|

시장보고서

상품코드

1851997

남미의 초음파 기기 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)South America Ultrasound Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

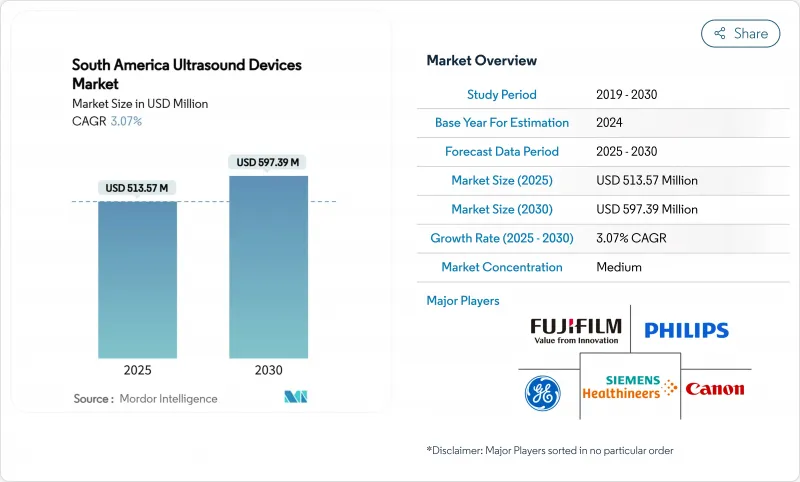

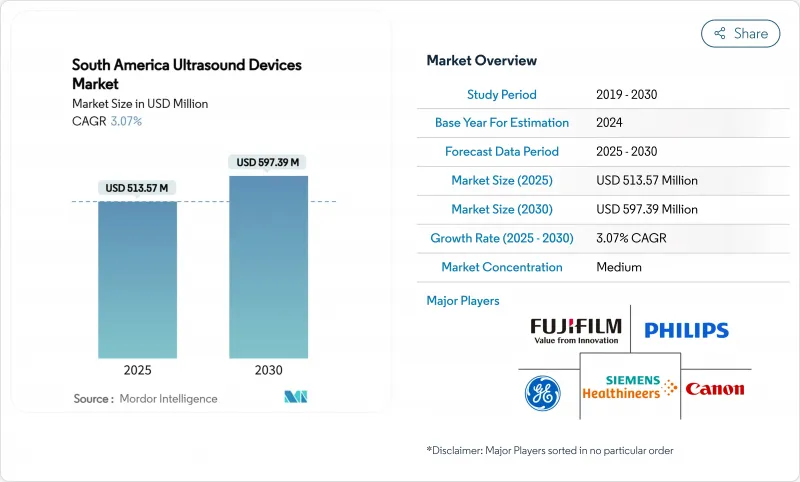

남미의 초음파 기기 시장 규모는 2025년에 5억 1,357만 달러로 추계되고, 2030년에는 5억 9,739만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 3.07%를 나타낼 전망입니다.

현재 성장의 원동력은 보험 상환 범위의 확대, 비감염성 질환 증가, 워크플로우의 효율화와 액세스 확대를 실현하는 AI 대응 시스템 및 무선 시스템의 꾸준한 전개입니다. 브라질은 대규모 설치 기반을 통해 남미의 초음파 기기 시장을 계속 지원하고 있지만, 아르헨티나는 공공 투자와 민간 투자로 이미지 처리 인프라가 현대화되어 성장 속도를 높이고 있습니다. 휴대용형이 2차 도시에 침투해, 의사 부족에 대응해, POC(Point-of-Care)로의 이용이 퍼지고 있습니다. 고밀도 초점 초음파(HIFU)는 종양학의 보조 요법으로 보급되고 있으며 차세대 플랫폼에 대한 수요를 자극하고 있습니다.

남미의 초음파 기기 시장 동향과 인사이트

영상 진료 보상 확대가 초음파 채용을 뒷받침

보험 상환 제도의 확대는 환자의 자기 부담액을 줄이고 의료 제공업체의 경제성을 지원함으로써 남미의 초음파 기기 시장을 강화하고 있습니다. 브라질 메디케어는 현재 조직 파쇄 요법에 평균 1만 7,500달러를 환불하고 병원이 하이 엔드 HIFU 시스템을 구매하도록 격려하고 있습니다. 아르헨티나에서는 예방 검진에 경동맥 초음파 검사와 대퇴골 초음파 검사가 추가되어 무증상 성인의 51%에 경동맥 플라크가 발견되어 조기 발견의 가치가 강조되었습니다. 콜롬비아에서는 원격 초음파 진단에 대한 원격 의료 보험 상환이 확대되어 86%의 시설이 임산부 케어에 ICT를 이용하고 있어 클라우드 연결 프로브에 대한 수요가 높아지고 있습니다. 이러한 정책 전환은 제품 포트폴리오를 상환할 수 있는 절차에 맞추는 공급업체의 인센티브를 강화합니다. 건전한 진료 보상은 현금이 한정된 공공 제도로 운영되는 의료 제공업체의 마진 압력을 더욱 경감합니다.

심장·복부 초음파 수요를 견인하는 비감염성 질환 증가

비감염성 질환은 여전히 이 지역에서 가장 큰 사망 요인으로 일상적인 영상 진단의 필요성을 증가시키고 있습니다. 콜롬비아에서는 2024년에 11만 7,620명의 신규암 환자가 발생하여 종양의 병기 분류와 지침을 위한 실시간 초음파 검사의 보급이 가속화되었습니다. 아르헨티나에서 혈관 초음파 검사는 검사를 받은 성인의 절반 이상에서 잠재성 경동맥 플라크를 감지하여 동맥 경화의 조용한 급증을 시사합니다. 브라질의 노인 인구는 2070년까지 37.8%에 달하며, 평균 수명은 83.9세까지 연장될 수 있으며 만성 질환 관리 업무가 확대됩니다. 지속적인 영상 진단은 특히 심장, 복부, 혈관 평가에서 적시에 개입할 수 있습니다. 결과적으로 병원은 초음파 검사 장비를 늘리고 외래 센터는 일상적인 후속을 위해 휴대용 장치에 중점을 둡니다.

장기화하는 다양한 규제 승인 프로세스

의료기기기업은 제품 출시를 지연시키는 이질적이고 종종 장기간에 걸친 승인틀에 직면하고 있습니다. 브라질 ANVISA는 클래스 III 및 클래스 IV 시스템에 대한 완전한 등록과 브라질 적정 제조 규범 증명서의 취득을 요구하고 있기 때문에 스케줄이 5-6개월 연장됩니다. 2024년 규제는 외국인의 승인에 의존하는 것으로 인정되었지만, 인근 국가들 간에 문서화 규칙이 불일치하기 때문에 여전히 컴플라이언스 비용이 부과됩니다. 이 제약은 소규모 혁신 기업의 시장 진입을 억제하고, 최신 기능에 대한 액세스를 장기화하고, 남미 초음파 기기 시장의 경쟁력을 약화시키고 있습니다.

부문 분석

남미의 초음파 기기 시장에서는 방사선과가 2024년 26.81%의 점유율을 획득하여 패권을 잡았습니다. 이 배경에는 다과목 진단에서 필수적인 역할과 AI를 활용한 측정 도구의 통합이 진행될 수 있습니다. 방사선과의 남미의 초음파 기기 시장 규모는 장기 라벨링을 자동화하는 Siemens Acuson Sequoia 3.5에서 볼 수 있듯이 워크플로의 가속화에 기여했습니다. 순환기과와 산부인과는 스크리닝의 강화에 의해 계속 큰 규모를 유지하고 있으며, 치명타 케어는 신속한 트리아지에 POC(Point-of-Care) 스캐닝을 활용하고 있습니다.

마취과는 2030년까지 연평균 복합 성장률(CAGR) 4.97%를 나타낼 것으로 예측되며 응용 분야에서 가장 빠르게 성장합니다. 초음파 가이드 하 신경 블록의 보급은 절차의 성공과 환자의 결과를 향상시킵니다. 민드레이의 국소 마취 교육 시리즈는 임상의의 숙련도를 강화합니다. 병원의 조달 팀은 휴대용 프로브를 수술실용 카트에 동봉하고, 그 기세를 지속하고 있습니다. 수술 건수 증가와 환자 안전 프로토콜의 강화는 남미의 초음파 기기 시장에서 마취과의 공헌을 계속 촉진할 것으로 보입니다.

3D/4D 기술층은 2024년 남미의 초음파 기기 시장 점유율의 47.27%를 차지하며 태아 평가 및 종양 병기 진단에 필수적인 뛰어난 용적 선명도가 견인했습니다. GE Voluson Signature 20과 같은 AI 지원 플랫폼은 두 번째 트리메스터 검사를 40% 단축하고 효율성을 강조합니다. 전통적인 2D는 AI에 의한 이미지 최적화를 통해 관련성을 유지하며 도플러는 심혈관 평가를 지원합니다.

HIFU 시스템은 2030년까지 연평균 복합 성장률(CAGR) 5.15%를 기록하며, 비침습성 종양 절제의 성공에 힘입어 기술에서 가장 빠릅니다. 간암 조직 파쇄술의 증례 수는 세계에서 300을 넘어 임상적으로 받아들여지고 있는 것을 나타냅니다. 전립선 치료와 자궁 근종 치료로 확대됨에 따라 적응증이 확대되고 치료 플랫폼의 남미의 초음파 기기 시장 규모 확대에 탄력이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 이미지 보험 상환 확대가 초음파 도입을 뒷받침

- 비감염성 질환 부담의 증대가 심장·복부 초음파 수요를 견인

- 워크 플로우의 효율을 높이는 AI 대응 & 무선 초음파 솔루션 채용

- 초음파 영상 진단의 연구 개발에 대한 정부와 민간 자금 지원

- 암 이환율의 상승이 방사선 프리의 이미징 수요를 견인

- 휴대용 및 원격 의료 일체형 초음파 기기의 성장

- 시장 성장 억제요인

- 긴 규제 당국의 승인 프로세스

- 2차 도시에서 인증 초음파 검사사와 방사선 기사의 한정된 이용 가능성

- 높은 설비 비용과 유지 보수 부담

- 원격지 및 미개척 지역에서 액세스 제한

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액 단위 : 달러)

- 용도별

- 마취학

- 심장학

- 산부인과

- 근골격계

- 방사선학

- 중환자 치료

- 기타 용도

- 기술별

- 2D 초음파 영상

- 3D 및 4D 초음파 영상

- 도플러 영상

- 고밀도 집속 초음파(HIFU)

- 기타 기술

- 휴대성별

- 고정형 시스템

- 이동식 카트 기반 시스템

- 휴대용/무선 시스템

- 최종 사용자별

- 병원 및 수술센터

- 진단 영상 센터

- 외래 및 응급 센터

- 기타 최종 사용자

- 국가별

- 브라질

- 아르헨티나

- 칠레

- 콜롬비아

- 기타 남미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Koninklijke Philips NV

- FUJIFILM Holdings Corporation

- Canon Medical Systems Corporation

- Mindray Bio-Medical Electronics Co., Ltd.

- Samsung Medison Co., Ltd.

- Hitachi, Ltd.(Healthcare Solutions)

- Hologic, Inc.

- Esaote SpA

- Konica Minolta, Inc.

- Clarius Mobile Health Corp.

- Butterfly Network, Inc.

- Terason(Teratech Corp.)

- Shimadzu Corp.

- Telemed Medical Systems

- EDAN Instruments Inc.

- Vinno Technology Co. Ltd.

- Landwind Medical

- ContextVision AB

제7장 시장 기회와 향후 전망

KTH 25.11.18The South America Ultrasound Devices Market size is estimated at USD 513.57 million in 2025, and is expected to reach USD 597.39 million by 2030, at a CAGR of 3.07% during the forecast period (2025-2030).

Current growth is driven by wider reimbursement coverage, rising non-communicable diseases, and the steady roll-out of AI-enabled and wireless systems that improve workflow efficiency and expand access. Brazil continues to anchor the South America ultrasound devices market through a large installed base, while Argentina is setting the growth pace as public and private investment modernizes imaging infrastructure. Portable models are penetrating secondary cities, addressing physician shortages and catalyzing wider usage across point-of-care settings. High-intensity focused ultrasound (HIFU) is gaining traction as an adjunct therapy in oncology, stimulating incremental demand for next-generation platforms.

South America Ultrasound Devices Market Trends and Insights

Expansion of Imaging Reimbursement Boosting Ultrasound Adoption

Broader reimbursement schemes are strengthening the South America ultrasound devices market by lowering out-of-pocket costs for patients and supporting provider economics. Brazil's Medicare now reimburses an average USD 17,500 for histotripsy therapy, encouraging hospitals to procure high-end HIFU systems. Argentina added carotid and femoral ultrasound to preventive screening, revealing carotid plaques in 51% of asymptomatic adults, which underscores early detection value. Colombia extended telemedicine reimbursement to remote ultrasound interpretation, with 86% of facilities using ICTs for maternal care, fueling demand for cloud-connected probes. These policy shifts reinforce supplier incentives to align product portfolios with reimbursed procedures. Healthy reimbursement further alleviates margin pressure for providers operating in cash-limited public systems.

Escalating Non-Communicable Disease Burden Driving Demand for Cardiac & Abdominal Ultrasound

Non-communicable diseases remain the largest mortality contributor in the region and elevate routine imaging needs. Colombia recorded 117,620 new cancer cases in 2024, accelerating uptake of real-time ultrasound for tumor staging and guidance. Vascular ultrasound studies in Argentina detected subclinical carotid plaques in more than half of tested adults, signifying a silent surge in atherosclerosis. Brazil's elderly population is set to reach 37.8% by 2070, and life expectancy could climb to 83.9 years, broadening chronic disease management workloads. Continuous imaging underpins timely intervention, particularly for cardiac, abdominal, and vascular assessments. Consequently, hospitals are enlarging their ultrasound fleets while outpatient centers focus on portable devices for routine follow-up.

Prolonged & Divergent Regulatory Approval Processes

Medical device firms face heterogeneous and often lengthy approval frameworks that slow product launches. Brazil's ANVISA requires Class III and Class IV systems to obtain full registration and Brazil-Good Manufacturing Practice certificates, extending timelines by 5-6 months. Although 2024 regulations permit reliance on foreign approvals, discordant documentation rules across neighboring countries still impose added compliance cost. The constraint curbs initial market entrance for smaller innovators and prolongs access to the latest features, dampening the competitive intensity within the South America ultrasound devices market.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of AI-Enabled & Wireless Ultrasound Solutions Enhancing Workflow Efficiency

- Government and Private Funding for R&D in Ultrasound Imaging

- Limited Availability of Certified Sonographers and Radiologists in Secondary Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiology upheld supremacy in the South America ultrasound devices market with 26.81% share in 2024, backed by its integral role in multi-specialty diagnostics and the growing integration of AI-powered measurement tools. The South America ultrasound devices market size for radiology benefited from faster workflow, as seen with Siemens Acuson Sequoia 3.5 that automates organ labeling. Cardiology and gynecology/obstetrics remain sizable due to heightened screening, while critical care leverages point-of-care scanning for rapid triage.

Anesthesiology is projected to log a 4.97% CAGR through 2030, marking the quickest rise among applications. Wider uptake of ultrasound-guided nerve blocks improves procedural success and patient outcomes; Mindray's regional anesthesia education series strengthens clinician proficiency. Hospital procurement teams now bundle portable probes with operating-room carts, sustaining momentum. Rising surgical volumes and enhanced patient safety protocols will continue to propel anesthesiology's contribution to the South America ultrasound devices market.

The 3D/4D technology tier captured 47.27% of the South America ultrasound devices market share in 2024, driven by superior volumetric clarity essential for fetal assessments and oncology staging. AI-enabled platforms like GE Voluson Signature 20 shorten second-trimester exams by 40%, underscoring efficiency gains. Conventional 2D remains relevant through AI-enhanced image optimisation, while Doppler supports cardiovascular evaluation.

HIFU systems will record a 5.15% CAGR to 2030, the fastest among technologies, buoyed by non-invasive tumor ablation success. Liver cancer histotripsy cases surpassing 300 globally demonstrate clinical acceptance. Expansion into prostate and uterine fibroid therapy will widen indications, adding momentum to the South America ultrasound devices market size growth for therapeutic platforms.

The South America Ultrasound Devices Market Report is Segmented by Application (Anesthesiology, Cardiology, Gynecology/Obstetrics, and More), Technology (2D Ultrasound Imaging, and More), Portability (Stationary Systems, and More), End User (Hospitals & Surgical Centers, and More), and Geography (Brazil, Argentina, Chile, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- GE HealthCare Technologies Inc.

- Siemens Healthineers

- Koninklijke Philips

- FUJIFILM

- Canon

- Mindray Bio-Medical Electronics Co., Ltd.

- Samsung Group

- Hitachi, Ltd. (Healthcare Solutions)

- Hologic

- Esaote

- Konica Minolta

- Clarius Mobile Health Corp.

- Butterfly Network, Inc.

- Terason (Teratech Corp.)

- Shimadzu

- Telemed Medical Systems

- EDAN Instruments Inc.

- Vinno Technology Co. Ltd.

- Landwind Medical

- ContextVision AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Imaging Reimbursement Boosting Ultrasound Adoption

- 4.2.2 Escalating Non-Communicable Disease Burden Driving Demand for Cardiac & Abdominal Ultrasound

- 4.2.3 Adoption of AI-Enabled & Wireless Ultrasound Solutions Enhancing Workflow Efficiency

- 4.2.4 Government and Private Funding for R&D in Ultrasound Imaging

- 4.2.5 Rising Cancer Incidence Driving Demand for Radiation-Free Imaging

- 4.2.6 Growth in Portable & Telemedicine-Integrated Ultrasound Devices

- 4.3 Market Restraints

- 4.3.1 Prolonged & Divergent Regulatory Approval Processes

- 4.3.2 Limited Availability of Certified Sonographers and Radiologists in Secondary Cities

- 4.3.3 High Equipment Costs & Maintenance Burden

- 4.3.4 Limited Access in Remote & Underserved Regions

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Application

- 5.1.1 Anesthesiology

- 5.1.2 Cardiology

- 5.1.3 Gynecology / Obstetrics

- 5.1.4 Musculoskeletal

- 5.1.5 Radiology

- 5.1.6 Critical Care

- 5.1.7 Other Applications

- 5.2 By Technology

- 5.2.1 2D Ultrasound Imaging

- 5.2.2 3D & 4D Ultrasound Imaging

- 5.2.3 Doppler Imaging

- 5.2.4 High-intensity Focused Ultrasound (HIFU)

- 5.2.5 Other Technologies

- 5.3 By Portability

- 5.3.1 Stationary Systems

- 5.3.2 Portable Cart-based Systems

- 5.3.3 Handheld / Wireless Systems

- 5.4 By End User

- 5.4.1 Hospitals & Surgical Centers

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Ambulatory Care & Emergency Centers

- 5.4.4 Other End Users

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GE HealthCare Technologies Inc.

- 6.3.2 Siemens Healthineers AG

- 6.3.3 Koninklijke Philips N.V.

- 6.3.4 FUJIFILM Holdings Corporation

- 6.3.5 Canon Medical Systems Corporation

- 6.3.6 Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.7 Samsung Medison Co., Ltd.

- 6.3.8 Hitachi, Ltd. (Healthcare Solutions)

- 6.3.9 Hologic, Inc.

- 6.3.10 Esaote SpA

- 6.3.11 Konica Minolta, Inc.

- 6.3.12 Clarius Mobile Health Corp.

- 6.3.13 Butterfly Network, Inc.

- 6.3.14 Terason (Teratech Corp.)

- 6.3.15 Shimadzu Corp.

- 6.3.16 Telemed Medical Systems

- 6.3.17 EDAN Instruments Inc.

- 6.3.18 Vinno Technology Co. Ltd.

- 6.3.19 Landwind Medical

- 6.3.20 ContextVision AB

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment