|

시장보고서

상품코드

1851749

자전거 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bicycle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

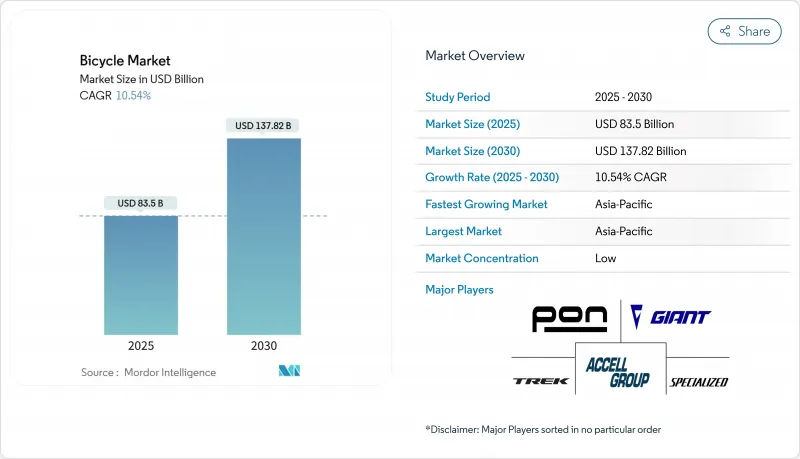

자전거 시장 규모는 2025년에 835억 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 10.54%를 나타낼 것으로 예측되며, 2030년에 1,378억 2,000만 달러에 달할 전망입니다.

도시 중심부에서는 혼잡 통행료 제도를 확대 시행하고 있으며, 고용주들은 건강 증진 프로그램에 자전거 이용 장려책을 포함시켜 자전거 수요를 지속적으로 촉진하고 있습니다. 이러한 수요는 탄소 배출 감축을 목표로 한 강화된 기후 정책과 더불어, 이미 예상치를 초과한 정부의 대규모 인프라 투자로 더욱 강화되고 있습니다. 또한 배터리 안전 기술의 지속적인 발전은 안전 우려를 해소함으로써 잠재적 소비자 기반을 확대하고 있습니다. 소비자 직거래 브랜드의 등장과 소프트웨어 기반 차량 관리 서비스의 통합은 소매 환경을 재정의하며 운영 효율성을 최적화하고 고객 접근성을 향상시키고 있습니다. 상승하는 연료 가격은 자전거가 자동차 대비 비용 우위를 더욱 확대시켜 경제적으로 더 실용적인 선택지로 만들고 있습니다. 전반적으로 자전거 시장은 유리한 규제 체계, 기술 발전, 지속 가능하고 활동적인 이동 솔루션으로의 도시 생활 방식 전환에 힘입어 성장을 지속하고 있습니다.

세계의 자전거 시장 동향 및 인사이트

친환경 교통 수단을 장려하는 정부 지원

전 세계 정부는 자전거 타기를 단순한 레크리에이션 활동이 아닌 기후 인프라의 핵심 요소로 점점 더 인식하고 있습니다. 이러한 변화는 2024년 4월 유럽연합(EU)이 채택한 '자전거 이용에 관한 유럽 선언'에서 명확히 드러납니다. 이 선언은 회원국들이 자전거 인프라를 강화하고 지속 가능한 교통 시스템에 통합하기 위한 36개의 구속력 있는 약속을 제시합니다. 마찬가지로 미국에서는 '활동적 교통 인프라 투자 프로그램'을 통해 매년 4,450만 달러를 투입해 연결된 자전거 네트워크를 구축함으로써 자전거 이용자의 접근성과 안전성을 높이고 있습니다. 주 차원에서는 캘리포니아가 4년간 9억 3,000만 달러를 투입해 265마일의 신규 자전거 도로를 건설하기로 약속하며 도시 계획에서 자전거의 중요성을 더욱 강조하고 있습니다. 이러한 포괄적인 정책 조치들은 자전거 관련 제품 및 서비스에 대한 지속적인 수요를 촉진하여 제조업체들이 생산 능력을 확대하도록 장려하고, 소매업체들이 증가하는 시장 수요를 충족시키기 위해 재고 수준을 높이는 동기를 부여하고 있습니다.

도시 혼잡이 일상 통근용 자전거 이용을 촉진

도시 밀집도가 높아짐에 따라, 특히 교통 혼잡의 경제적·사회적 비용에 직면한 아시아태평양 지역 메가시티에서 자전거 솔루션의 필요성이 절실합니다. 혼잡 통행료 부과와 저배출 구역 지정은 개인 차량보다 자전거 이용을 더욱 장려합니다. 하이브리드 근무 모델도 통근 방식을 재편하여, 자전거가 짧고 유연한 이동에 이상적인 수단이 되게 했습니다. 네덜란드는 철도망과 연계된 자전거 고속도로를 통해 자전거를 성공적으로 통합한 사례로, 자동차 소유에 필적하는 다중 모드 교통 시스템을 구축하면서 환경 및 이동성 문제를 해결하고 있습니다. 기업들은 직원 복지 프로그램과 지속가능성 보고 의무에 힘입어 자전거 이용을 점점 더 도입하고 있습니다. 자전거 인프라 투자는 인재 유치와 탄소 감축 목표 달성에 도움이 되며, 환경·사회·지배구조(ESG) 목표와도 부합합니다.

자전거와 같은 대체 수단 및 기타 더 빠른 교통 수단의 가용성이 자전거 이용을 저해

전기 스쿠터, 차량 공유 서비스, 자율주행 차량 시범 운영이 단거리 이동성을 해결함에 따라 교통 수단 간 경쟁이 심화되고 있습니다. 도시 지역에서 전기 자전거 소유 비용은 이제 전기 스쿠터 및 차량 공유 구독 비용과 경쟁할 정도로 높아져 가격 경쟁이 격화되고 있습니다. 마이크로모빌리티 플랫폼 통합에 힘입은 통합 교통 앱은 자전거를 수많은 교통 수단 중 하나로 만들었습니다. 광범위한 지하철 시스템을 갖춘 아시아태평양 도시에서는 대중교통 발전으로 장거리 통근 시 자전거 이용의 매력이 감소했습니다. 대체 교통 수단에 대한 규제는 빠르게 진전되는 반면, 자전거 인프라 구축은 지연되고 있습니다. 예를 들어, 전기 스쿠터 공유 프로그램은 신속한 승인을 받는 반면, 자전거 관련 프로젝트는 더 오랜 시간이 소요됩니다. 그러나 자전거의 건강 및 환경적 이점은 대체 위협을 제한하여 시장 존재감을 보장합니다.

부문 분석

2024년 전기 자전거는 자전거 시장의 51.25%를 차지했으며, 해당 부문은 2030년까지 연평균 12.76% 성장률(CAGR)을 기록할 것으로 전망됩니다. 따라서 전기 자전거 시장 규모는 소비자 신뢰를 높이는 UL 2849와 같은 안전 인증의 추진으로 향후 10년 내 두 배 이상 성장할 전망입니다. 배터리는 이제 탈착이 가능하고 항공 운송 규정을 준수하여 사용 사례가 확대되고 있습니다. 한편, 기존 도로용 및 도시용 자전거는 여전히 큰 판매량을 유지하며 부품 공급업체의 규모의 경제를 지속시키고 있습니다.

기술 융합이 경쟁 우위를 결정합니다. 내비게이션 통합, 도난 추적, 예측 유지보수 기능이 라이더 경험을 풍부하게 하여 프리미엄 가격대를 형성합니다. 아시아태평양 지역 생산사는 비용 효율적인 생산 능력을 활용하는 반면, 유럽 조립사는 근접성을 활용해 프리미엄 틈새 시장을 공략합니다. 중국의 배터리 재활용 의무화는 다른 지역이 따를 수 있는 모델을 제시하며, 규정을 준수하는 브랜드에 애프터서비스 수익을 추가합니다. 자전거와 차량 분석을 결합한 소프트웨어 중심 기업들은 자산 부담이 적은 이동성 예산 접근을 제공하며 시장 진입이 여전히 열려 있습니다.

2024년에도 일반 프레임이 자전거 시장을 계속 주도하며 85.78%라는 상당한 점유율을 차지할 전망입니다. 이러한 우위는 대량 생산된 기하학적 구조의 강력한 매력, 비용 효율적인 가격, 기존 인프라와의 원활한 호환성을 종합적으로 반영하여 일반 프레임을 소비자 선호 선택지로 만든다. 반면 접이식 디자인은 2030년까지 연평균 11.43%라는 인상적인 성장률을 기록하며 강력한 성장 궤도를 보일 전망입니다. 이 성장률은 전체 자전거 시장의 두 배에 달하며, 특히 도시 주거 공간의 한계와 철도망과의 효율적인 라스트마일 연결성 증대 요구와 같은 과제에 대응하는 컴팩트하고 공간 효율적인 솔루션에 대한 수요 증가가 주된 동력입니다.

마그네슘 힌지와 퀵 릴리스 클램프의 소재 발전으로 무게 부담이 줄어들었고, 일반 자전거와 동일한 보증 기간으로 과거의 망설임도 사라졌습니다. 자전거 업계에서는 직원용 차량으로 접이식 자전거를 선호하는데, 책상 아래나 작은 사물함에 안전하게 보관할 수 있기 때문입니다. 독일과 네덜란드를 중심으로 철도-자전거 복합 통근을 지원하는 유럽 정책은 접이식 모델에 규제적 호재를 제공합니다. 그러나 접이식 자전거의 소매 가격이 격차를 좁히기 전까지는 연간 판매량의 대부분이 여전히 일반 자전거에서 나올 것입니다.

지역 분석

2024년 아시아태평양 지역은 전 세계 시장의 48.11%를 차지하며 주요 수익 기여 지역으로서의 입지를 공고히 했습니다. 해당 지역은 여러 요인에 힘입어 2030년까지 13.33%의 높은 연평균 복합 성장률(CAGR)을 달성할 것으로 전망됩니다. 중국에서는 전기 자전거의 광범위한 보급, 의무적 배터리 재활용 정책 시행, 지속 가능한 교통수단으로서 이륜차 사용을 적극 장려하는 도시 교통 정책으로 인해 자전거 시장이 크게 성장하고 있습니다. 반면 일본은 인증 체계를 유럽 표준과 전략적으로 연계하여 수출 절차를 간소화하고 국내 브랜드의 글로벌 경쟁력을 강화하고 있습니다.

북미와 유럽에서는 대규모 인프라 투자 프로그램이 자전거에 대한 안정적이고 지속적인 수요를 창출하고 있습니다. 시장의 지리적 분포는 제조 활동이 아시아에 집중되어 있음을 보여주며, 선진 시장에서는 유리한 정책 조치에 힘입어 성장이 이루어지고 있습니다. 이러한 역학은 기존 아시아 제조업체의 우위를 강화할 뿐만 아니라 서구 시장에서 고품질 및 혁신적인 제품을 중시하는 소비자층을 대상으로 프리미엄 제품 포지셔닝 기회를 창출하는 무역 흐름을 촉진합니다.

중동 및 아프리카 자전거 시장은 전기 자전거 채택률이 두 자릿수 증가율을 보이며 가속화되고 전통적 자전거 수요도 꾸준히 유지되면서 견조한 성장을 경험하고 있습니다. 두바이, 케이프타운, 나이로비, 텔아비브 등 주요 도시의 도시 소비자들은 특히 전기 자전거를 자동차나 오토바이 같은 기존 차량에 대한 현대적이고 환경 친화적인 대안으로 인식하는 경향이 점점 더 강해지고 있습니다. 그러나 표준화된 안전 규정, 보험 체계, 교통 권리의 부재는 여전히 도전 과제로 남아 여러 아프리카 국가에서 자전거 시장의 신속한 제도화를 저해하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 도시 교통 혼잡으로 인한 일상 통근용 자전거 이용 증가

- 피트니스 트렌드로 인한 사이클링 활동 인기 상승

- 친환경 교통 수단 장려를 위한 정부 지원

- 환경 의식 및 지속가능성 인식이 소비자의 자전거 이용 촉진

- 직장 웰니스 프로그램으로 인한 직원 자전거 이용 장려

- 상승하는 연료 가격으로 인한 자전거의 비용 효율적 대안화

- 시장 성장 억제요인

- 자전거 대체 수단 및 더 빠른 교통수단의 가용성으로 인한 자전거 이용 감소

- 위조 자전거의 존재로 인한 시장 성장 저해

- 높은 전기 자전거 비용으로 인한 글로벌 확산 제한

- 농촌 지역의 열악한 도로 상태로 인한 원활한 자전거 이용 경험 저해

- 규제 상황

- 기술적 진보

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 도로/도시용

- 산악/전지형용

- 하이브리드

- 전기 자전거

- 기타 유형

- 설계별

- 일반형

- 접이식

- 최종 사용자별

- 남성

- 여성

- 어린이

- 유통 채널별

- 오프라인 소매점

- 온라인 소매점

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 네덜란드

- 폴란드

- 벨기에

- 스웨덴

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 한국

- 태국

- 싱가포르

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 칠레

- 페루

- 기타 남미

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 모로코

- 튀르키예

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Accell Group NV

- Trek Bicycle Corporation

- Pon Holdings BV

- Giant Manufacturing Co. Ltd

- Specialized Bicycle Components Inc.

- Shimano Inc.

- Scott Sports SA

- Merida Industry Co. Ltd

- Stryder Cycle Private Limited

- Cycles Devinci inc.

- Pending System GmbH & Co. KG

- Brompton Bicycle Ltd

- Decathlon SA

- Rad Power Bikes Inc.

- Riese and Muller GmbH

- Bulls Bikes GmbH

- Yadea Group Holdings Ltd

- Canyon Bicycles GmbH

- Hero Cycles Limited

- Ribble Cycles

제7장 시장 기회와 장래의 전망

HBR 25.11.25The bicycle market size is estimated at USD 83.50 billion in 2025, and is expected to reach USD 137.82 billion by 2030, at a CAGR of 10.54% during the forecast period (2025-2030).

Urban centers are increasingly implementing congestion charges, while employers are incorporating bicycle incentives into wellness programs, driving sustained demand for bicycles. This demand is further reinforced by significant government investments in infrastructure, which have already exceeded projections, alongside stricter climate policies aimed at reducing carbon emissions. Additionally, ongoing advancements in battery safety technology are expanding the potential consumer base by addressing safety concerns. The emergence of direct-to-consumer brands and the integration of software-enabled fleet services are redefining the retail landscape, optimizing operational efficiencies, and enhancing customer accessibility. Rising fuel prices are further amplifying the cost advantage of bicycles over motorized vehicles, making them a more economically viable option. Overall, the bicycle market continues to experience growth, supported by favorable regulatory frameworks, technological progress, and a shift in urban lifestyles toward sustainable and active mobility solutions.

Global Bicycle Market Trends and Insights

Government support encourages eco-friendly transportation methods

Governments worldwide are increasingly recognizing cycling as a critical element of climate infrastructure rather than merely a recreational activity. This shift is evident in the European Union's adoption of the European Declaration on Cycling in April 2024, which outlines 36 binding commitments for member states to enhance cycling infrastructure and promote its integration into sustainable transport systems . Similarly, in the United States, the Active Transportation Infrastructure Investment Program provides USD 44.5 million annually to develop connected cycling networks, fostering greater accessibility and safety for cyclists. On a state level, California has committed USD 930 million over four years to build 265 miles of new bike paths, further emphasizing the importance of cycling in urban planning . These comprehensive policy measures are driving sustained demand for cycling-related products and services, encouraging manufacturers to scale up production capacities and motivating retailers to increase their inventory levels to meet the growing market needs.

Urban congestion boosts bicycle usage for daily commute

As urban density pressures rise, especially in Asia-Pacific megacities facing traffic congestion's economic and social costs, the need for cycling solutions is critical. Congestion pricing and low-emission zones further promote cycling over private vehicles. Hybrid work models have also reshaped commuting, making cycling ideal for shorter, flexible trips. The Netherlands exemplifies successful cycling integration with cycling highways linked to rail networks, creating a multimodal transport system that rivals car ownership while addressing environmental and mobility challenges. Corporations are increasingly adopting cycling, driven by employee wellness initiatives and sustainability reporting mandates. Investments in cycling infrastructure help attract talent and meet carbon reduction goals, aligning with environmental and social governance (ESG) objectives.

Availability of substitute like bikes, and other faster transport modes discourages the use of bicycle

Competition among transport modes is intensifying as electric scooters, ride-sharing services, and autonomous vehicle pilots address short-distance mobility. In urban areas, e-bike ownership costs now rival those of electric scooters and ride-sharing subscriptions, heightening pricing competition. Integrated transport apps, driven by micromobility platform consolidation, have made bicycles one of many transport options. In Asia-Pacific cities with extensive metro systems, public transportation advancements have reduced cycling's appeal for longer commutes. While regulations for alternative transport modes advance quickly, cycling infrastructure faces delays. For instance, electric scooter-sharing programs receive rapid approvals, whereas cycling projects take longer. However, cycling's health and environmental benefits limit substitution threats, ensuring its market presence.

Other drivers and restraints analyzed in the detailed report include:

- Fitness trends increase popularity of cycling activities

- Environmental awareness and sustainability drives bicycle usage among consumers

- High e-bike cost restricts wider adoption globally

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-bicycles held 51.25% of the bicycle market in 2024, and the segment is forecast to post a 12.76% CAGR to 2030. The bicycle market size for e-bicycles is therefore on track to more than double within the decade, propelled by safety certifications such as UL 2849 that boost consumer trust. Batteries are now removable and airline-compliant, widening use cases. Meanwhile, conventional road and city bikes preserve large sales volumes, sustaining economies of scale for component suppliers.

Technology convergence defines competitive edges: integrated navigation, theft-tracking, and predictive maintenance enrich the rider experience and push premium price points. Asia-Pacific producers benefit from cost-efficient capacity, while European assemblers leverage proximity to capture premium niches. Battery recycling mandates in China set a template other regions may follow, adding after-sales service revenue for compliant brands. Market entry remains open for software-native firms bundling bikes with fleet analytics, providing asset-light access to mobility budgets.

In 2024, regular frames continue to dominate the bicycle market, accounting for a substantial 85.78% market share. This dominance highlights the strong appeal of mass-produced geometries, cost-effective pricing, and seamless compatibility with existing infrastructure, which collectively make regular frames a preferred choice among consumers. On the other hand, folding designs are projected to experience a robust growth trajectory, registering an impressive 11.43% CAGR through 2030. This growth rate, which is double that of the overall bicycle market, is primarily driven by the rising demand for compact and space-efficient solutions, particularly in response to challenges such as limited urban housing space and the growing need for efficient last-mile connectivity with rail networks.

Material advances in magnesium hinges and quick-release clamps now limit weight premiums, and warranty parity with regular bikes removes past hesitations. In the bicycle industry, corporations also favor foldables for employee fleets because units store safely under desks and in small lockers. European policy supporting combined rail-bike commutes, notably in Germany and the Netherlands, gives folding models regulatory tailwinds. Yet the bulk of annual volume will still come from regular bikes until folding retail prices close the gap.

The Bicycle Market Report is Segmented by Product Type (Road/City, Mountain/All-Terrain, Hybrid, E-Bicycle, and Others), Design (Regular and Folding), End-User (Men, Women, and Children), Distribution Channel (Offline Retail Stores and Online Retail Stores), and Geography ((North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2024, the Asia-Pacific region solidified its position as a key revenue contributor, accounting for 48.11% of the global market. The region is forecasted to achieve a strong compound annual growth rate (CAGR) of 13.33% through 2030, driven by several factors. In China, the bicycle market is experiencing significant growth due to the widespread adoption of e-bikes, the enforcement of mandatory battery-recycling initiatives, and urban traffic policies that actively encourage the use of two-wheelers as a sustainable mode of transportation. Japan, on the other hand, is strategically aligning its certification frameworks with European standards, thereby simplifying export procedures and enhancing the global competitiveness of its domestic brands.

In North America and Europe, large-scale infrastructure investment programs are creating a stable and sustained demand for bicycles. The market's geographic distribution underscores a concentration of manufacturing activities in Asia, while developed markets are witnessing growth driven by favorable policy measures. This dynamic fosters trade flows that not only reinforce the dominance of established Asian manufacturers but also create opportunities for premium product positioning in Western markets, catering to a consumer base that values high-quality and innovative offerings.

The bicycle market in the Middle East and Africa is experiencing robust growth, with e-bike adoption accelerating at double-digit rates and traditional bicycles maintaining steady demand. Urban consumers in key cities such as Dubai, Cape Town, Nairobi, and Tel Aviv are increasingly perceiving bicycles, particularly e-bikes, as modern, eco-conscious alternatives to conventional vehicles like cars and motorbikes. However, the lack of standardized safety regulations, insurance frameworks, and traffic rights continues to pose challenges, hindering the rapid formalization of the bicycle market in several African nations.

- Accell Group NV

- Trek Bicycle Corporation

- Pon Holdings BV

- Giant Manufacturing Co. Ltd

- Specialized Bicycle Components Inc.

- Shimano Inc.

- Scott Sports SA

- Merida Industry Co. Ltd

- Stryder Cycle Private Limited

- Cycles Devinci inc.

- Pending System GmbH & Co. KG

- Brompton Bicycle Ltd

- Decathlon SA

- Rad Power Bikes Inc.

- Riese and Muller GmbH

- Bulls Bikes GmbH

- Yadea Group Holdings Ltd

- Canyon Bicycles GmbH

- Hero Cycles Limited

- Ribble Cycles

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban congestion boosts bicycle usage for daily commute

- 4.2.2 Fitness trends increase popularity of cycling activities

- 4.2.3 Government support encourages eco-friendly transportation methods

- 4.2.4 Environmental awareness and sustainability drives bicycle usage among consumers

- 4.2.5 Workplace wellness programs encourage employee bicycle usage

- 4.2.6 Rising fuel prices make bicycles cost-effective alternatives

- 4.3 Market Restraints

- 4.3.1 Availability of substitute like bikes, and other faster transport modes discourages the use of bicycle

- 4.3.2 Presence of counterfeit bicycles hinders market growth

- 4.3.3 High e-bike cost restricts wider adoption globally

- 4.3.4 Poor road conditions in rural areas hinder smooth bicycle experience

- 4.4 Regulatory Landscape

- 4.5 Technological Advancements

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Road/City

- 5.1.2 Mountain/All-Terrain

- 5.1.3 Hybrid

- 5.1.4 E-Bicycle

- 5.1.5 Other Types

- 5.2 By Design

- 5.2.1 Regular

- 5.2.2 Folding

- 5.3 By End-User

- 5.3.1 Men

- 5.3.2 Women

- 5.3.3 Children

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accell Group NV

- 6.4.2 Trek Bicycle Corporation

- 6.4.3 Pon Holdings BV

- 6.4.4 Giant Manufacturing Co. Ltd

- 6.4.5 Specialized Bicycle Components Inc.

- 6.4.6 Shimano Inc.

- 6.4.7 Scott Sports SA

- 6.4.8 Merida Industry Co. Ltd

- 6.4.9 Stryder Cycle Private Limited

- 6.4.10 Cycles Devinci inc.

- 6.4.11 Pending System GmbH & Co. KG

- 6.4.12 Brompton Bicycle Ltd

- 6.4.13 Decathlon SA

- 6.4.14 Rad Power Bikes Inc.

- 6.4.15 Riese and Muller GmbH

- 6.4.16 Bulls Bikes GmbH

- 6.4.17 Yadea Group Holdings Ltd

- 6.4.18 Canyon Bicycles GmbH

- 6.4.19 Hero Cycles Limited

- 6.4.20 Ribble Cycles