|

시장보고서

상품코드

1851745

모바일 인공지능(AI) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Mobile Artificial Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

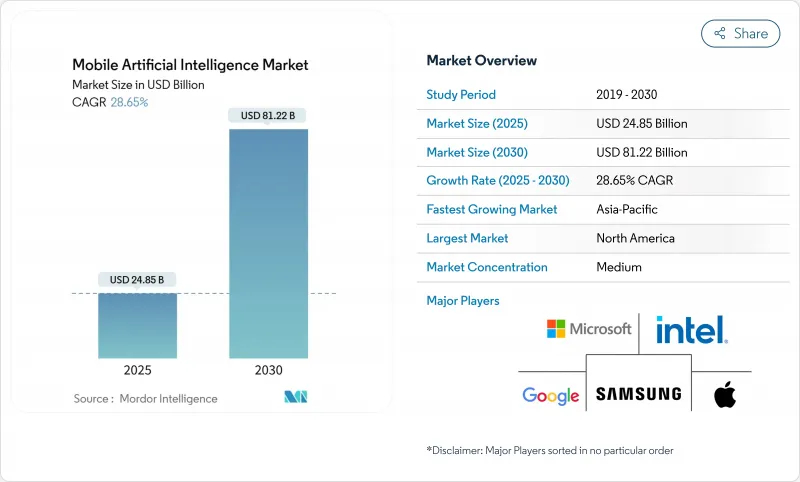

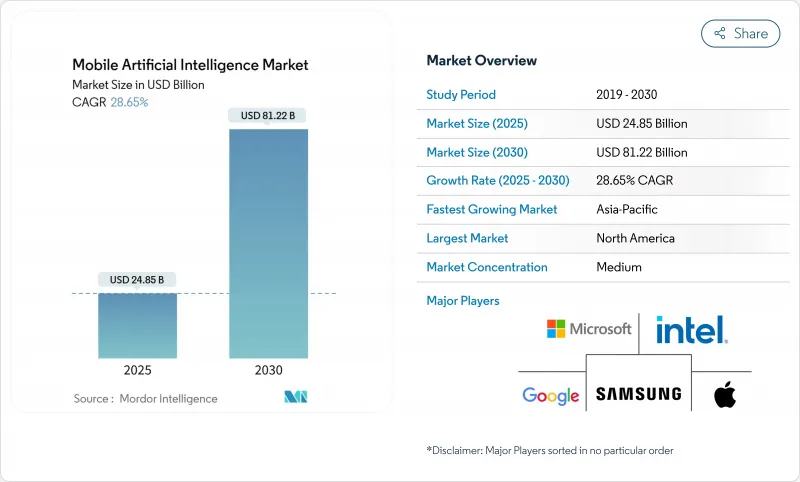

모바일 인공지능(AI) 시장 규모는 2025년에 248억 5,000만 달러로 평가되었고, 예측 기간 중(2025-2030년) CAGR은 28.65%를 나타낼 것으로 예측되며, 2030년에 812억 2,000만 달러에 달할 전망입니다.

데이터 주권에 대한 규제 강화, 신경망 처리 장치(NPU)의 급속한 혁신, 저지연 추론에 대한 기업 수요가 주요 성장 촉매제입니다. 퀄컴의 스냅드래곤 8 엘리트와 ARM의 코어텍스-X925 같은 획기적인 칩 설계는 스마트폰, 차량, 산업용 기기의 성능 기준을 재설정하고 있습니다. 공급업체 전략은 이제 시장 출시 기간을 단축하고 차별화된 온디바이스 AI 기능을 가능하게 하는 수직 통합형 하드웨어-소프트웨어 스택을 강조합니다. 첨단 기판 및 고대역폭 메모리의 공급망 제약은 가격과 가용성에 계속 영향을 미치고 있지만, 아시아태평양 지역의 확고한 생산 능력 확장은 2026년 이후 완화될 것임을 시사합니다.

세계의 모바일 인공지능(AI) 시장 동향 및 인사이트

AI 지원 프로세서 수요 급증

전례 없는 AI 중심 칩셋 채택이 기기 아키텍처를 재편하고 있습니다. ARM의 3nm 코어텍스-X925는 3.8GHz에서 기존 코어 대비 46% 향상된 처리량을 제공하면서도 프리미엄 스마트폰에 적합한 전력 상한선을 유지합니다. 퀄컴과 엔비디아처럼 장기적인 파운드리 할당을 확보한 제조사들은 공급 리스크를 완화하고 경쟁력 있는 비용 구조를 확보합니다. 삼성 갤럭시 S25는 NPU 성능이 40% 향상되었음을 보여주며, 성능 마케팅이 일반적인 CPU 지표에서 지속적인 AI 추론 능력으로 전환되었음을 강조합니다. 칩 수요는 또한 휴대용 폼 팩터에서 25와트 소모를 지원하는 고체 냉각 기술 혁신을 주도하고 있습니다. 이로 인한 성능 여유는 이전에는 클라우드 서비스에 의존했던 대화형 인터페이스, 실시간 비전, 온디바이스 분석을 가속화합니다.

생성형 AI 스마트폰 출시

생성형 AI는 플래그십 독점 기술에서 대중 시장으로 확산 중입니다. 캐널리스는 2028년까지 글로벌 핸드셋 출하량의 54%가 AI 지원 기능을 갖출 것으로 전망하며, 이는 과거 LTE 전환과 유사한 가파른 보급 곡선을 보여줍니다. 애플의 뉴럴 엔진은 이제 메시징을 위한 기기 내 컨텍스트 모델링을 수행하며, 삼성 갤럭시 AI는 실시간 번역 및 콘텐츠 초안 작성을 제공합니다. 인도의 가격 민감도는 도입 장벽을 보여줍니다. 600달러 미만 기기는 2024년 출하량의 4-5%에 불과해 초기 AI 보급을 제한합니다. 이를 해소하기 위해 미디어텍은 중급형 핸드셋에 최적화된 통합 NPU를 탑재한 디멘시티 9400을 출시했습니다. 기업용 플릿도 물량 증가를 주도하며, OPPO는 구글 및 마이크로소프트와의 협력을 통해 5천만 대에 생성형 AI 기능을 탑재하겠다고 약속했습니다.

AI 칩셋 프리미엄 가격

입문형 AI 스마트폰도 여전히 600달러 근처에서 출시되어 고성장 대량 시장의 보급을 제한하고 있습니다. 마이크론과 SK하이닉스의 생산 능력이 2025년까지 예약 완료된 상태라 고대역폭 메모리 부족 현상이 지속되며, 이로 인해 부품 원가(BOM)가 계속 높은 수준을 유지하고 있습니다. TSMC의 CoWoS(Chip-on-Wafer-on-Substrate) 라인 주변의 패키징 병목 현상은 모바일 기기 제조사에 추가적인 비용 압박을 가중시키고 있습니다. 벤더들은 기능 세분화로 대응 중 : 핵심 AI 기능은 기존 실리콘의 소프트웨어 최적화로 구현하고, 프리미엄 모델에만 고급 NPU 가속 기능을 추가합니다. 2026년 이후 대만과 일본에서 가동 예정인 신규 팹이 AI 칩셋과 비-AI 칩셋 간 가격 격차를 점진적으로 줄일 전망입니다.

부문 분석

스마트폰은 2024년 매출의 56%를 차지했으나, 대화형 차량 내 어시스턴트 및 자율 주행 기능이 고급 옵션에서 주류 기능으로 전환되면서 자동차 애플리케이션은 2030년까지 연평균 29.40%의 성장률을 기록할 전망입니다. 레벨 3 고속도로 자율 주행 기능이 프리미엄 모델의 표준 장비로 자리 잡으면 자동차 시스템용 모바일 인공지능(AI) 시장 규모가 급속히 확대될 전망입니다. 사운드하운드-텐센트 같은 파트너십은 다국어 음성 제어 기술이 기존 인포테인먼트 스택과 통합 가능함을 입증합니다. 카메라 앱은 야간 모드 및 노이즈 제거 파이프라인에 AI를 지속적으로 도입 중이며, 드론은 GNSS 신호가 차단된 구역에서 장애물 회피를 위해 엣지 추론 기술을 활용합니다.

차량 내 AI의 고성장은 전자 제어 장치(ECU)의 구조적 변화를 반영하며, AI가 이제 인식, 의도 예측, 맞춤형 사용자 경험을 주도합니다. 메르세데스-벤츠는 CARIAD 플랫폼을 통해 대규모 언어 모델을 통합하여 운전자의 습관을 학습하고 서비스 일정을 능동적으로 관리합니다. 산업용 로봇과 의료용 웨어러블은 추가적인 고부가가치 틈새 시장을 대표하며, 모바일 인공지능(AI) 시장이 소비자 메시징을 넘어 임무 핵심 영역으로 확대되고 있음을 보여줍니다.

하드웨어는 NPU, GPU, 밀리미터파 센서가 다양한 기기에 탑재되며 2024년 지출의 64%를 차지했습니다. 그럼에도 기업들이 모델 훈련, 미세 조정, 수명 주기 관리를 아웃소싱함에 따라 서비스 매출은 연평균 27.00% 성장할 전망입니다. 버라이즌과 SK통신의 관리형 서비스는 클라우드 GPU, 엣지 노드, 오케스트레이션 소프트웨어를 묶어 기업들이 선행 자본 지출 없이 AI 기능을 추가할 수 있게 합니다. ARM의 Kleidi와 같은 소프트웨어 라이브러리는 일반 CPU에서 N차원 텐서 연산을 가속화하여 설치된 실리콘의 활용도를 높입니다.

센서 진화는 로컬에서 1차 AI를 실행하는 마이크로 컨트롤러를 내장함으로써 하드웨어-소프트웨어 경계를 더욱 모호하게 만듭니다. 이로 인한 데이터 경제는 분석, 업데이트, 규정 준수 서비스에 대한 반복 수익을 창출하며, 플랫폼 모델이 모바일 인공지능(AI) 시장을 어떻게 재편하는지 입증합니다.

모바일 인공지능(AI) 시장 보고서는 용도(스마트폰, 카메라, 드론, 로봇, 자동차, 기타 용도), 컴포넌트(하드웨어, 소프트웨어, 서비스), 기술(CPU, GPU, NP U/AI 가속기, DSP), 처리 유형(온 디바이스/엣지, 클라우드 기반, 하이브리드), 최종 사용자 산업(소비자 가전, 자동차와 모빌리티, 산업과 제조업 등), 지역별로 구분됩니다.

지역 분석

북미는 2024년 매출 점유율 35%를 차지했으며, 기업들이 사내 AI 워크로드를 호스팅하기 위해 프라이빗 5G 및 엣지 노드를 신속히 구축했기 때문입니다. OpenAI의 400억 달러 자금 조달을 포함한 대규모 투자 라운드는 기초 모델 연구 및 상용화 분야에서 해당 지역의 리더십을 강화합니다. 정부 보조금과 국방 계약은 엄격한 규정 준수 기준을 충족하는 안전한 온 디바이스 솔루션에 대한 수요를 더욱 촉진합니다.

아시아태평양 지역은 2030년까지 연평균 복합 성장률(CAGR) 24.80%로 가장 빠르게 성장하는 지역으로, 소프트뱅크의 9억 6천만 달러 인프라 계획과 SK 그룹의 65억 달러 규모 데이터센터 확장이 이를 주도하고 있습니다. 일본의 크리스탈 인텔리전스(Cristal Intelligence) 이니셔티브와 한국의 GPU-as-a-Service(GPUaaS) 서비스는 내부 전문성이 부족한 중견 기업에도 AI 역량을 확장합니다. 인도의 스마트폰 농촌 지역 확대 및 토착어 모델 프로젝트는 강력한 하류 수요를 시사합니다.

유럽은 독일, 프랑스, 영국이 주도하는 꾸준한 확장을 기여하며, 각국은 EU 인공지능법 하의 엄격한 개인정보 보호 규정과 자동차·산업 정책을 연계하고 있습니다. 중동은 석유 수익금을 인공지능 허브에 투자하는 반면, 아프리카는 모바일 중심 사용 패턴을 활용해 농업 및 핀테크 분야의 인공지능 서비스를 시범 운영 중입니다. 종합적으로 지역별 차이는 인프라 성숙도, 규제 환경, 기기 가격 경쟁력에 집중되며, 이 요소들이 종합적으로 모바일 인공지능(AI) 시장의 도입 속도를 결정합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI 지원 프로세서 수요 급증

- 생성형 AI 스마트폰 출시

- 엣지 AI 칩의 에너지 효율 향상

- 소비자 프라이버시 및 저지연 요구

- 모바일 최적화 대규모 언어 모델(LLM) 프레임워크

- 5G 통신사 AI 기능 번들

- 시장 성장 억제요인

- AI 칩셋의 프리미엄 가격 정책

- 열 및 전력 예산 제약

- 기기 내 데이터에 대한 규제 감독

- 첨단 기판공급 크런치

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 스마트폰

- 카메라

- 드론

- 로봇 공학

- 자동차

- 기타 용도

- 컴포넌트별

- 하드웨어(AI 칩셋, 센서)

- 소프트웨어(SDK, 프레임워크)

- 서비스(통합, 유지보수)

- 기술별

- CPU

- GPU

- NPU/AI 가속기

- DSP

- 가공 유형별

- 온 디바이스/엣지

- 클라우드 기반

- 하이브리드

- 최종 사용자 업계별

- 소비자 가전

- 자동차 및 모빌리티

- 산업 및 제조업

- 헬스케어 및 생명과학

- 방위 및 항공우주

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Qualcomm Technologies

- Apple Inc.

- Samsung Electronics

- MediaTek Inc.

- Huawei Technologies(HiSilicon)

- Alphabet Inc.(Google)

- Nvidia Corporation

- Intel Corporation

- Microsoft Corporation

- IBM Corporation

- ARM Ltd.

- OPPO

- Xiaomi Corp.

- Vivo

- Honor Device Co.

- Baidu Inc.

- TSMC

- Synopsys

- Cadence Design Systems

- Graphcore

- Cerebras Systems

제7장 시장 기회와 장래의 전망

HBR 25.11.25The Mobile Artificial Intelligence Market size is estimated at USD 24.85 billion in 2025, and is expected to reach USD 81.22 billion by 2030, at a CAGR of 28.65% during the forecast period (2025-2030).

Heightened regulatory focus on data sovereignty, rapid neural-processing-unit (NPU) innovation, and enterprise demand for low-latency inference are the primary growth catalysts. Breakthrough chip designs such as Qualcomm's Snapdragon 8 Elite and ARM's Cortex-X925 are resetting performance baselines for smartphones, vehicles, and industrial devices. Vendor strategies now emphasize vertically integrated hardware-software stacks that shorten time-to-market and enable differentiated on-device AI features. Supply-chain constraints in advanced substrates and high-bandwidth memory continue to influence pricing and availability, yet committed capacity expansions in Asia Pacific signal relief after 2026.

Global Mobile Artificial Intelligence Market Trends and Insights

AI-Capable Processor Demand Surge

Unprecedented uptake of AI-centric chipsets is reshaping device architecture. ARM's 3 nm Cortex-X925 delivers 46% higher throughput than prior cores at 3.8 GHz while holding power ceilings suitable for premium phones. Manufacturers securing long-term foundry allocation, such as Qualcomm and NVIDIA, mitigate supply risk and lock in competitive cost structures. Samsung's Galaxy S25 showcases a 40% NPU boost, underscoring how performance marketing has shifted from general CPU metrics to sustained AI inference capability. Chip demand is also driving innovation in solid-state cooling that supports 25-watt dissipation in handheld form factors. The resulting performance headroom accelerates conversational interfaces, real-time vision, and on-device analytics that previously relied on cloud services.

Generative-AI Smartphone Launches

Generative AI is moving from flagship exclusivity toward mass-market availability. Canalys projects that 54% of global handset shipments will be AI-ready by 2028, a steep adoption curve that mirrors past LTE transitions. Apple's Neural Engine now performs on-device context modeling for messaging, while Samsung's Galaxy AI offers live translation and content drafting. Price sensitivity in India illustrates adoption friction: sub-USD 600 devices represent only 4-5% of 2024 shipments, limiting early AI penetration. To bridge the gap, MediaTek introduced Dimensity 9400 with an integrated NPU tuned for mid-range handsets. Enterprise fleets also drive volume, with OPPO pledging to embed generative-AI features in 50 million units via Google and Microsoft partnerships.

Premium Pricing of AI Chipsets

Entry-level AI smartphones still debut near USD 600, limiting penetration in high-volume growth economies. High-bandwidth-memory shortages persist because Micron and SK Hynix have capacity booked out through 2025, sustaining elevated bill-of-materials costs. Packaging bottlenecks around TSMC's CoWoS lines add further cost pressure for mobile device makers. Vendors respond by tiering feature sets: essential AI functions are delivered via software optimization on legacy silicon, while premium models add advanced NPU acceleration. New fabs coming online in Taiwan and Japan after 2026 may gradually reduce the price delta between AI and non-AI chipsets.

Other drivers and restraints analyzed in the detailed report include:

- Edge-AI Chip Energy-Efficiency Gains

- Consumer Privacy and Low-Latency Need

- Thermal and Power-Budget Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smartphones retained 56% of 2024 revenue, yet automotive applications are set to post a 29.40% CAGR through 2030 as conversational in-car assistants and autonomous functions transition from luxury options to mainstream features. The mobile artificial intelligence market size for automotive systems is projected to scale rapidly once Level-3 highway pilots become standard equipment in premium models. Partnerships like SoundHound-Tencent prove that multilingual voice control can be integrated with existing infotainment stacks. Camera apps continue adopting AI for night-mode and de-noise pipelines, while drones leverage edge inference for obstacle avoidance in GNSS-denied zones.

High growth in vehicles reflects structural changes in electronic control units, where AI now governs perception, intent prediction, and personalized user experience. Mercedes-Benz integrates large language models via CARIAD platforms that learn driver routines and proactively schedule servicing. Industrial robots and medical wearables represent additional high-value niches, underscoring how the mobile artificial intelligence market is broadening beyond consumer messaging to mission-critical domains.

Hardware held 64% of the 2024 spend thanks to NPUs, GPUs, and mm-wave sensors embedded across devices. Nevertheless, services revenue is forecast to climb 27.00% CAGR as enterprises outsource model training, fine-tuning, and lifecycle management. Managed offerings from Verizon and SK Telecom bundle cloud GPUs, edge nodes, and orchestration software, letting firms add AI features without upfront capex. Software libraries such as ARM's Kleidi accelerate N-dimensional tensor operations on generic CPUs, improving utilization of installed silicon.

Sensor evolution further blurs hardware-software boundaries by embedding micro-controllers that execute first-pass AI locally. The resulting data economy creates recurring revenue for analytics, updates, and compliance services, validating how platform models reshape the mobile artificial intelligence market.

The Mobile Artificial Intelligence Market Report is Segmented by Application (Smartphone, Camera, Drone, Robotics, Automotive, and Other Applications), Component (Hardware, Software, and Services), Technology (CPU, GPU, NPU/AI Accelerator, and DSP), Processing Type (On-device/Edge, Cloud-Based, and Hybrid), End-User Industry (Consumer Electronics, Automotive and Mobility, Industrial and Manufacturing, and More), and Geography.

Geography Analysis

North America held 35% revenue share in 2024 as enterprises rapidly deployed private 5G and edge nodes to host on-premises AI workloads. Large funding rounds, including OpenAI's USD 40 billion raise, reinforce the region's leadership in foundational-model research and commercial adoption. Government grants and defense contracts further stimulate demand for secure on-device solutions that meet stringent compliance standards.

Asia Pacific is the fastest-growing territory with a 24.80% CAGR through 2030, propelled by SoftBank's USD 960 million infrastructure plan and SK Group's USD 6.5 billion data-center build-out. Japan's Cristal Intelligence initiative and South Korea's GPU-as-a-Service offerings extend AI capabilities to mid-market enterprises without in-house expertise. India's smartphone expansion into rural districts and indigenous language model projects point to robust downstream demand.

Europe contributes steady expansion led by Germany, France, and the United Kingdom, each aligning automotive and industrial policy with strict privacy rules under the EU AI Act. The Middle East is channeling oil-windfall funds into AI hubs, while Africa leverages mobile-first usage patterns to pilot AI services in agriculture and fintech. Altogether, regional divergences center on infrastructure maturity, regulatory climate, and device affordability, factors that collectively shape deployment velocity in the mobile artificial intelligence market.

- Qualcomm Technologies

- Apple Inc.

- Samsung Electronics

- MediaTek Inc.

- Huawei Technologies (HiSilicon)

- Alphabet Inc. (Google)

- Nvidia Corporation

- Intel Corporation

- Microsoft Corporation

- IBM Corporation

- ARM Ltd.

- OPPO

- Xiaomi Corp.

- Vivo

- Honor Device Co.

- Baidu Inc.

- TSMC

- Synopsys

- Cadence Design Systems

- Graphcore

- Cerebras Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-capable processor demand surge

- 4.2.2 Generative-AI smartphone launches

- 4.2.3 Edge-AI chip energy-efficiency gains

- 4.2.4 Consumer privacy and low-latency need

- 4.2.5 Mobile-optimised LLM frameworks

- 4.2.6 5G-telco AI-feature bundles

- 4.3 Market Restraints

- 4.3.1 Premium pricing of AI chipsets

- 4.3.2 Thermal and power-budget constraints

- 4.3.3 Regulatory scrutiny on on-device data

- 4.3.4 Advanced substrate supply crunch

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Smartphone

- 5.1.2 Camera

- 5.1.3 Drone

- 5.1.4 Robotics

- 5.1.5 Automotive

- 5.1.6 Other Applications

- 5.2 By Component

- 5.2.1 Hardware (AI Chipsets, Sensors)

- 5.2.2 Software (SDKs, Frameworks)

- 5.2.3 Services (Integration, Maintenance)

- 5.3 By Technology

- 5.3.1 CPU

- 5.3.2 GPU

- 5.3.3 NPU/AI Accelerator

- 5.3.4 DSP

- 5.4 By Processing Type

- 5.4.1 On-device/Edge

- 5.4.2 Cloud-based

- 5.4.3 Hybrid

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Automotive and Mobility

- 5.5.3 Industrial and Manufacturing

- 5.5.4 Healthcare and Life-Sciences

- 5.5.5 Defense and Aerospace

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Qualcomm Technologies

- 6.4.2 Apple Inc.

- 6.4.3 Samsung Electronics

- 6.4.4 MediaTek Inc.

- 6.4.5 Huawei Technologies (HiSilicon)

- 6.4.6 Alphabet Inc. (Google)

- 6.4.7 Nvidia Corporation

- 6.4.8 Intel Corporation

- 6.4.9 Microsoft Corporation

- 6.4.10 IBM Corporation

- 6.4.11 ARM Ltd.

- 6.4.12 OPPO

- 6.4.13 Xiaomi Corp.

- 6.4.14 Vivo

- 6.4.15 Honor Device Co.

- 6.4.16 Baidu Inc.

- 6.4.17 TSMC

- 6.4.18 Synopsys

- 6.4.19 Cadence Design Systems

- 6.4.20 Graphcore

- 6.4.21 Cerebras Systems

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment