|

시장보고서

상품코드

1851901

의약품 의료기기 조합 제품 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Drug Device Combination Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

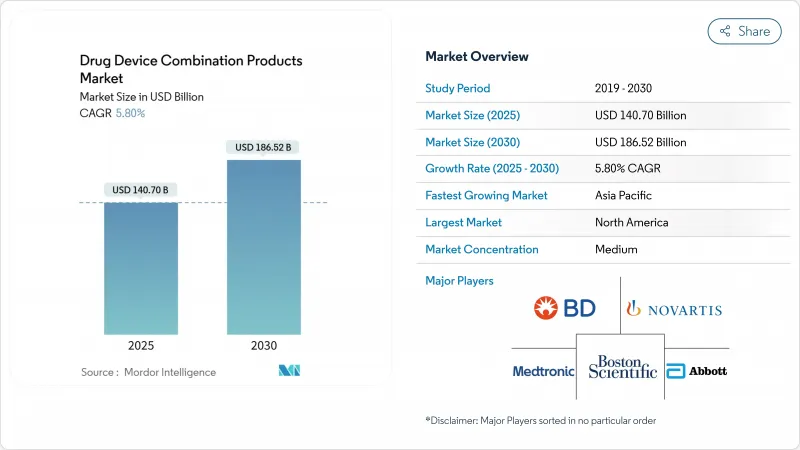

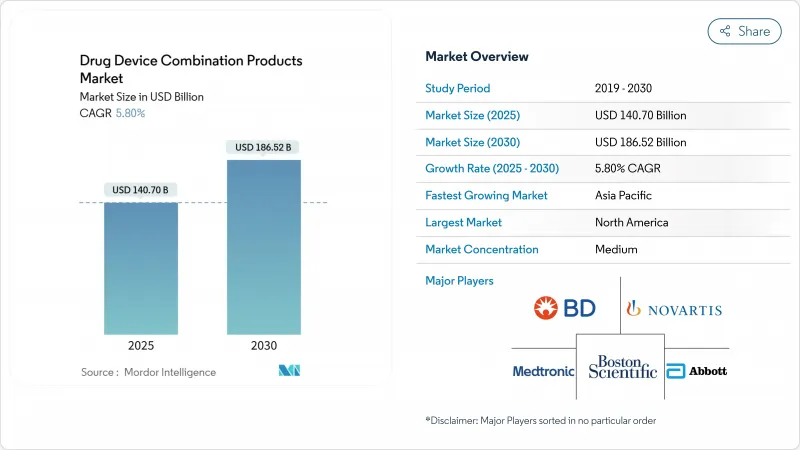

의약품 의료기기 조합 제품 시장은 2025년에 1,407억 달러로 추정되고, 2030년에는 1,865억 2,000만 달러에 이를 전망이며, CAGR 5.8%로 성장할 것으로 예측됩니다.

성장의 배경에는 만성 질환의 유병률 상승, 승인까지의 기간을 단축하는 미국의 규제 당국의 가속화, 의료비 전체를 삭감하면서 어드히어런스를 향상시키는 통합 치료에 대한 환자 수요가 있습니다. 실시간 모니터링 및 약물 전달의 융합으로, 이전에는 수동적이었던 장치가 능동적인 질병 관리 플랫폼으로 변모하고, 지불자와 의료 제공업체에게 새로운 가치 제안을 창출하고 있습니다. 북미는 강력한 혁신 자금을 통해 리드를 유지하고 있으며, 아시아태평양은 비용 경쟁력 있는 무균 제조와 지지적인 정책 조화를 통해 기세를 늘리고 있습니다. 기존 기업이 틈새 시장의 혁신자를 인수하여 의약품 및 의료기기의 노하우와 디지털 기능을 확보함으로써 경쟁이 격화됩니다.

세계의 의약품 의료기기 조합 제품 시장 동향 및 인사이트

만성 질환의 부담 증가가 표적 병용 요법 수요 견인

심혈관 질환은 세계 6억 5,500만 명에 영향을 미치고 있으며, 기계적 지원 및 국소 약물 요법을 통합한 약물 용출 스텐트 및 약물 코팅 풍선에 대한 수요를 지원합니다. FDA가 승인한 AGENT 파클리탁셀 코팅 풍선은 주요 심장 부작용을 비코팅 장치에 비해 11.1% 줄이고 통합 플랫폼의 임상 우위를 강화하고 있습니다. 지속적인 포도당 모니터링과 자동 인슐린 투여를 결합한 당뇨병 솔루션은 현재 기존의 요법보다 훨씬 높은 70%의 혈당 조절률을 달성하고 있습니다. 종양학은 84%의 진단 정확도를 달성하고 재수술을 제한하는 Lumisight와 같은 수술 중 영상과 약물의 하이브리드로 전환하고 있습니다. 이러한 예는 의약품 의료기기 조합 제품 시장의 혁신자가 정밀 진단 및 치료를 결합하여 장기적인 비용을 절감하는 방법을 보여줍니다.

급속한 고령화로 자기 투여 제제의 보급이 진행됨

65세 이상의 세계 인구는 2030년까지 7억 7,100만 명에 이를 전망이며, 손끝의 민첩함의 쇠퇴를 보완하는 사용하기 쉬운 의료기기에 대한 요구가 높아집니다. 입소메드 YpsoDose와 같은 자동 주사기는 노인을 돕기 위해 시청각 신호를 사용합니다. 이미 CAGR 6.56%로 가장 급성장하고 있는 최종 사용자인 재택 간호 현장에서는 엔벡터 스마트폰 대응 인슐린 시스템과 같은 패치 펌프가 이익을 가져오고 환자 자신이 안전하게 치료할 수 있게 됩니다. 실시간 어드히어런스 데이터는 만성 질환 환자의 절반을 차지하는 컴플라이언스 위반을 해결합니다. FDA의 휴먼 팩터 지침은 노인이 처음 사용하는 경우에도 올바르게 사용할 수 있도록 설계를 위해 제조업체를 안내합니다.

다시설에서의 규제 준수는 비용 및 지연 초래

유럽의 MDR과 IVDR의 확대로 문서화 부담이 증가하고 이전 규칙에 비해 승인에 8-12개월이 걸립니다. 노티파이드 바디에 의한 심사는 제형 개발자의 컴플라이언스 비용을 25-40% 상승시킵니다. FDA와 EMA의 분류가 다르기 때문에 중복 시험을 실시할 수밖에 없지만, 아시아태평양에서는 ASEAN의 하모나이제이션 노력에도 불구하고 단편화된 채로 남아 있습니다. 상호 승인이 없기 때문에 기업은 별도의 품질 시스템을 유지해야 하며 오버헤드가 팽창하고, 의약품 의료기기 조합 제품 시장에서 새로운 치료제의 세계 전개가 지연되고 있습니다.

부문 분석

약물 용출 스텐트는 재협착을 감소시키는 수십년에 걸친 근거를 반영하여 2024년 점유율 24.56%로 선두를 유지했습니다. 폴리머의 지속적인 진보로 약물의 용출이 180일을 넘어서 이 부문의 의약품 의료기기 조합 제품 시장에서 우위를 유지하고 있습니다. 한편, 프리필드 시린지는 생물제제의 수량이 증가하고 스마트 센서가 지불자를 위한 주사 이벤트를 기록하기 때문에 2030년까지의 CAGR이 6.34%로 되었습니다. 프리필드 시스템의 의약품 의료기기 조합 제품 시장 규모는 연결 표준이 성숙하고 가치 기반 케어가 어드히어런스 추적에 보상됨에 따라 현저하게 상승할 것으로 예측됩니다.

경피 패치는 고분자 마이크로니들을 사용하여 체중 감량 요법으로 확대됩니다. 자동 주사기는 인체 공학적 개선으로 성장하고 착용 가능한 주사기는 기저 인슐린 전달을 눈에 띄지 않는 패치 경험으로 바꿉니다. 모바일 앱과 연동하는 커넥티드 흡입기는 천식 컨트롤 스코어를 기존 제품에 비해 43% 향상시켰습니다. 보스턴 사이언티픽사의 Intera Oncology사 인수로 간동맥암 주입용 주입 펌프가 소형화되어 의약품 의료기기 조합 제품 시장에서의 프레즌스가 강화되었습니다.

심혈관 치료는 2024년 매출의 35.51%를 차지했으며, 약물 용출 스텐트, 코팅 풍선, 리듬 관리 임플란트가 그 기둥이 됩니다. 펄스 자기장 절제는 심장의 다음 국경이며,이 분야는 의약품 의료기기 조합 제품 시장의 주력입니다. 반면 통증 관리는 이식 가능한 신경 조절이 비 오피오이드 대체 요법을 제공하고 보험 적용을 받았기 때문에 CAGR은 6.45%입니다. 신경조절 시스템의 의약품 의료기기 조합 제품 시장 규모는 만성 통증 환자 증가와 함께 빠르게 확대될 것으로 예측됩니다.

당뇨병은 센서 펌프 생태계에 의해 견조한 기세를 유지하고 있습니다. 호흡기 질환은 디지털 흡입기 및 폐 고혈압증을 위한 새로운 제형으로부터 혜택을 받습니다. 종양학은 치료 위치에 대한 즉각적인 피드백을 제공하는 이미지 유도 약물 전달로 이동합니다. 비만 임플란트 및 정신 건강 스패치는 의약품 의료기기 조합 제품 산업을 더욱 다양화시킬 수 있는 새로운 카테고리입니다.

지역 분석

북미는 FDA의 명확한 규제 아키텍처와 높은 헬스케어 지출에 힘입어 2024년 세계 매출의 40.56%를 차지했습니다. 존슨 엔드 존슨에 의한 125억 달러의 Shockwave Medical 인수와 같은 대형 인수는 심장 인터벤션 포트폴리오를 강화하고 지역 우위를 강화합니다. 디지털 헬스 파트너십이 활발해지고, 커넥티드 포도당 모니터링 에코시스템이 실현되어 의약품 의료기기 조합 제품 시장이 더욱 강화됩니다.

2030년까지 연평균 복합 성장률(CAGR)은 아시아태평양이 가장 빠른 6.82%로 전망되며, 중국, 인도, 베트남 제조 클러스터는 무균 조립 비용을 절감하고 ASEAN 의료기기 지침과 같은 이니셔티브는 국경을 넘어 등록을 간소화합니다. 각국 정부는 연구개발 세제 우대 조치에 자금을 제공하고, 지역 CDMO는 세계 아웃소싱 계약을 획득하며 시장 범위를 확대합니다. 싱가포르와 한국은 효율적인 윤리 승인주기로 임상시험 활동을 유치하고 있습니다.

유럽에서는 MDR 관련 종이 작업에도 불구하고 완만한 진전이 계속되고 있습니다. 독일, 스위스, 아일랜드의 혁신 허브가 커넥티드 흡입기와 디지털 신경 조절을 리드하고 있습니다. 민간 협력은 데이터 대응 기기의 상환을 통합하는 시험 프로그램을 지원하며, 이 지역은 의약품 의료기기 조합 제품 산업에 필수적인 존재가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환의 부담 증가가 표적 병용 요법 수요 견인

- 고령화의 급속한 진전이 자기 관리형 제제의 보급 뒷받침

- 저침습 및 스마트 딜리버리 플랫폼의 돌파구

- 미국 FDA의 신속화된 복합제품 패스웨이가 시장 투입까지의 시간 단축

- 커넥티드 흡입기와 패치가 페이어에 의무화된 어드히어런스 분석을 가능하게 함

- 아시아 전역에서 확대하는 저비용의 멸균 어셈블리 생산 능력이 ASP 인하

- 시장 성장 억제요인

- 다시설 규제 대응은 비용 및 지연 초래

- 무균성 및 투여 정밀도와 관련된 높은 리콜율

- 아피스에 적합한 특수 폴리머 공급 핍박

- 디지털 콤보 기기의 통일 상환 코드 부재

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁의 격렬함

제5장 시장 규모 및 성장 예측

- 제품별

- 약제 용출 스텐트

- 경피 흡수 패치

- 주입 펌프

- 약제 코팅 풍선

- 흡입기

- 프리필드 주사기

- 웨어러블 주사기

- 자동 주사기

- 기타

- 용도별

- 심혈관 질환

- 당뇨병

- 암 치료

- 호흡기 질환

- 통증 관리

- 기타

- 최종 사용자별

- 병원 및 클리닉

- 외래 외과 센터

- 홈케어

- 기타

- 투여 경로별

- 오랄

- 비경구

- 경피

- 임플란트

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Medtronic plc

- Boston Scientific Corporation

- Johnson & Johnson

- Novartis AG

- GlaxoSmithKline plc

- Becton, Dickinson and Company

- Terumo Corporation

- Stryker Corporation

- WL Gore & Associates, Inc.

- AbbVie

- Viatris Inc.(Mylan)

- Cook Medical

- Hisamitsu Pharmaceutical

- Teva Pharmaceutical Industries

- Solventum

- Phillips-Medisize

- Ypsomed AG

- AstraZeneca plc

- Novo Nordisk

제7장 시장 기회 및 향후 전망

AJY 25.11.19The drug device combination products market stood at USD 140.7 billion in 2025 and is forecast to reach USD 186.52 billion by 2030, advancing at a 5.8% CAGR fda.gov.

Growth stems from rising chronic-disease prevalence, faster U.S. regulatory pathways that trim approval timelines , and patient demand for integrated therapies that improve adherence while lowering overall care costs. Convergence of real-time monitoring with targeted drug delivery is turning once-passive devices into active disease-management platforms, creating fresh value propositions for payers and providers. North America keeps its lead through robust innovation funding, whereas Asia-Pacific gains momentum on cost-competitive sterile manufacturing and supportive policy harmonization. Competitive activity intensifies as incumbents buy niche innovators to secure drug-device know-how and digital capabilities.

Global Drug Device Combination Products Market Trends and Insights

Growing Burden of Chronic Illnesses Driving Demand for Targeted Combination Therapies

Cardiovascular disease affects 655 million people worldwide, sustaining demand for drug-eluting stents and drug-coated balloons that unite mechanical support with localized pharmacotherapy. The FDA-cleared AGENT paclitaxel-coated balloon cut major adverse cardiac events by 11.1% versus uncoated devices, reinforcing the clinical edge of integrated platforms . Diabetes solutions that couple continuous glucose monitoring with automated insulin dosing now achieve 70% glycemic-control rates, far higher than traditional regimens. Oncology is moving toward intra-operative imaging-drug hybrids such as Lumisight, which delivers 84% diagnostic accuracy and limits repeat surgeries. These examples show how drug device combination products market innovators lower long-term costs by pairing precision diagnostics with therapy .

Rapidly Ageing Population Boosting Uptake of Self-Administered Delivery Formats

The global population aged 65+ will reach 771 million by 2030, amplifying need for easy-to-use devices that offset declining dexterity. Autoinjectors like Ypsomed's YpsoDose use audio-visual cues to aid seniors. Home care settings-already the fastest-growing end-user at a 6.56% CAGR-benefit from patch pumps such as Embecta's smartphone-enabled insulin system that lets patients treat themselves safely. Real-time adherence data address non-compliance, which affects half of chronic-disease patients. The FDA's human-factors guidance steers manufacturers toward designs that older adults can use correctly on first attempt.

Multicentre Regulatory Compliance Adds Cost & Delays

Europe's MDR and IVDR expansions raise documentation burdens, adding 8-12 months to approvals versus earlier rules. Notified-body reviews elevate compliance costs 25-40% for combination developers. Divergent FDA-EMA classifications force duplicate studies, while Asia-Pacific remains fragmented despite ASEAN harmonization efforts. Without mutual recognition, firms must maintain separate quality systems, inflating overhead and slowing global roll-out of novel therapies within the drug device combination products market.

Other drivers and restraints analyzed in the detailed report include:

- Breakthroughs in Minimally-Invasive & Smart Delivery Platforms

- US FDA's Expedited Combo-Product Pathways Shortening Time-to-Market

- High Recall Rates Linked to Sterility / Dose Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drug-eluting stents retained leadership with a 24.56% share in 2024, reflecting decades of evidence for reduced restenosis. Continued polymer advances extend drug elution beyond 180 days, preserving the segment's dominance in the drug device combination products market. Prefilled syringes, however, are charting a 6.34% CAGR through 2030 as biologics volumes climb and smart sensors log injection events for payers. The drug device combination products market size for prefilled systems is projected to climb markedly as connectivity standards mature and value-based care rewards adherence tracking.

Transdermal patches now use microneedles for macromolecules, expanding into weight-loss therapies. Autoinjectors grow on ergonomic refinements, while wearable injectors turn basal-insulin delivery into a discreet patch experience. Connected inhalers that pair with mobile apps improved asthma-control scores 43% versus conventional devices. Infusion pumps miniaturize for hepatic-artery cancer infusions following Boston Scientific's Intera Oncology buy, strengthening its presence inside the drug device combination products market.

Cardiovascular therapies claimed 35.51% of 2024 revenue, anchored by drug-eluting stents, coated balloons, and rhythm-management implants. Pulsed-field ablation represents the next cardiac frontier and keeps the segment a mainstay in the drug device combination products market. Pain management, however, is on a 6.45% CAGR path as implantable neuromodulation offers a non-opioid alternative and garners insurance coverage. The drug device combination products market size for neuromodulation systems is projected to rise quickly as chronic-pain prevalence climbs.

Diabetes maintains robust momentum through sensor-pump ecosystems. Respiratory disorders benefit from digital inhalers and novel formulations for pulmonary hypertension. Oncology is shifting toward imaging-guided drug delivery that provides immediate feedback on therapeutic placement. Obesity implants and mental-health patches represent emerging categories that could further diversify the drug device combination products industry.

The Drug Device Combination Products Market Report is Segmented by Product (Drug-Eluting Stents, Transdermal Patches, Infusion Pumps, and More), Application (Cardiovascular Diseases, Diabetes, Cancer Therapy, and More), End-User (Hospitals and Clinics, and More), Route of Administration (Oral, Parenteral, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 40.56% of global revenue in 2024, supported by the FDA's clear regulatory architecture and high healthcare spending. Large acquisitions, such as Johnson & Johnson's USD 12.5 billion Shockwave Medical buy, augment cardiac-intervention portfolios and reinforce regional dominance. Digital-health partnerships flourish, enabling connected glucose-monitoring ecosystems that further entrench the drug device combination products market.

Asia-Pacific delivers the fastest 6.82% CAGR through 2030. Manufacturing clusters in China, India, and Vietnam slash sterile-assembly costs, while initiatives like the ASEAN Medical Device Directive streamline cross-border registration. Governments fund R&D tax incentives, and regional CDMOs win global outsourcing contracts, broadening market reach. Singapore and South Korea attract clinical-trial activity through efficient ethics-approval cycles.

Europe continues moderate progress despite MDR-related paperwork. Innovation hubs in Germany, Switzerland, and Ireland lead in connected inhalers and digital neuromodulation. Public-private alliances support pilot programs that integrate reimbursement for data-enabled devices, keeping the region integral to the drug device combination products industry.

- Abbott Laboratories

- Medtronic

- Boston Scientific

- Johnson & Johnson

- Novartis

- GlaxoSmithKline

- Beckton Dickinson

- Terumo

- Stryker

- W. L. Gore & Associates

- Abbvie

- Viatris

- Cook Group

- Hisamitsu Pharmaceutical

- Teva Pharmaceutical Industries

- Solventum

- Phillips-Medisize

- Ypsomed

- AstraZeneca

- Novo Nordisk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden Of Chronic Illnesses Driving Demand for Targeted Combination Therapies

- 4.2.2 Rapidly Ageing Population Boosting Uptake of Self-Administered Delivery Formats

- 4.2.3 Breakthroughs In Minimally-Invasive & Smart Delivery Platforms

- 4.2.4 US FDA's Expedited Combo-Product Pathways Shortening Time-To-Market

- 4.2.5 Connected Inhalers & Patches Enabling Payer-Mandated Adherence Analytics

- 4.2.6 Low-Cost Sterile Assembly Capacity Scaling Up Across Asia Lowers ASPs.

- 4.3 Market Restraints

- 4.3.1 Multicentre Regulatory Compliance Adds Cost & Delays

- 4.3.2 High Recall Rates Linked to Sterility / Dose Accuracy

- 4.3.3 Tight Supply of Specialty Polymers Compatible with Apis

- 4.3.4 Absence Of Unified Reimbursement Codes for Digital Combo Devices

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Drug-Eluting Stents

- 5.1.2 Transdermal Patches

- 5.1.3 Infusion Pumps

- 5.1.4 Drug-Coated Balloons

- 5.1.5 Inhalers

- 5.1.6 Prefilled Syringes

- 5.1.7 Wearable Injectors

- 5.1.8 Autoinjectors

- 5.1.9 Others

- 5.2 By Application

- 5.2.1 Cardiovascular Diseases

- 5.2.2 Diabetes

- 5.2.3 Cancer Therapy

- 5.2.4 Respiratory Disorders

- 5.2.5 Pain Management

- 5.2.6 Others

- 5.3 By End-User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home Care Settings

- 5.3.4 Others

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Parenteral

- 5.4.3 Transdermal

- 5.4.4 Implantable

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Medtronic plc

- 6.3.3 Boston Scientific Corporation

- 6.3.4 Johnson & Johnson

- 6.3.5 Novartis AG

- 6.3.6 GlaxoSmithKline plc

- 6.3.7 Becton, Dickinson and Company

- 6.3.8 Terumo Corporation

- 6.3.9 Stryker Corporation

- 6.3.10 W. L. Gore & Associates, Inc.

- 6.3.11 AbbVie

- 6.3.12 Viatris Inc. (Mylan)

- 6.3.13 Cook Medical

- 6.3.14 Hisamitsu Pharmaceutical

- 6.3.15 Teva Pharmaceutical Industries

- 6.3.16 Solventum

- 6.3.17 Phillips-Medisize

- 6.3.18 Ypsomed AG

- 6.3.19 AstraZeneca plc

- 6.3.20 Novo Nordisk

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment