|

시장보고서

상품코드

1851813

컴퓨터 비전 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Computer Vision - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

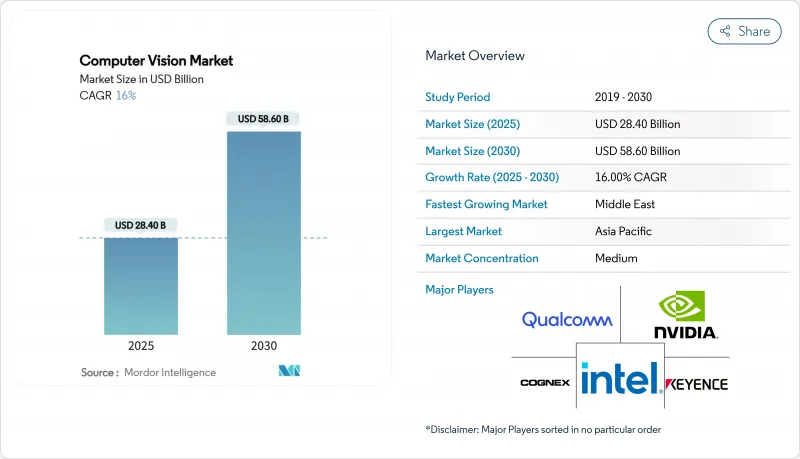

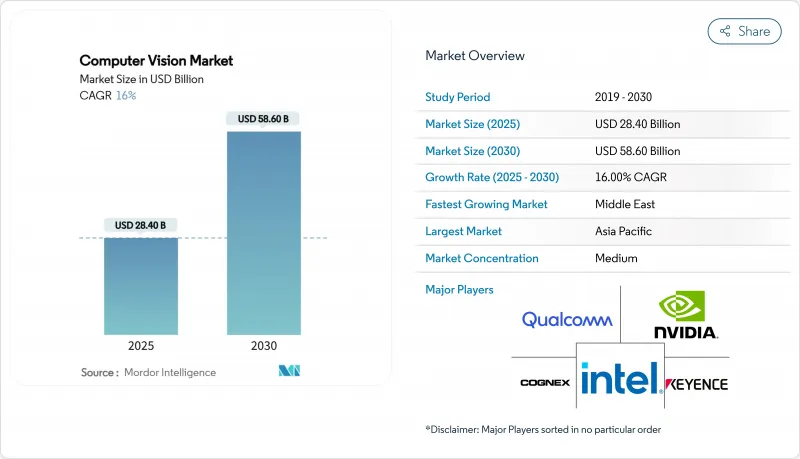

컴퓨터 비전 시장 규모는 2025년에 284억 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 16%로, 2030년에는 586억 달러에 이를 것으로 예상됩니다.

성장의 축은 추론을 클라우드 서버에서 디바이스의 프로세서로 마이그레이션하는 더 빠른 에지 AI 칩셋입니다. 또한 공장에서의 노동력 부족, 비전 가이데드 로봇의 사용 증가, 아시아태평양의 수출 지향 공장에서의 산업용 카메라의 보급도 수요의 추풍이 되고 있습니다. 동시에 자동차 OEM은 EU의 일반 안전 규정 II를 준수하기 위해 멀티 카메라 ADAS 제품군을 도입하여 규제 마감일을 내장 비전 센서의 대량 출하로 바꾸고 있습니다. 첨단 칩의 수출 규제가 Tier2 경제권에공급을 엄격히 하고 있지만, 국내 반도체 투자를 가속, 시장 경쟁 역학을 바꾸고 있다고 합니다.

세계의 컴퓨터 비전 시장 동향과 인사이트

제조에서의 비전 가이드 로보틱스 채용 증가

고도의 비전을 갖춘 협동 로봇이 이전에는 인간의 눈이 필요했던 조립 검증이나 결함 검사를 실시하게 되어 공장 관리자는 픽 앤 플레이스의 루틴을 넘어 자동화를 에스컬레이션시키고 있습니다. NIST는 머신 비전을, 특히 서브 미크론의 공차가 양보할 수 없는 반도체나 바이오 제조의 클린 룸에서 로봇의 유연성을 가능하게 하는 기둥으로 분류하고 있습니다. 현대자동차의 전자기기 라인은 혼합 데이터 세트에서 알고리즘을 재학습하고 생산을 중단하지 않고 모델을 최신으로 유지하는 모바일 로봇을 도입한 후 패스트 패스 수율이 향상되었다고 보고하고 있습니다. 또한 비전 가이디드 코봇은 예지 보전의 밑바닥이기도 하고, 고장에 의해 스케줄이 미치기 전에 도구의 마모를 특정할 수 있습니다. 투자 수익률은 휴머노이드 로봇을 상회하고, 일찌기 비구조화 환경에서 자동화에 저항이 있던 건설이나 농업 분야에서의 이용이 퍼지고 있습니다. 이러한 변화가 결합되어 희귀 숙련 노동자에 대한 의존을 억제하고 다품종 생산 라인에서 처리량의 일관성을 높임으로써 공장 경제가 재구성됩니다.

규제 산업에서 엄격한 품질 관리의 의무화

겹치는 리콜로 수작업에 의한 검사의 한계가 노출됨으로써 규제 당국은 자동 광학 검사가 필수적이라고 생각하게 되었습니다. EU의 일반 안전 규칙 II에서는 2024년 7월부터 자동차 제조업체에 보행자 감지 카메라와 긴급 브레이크 로직을 통합할 것을 의무화하고 있으며, 티어원 공급업체는 비전 모델을 중심으로 전자 제어 장치를 재설계해야 합니다. 제약회사는 딥러닝 비전을 도입하여 블리스터 씰의 무결성과 라벨의 정확성을 검증하고 있습니다. 식품 가산업자는 코그넥스의 In-Sight 센서를 통합하여 이물 검출률을 100%로 함으로써 이물 오염 콜백을 줄이고 감사 추적을 강화하고 있습니다. 환경보호기관은 폐수 컴플라이언스의 지속적인 비디오 증거를 요구하고 있으며, 비전 시스템을 재량 지출에서 조달 의사 결정에 영향을 미치는 위험 완화 자산으로 전환하고 있습니다.

복잡한 시스템 통합 요구 사항

기존의 공장 라인은 자체 필드버스 프로토콜과 비차폐 배선에 의존하며 수동 검사를 카메라 시스템에 드롭인으로 대체하는 것을 복잡하게 합니다. 가혹한 현장 진동과 전자기 노이즈는 이미지의 충실도를 줄이고 견고한 광학 부품과 긴 교정 사이클을 요구합니다. 멀티 센서 퓨전이 LiDAR 및 열 입력을 추가하는 경우, 통합자는 이기종 실시간 운영 체제간에 데이터 스트림을 동기화해야 하며, 사내 전문 지식이 없는 중소기업의 경우 도입 일정이 연장됩니다. 커스텀 미들웨어와 안전 인증은 프로젝트 예산을 부풀리게 하고, 원래의 ROI 계산을 넘어 채용을 앞당기기도 합니다.

부문 분석

2024년의 컴퓨터 비전 시장 매출의 68.0%는 하드웨어였는데, 이는 기업이 생산 라인의 개조를 위해 산업용 카메라, 조명 유닛, 전용 프로세서를 구입했기 때문입니다. 이 중 에지 AI 가속기는 2030년까지 연평균 복합 성장률(CAGR)이 24.5%로 모든 하위 구성 요소 중 가장 빠릅니다. 카메라 모듈은 여전히 가장 큰 슬라이스이지만 지능형 센서가 이미지 캡처와 추론을 통합하고 케이블 비용과 대기 시간을 줄이면서 달러 점유율이 줄어 듭니다. 광학 장비 공급업체는 농업 및 재활용을 위해 가시 스펙트럼을 초과하는 물질의 시그니처를 검출하는 하이퍼스펙트럼 렌즈로부터 이익을 얻는다. 소프트웨어 측면에서 컨테이너화된 추론 스택과 미들웨어는 지속적인 모델의 재튜닝에 대한 축족을 반영하여 영구 라이선스 알고리즘보다 큰 연간 구독 예산을 획득하고 있습니다. 하드웨어의 컴퓨터 비전 시장 규모는 자동차 및 전자 OEM의 견조한 설비 투자에 힘입어 2030년까지 340억 달러 이상에 달할 것으로 예상됩니다.

소프트웨어 플랫폼은 2024년 지출액의 32.0%를 차지하며, 기업이 단발 배포보다 데이터 파이프라인과 DevOps 통합을 강조함에 따라 꾸준히 성장했습니다. 에지 오케스트레이션 프레임워크는 수천 개의 엔드포인트에 모델 업데이트를 제공하고 디바이스를 적응형 센서 네트워크로 전환하는 데 도움이 됩니다. 이 변화는 On-Premise에서의 데이터 처리와 투명한 감사 추적을 선호하는 사이버 보안에 대한 우려 증가와 일치합니다. 그 결과 시스템 통합사업자는 ML 전문 팀이 없는 중견 공장을 위해 시간 대 가치를 압축하는 턴키 스택을 번들로 제공하여 컴퓨터 비전 시장의 대응 가능한 수요를 확대하고 있습니다.

컴퓨터 비전 시장은 구성 요소별(하드웨어 및 소프트웨어), 최종 사용자 산업별(생명과학, 자동차 제조, 소매 및 E-Commerce, 물류 및 창고 등), 지역별로 구분되어 있습니다.

지역별 분석

아시아태평양은 2024년 컴퓨터 비전 시장 매출의 41.0%를 차지하고 중국의 산업용 카메라 매출이 2023년 185억 위안에서 2024년에는 207억 위안으로 28.35% 증가해 급속한 로봇 공학 도입에 연결됐습니다. 일본 칩 파운드리과 한국 스마트폰 OEM은 웨이퍼 스케일 AOI 도구의 높은 수요를 유지하고 인도는 정밀 농업 조종사의 규모를 확대하여 기후 변화로 인한 식량 공급에 대한 스트레스를 상쇄합니다. 정부의 그린 팩토리 프로그램은 스마트 카메라를 통한 리노베이션을 지원하고 거시적인 역풍 속에서도 안정적인 설비 투자 흐름을 지원합니다. 최상급 GPU를 제한하는 수출 규제 정책이 지역 팹을 국산 가속기로 향하게 하여 지역의 자립성을 서서히 높여가고 있습니다.

중동은 2030년까지 연평균 복합 성장률(CAGR)이 17.2%로 가장 빠르며 사우디아라비아가 1,000억 달러의 AI기금을 설립하고 UAE가 2031년까지 세계 AI 허브 상위 10개국에 들어가겠다는 야망을 내걸고 있습니다. 리야드와 두바이에서는 국가가 지원하는 스마트 시티의 건설이 진행되고 있으며, 교통 흐름과 중요한 인프라 보호를 위해 에지 분석 기능을 갖춘 감시 카메라가 대량으로 구입되고 있습니다. 항만과 자유 구역에서 물류 자동화에 대한 병행 투자는 걸프 지역의 컴퓨터 비전 시장을 더욱 확장시킵니다.

북미에서는 NHTSA의 자동 브레이크 의무화가 가까이 다가오고 있으며 ADAS 카메라의 지속적인 출하가 촉진되는 반면, 미국 국방부는 비전 중심의 자율화 프로젝트에 자금을 투입하고 견조한 조달 c를 유지하고 있습니다. 그러나 인재 부족과 칩 수출의 억제가 당면의 성장을 완만하게 하고 있으며, 현지에서의 훈련 이니셔티브와 다양한 실리콘 공급의 필요성이 부각되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 제조에 있어서 시각 유도 로봇의 채용 증가

- 규제 산업 전체에 걸친 엄격한 품질 관리 의무

- 차재 ADAS 카메라 통합의 급증

- 온 디바이스 비전을위한 대기 시간과 전력 소비를 줄이는 에지 AI 칩셋

- 하이퍼스펙트럼과 뉴로모픽 센서가 여는 새로운 이용 사례

- 시장 성장 억제요인

- 복잡한 시스템 통합 요건

- 숙련된 컴퓨터 비전 기술자의 부족

- 데이터 라벨링 비용의 상승

- 첨단 비전 프로세서 수출 규제

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 구성 요소별

- 하드웨어

- 카메라

- 프로세서(GPU/ASIC/FPGA)

- 광학 및 조명

- 소프트웨어

- 기존 알고리즘

- 딥러닝 프레임워크

- 엣지 미들웨어

- 하드웨어

- 최종 사용자 업계별

- 생명과학

- 제조

- 일렉트로닉스 조립

- 식음료

- 포장

- 국방 및 보안

- 자동차

- ADAS

- 자율주행차량

- 소매 및 전자상거래

- 물류 및 창고

- 농업 및 임업

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- ASEAN

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Intel Corporation

- Cognex Corporation

- Keyence Corporation

- Sony Group Corp.

- NVIDIA Corporation

- Omron Corporation

- Basler AG

- Teledyne FLIR LLC

- Qualcomm Inc.

- Google LLC

- Advanced Micro Devices(AMD)

- Adlink Technology Inc.

- Hikvision Robotics

- Stemmer Imaging AG

- Dahua Technology

- Zebra Technologies

- Amazon Web Services(AWS)

- Clarifai Inc.

- Allied Vision Technologies

- OpenCV.ai

- Matrox Imaging

제7장 시장 기회와 향후 전망

KTH 25.11.17The Computer Vision Market size is estimated at USD 28.40 billion in 2025, and is expected to reach USD 58.60 billion by 2030, at a CAGR of 16% during the forecast period (2025-2030).

Growth pivots around faster edge-AI chipsets that move inference from cloud servers to on-device processors, a shift encouraged by stricter automotive and manufacturing regulations that insist on real-time, auditable inspection data. Demand also benefits from acute labor shortages on factory floors, increasing use of vision-guided robotic,s and wider industrial camera uptake across Asia-Pacific's export-oriented plant,s Sohu. Simultaneously, automotive OEMs implement multi-camera ADAS suites to comply with EU General Safety Regulation II, turning regulatory deadlines into volume shipments for embedded visionsensorsr. Export-control rules on advanced chips tighten supply for Tier 2 economies, yet they accelerate domestic semiconductor investments, altering competitive dynamics in the computer vision market.

Global Computer Vision Market Trends and Insights

Rising Adoption of Vision-Guided Robotics in Manufacturing

Plant managers escalate automation beyond pick-and-place routines as collaborative robots equipped with advanced vision now handle assembly verification and defect inspection that previously required human eyes. NIST classifies machine vision as an enabling pillar for robotic flexibility, especially in semiconductor and biomanufacturing cleanrooms where sub-micron tolerances are non-negotiable.Hyundai's electronics lines report higher first-pass yield after introducing mobile robots that retrain algorithms on mixed data sets, keeping models current without halting production. Vision-guided cobots also underpin predictive maintenance, identifying tool wear before failures disrupt schedules. Return on investment outperforms humanoid robotics, widening use in construction and agritech, where unstructured settings once resisted automation. Together, these shifts reshape factory economics by curbing reliance on scarce skilled labor and boosting throughput consistency in high-mix lines.

Stringent Quality-Control Mandates Across Regulated Industries

Regulators now view automated optical inspection as essential after repeated recalls exposed limitations of manual checks. EU General Safety Regulation II obliges automakers to embed pedestrian-detection cameras and emergency-braking logic from July 2024, compelling tier-one suppliers to redesign electronic control units around vision models. Pharmaceutical packagers deploy deep-learning vision to verify blister-seal integrity and label accuracy, aligning with FDA validation guidelines for automated inspection. Food processors integrate Cognex In-Sight sensors that achieve 100% foreign-object detection, reducing contamination callbacks and strengthening audit trails.Environmental agencies likewise demand continuous video evidence of effluent compliance, turning vision systems from discretionary spend into risk-mitigation assets that influence procurement decisions.

Complex System-Integration Requirements

Legacy factory lines rely on proprietary field-bus protocols and unshielded wiring that complicate the drop-in replacement of manual inspection with camera systems. Harsh shop-floor vibration and electromagnetic noise degrade image fidelity, demanding ruggedized optics and lengthy calibration cycles. When multi-sensor fusion adds LiDAR or thermal inputs, integrators must synchronize data streams across heterogeneous real-time operating systems, extending deployment timelines for small and mid-sized enterprises that lack in-house expertise. Custom middleware and safety certification inflate project budgets, sometimes eclipsing initial ROI calculations and postponing adoption.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Automotive ADAS Camera Integration

- Edge-AI Chipsets Lowering Latency & Power for On-Device Vision

- Shortage of Skilled Computer-Vision Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024 hardware accounted for 68.0% of computer vision market revenue as enterprises purchased industrial cameras, illumination units and dedicated processors to retrofit production lines. Within this total, edge-AI accelerators exhibit a 24.5% CAGR through 2030, the fastest trajectory among all sub-components, as designers replace discrete GPU farms with low-power ASICs and NPUs embedded at the image source. Camera modules remain the largest slice, yet their dollar share narrows as intelligent sensors merge image capture and inference, trimming cabling costs and latency. Optics vendors profit from hyperspectral lenses that detect material signatures beyond the visible spectrum for agriculture and recycling. On the software side, containerized inference stacks and middleware now receive annual subscription budgets larger than perpetual-license algorithms, reflecting the pivot toward continuous model retuning. The computer vision market size for hardware is forecast to exceed USD 34 billion by 2030, supported by resilient capital expenditure among automotive and electronics OEMs.

Software platforms contribute 32.0% of 2024 outlay and grow steadily as firms valorize data pipelines and DevOps integration over one-off deployments. Edge orchestration frameworks help distribute model updates across thousands of endpoints, turning device fleets into adaptive sensor networks. The shift aligns with rising cyber-security concerns that favor on-premises data handling and transparent audit trails. As a result, systems integrators bundle turnkey stacks that compress time-to-value for mid-tier factories lacking dedicated ML teams, in turn expanding addressable demand for the computer vision market.

The Computer Vision Market is Segmented by Components (Hardware and Software), by End-User Industry (Life Science, Manufactur Automotive, Retail and E-Commerce, Logistics and Warehousing and More) and Geography.

Geography Analysis

Asia-Pacific commanded 41.0% of the computer vision market revenue in 2024, buoyed by China's industrial camera sales that rose from CNY 18.5 billion in 2023 to CNY 20.7 billion in 2024, a 28.35% jump tied to rapid robotics adoption. Japan's chip foundries and South Korea's smartphone OEMs sustain high unit demand for wafer-scale AOI tools, while India scales precision-agriculture pilots to offset climate stress on food supply. Government green-factory programs subsidize retrofits with smart cameras, anchoring a steady capital-spending stream even amid macro headwinds. Export-control policies restricting top-tier GPUs push local fabs toward domestic accelerators, gradually lifting regional self-reliance.

The Middle East exhibits the fastest trajectory at 17.2% CAGR to 2030, propelled by Saudi Arabia's USD 100 billion AI fund and the UAE's ambition to rank among the top 10 global AI hubs by 2031. State-backed smart-city builds in Riyadh and Dubai purchase large volumes of surveillance cameras with edge analytics for traffic flow and critical-infrastructure protection. Parallel investments in logistics automation at ports and free zones further enlarge the computer vision market in the Gulf.

North America benefits from NHTSA's impending automatic-braking mandate, driving continuous ADAS camera shipments, while the US Department of Defense bankrolls vision-centric autonomy projects, sustaining a robust procurement c. Europe's Industry 4.0 policy fund supports AI-powered inspection retrofits, and its strict labeling standards stimulate demand in food and pharma plants. However, talent scarcity and chip export curbs moderate near-term growth, highlighting the need for local training initiatives and diversified silicon supply.

- Intel Corporation

- Cognex Corporation

- Keyence Corporation

- Sony Group Corp.

- NVIDIA Corporation

- Omron Corporation

- Basler AG

- Teledyne FLIR LLC

- Qualcomm Inc.

- Google LLC

- Advanced Micro Devices (AMD)

- Adlink Technology Inc.

- Hikvision Robotics

- Stemmer Imaging AG

- Dahua Technology

- Zebra Technologies

- Amazon Web Services (AWS)

- Clarifai Inc.

- Allied Vision Technologies

- OpenCV.ai

- Matrox Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of vision-guided robotics in manufacturing

- 4.2.2 Stringent quality-control mandates across regulated industries

- 4.2.3 Surge in automotive ADAS camera integration

- 4.2.4 Edge-AI chipsets lowering latency and power for on-device vision

- 4.2.5 Hyperspectral and neuromorphic sensors opening new use-cases

- 4.3 Market Restraints

- 4.3.1 Complex system-integration requirements

- 4.3.2 Shortage of skilled computer-vision engineers

- 4.3.3 Escalating data-labeling cost inflation

- 4.3.4 Export-control curbs on advanced vision processors

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Components

- 5.1.1 Hardware

- 5.1.1.1 Cameras

- 5.1.1.2 Processors (GPUs / ASIC / FPGA)

- 5.1.1.3 Optics and Lighting

- 5.1.2 Software

- 5.1.2.1 Traditional Algorithms

- 5.1.2.2 Deep-Learning Frameworks

- 5.1.2.3 Edge Middleware

- 5.1.1 Hardware

- 5.2 By End-user Industry

- 5.2.1 Life Sciences

- 5.2.2 Manufacturing

- 5.2.2.1 Electronics Assembly

- 5.2.2.2 Food and Beverage

- 5.2.2.3 Packaging

- 5.2.3 Defense and Security

- 5.2.4 Automotive

- 5.2.4.1 ADAS

- 5.2.4.2 Autonomous Vehicles

- 5.2.5 Retail and E-commerce

- 5.2.6 Logistics and Warehousing

- 5.2.7 Agriculture and Forestry

- 5.2.8 Other Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 India

- 5.3.3.5 ASEAN

- 5.3.3.6 Australia and New Zealand

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Middle East

- 5.3.4.1 GCC

- 5.3.4.2 Turkey

- 5.3.4.3 Rest of Middle East

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Nigeria

- 5.3.5.3 Rest of Africa

- 5.3.6 South America

- 5.3.6.1 Brazil

- 5.3.6.2 Argentina

- 5.3.6.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Cognex Corporation

- 6.4.3 Keyence Corporation

- 6.4.4 Sony Group Corp.

- 6.4.5 NVIDIA Corporation

- 6.4.6 Omron Corporation

- 6.4.7 Basler AG

- 6.4.8 Teledyne FLIR LLC

- 6.4.9 Qualcomm Inc.

- 6.4.10 Google LLC

- 6.4.11 Advanced Micro Devices (AMD)

- 6.4.12 Adlink Technology Inc.

- 6.4.13 Hikvision Robotics

- 6.4.14 Stemmer Imaging AG

- 6.4.15 Dahua Technology

- 6.4.16 Zebra Technologies

- 6.4.17 Amazon Web Services (AWS)

- 6.4.18 Clarifai Inc.

- 6.4.19 Allied Vision Technologies

- 6.4.20 OpenCV.ai

- 6.4.21 Matrox Imaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment