배치를 최적화하며, 유지율을 높일 수 있습니다. 분류 체계와 수동 평가를 구축하는 존슨앤드존슨의 AI 기술 추론 프레임워크는 학습 연계성과 채용 정확도를 개선했습니다. 제조업은 시급성을 보여줍니다. 공장 중 42%가 향후 5년 내 AI/ML 활용을 확대할 계획이며, 50%는 내년에 품질 관리 AI를 도입할 예정입니다. 관리자의 역할 변화: 70%가 인력 변혁을 성과에 핵심적 요소로 인식합니다. 이러한 요소들이 종합적으로 인력 분석 시장 전반에 걸쳐 기업 수요를 촉진합니다.

클라우드 HCM 통합은 데이터 확산 및 분석 구축을 촉진

Oracle Fusion HCM Analytics 및 SAP SuccessFactors Workforce Analytics와 같은 클라우드 HCM 제품군은 구성, 보상, 기술에 대한 실시간 지표를 제공하여 HR 리더가 역량을 비즈니스 목표에 부합하도록 지원합니다. 원 모델(One Model)과 같은 통합 플랫폼은 다중 HCM 소스의 데이터를 표준화하고 이직률 및 임금 평등성에 대한 예측 인사이트으로 보강합니다. 지방자치단체의 도입 사례는 규모를 보여줍니다. 로스앤젤레스시는 5만 명의 직원을 위해 워크데이(Workday)를 운영하며, AI가 이력서 심사 및 기술 태깅을 안내합니다. 따라서 클라우드의 보편화는 인력 분석 시장 전반에 걸쳐 사용 사례의 양을 가속화합니다.

데이터 프라이버시와 규정 준수 복잡성이 시장 성장 억제

2024년 8월 발효 예정인 EU AI 법안은 다수 HR-AI 애플리케이션을 고위험으로 지정하여 위험 평가와 투명성을 요구합니다. 기업이 대규모 언어 모델을 통합함에 따라 GDPR 의무는 심화되어 설명 가능한 AI와 프라이버시 바이 디자인(Privacy-by-Design) 워크플로우를 의무화합니다. 북미에서는 CCPA 및 주 AI 법규로 인해 HR 관리자의 42%가 규정 준수에 대해 불확실해합니다. 이러한 중복된 의무는 의사 결정 주기를 늦추고 인력 분석 시장의 총소유비용(TCO)을 높입니다.

부문 분석

솔루션은 2024년 인력 분석 시장의 65.3%를 차지했으며, 이는 예측 알고리즘을 내장한 종합 플랫폼에 대한 광범위한 수요를 반영합니다. 인재 확보 및 개발 최적화 솔루션은 기업들이 기술 격차를 메우면서 강력한 성장세를 보이고 있습니다. 헌팅턴 잉걸스 인더스트리즈는 AI 네이티브 도구 도입으로 채용 속도를 25% 단축하고 유지율을 30% 높였습니다. 성과 및 참여도 분석 시장도 확대되고 있으며, 엘카미노 헬스는 간호사 이직률을 7% 포인트 감소시켜 연간 84만 달러를 절감했습니다. 서비스 부문은 규모는 작지만 기업들이 구현, 관리형 서비스 및 교육 지원을 확보함에 따라 연평균 17.2%의 성장률을 기록하고 있습니다. 전문 서비스는 복잡한 데이터 마이그레이션을 지원하며, 관리형 서비스는 HR 팀이 전략에 집중할 수 있게 합니다. 비지어(Visier)의 'Vee'와 같은 생성형 AI 어시스턴트 도입은 경쟁 차별화를 강화하고 솔루션 성장을 지속시킵니다.

교육 및 지원에 대한 관심이 높아지고 있습니다. 제조업체의 31%가 분석 이니셔티브 실현을 위한 역량 강화 필요성을 언급했습니다. 학습 및 변화 관리 모듈을 묶어 제공하는 업체들은 인력 분석 시장 내에서 점유율을 점차 확대하고 있습니다.

클라우드 플랫폼은 2024년 59.2% 점유율을 기록했으며, 기업들이 초기 비용 절감과 원활한 업그레이드를 추구함에 따라 연평균 16.5% 성장할 전망입니다. 원 모델(One Model)은 워크데이(Workday)와 SAP 성공 팩터스(SuccessFactors)의 데이터를 분석 준비 완료 프레임워크로 추상화하여 가치를 입증합니다. 로스앤젤레스 같은 대규모 공공 부문 고객사는 클라우드 스택에서 수만 명의 직원을 관리할 때 확장성과 보안성을 보여줍니다.

데이터 주권이 요구되는 분야, 특히 BFSI(금융 서비스) 및 국방 분야에서는 온프레미스 방식이 여전히 유효합니다. 민감한 데이터는 로컬에 저장하고 분석 컴퓨팅은 클라우드에서 실행하는 하이브리드 전개 방식이 절충안으로 부상하고 있습니다. 공급업체들은 암호화 및 권한 모델을 강화하고 있습니다. SAP와 Oracle 모두 역할 기반 제어 및 규정 준수 인증 기능을 추가했습니다. 따라서 인력 분석 시장은 로컬 모델을 포기하지 않으면서도 결정적으로 클라우드로 기울고 있습니다.

지역 분석

북미는 2024년 인력 분석 시장의 25.6%를 차지했으며, 세분화된 인력 지표 도입을 촉진하는 SEC 공시 의무가 이를 뒷받침했습니다. 로스앤젤레스시는 Workday의 AI 기능을 통해 5만 명의 직원 채용 및 급여 처리를 자동화하여 처리 시간을 획기적으로 단축함으로써 선진적인 성숙도를 보여주고 있습니다. 캐나다는 공공 부문 디지털화를 활용하는 반면, 멕시코는 근거리 아웃소싱을 통해 제조업 인사 프로그램에 분석을 통합하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 16.3%의 가장 빠른 성장률을 보일 전망입니다. 인도의 타타 스틸 칼링가나가르 공장은 130명의 직원을 분석 기술로 교육하고 적중률을 60%에서 90%로 높여 연간 400만 달러를 절감했습니다. 중국은 자동화와 근로자 재교육을 연계하기 위해 적극적으로 투자하는 반면, 일본과 한국은 분석 기술을 고령화 인력 전략과 결합하고 있습니다. 호주와 뉴질랜드는 비수도권 지역에서 2년 이상 근무하는 의료 전문가가 41%에 불과한 현실을 해결하기 위해 분석 기술을 적용하고 있습니다.

유럽은 GDPR과 AI 법안의 영향으로 꾸준히 성장 중입니다. 두 법안 모두 투명한 알고리즘과 인간의 감독을 요구합니다. 독일, 영국, 프랑스가 대규모로 도입 중이며, 프랑스 스타트업들은 비지어(Visier)와 르 랩 RH(Le Lab RH)의 협업으로 혜택을 보고 있습니다. 네덜란드는 다국적 기업들 사이에서 강력한 도입세를 보이고 있는 반면, 남유럽은 제한된 분석 인재 공급으로 인해 뒤처지고 있습니다. 중동과 아프리카는 초기 단계의 기회를 구성합니다. UAE와 사우디아라비아는 비전 2030 프로그램에 분석을 접목하고 있으며, 남아프리카 공화국은 기술 매핑에 초점을 맞춘 공공 부문 시범 사업을 시작합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이브리드 업무 환경에서 데이터 기반 인재 의사 결정에 대한 수요 증가

- 클라우드 HCM 스위트에 의한 인사 데이터 확산

- 예측적 인적 분석을 위한 AI/ML 도입

- 경제적 불확실성 속 인력 비용 최적화

- 역량 매핑이 필요한 기술 기반 인재 시장으로의 전환

- ESG 및 다양성 보고 의무화로 인한 분석 도입 가속화

- 시장 성장 억제요인

- 데이터 개인정보 보호 및 규정 준수 복잡성 (GDPR, CCPA, AI 법안)

- 높은 구현 비용 및 변화 관리 부담

- AI 기반 분석의 알고리즘 편향 및 윤리적 우려

- 긱/유연근무 생태계의 분산된 데이터 사일로

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 컴포넌트 유형별

- 솔루션

- 인재 확보 및 개발 최적화

- 급여 및 인력 모니터링

- 성능 및 참여 분석

- 이직률 및 유지율 분석

- 위험 및 규정 준수 분석

- 서비스

- 전문 서비스

- 관리형 서비스

- 교육 및 지원 서비스

- 솔루션

- 전개 유형별

- 클라우드

- 온프레미스

- 조직 규모별

- 대기업

- 중소기업(SME)

- 최종 사용자 업계별

- 은행, 금융서비스 및 보험(BFSI)

- 제조업

- IT 및 통신

- 헬스케어 및 생명과학

- 소매 및 전자상거래

- 정부 및 공공 부문

- 에너지 및 유틸리티

- 운송 및 물류

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Accenture plc

- ADP, Inc.

- BambooHR LLC

- Capgemini SE

- Ceridian HCM Holding Inc.

- ChartHop, Inc.

- Cisco Systems, Inc.

- CultureAmp Pty Ltd

- Darwinbox Digital Solutions Pvt. Ltd.

- Eightfold AI, Inc.

- Gusto, Inc.

- IBM Corporation

- Infor, Inc.

- Kronos-UKG, Inc.

- Lattice, Inc.

- Microsoft Corp.(Viva Insights)

- Namely, Inc.

- Oracle Corporation

- Peoplestreme Pty Ltd(Ascender)

- SAP SE

- Skillsoft Corp.(SumTotal Systems)

- Tableau Software LLC

- Visier, Inc.

- Workday, Inc.

- Zoho Corporation(Zoho People Analytics)

제7장 시장 기회와 장래의 전망

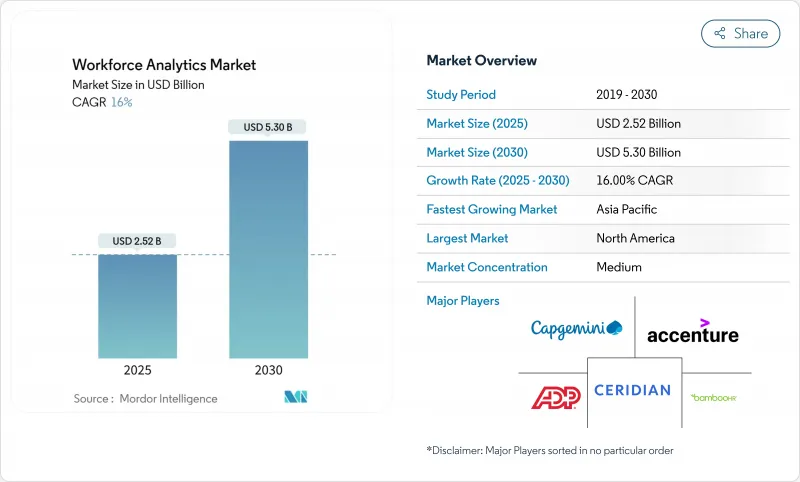

HBR 25.11.17The workforce analytics market reached USD 2.52 billion in 2025 and is forecast to advance at a 16.0% CAGR, taking the total to USD 5.30 billion by 2030.

Growth stems from organizations moving rapidly toward data-driven talent decisions, hybrid-work optimization, and AI-powered analytics. Heightened focus on predictive planning, real-time insights, and cost optimization keeps demand robust even in cautious economic climates. Cloud-based deployments expand quickly as integration with HCM suites multiplies data volumes and unlocks use cases, while sector-specific needs in healthcare and manufacturing accelerate adoption. Regional momentum is striking: North America commands early enterprise uptake, yet Asia-Pacific's digital transformation programs create the fastest expansion path. Competitive dynamics stay moderately intense as HCM platform leaders fold analytics into core offerings and pure-play vendors pursue strategic funding rounds, acquisitions, and partnerships to build scale.

Global Workforce Analytics Market Trends and Insights

AI-Powered Predictive Analytics Transforms Workforce Decision-Making

Enterprise adoption of machine-learning models allows HR teams to predict talent gaps, refine allocation, and lift retention. Johnson & Johnson's AI skills-inference framework, which builds taxonomies and passive assessments, improved learning alignment and hiring accuracy. Manufacturing illustrates urgency: 42% of plants plan to raise AI/ML use within five years, with 50% deploying quality-control AI in the coming year. Managers shift roles as 70% view workforce transformation as critical to performance. These factors collectively stimulate enterprise demand across the workforce analytics market.

Cloud HCM Integration Drives Data Proliferation and Analytics Adoption

Cloud HCM suites such as Oracle Fusion HCM Analytics and SAP SuccessFactors Workforce Analytics offer real-time metrics on composition, compensation, and skills, empowering HR leaders to match capabilities to business goal. Integration platforms like One Model standardize data from multiple HCM sources and enrich it with predictive insights on attrition and pay equity. Municipal deployments highlight scale: the City of Los Angeles runs Workday for 50,000 staff, with AI guiding resume screening and skill tagging. Cloud ubiquity therefore accelerates use-case volume across the workforce analytics market.

Data Privacy and Regulatory Compliance Complexity Constrains Market Growth

The EU AI Act, effective August 2024, designates many HR-AI applications high-risk, demanding risk assessments and transparency. GDPR obligations deepen as firms integrate large language models, mandating explainable AI and privacy-by-design workflows. In North America, CCPA and state AI laws leave 42% of HR managers uncertain about compliance. These overlapping mandates slow decision cycles and elevate total cost of ownership for the workforce analytics market.

Other drivers and restraints analyzed in the detailed report include:

- Skills-Based Talent Marketplace Evolution Requires Advanced Capability Mapping

- Economic Uncertainty Accelerates Workforce Cost Optimization Strategies

- High Implementation Costs and Change Management Complexity Limit Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions represented 65.3% of the workforce analytics market in 2024, reflecting pervasive demand for comprehensive platforms that embed predictive algorithms. Talent acquisition and development optimization solutions enjoy strong momentum as enterprises fill skills gaps; Huntington Ingalls Industries recorded 25% faster hiring and 30% higher retention by deploying AI-native tools. Performance and engagement analytics also expand as El Camino Health reduced RN turnover by 7 points, saving USD 840,000 annually. Services, although smaller, post 17.2% CAGR as firms secure implementation, managed-service, and training support. Professional services guide complex data migrations, while managed services allow HR teams to focus on strategy. The introduction of generative AI assistants such as Visier's "Vee" sharpens competitive differentiation and sustains solution growth.

Training and support fetch mounting interest: 31% of manufacturers cite upskilling needs to realize analytics initiatives. Providers that bundle learning and change-management modules thereby capture incremental share within the workforce analytics market.

Cloud platforms held 59.2% share in 2024 and will grow at 16.5% CAGR as organizations chase lower upfront costs and seamless upgrades. One Model proves value by abstracting data from Workday and SAP SuccessFactors into analytics-ready frameworks. Large public-sector clients such as Los Angeles showcase scale and security when managing tens of thousands of employees on cloud stacks.

On-premises retains relevance where data sovereignty dictates, especially in BFSI and defense. Hybrid deployment emerges as a compromise, storing sensitive data locally while running analytics compute in the cloud. Vendors strengthen encryption and permission models: SAP and Oracle both add role-based controls and compliance attestations. The workforce analytics market therefore skewers decisively toward cloud without abandoning localized models.

Workforce Analytics Market Report is Segmented by Component (Solutions, Services), Deployment Type (Cloud, On-Premises), Organization Size (Large Enterprises, Smes), End-User Industry (BFSI, Manufacturing, IT and Telecom, Healthcare, Retail, Government, Energy and Utilities and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

North America held 25.6% of the workforce analytics market in 2024, supported by SEC disclosure mandates that push granular workforce metrics. The City of Los Angeles demonstrates advanced maturity by automating hiring and payroll for 50,000 staff through Workday's AI features, lowering processing times materially. Canada capitalizes on public-sector digitization, while Mexico rides near-shoring to embed analytics in manufacturing HR programs.

Asia-Pacific shows the fastest 16.3% CAGR through 2030. India's Tata Steel Kalinganagar plant saved USD 4 million annually by training 130 staff in analytics and boosting strike rates from 60% to 90%. China invests aggressively to align automation and worker reskilling, while Japan and South Korea blend analytics with aging-workforce strategies. Australia and New Zealand apply analytics to retain healthcare professionals, where only 41% stay more than two years in non-metro areas.

Europe grows steadily on the back of GDPR and the AI Act, which both demand transparent algorithms and human oversight. Germany, the United Kingdom, and France implement at scale, with French start-ups benefiting from Visier and Le Lab RH collaboration. The Netherlands sees robust adoption among multinationals, whereas Southern Europe lags because of limited analytics talent supply. Middle East and Africa constitute early-stage opportunities: UAE and Saudi Arabia weave analytics into Vision 2030 programs, and South Africa begins public-sector pilots focused on skills mapping.

- Accenture plc

- ADP, Inc.

- BambooHR LLC

- Capgemini SE

- Ceridian HCM Holding Inc.

- ChartHop, Inc.

- Cisco Systems, Inc.

- CultureAmp Pty Ltd

- Darwinbox Digital Solutions Pvt. Ltd.

- Eightfold AI, Inc.

- Gusto, Inc.

- IBM Corporation

- Infor, Inc.

- Kronos-UKG, Inc.

- Lattice, Inc.

- Microsoft Corp. (Viva Insights)

- Namely, Inc.

- Oracle Corporation

- Peoplestreme Pty Ltd (Ascender)

- SAP SE

- Skillsoft Corp. (SumTotal Systems)

- Tableau Software LLC

- Visier, Inc.

- Workday, Inc.

- Zoho Corporation (Zoho People Analytics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing need for data-driven talent decisions in hybrid workplaces

- 4.2.2 Proliferation of HR data from cloud HCM suites

- 4.2.3 Adoption of AI/ML for predictive people analytics

- 4.2.4 Workforce cost-optimization amid economic uncertainty

- 4.2.5 Shift to skills-based talent marketplaces requiring capability mapping

- 4.2.6 ESG and diversity-reporting mandates accelerating analytics roll-outs

- 4.3 Market Restraints

- 4.3.1 Data-privacy and compliance complexity (GDPR, CCPA, AI Acts)

- 4.3.2 High implementation cost and change-management burden

- 4.3.3 Algorithmic-bias and ethics concerns in AI-driven analytics

- 4.3.4 Fragmented data silos in gig/flexible-work ecosystems

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component Type

- 5.1.1 Solutions

- 5.1.1.1 Talent Acquisition and Development Optimization

- 5.1.1.2 Payroll and Workforce Monitoring

- 5.1.1.3 Performance and Engagement Analytics

- 5.1.1.4 Turnover and Retention Analytics

- 5.1.1.5 Risk and Compliance Analytics

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.2.3 Training and Support Services

- 5.1.1 Solutions

- 5.2 By Deployment Type

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Manufacturing

- 5.4.3 IT and Telecom

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Retail and e-Commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Transportation and Logistics

- 5.4.9 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia_Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 ADP, Inc.

- 6.4.3 BambooHR LLC

- 6.4.4 Capgemini SE

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 ChartHop, Inc.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 CultureAmp Pty Ltd

- 6.4.9 Darwinbox Digital Solutions Pvt. Ltd.

- 6.4.10 Eightfold AI, Inc.

- 6.4.11 Gusto, Inc.

- 6.4.12 IBM Corporation

- 6.4.13 Infor, Inc.

- 6.4.14 Kronos-UKG, Inc.

- 6.4.15 Lattice, Inc.

- 6.4.16 Microsoft Corp. (Viva Insights)

- 6.4.17 Namely, Inc.

- 6.4.18 Oracle Corporation

- 6.4.19 Peoplestreme Pty Ltd (Ascender)

- 6.4.20 SAP SE

- 6.4.21 Skillsoft Corp. (SumTotal Systems)

- 6.4.22 Tableau Software LLC

- 6.4.23 Visier, Inc.

- 6.4.24 Workday, Inc.

- 6.4.25 Zoho Corporation (Zoho People Analytics)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment