|

시장보고서

상품코드

1910644

플렉소 인쇄 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Flexographic Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

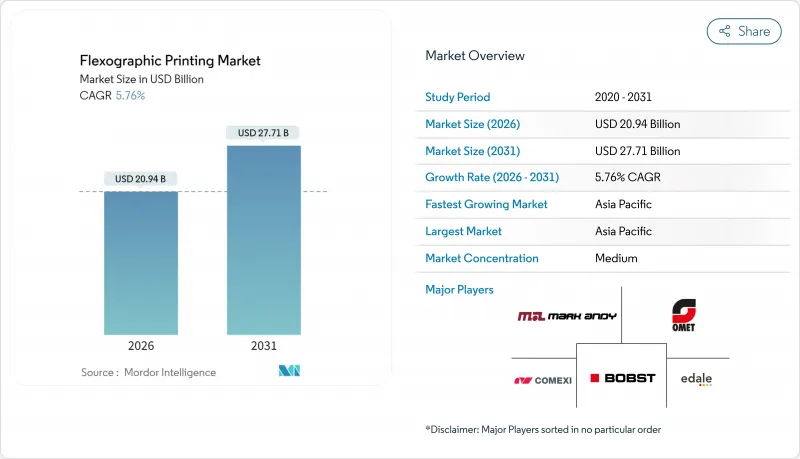

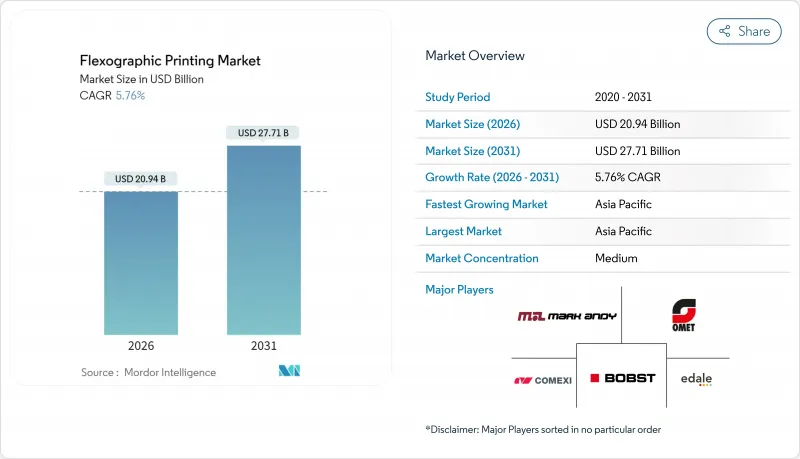

세계의 플렉소 인쇄 시장은 2025년에 198억 달러로 평가되었으며, 2026년 209억 4,000만 달러에서 2031년까지 277억 1,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중 (2026-2031년) CAGR은 5.76%로 예상됩니다.

전자상거래량 증가, 식품 접촉 규제 엄격화, AI를 활용한 인쇄기 자동화의 지속적인 개선이 플렉소 인쇄 시장의 이러한 기세를 유지할 것으로 예측됩니다. 벤더는 짧은 SKU 라이프사이클에 대응하는 브랜드를 위한 협폭 웹 인쇄기 및 디지털 하이브리드 인쇄기의 최적화를 진행하고 있는 한편, 컨버터는 세계의 VOC(휘발성 유기 화합물) 기준치에 대한 적합을 위해, 수성 잉크 채용을 강화하고 있습니다. 지속 가능한 골판지 물류에 대한 수요 증가와 신속한 판 설치 및 검사 시스템에 대한 투자가 함께 플렉소 인쇄 시장은 경쟁하는 평판 인쇄나 그라비아 인쇄 수법에 대해 우위적인 입장을 유지하고 있습니다. 아시아태평양의 생산 능력과 순환형 포장에 대한 정부의 우대조치가 함께 이 지역은 플렉소 인쇄 시장에서 주도적 역할을 더욱 확고하게 하고 있습니다.

세계의 플렉소 인쇄 시장 동향과 통찰

브랜드 소유자에 의한 SKU 사이클 단축 수요

소비자의 선호도 변화가 전례 없는 속도로 진행되는 동안, 브랜드 매니저는 포장 디자인을 자주 쇄신할 수밖에 없습니다. 컨버터는 이에 대응하고, 몇 분만에 판 교환을 완료하는 협폭 웹 인쇄기를 활용함으로써, 다운타임과 재료 폐기를 억제하고 있습니다. Onyx GO와 같은 솔루션은 활성 가시성 제어를 통해 설치 시 스크랩을 30% 절감합니다. 단기화에 의해 소매업체는 계절 한정 상품을 잉여 재고를 안지 않고 시험적으로 전개할 수 있어 플렉소 인쇄 시장 전체에서 운전 자금의 부담을 경감합니다. 동시에 클라우드 기반 워크플로우 소프트웨어가 아트워크 승인을 가속화하여 새로운 디자인이 컨셉부터 매장 전개에 이르기까지 몇 주 내에 실현되도록 합니다.

비용 효율적인 장기 패키지 인쇄

인쇄 매수가 수백만을 초과하는 경우 플렉소 인쇄는 여전히 최저 단가를 제공합니다. 포토폴리머 버전은 수십만회의 사이클을 견디며 에너지 절약형 건조기가 운영 비용을 절감합니다. DuPont의 Orion 사례에서는 그라비아 인쇄에서 플렉소 인쇄로 이행해 용제 사용량을 30% 삭감해, 작업 현장의 안전성도 향상했습니다. 이러한 경제성으로 인해 기존 소비재 라인은 플렉소 인쇄 시장에 정착하고 OEM 제조업체는 인쇄기 가동률과 예비 부품 판매를 유지합니다. 아시아의 컨버터 기업은 3교대제로 가동하면서 이러한 비용 우위성을 최대한 활용하여 수출 주도 수요에 대응하고 있습니다.

소규모 인쇄에서의 디지털 잉크젯 카니발리제이션

압전 헤드와 수성 분산 잉크의 진보로 경쟁력 있는 클릭률로 가변 데이터와 오프셋에 가까운 화질을 실현하고 있습니다. 제약 패키지 제조업체는 디지털 라인을 ERP 소프트웨어와 통합하고 국가별 첨부 문서를 주문형으로 생산하여 재고를 0으로 줄입니다. 이에 대응하여, 플렉소 인쇄 시장은 기존 유닛과 인라인 잉크젯 스테이션을 융합한 하이브리드 인쇄기로 전환을 진행하고 있어, 확립된 마무리 워크플로우를 유지하면서 직렬화 기능을 추가하고 있습니다.

부문 분석

컨버터가 대량 생산 모드와 개별화 배치 생산 사이를 전환할 수 있는 단일 라인을 추구하면서 디지털 하이브리드 인쇄기의 새로운 도입 점유율이 상승했습니다. 2025년에는 협폭 웹 기기가 수익의 30.52%를 차지했지만, 하이브리드는 9.09%의 연평균 복합 성장률(CAGR)로 성장을 지속하여 있어 플렉소 인쇄 시장 전체를 크게 웃돌고 있습니다. 전형적인 구성은 브랜드 컬러용 10색 플렉소 데크와 리와인더 바로 앞에 배치된 CMYK 잉크젯 바를 결합합니다. 이러한 설정을 사용하면 작업 전환 시간을 5분 미만으로 줄일 수 있으며 평균 주문량이 5,000개 선형 미터 미만인 경우에도 라인 수익성을 유지할 수 있습니다. 중간 폭 웹 라인은 티슈 오버랩 및 스낵 포장지에서 여전히 선호되고 있으며, 광폭 웹 CI 플렉소는 스탠드업 파우치에서 우위를 유지하고 있습니다. 매엽 인쇄기는 다운스트림 공정에서 정밀한 금형 제거 스테이션이 필요한 접이식 판지에 해당합니다.

모듈형 플랫폼을 도입한 컨버터는 고객의 제품 구성 변화에 따라 나중에 코로나 처리 장치, 냉각 롤 또는 두 번째 잉크젯 바를 추가할 수 있습니다. SapphireLUCE는 이 모듈화를 구현하고 있으며, 1200 X 1200 DPI의 해상도와 분당 150미터의 속도를 양립하고 있습니다. 서비스 수준 계약에는 종종 예지 보전 분석이 포함되어 계획되지 않은 다운타임을 가동 시간의 2% 미만으로 줄입니다. 이러한 기능 세트를 통해 OEM 제조업체는 가격 결정력을 유지할 수 있습니다. 이는 신흥국의 재생 인쇄기의 상승에 따라 플렉소 인쇄 시장 전체가 경쟁 압력에 직면하고 있는 상황에서도 변하지 않습니다.

수성 시스템은 2025년에 적은 냄새와 대부분의 관할 구역에서 식품 직접 접촉 승인을 통해 매출액의 40.42%를 차지했습니다. 이들은 골판지 상자, 접이식 판지, 종이 포장의 핵심 화학입니다. 한편, UV 경화형 잉크는 비 다공질 필름 상에서 고속 인쇄와 우수한 내찰상성을 실현하기 위해 2031년까지 연평균 복합 성장률(CAGR) 8.28%로 확대가 전망됩니다. 에너지 경화형 솔루션은 수은 아크 장치보다 65% 적게 전력을 소모하는 콤팩트 LED 램프를 필요로 하며 공장의 전기 요금 절감에 기여합니다. 용제계 잉크는 미국 환경보호청(EPA) 제59조 규제에 따른 VOC 배출 상한의 강화로 점유율을 계속 축소하고 있습니다. 전자선 경화형 잉크는 2% 미만의 보급률로 틈새 시장에 머물지만, 유제품용 뚜껑재나 무균 카톤 분야에서 유망시되고 있습니다.

잉크 공급업체는 안료 분산 안정성, 유동학 제어 및 저이행성 첨가제 패키지로 차별화를 도모하고 있습니다. INX International의 GelFlex EB 잉크는 특정 스낵 용도에서 라미네이션을 필요로 하지 않으며 게이지 중량을 줄이고 호일 사용량을 줄일 수 있습니다. 이러한 혁신은 플렉소 인쇄 시장 전체에 퍼지는 지속가능성의 조류를 반영합니다.

지역별 분석

아시아태평양은 2025년에 38.05%의 최대 수익 점유율을 창출해 2031년까지 연평균 복합 성장률(CAGR) 9.06%로 확대가 전망됩니다. 중국은 기재, 잉크 및 기계를 공급해 통합 비용 시너지를 실현하는 한편, 인도에서는 2자리 성장의 전자상거래 소포가 국내 포장 수요를 견인하고 있습니다. 일본과 한국은 자동화를 중시하고 협동 로봇에 의한 롤 교환 기능을 갖춘 인쇄 라인의 개발을 선도하고 있습니다. ASEAN 국가의 정부 재활용 목표는 수성 잉크와 단일 소재 파우치 설계를 촉진하고 플렉소 인쇄 시장 전반에서 대응할 수 있는 기회를 확대하고 있습니다.

북미는 기술 혁신의 선구자로서 AI 구동형 검사 카메라와 클라우드 접속형 점도 컨트롤러의 시험 운용을 주도하고 있습니다. 브랜드 오너는 FDA 준거 저이행 워크플로우를 실현하는 컨버터를 평가해, 고부가가치 인쇄의 유지를 추진. 노동력 부족이 계속되고 있는 가운데, Ricoh의 '고도 캐리어 교육 프로그램' 등, 인쇄기의 데이터 분석을 오퍼레이터에게 습득시키는 대처가 전개되고 있습니다. 니어 쇼어링 동향으로 소비재의 제조 거점이 아시아에서 멕시코로 이행하여 북미 내의 연속식 플렉소 인쇄 라인에 신규 투자가 촉진되고 있습니다.

유럽에서는 엄격한 규제 감시가 계속되고 있으며, "제로 오염" 틀 아래에서 식물 유래 광 개시제와 광물유 프리 잉크 세트의 신속한 도입이 요구되고 있습니다. 독일은 엔지니어링의 우수성을 바탕으로, 프랑스는 바이오플라스틱 포장을 가속화하고, 이탈리아는 Bobst의 1,200제곱미터에 이르는 피렌체 센터와 같은 협폭 웹 기술 거점의 확대를 추진하고 있습니다. 동유럽 컨버터는 유리한 임금 구조를 활용하여 수주 증가에 대응하고 플렉소 인쇄 시장에서 이 지역의 다양한 역할을 강화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 브랜드 오너로부터의 SKU 사이클 단축 요망

- 비용 효율적인 긴 패키지 인쇄

- 식품 접촉 적합을 위한 수성 잉크 채용

- 지속 가능한 골판지 물류로 전환

- AI를 활용한 인쇄기 자동화와 폐기물 감축

- 전자상거래가 멀티월 메일러 수요를 가속

- 시장 성장 억제요인

- 소규모 생산에서 디지털 잉크젯 카니발리제이션

- 포토폴리머 판의 가격 변동성

- 용제계 VOC 규제 강화

- 숙련된 인쇄 오퍼레이터의 부족

- 공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 인쇄 기기 유형별

- 협폭 웹

- 중간 웹

- 광폭 웹

- 매엽식

- 디지털 하이브리드

- 잉크 유형별

- 수성

- 용제 베이스

- UV 경화형

- 전자빔

- 기재 유형별

- 종이 및 판지

- 연질 플라스틱 필름

- 금속 포일

- 기타 기판 유형

- 용도별

- 골판지 상자

- 접이식 판지

- 연포장

- 라벨

- 인쇄 매체

- 기타 용도

- 최종 사용 산업별

- 식품 및 음료

- 의료 및 의약품

- 퍼스널케어 및 화장품

- 산업

- 기타 최종 사용 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bobst Group SA

- Heidelberger Druckmaschinen AG

- Mark Andy Inc.

- Comexi Group

- Koenig and Bauer AG

- Windmoller & Holscher KG

- Uteco Group

- OMET SRL

- Edale Ltd.

- Star Flex International

- InterFlex Group

- Flexopack SA

- Pepin Manufacturing Inc.

- Wolverine Flexographic LLC

- Siva Group

- Gallus Ferd. Ruesch AG

- Nilpeter A/S

- Soma Engineering

- PCMC(Barry-Wehmiller)

- Tresu Group

- MPS Systems BV

제7장 시장 기회와 미래 전망

SHW 26.01.26The flexographic printing market was valued at USD 19.80 billion in 2025 and estimated to grow from USD 20.94 billion in 2026 to reach USD 27.71 billion by 2031, at a CAGR of 5.76% during the forecast period (2026-2031).

Rising e-commerce volumes, stringent food-contact regulations, and continuous improvements in AI-enabled press automation are expected to uphold this momentum in the flexographic printing market. Equipment vendors are optimizing narrow-web and digital-hybrid presses to serve brands that juggle shorter SKU life cycles, while converters intensify water-based ink adoption to comply with global VOC thresholds. Growing demand for sustainable corrugated logistics, together with investments in rapid plate-mounting and inspection systems, keeps the flexographic printing market well placed against competing lithography and gravure methods. Asia-Pacific's manufacturing capacity, paired with government incentives for circular packaging, further cements the region's leadership role in the flexographic printing market.

Global Flexographic Printing Market Trends and Insights

Brand-owner Demand for Shorter SKU Cycles

Consumer preferences now turn over faster than ever, pushing brand managers to refresh packaging artwork frequently. Converters respond by leaning on narrow-web presses that complete plate changes in minutes, curbing downtime and material waste. Solutions such as the Onyx GO deliver active register control that lowers setup scrap by 30%. Shorter runs also let retailers pilot seasonal editions without carrying surplus inventory, reducing the working-capital burden throughout the flexographic printing market. In parallel, cloud-based workflow software accelerates artwork approvals, ensuring that new designs progress from concept to shelf within weeks.

Cost-Effective Long-Run Package Printing

Where volumes exceed millions of impressions, flexography still offers the lowest unit cost. Photopolymer plates last hundreds of thousands of cycles, while energy-efficient dryers reduce operating expenses. DuPont's Orion case illustrates 30% solvent savings after migrating from gravure to flexo, along with safer shop-floor conditions. Such economics keep legacy consumer-goods lines anchored in the flexographic printing market, preserving press utilization and spare-parts sales for OEMs. Asian converters, often running three shifts, maximize these cost advantages to meet export-driven demand.

Digital Inkjet Cannibalisation in Short Runs

Advances in piezo-electric heads and aqueous dispersion inks enable variable data and near-offset image quality at competitive click rates. Pharmaceutical packagers integrate digital lines with ERP software to produce country-specific leaflets on demand, cutting inventory to zero. In response, the flexographic printing market is pivoting to hybrid presses that merge in-line inkjet stations with conventional units, preserving established finishing workflows while adding serialization capability.

Other drivers and restraints analyzed in the detailed report include:

- Water-Based Ink Adoption for Food Contact Compliance

- Shift Toward Sustainable Corrugated Logistics

- Volatile Photopolymer Plate Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital-hybrid presses lifted their share of new installations as converters sought one line that could alternate between mass-production mode and personalized batches. Although narrow-web machines secured 30.52% of revenue in 2025, the hybrid cohort is on course for 9.09% CAGR, well above the overall flexographic printing market. Typical configurations combine 10-color flexo decks for brand colors with CMYK inkjet bars placed just before the rewinder. Such set-ups reduce job changeover time to under five minutes, keeping lines profitable even when average order quantities fall below 5,000 linear m. Medium-web lines remain favored in tissue overwraps and snack wrappers, while wide-web CI flexo retains dominance in stand-up pouches. Sheet-fed presses serve folding cartons that require precise die-cutting stations downstream.

Converters equipping themselves with modular platforms can later bolt on corona treaters, chill rolls, or second inkjet bars as client mixes evolve. The SapphireLUCE exemplifies this modular path, pairing 1200 X 1200 DPI resolution with speeds of 150 mpm. Service-level agreements often bundle predictive-maintenance analytics, shrinking unplanned downtime below 2% of available hours. These feature sets sustain pricing power for OEMs, even as the broader flexographic printing market experiences competitive pressure from refurbished presses in emerging economies.

Water-based systems commanded 40.42% revenue in 2025 thanks to low odour and direct-food-contact approval in most jurisdictions. They form the baseline chemistry for corrugated boxes, folding cartons, and paper wraps. UV-curable inks, however, are projected to register 8.28% CAGR through 2031 because they support higher line speeds and excellent scratch resistance on non-porous films. Energy-curable solutions require compact LED lamps that draw 65% less power than mercury arc units, reducing plant electricity bills. Solvent variants, constrained by tightening VOC caps under the US EPA Part 59 ruling, continue to cede share. Electron-beam curables remain a niche at under 2% penetration but show promise in dairy lidding and aseptic cartons.

Ink suppliers differentiate through pigment dispersion stability, rheology control, and low-migration additive packages. INX International's GelFlex EB ink removes lamination in certain snack applications, dropping gauge weight and cutting foil usage. Such innovations echo the broader sustainability narrative resonating throughout the flexographic printing market.

The Flexographic Printing Market Report is Segmented by Printing Equipment Type (Narrow Web, Medium Web, and More), Ink Type (Water-Based, Solvent-Based, and More), Substrate Type (Paper and Paperboard, Flexible Plastic Films, and More), Application (Corrugated Boxes, Folding Carton, and More), End-User Industry (Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated the largest revenue slice at 38.05% in 2025 and is projected to compound at 9.06% CAGR to 2031. China supplies substrates, inks, and machinery, enabling integrated cost synergies, while India posts double-digit e-commerce parcel growth that fuels domestic packaging demand. Japan and South Korea emphasize automation, pioneering press lines equipped with cobot-assisted roll changes. Government recycling targets across ASEAN incentivize water-based inks and mono-material pouch designs, broadening addressable opportunities throughout the flexographic printing market.

North America remains the technology pione-er, hosting pilot runs for AI-driven inspection cameras and cloud-connected viscosity controllers. Brand owners reward converters that demonstrate FDA-compliant low-migration workflows, sustaining high value-added print per square meter. Labor shortages persist, prompting initiatives like Ricoh's Advanced Career Education program that trains operators in press-side data analytics. Nearshoring trends reroute consumer-goods manufacturing from Asia to Mexico, spurring fresh investments in CI flexo lines within North America.

Europe maintains keen regulatory oversight, compelling swift adoption of plant-based photoinitiators and mineral-oil-free ink sets under the Zero Pollution framework. Germany anchors engineering excellence, France accelerates bio-plastic packaging, and Italy scales narrow-web competence hubs such as Bobst's 1,200 sqm Florence center. Eastern European converters leverage favorable wage structures to absorb overflow orders, reinforcing the region's diverse role in the flexographic printing market.

- Bobst Group SA

- Heidelberger Druckmaschinen AG

- Mark Andy Inc.

- Comexi Group

- Koenig and Bauer AG

- Windmoller & Holscher KG

- Uteco Group

- OMET SRL

- Edale Ltd.

- Star Flex International

- InterFlex Group

- Flexopack SA

- Pepin Manufacturing Inc.

- Wolverine Flexographic LLC

- Siva Group

- Gallus Ferd. Ruesch AG

- Nilpeter A/S

- Soma Engineering

- PCMC (Barry-Wehmiller)

- Tresu Group

- MPS Systems B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brand - owner demand for shorter SKU cycles

- 4.2.2 Cost-effective long-run package printing

- 4.2.3 Water-based ink adoption for food contact compliance

- 4.2.4 Shift toward sustainable corrugated logistics

- 4.2.5 AI-driven press automation and waste reduction

- 4.2.6 E-commerce accelerates multi-wall mailers

- 4.3 Market Restraints

- 4.3.1 Digital inkjet cannibalisation in short runs

- 4.3.2 Volatile photopolymer plate prices

- 4.3.3 Solvent-based VOC regulations tightening

- 4.3.4 Skilled press-operator shortage

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Equipment Type

- 5.1.1 Narrow Web

- 5.1.2 Medium Web

- 5.1.3 Wide Web

- 5.1.4 Sheet-Fed

- 5.1.5 Digital-Hybrid

- 5.2 By Ink Type

- 5.2.1 Water-Based

- 5.2.2 Solvent-Based

- 5.2.3 UV-Curable

- 5.2.4 Electron-Beam

- 5.3 By Substrate Type

- 5.3.1 Paper and Paperboard

- 5.3.2 Flexible Plastic Films

- 5.3.3 Metallic Foil

- 5.3.4 Other Substrate Type

- 5.4 By Application

- 5.4.1 Corrugated Boxes

- 5.4.2 Folding Carton

- 5.4.3 Flexible Packaging

- 5.4.4 Labels

- 5.4.5 Print Media

- 5.4.6 Other Application

- 5.5 By End-user Industry

- 5.5.1 Food and Beverage

- 5.5.2 Healthcare and Pharmaceuticals

- 5.5.3 Personal Care and Cosmetics

- 5.5.4 Industrial

- 5.5.5 Other End-user Industry

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bobst Group SA

- 6.4.2 Heidelberger Druckmaschinen AG

- 6.4.3 Mark Andy Inc.

- 6.4.4 Comexi Group

- 6.4.5 Koenig and Bauer AG

- 6.4.6 Windmoller & Holscher KG

- 6.4.7 Uteco Group

- 6.4.8 OMET SRL

- 6.4.9 Edale Ltd.

- 6.4.10 Star Flex International

- 6.4.11 InterFlex Group

- 6.4.12 Flexopack SA

- 6.4.13 Pepin Manufacturing Inc.

- 6.4.14 Wolverine Flexographic LLC

- 6.4.15 Siva Group

- 6.4.16 Gallus Ferd. Ruesch AG

- 6.4.17 Nilpeter A/S

- 6.4.18 Soma Engineering

- 6.4.19 PCMC (Barry-Wehmiller)

- 6.4.20 Tresu Group

- 6.4.21 MPS Systems B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment