|

시장보고서

상품코드

1851717

비구아니드(Biguanides) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Biguanides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

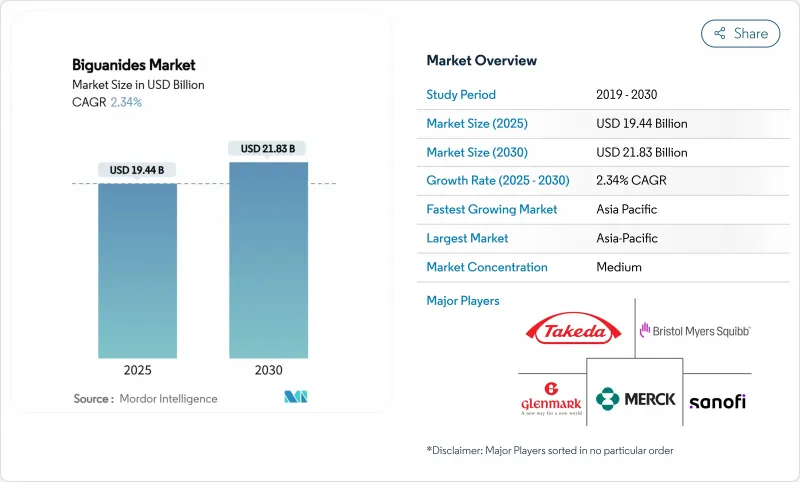

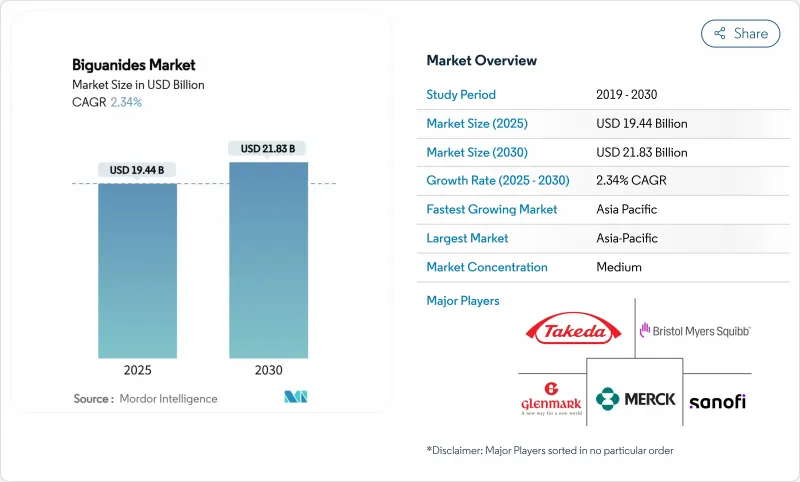

비구아니드 시장 규모는 2025년 194억 4,000만 달러로 추정되고, 2030년에는 218억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 CAGR 2.34%로 성장할 전망입니다.

2형 당뇨병의 제1선택제로서 메트포르민의 안정적인 수요가 수익의 기둥인 반면, 새로운 제형, 여성의 건강에 적응, 지역적인 접근의 확대가 성장을 가져옵니다. 아시아태평양은 대규모 당뇨병 인구와 활발한 제네릭 경쟁에 의해 판매량을 견인하고, 북미는 프리미엄 합제에 의해 가치를 유지하고 있습니다. NDMA(니트로소디메틸아민) 불순물을 포함한 규제 조치는 디지털 약국의 확대와 함께 공급의 탄력성과 유통 전략을 모두 형성하고 있습니다. 따라서 경쟁의 초점은 제조 품질, 가격 설정, 제제의 혁신이며 GLP-1 수용체 작용제와 SGLT-2 억제제에 대항하여 점유율을 지키고 패스트 라인 선택을 좌우하는 것입니다.

세계의 비구아니드 시장 동향 및 인사이트

2형 당뇨병(T2DM)의 세계 유병률 상승

2045년까지 7억 8,300만 명의 당뇨병 환자가 증가할 것으로 예상되고 있으며, 특히 이환율이 가장 상승한 아시아태평양에서 메트포르민 처방량이 유지되고 있습니다. 신흥 시장에서는 경쟁 제네릭 의약품이 진입 가격을 낮추고 있기 때문에 높은 처방수가 증가하고 있지만, 선진 시장에서는 혈당제어와 심혈관 베네핏을 양립시킨 프리미엄 합제가 선호되고 있습니다. 가이드라인에서 메트포르민이 제1선택약임을 재확인하고 병용요법이 기세를 늘리는 가운데도 기본적인 수요는 유지되고 있습니다. 따라서 제조업체는 이중 전략을 추구하고 있습니다. 즉, 비용에 민감한 의료 시스템용으로 대량 생산의 주력 정제를 지키고, 부유층용으로 부가가치가 높은 제형을 추진하는 것입니다. 당뇨병의 세계적인 확산에 따라, 비구아나이드계 약제 시장 확대는 각국 정부가 증대하는 헬스케어 비용에 직면하는 가운데, 예방 및 조기 개입 프로그램과의 관련성을 유지하고 있습니다.

대부분의 당뇨병 가이드라인에서 제1선택제로서 유리한 지위

2025년 당뇨병 가이드라인에서 메트포르민은 약물 치료의 첫 번째 선택 약물로 자리매김했으며, 이 위치는 지속적인 판매량의 안정성을 보장합니다. 같은 업데이트는 SGLT-2 억제제와 같은 애드온 약물의 조기 도입을 제창하고, 메트포르민을 포함한 2제 병용이나 3제 병용의 기회가 증가하고 있습니다. 예방적 접근법을 채택한 의료 시스템은 메트포르민의 임상적 유용성을 당뇨병 전증으로 확대하여 후보 환자를 늘리고 있습니다. 지역적 뉘앙스의 차이가 나타납니다. : 유럽에서는 비용 효과가 강조되고, 북미에서는 결과 기반의 증거가 중시되며, 신흥 시장에서는 최적화보다 저렴한 가격이 중요합니다. 전체적으로, 가이드라인의 무결성은 메트포르민 수요를 확보하는 것과 동시에, 배합비, 투여 편의성, 핵심적인 당뇨병 이외의 환자군에 관한 혁신을 제조업체에 촉구하고 있습니다.

처방 의사의 신뢰를 해치는 NDMA 불순물 리콜

2020년 이후 여러 메트포르민 배치에서 규제치를 초과하는 NDMA가 검출되어 테바사, 아포텍스사 등이 재고의 회수를 강요했습니다. 새로운 조사에 따르면, NDMA는 정제가 아질산염과 접촉할 때 생체 내에서 생성될 수 있어 안전성 모니터링이 강화되었습니다. 제조업체는 조립에 아스코르브산과 같은 산화 방지제를 채용해, 타이트 가스상 시험 프로토콜을 도입하는 것으로 대응했지만, 임상의의 경계심은 아직 남아 있습니다. 미국과 유럽의 규제 당국은 현재 시장 방출 전에 로트별 인증서를 요구하고 있으며 리드 타임을 늘리고 있습니다. 공급은 안정적이지만, 의식이 높아지면 대체 약물 클래스로의 전환을 가속화하고 컴플라이언스 비용을 상승시키기 때문에 비구아니드 시장은 당분간 완만하게 추이할 것으로 보입니다.

부문 분석

메트포르민은 2024년 비구아니드 시장 매출의 95.51%를 차지했으며, 비교할 수 없는 임상적 친근함과 저렴한 가격으로 이 클래스의 리더십을 지원하고 있습니다. 부포르민의 CAGR은 7.65%이며, 대사성 암 영역에서의 미충족 요구와 특정 지역의 승인에 의해 보다 작은 분자가 어떻게 점유율을 획득하고 있는지를 나타내고 있습니다. 펜포르민(Phenformin)은 역사적인 안전성의 철회에도 불구하고 항암 프로그램에서 다시 관심을 모으고 있으며, 보다 깊은 미토콘드리아로의 침투를 활용하여 살 종양 효과를 높이고 있습니다. 주요 공급업체는 메트포르민의 대량 생산을 계속하면서 이러한 이차 비구아니드에 소액을 투자하여 포트폴리오를 헤지하고 있습니다. 가격 책정의 유연성은 틈새 분자만큼 높지만 적응증의 범위가 제한되어 있기 때문에 절대 수익 가능성은 제한적입니다. 메트포르민의 점유율은 점차 낮아질 것입니다. 메트포르민과 관련된 비구아니드 시장 규모만이 여전히 150억 달러를 넘고 있으며, 이 분자의 구조적 중요성이 강조되고 있습니다.

2세대 분자는 생체이용률 최적화, 조직 특이적 AMPK 활성화의 표적화, 락테이트 산증의 위험 감소를 목표로 한 연구 자금을 모으고 있습니다. 유럽의 컨소시엄은 간세포암 예방을 위한 부포르민의 미량 투여를 연구하고 있으며, 일본 그룹은 체크포인트 억제제와 병용하여 펜포르민을 시험하고 있습니다. 규제 당국에 허용되는지 여부는 입증 가능한 안전 마진에 달려 있으며 초기 결과는 적절한 투여 관리에 의해 관리 가능한 프로파일을 시사합니다. 종양학의 임상시험에서 승인을 얻으면, 비싼 가격 설정에 의해 환자수의 감소가 상쇄되어, 비구아니드 시장에 신선하지만 일정한 톱 라인이 더해질 가능성이 있습니다.

즉각 방출 정제는 2024년에도 60.53%의 점유율을 유지했는데, 이는 처방 습관이 정착하고 있는 것과 밀리그램당 비용이 가장 낮기 때문입니다. 한편, 서방형 정제는 1일 1회 복용함으로써 복약 준수를 높이고 위장의 불쾌감을 최소화하기 때문에 CAGR 6.85%로 추이하고 있습니다. 독특한 친수성 매트릭스와 레이저 천공 삼투 펌프는 용출 제어를 유지하며 높은 단가와 더 긴 특허 기간을 요구합니다. 1,000mg의 고강도 제형은 정제의 부담을 줄이고 체중 과다 환자에서 체중 기반 투여 지침을 준수합니다. 서방 라인과 관련된 비구아니드 시장 규모는 2025년 51억 달러에서 2030년 71억 달러로 확대될 것으로 예측됩니다.

경구제는 마이너이지만, 정제를 삼킬 수 없는 소아나 노인층에 공헌하고 있습니다. 새로운 미각 마스킹 부형제와 소량 농축 제형은 더 많은 사람들에게 받아 들여지는 것을 목표로 합니다. 저자원 환경을 위해 조정된 가방 과립은 물 부족 문제를 피하고 농촌 클리닉에서의 복용을 단순화합니다. 용법 및 용량의 다양화에 의해 브랜드 아이덴티티가 강화되어 성숙하고 있는 치료제 카테고리에 있어서, 제조업체 각사는 가격 이상의 차별화를 도모할 수 있습니다.

지역 분석

아시아태평양은 2024년 매출의 35.62%를 차지했고, CAGR은 8.35%로 성장할 전망입니다. 이는 가격을 인하하면서도 판매량을 확대한 중국의 집중구매와 미치료의 당뇨병 환자가 방대하게 존재하는 인도가 견인하고 있습니다. 급속한 도시화 및 라이프스타일의 변화가 진단률을 높여 가격 규제 하에서도 처방의 성장을 확실히 하고 있습니다. 동남아시아 정부는 국민 모두 보험제도 안에서 메트포르민을 조성하고 있으며, 비싼 제제보다 저렴한 가격을 중시하고 있습니다.

북미에서는 정교한 급여자가 심근 경색에 효과적인 약물을 선호하고 사용하는 가치 중심 분야이지만 성장은 완만합니다. 메트포르민을 통합한 합제는 여전히 중요하지만, GLP-1 수용체 작용제는 점점 더 처방상의 우선순위를 증가시키고 있습니다. NDMA의 리콜 문제로 인해 병원 스튜어드십 프로그램이 가속화되어 공급업체에 대한 문서화 임계값이 증가했습니다. 판매량은 평평하지만 평균 판매 가격 상승으로 매출은 견조하게 추이하고 있습니다.

유럽에서는 기술 혁신의 도입과 예산 모니터링의 균형이 잡혀 있습니다. 각국의 의료제도는 수량 기준의 할인을 협상하고 있지만, 약제 경제모델이 합병증의 감소를 실증한 경우에는 서방정이나 배합정을 상환하고 있습니다. EMA가 승인한 주 1회 투여 인슐린 제형과 같은 환자 중심의 치료법은 치료 도구 상자를 강화하고 메트포르민을 포함한 병용 요법을 장려합니다.

중동 및 아프리카에서는 당뇨병 유병률이 상승하고 있지만 인프라는 다양합니다. 걸프 협력 회의 국가들은 고품질의 브랜드 의약품을 수입하고 있지만 사하라 이남 시장은 기증자 자금에 의한 제네릭 의약품에 의존하고 있습니다. 콜드체인의 갭이나 위조품의 만연에 의해 공급의 안전성에 과제가 남습니다.

브라질로 대표되는 남미에서는 SUS 제도 하에서 임신성 당뇨 프로토콜에서 메트포르민의 사용률이 상승하고 있습니다. 가격 통제는 금리를 제한하지만, 공공 조달은 엄청난 인구를 대상으로 하기 때문에 적합한 제조자에게는 수량이 확실합니다. 전반적으로 지역 불균일성으로 인해 기업은 패키징, 가격대 및 유통 물류를 조정해야 하며 지역 역풍에도 불구하고 전체 비구아니드 시장의 확대를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 2형 당뇨병(T2DM)의 세계적 유병률 상승

- 대부분의 당뇨병 가이드라인에서 제1선택약으로서의 지위

- 제네릭 의약품의 급속한 보급이 LMICs의 저가격화 촉진

- 여성의 건강(PCOS, GDM)에서 메트포르민 사용 증가

- 노화 방지 및 항암제로서의 비구아나이드의 탐색

- AI를 활용한 분자 재이용이 합제 가속

- 시장 성장 억제요인

- NDMA 불순물의 리콜이 처방자의 불신 초래

- 제1선택약으로서 GLP-1 Ras와 SGLT-2의 인기 상승

- 인도, 중국, 브라질의 가격 억제 정책이 마진 압박

- 전자상거래 채널에서 메트포르민의 규격 외품 및 위조품

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 분자별

- 메트포르민

- 펜포르민

- 부포르민

- 제형별

- 즉시 방출정

- 서방정

- 경구 솔루션

- 적응증별

- 2형 당뇨병

- 당뇨병 예비군

- 다낭성 난소 증후군(PCOS)

- 임신성 당뇨(GDM)

- 제제 유형별

- 단제요법

- 합제(FDC)

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Teva Pharmaceutical Industries

- Merck & Co.

- Takeda Pharmaceutical

- GSK plc

- Sanofi

- Boehringer Ingelheim

- Glenmark Pharma

- Zydus Lifesciences

- Bristol-Myers Squibb

- Sun Pharma

- Aurobindo Pharma

- Lupin Ltd.

- Ajanta Pharma

- Granules India

- Apotex

- IOL Chemicals & Pharma

- Sandoz AG

- Dr. Reddy's Laboratories

제7장 시장 기회 및 향후 전망

AJY 25.11.24The biguanides market size stood at USD 19.44 billion in 2025 and is forecast to reach USD 21.83 billion by 2030, advancing at a 2.34% CAGR over the period.

Steady demand for metformin as first-line therapy in type-2 diabetes anchors revenue, while incremental growth arises from newer dosage forms, women's health indications, and wider regional access. Asia-Pacific drives volume through large diabetic populations and vigorous generic competition, whereas North America sustains value through premium fixed-dose combinations. Regulatory actions that contain N-nitrosodimethylamine (NDMA) impurities, alongside digital pharmacy expansion, shape both supply resilience and distribution strategy. Competitive focus therefore rests on manufacturing quality, pricing agility, and formulation innovation to protect share against GLP-1 receptor agonists and SGLT-2 inhibitors that now influence first-line choices.

Global Biguanides Market Trends and Insights

Rising Global Prevalence of Type-2 Diabetes (T2DM)

The projected rise to 783 million diabetes cases by 2045 sustains prescription volumes for metformin, particularly in Asia-Pacific where incidence is climbing fastest. Emerging markets deliver high unit growth because competitive generics reduce entry price; developed markets prefer premium fixed-dose combinations that couple glycemic control with cardiovascular benefit. Guideline reaffirmation of metformin as first-line therapy sustains baseline demand even while combination therapy gains momentum. Manufacturers therefore pursue dual strategy: defend high-volume core tablets for cost-sensitive health systems and promote value-added formats in wealthier segments. The global footprint of diabetes ensures that biguanides market expansion remains linked to prevention and early intervention programs as governments confront mounting healthcare costs.

Favourable First-Line Therapy Status in Most Diabetes Guidelines

Diabetes guidelines for 2025 kept metformin at the center of initial pharmacologic treatment, a position that guarantees continued volume stability. The same updates advocate earlier introduction of add-on agents such as SGLT-2 inhibitors, increasing opportunities for dual and triple combinations that embed metformin. Health systems adopting preventive approaches extend metformin's clinical utility to prediabetes, enlarging its candidate pool. Regional nuances appear: Europe stresses cost-effectiveness, North America rewards outcome-based evidence, and emerging markets weigh affordability over optimization. Overall, guideline alignment secures metformin demand while encouraging manufacturers to innovate around combination ratios, dosing convenience, and patient groups beyond core diabetes.

NDMA Impurity Recalls Denting Prescriber Confidence

Successive recalls since 2020 exposed NDMA levels above regulatory limits in several metformin batches, forcing stock withdrawals from Teva, Apotex, and others. New research shows NDMA can form in-vivo when tablets encounter nitrites, intensifying safety scrutiny. Manufacturers responded by adopting antioxidants such as ascorbic acid in granulation and installing tighter gas-phase testing protocols, but clinician wariness lingers. U.S. and European regulators now require lot-specific certificates before market release, lengthening lead times. While supply has stabilized, heightened awareness accelerates switching to alternative drug classes and raises compliance costs, moderating the biguanides market trajectory in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Genericisation Driving Affordability in LMICs

- Increasing Use of Metformin in Women's Health (PCOS, GDM)

- Rising Popularity of GLP-1 RAs & SGLT-2s as First-Line Options

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metformin generated 95.51% of biguanides market revenue in 2024, underpinning class leadership through unmatched clinical familiarity and affordability. Buformin's 7.65% CAGR highlights how unmet needs in metabolic oncology and specific regional approvals allow smaller molecules to carve shares. Phenformin finds renewed interest in anticancer programs despite historic safety withdrawals, leveraging deeper mitochondrial penetration for enhanced tumoricidal effect. Major suppliers hedge portfolios by investing modest sums into these secondary biguanides while continuing high-volume metformin manufacture. Pricing flexibility is greater in niche molecules, but limited indication scope constrains absolute revenue potential. Observers expect metformin's share to taper gradually yet remain dominant throughout the forecast window as broader labels sustain prescriptions. The biguanides market size attached to metformin alone still exceeds USD 15 billion, underscoring the molecule's structural importance.

Second-generation molecules attract research funding aimed at optimizing bioavailability, targeting tissue-specific AMPK activation, and reducing lactic acidosis risk. European consortia explore buformin micro-dosing for hepatocellular carcinoma prevention, while Japanese groups test phenformin in combination with checkpoint inhibitors. Regulatory acceptance rests on demonstrable safety margins, and early results suggest manageable profiles with proper dosing controls. If oncology trials yield approval, premium pricing could offset smaller patient pools, contributing fresh but measured top-line additions to the biguanides market.

Immediate-release tablets retained a 60.53% share in 2024 owing to entrenched prescribing habits and the lowest cost per milligram. Extended-release tablets, though, are advancing at 6.85% CAGR as once-daily regimens boost adherence and minimize gastrointestinal discomfort. Proprietary hydrophilic matrices and laser-drilled osmotic pumps sustain controlled dissolution, commanding higher unit prices and lengthier patent life. High-strength 1,000 mg formats reduce pill burden and align with weight-based dosing guidelines in overweight populations. The biguanides market size tied to extended-release lines is projected to rise from USD 5.1 billion in 2025 to USD 7.1 billion by 2030.

Oral solutions, though minor, serve pediatric and geriatric segments unable to swallow tablets. Novel taste-masking excipients and small-volume concentrates aim to widen acceptance. Sachet granules tailored for low-resource settings bypass water scarcity issues and simplify dosing in rural clinics. Collectively, dosage-form diversification strengthens brand identity, allowing manufacturers to differentiate beyond price in a maturing therapeutic category.

The Biguanide Market Report is Segmented by Molecule (Metformin, Phenformin, and Buformin), Dosage Form (Immediate-Release Tablets, and More), Indication (Type-2 Diabetes Mellitus, Prediabetes, and More), Formulation Type (Monotherapy and Fixed-Dose Combinations), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 35.62% of 2024 revenue and is on track to deliver an 8.35% CAGR, driven by China's centralized procurement that cut prices yet expanded volume and India's vast untreated diabetic base. Rapid urbanization coupled with lifestyle shifts boosts diagnosis rates, ensuring prescription growth even under price caps. Southeast Asian governments subsidize metformin within universal coverage schemes, emphasizing affordability over premium formulations.

North America embodies a value-focused yet slower-growing arena where sophisticated payers favor agents offering cardiorenal benefit. Fixed-dose combinations that integrate metformin maintain relevance, but GLP-1 receptor agonists increasingly command formulary preference. NDMA recall fallout accelerated hospital stewardship programs, raising documentation thresholds for suppliers. Despite flat volumes, revenue holds steady owing to higher average selling prices.

Europe balances innovation adoption with budget oversight. National health systems negotiate volume-based discounts yet reimburse extended-release and combination tablets when pharmacoeconomic models demonstrate reduced complications. EMA approvals of patient-centric modalities such as weekly insulin augment the therapeutic toolbox and encourage combination regimens featuring metformin.

Middle East & Africa experience rising diabetes prevalence but variable infrastructure. Gulf Cooperation Council states import high-quality brands, while sub-Saharan markets rely on donor-financed generics. Supply security challenges persist due to cold-chain gaps and counterfeit penetration.

South America, led by Brazil, witnesses rising metformin uptake in gestational diabetes protocols under the SUS system. Price controls limit margins, but public procurement covers vast populations, offering volume certainty for compliant manufacturers. Collectively, regional heterogeneity obliges companies to tailor packaging, price tiers, and distribution logistics, sustaining overall biguanides market expansion despite localized headwinds.

- Teva Pharmaceutical Industries

- Merck

- Takeda Pharmaceuticals

- GlaxoSmithKline

- Sanofi

- Boehringer Ingelheim

- Glenmark Pharma

- Zydus Lifesciences

- Bristol-Myers Squibb

- Sun Pharmaceuticals Industries

- Aurobindo Pharma

- Lupin

- Ajanta Pharma

- Granules India

- Apotex

- IOL Chemicals & Pharma

- Sandoz Group

- Dr. Reddy's Laboratories

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Prevalence Of Type-2 Diabetes (T2DM)

- 4.2.2 Favourable First-Line Therapy Status In Most Diabetes Guidelines

- 4.2.3 Rapid Genericisation Driving Affordability In LMICs

- 4.2.4 Increasing Use of Metformin In Women's Health (PCOS, GDM)

- 4.2.5 Exploration of Biguanides As Geroprotective & Anti-Cancer Agents

- 4.2.6 AI-Enabled Molecule Repurposing Accelerating Fixed-Dose Combos

- 4.3 Market Restraints

- 4.3.1 NDMA Impurity Recalls Denting Prescriber Confidence

- 4.3.2 Rising Popularity Of GLP-1 Ras & SGLT-2s As First-Line Options

- 4.3.3 Price-Control Policies In India, China And Brazil Compressing Margins

- 4.3.4 Sub-Standard / Counterfeit Metformin In E-Commerce Channels

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Molecule

- 5.1.1 Metformin

- 5.1.2 Phenformin

- 5.1.3 Buformin

- 5.2 By Dosage Form

- 5.2.1 Immediate-Release Tablets

- 5.2.2 Extended-Release Tablets

- 5.2.3 Oral Solution

- 5.3 By Indication

- 5.3.1 Type-2 Diabetes Mellitus

- 5.3.2 Prediabetes

- 5.3.3 Polycystic Ovary Syndrome (PCOS)

- 5.3.4 Gestational Diabetes Mellitus (GDM)

- 5.4 By Formulation Type

- 5.4.1 Monotherapy

- 5.4.2 Fixed-Dose Combinations (FDCs)

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Teva Pharmaceutical Industries

- 6.3.2 Merck & Co.

- 6.3.3 Takeda Pharmaceutical

- 6.3.4 GSK plc

- 6.3.5 Sanofi

- 6.3.6 Boehringer Ingelheim

- 6.3.7 Glenmark Pharma

- 6.3.8 Zydus Lifesciences

- 6.3.9 Bristol-Myers Squibb

- 6.3.10 Sun Pharma

- 6.3.11 Aurobindo Pharma

- 6.3.12 Lupin Ltd.

- 6.3.13 Ajanta Pharma

- 6.3.14 Granules India

- 6.3.15 Apotex

- 6.3.16 IOL Chemicals & Pharma

- 6.3.17 Sandoz AG

- 6.3.18 Dr. Reddy's Laboratories

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment