|

시장보고서

상품코드

1852036

프랑스의 내시경 검사 기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)France Endoscopy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

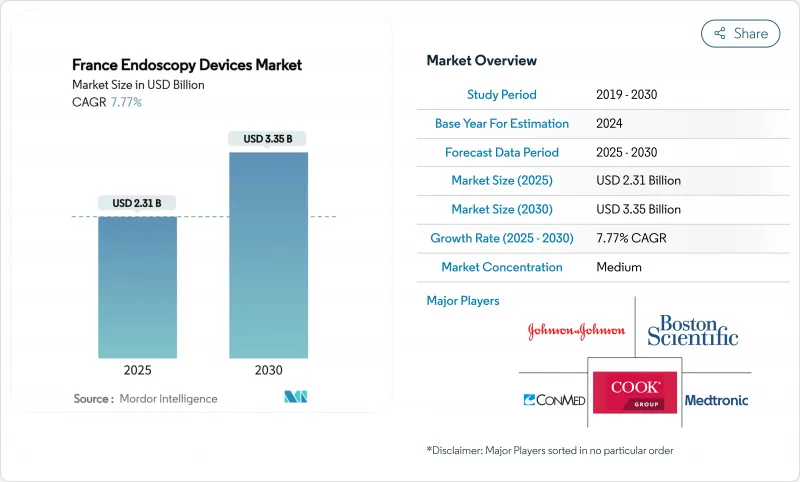

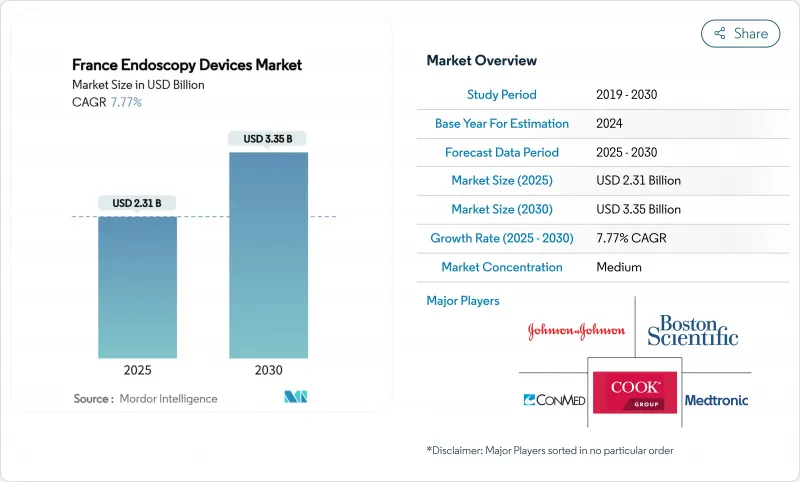

프랑스의 내시경 검사 기기 시장 규모는 2025년에 23억 1,000만 달러로 추정되고, 2030년에는 33억 5,000만 달러에 이를 전망이며, CAGR 7.77%로 성장할 것으로 예측됩니다.

성장 전망은 정부 주도의 암 검진 의무화, AI 지원 화상 처리의 급속한 채용, 감염 관리 효율을 높이는 일회용 플랫폼에 대한 구조적인 축족이 원동력이 되고 있습니다. 민간 보험 적용 확대 및 선택적 수술 외래 센터로의 전환은 프리미엄 장비 수요를 강화하고 있는 반면 EU-MDR 재인증 백로그는 당분간 제품 출시를 억제하고 있습니다. 기존 기업은 고성장의 디스포저블 하위 부문에서 점유율을 확보하기 위해 겨냥한 M&A를 추구하고, 중소의 혁신적 기업은 소화기내과 및 호흡기 내과 워크플로우용으로 설계된 클라우드 기반의 애널리틱스로 차별화를 도모하기 때문에 경쟁의 격렬함은 증가하고 있습니다. 프랑스 전역에서 병원은 예산 한계에 직면하여 교체 주기를 늘리고 있지만 외래 시설은 재처리 가동 중지 시간을 최소화하는 빠른 회전 시스템에 대한 투자를 계속하고 있으며 프랑스 내시경 검사 기기 시장 확대의 다음 단계를 지원합니다.

프랑스 내시경 검사 기기 시장 동향 및 인사이트

진단용 내시경 수요를 높이는 정부의 암 예방 전략

프랑스의 2025-2030년 암 계획에서는 조기 발견이 우선되고, 병원은 시각화 플랫폼의 업그레이드 및 소장 캡슐 프로그램의 확대를 촉구하고 있습니다. 현재 연간 24,000건 이상의 캡슐 수술이 실시되고 있으며, 치료의 다양성보다 진단 정밀도의 우선이 강조되고 있습니다. 가치 기반 조달 기준은 발견에서 치료까지의 간격을 단축하는 시스템에 보상을 주고 놓치는 병변률을 줄이는 AI 지원 대장 내시경 검사에 예산을 돌려줍니다. 스크리닝 프로토콜을 따르는 포트폴리오를 가진 공급업체는 보다 신속한 입찰 승인을 얻어 고화질 이미지의 전국 전개를 강화하고 있습니다. 도시 지역의 종양학 기지에서는 장비 갱신 주기가 지방 동업 타사보다 2년 더 짧다고 보고되었지만, 이는 예방 주도 경로에서 프랑스 내시경 검사 기기 시장을 지원하는 목표로 삼은 자금 조달을 반영합니다.

민간 의료 보험 보급률의 상승이 프리미엄 기기 구입 촉진

보완 보험이 국민 의료비의 14%를 커버하게 되었고, 민간 시설은 4K 내시경 타워와 클라우드 기반 분석 스위트를 우선적으로 구입할 수 있게 되었습니다. 민간 시설에서 인공지능 강화 시스템의 구매율은 공공 부문을 2.3:1로 웃돌고, 제조업체가 자금 조달 모델에 따라 제품을 분할하는 2단 시장을 형성하고 있습니다. 환자의 선호 조사는 AI 유도 진단을 위해 여행하는 의욕이 높아지고 민간 투자의 기세를 강화하고 있습니다. 공공 구매자는 지급액을 진단 수율과 연결하는 위험 분담 계약을 협상함으로써 이에 대응하여 기술 격차를 서서히 줄이고 있습니다. 상환 인센티브와 시설 차별화의 선순환은 프랑스 내시경 검사 기기 시장 전체의 보험료 성장을 지원합니다.

국가 예산의 핍박에 따른 높은 자본 및 운영 비용

2025년 진단 관련 군요금 갱신은 의료기기 인플레이션보다 낮아 공립병원은 장비 라이프사이클을 2.3년 연장할 수밖에 없었습니다. 41%의 시설은 자원을 늘리기 위해 절차의 적합성 임계값을 엄격히 함으로써 대응했습니다. 이 때문에 설비 기반의 노후화가 길어지고 AI 대응 플랫폼의 도입이 늦어져 민간 자금으로 운영되고 있는 동업 타사와의 기술 격차가 발생하고 있습니다. 공급업체는 모듈식 업그레이드 및 기술에 따라 비용을 분산시키는 활용 기반 대출을 제공함으로써 대응하고 있습니다. 그럼에도 불구하고 지속적인 재정 압력은 프랑스 내시경 검사 기기 시장에서 자본 집약형 타워의 단기 상승을 억제합니다.

부문 분석

2024년 프랑스 내시경 검사 기기 시장의 41.1%를 내시경 카테고리가 차지했습니다. 일회용 내시경의 CAGR은 13.6%를 기록하여 재사용형 내시경을 크게 따돌렸습니다. 가이드라인이 준수되었음에도 불구하고, 재처리된 범위의 30%에 생물 부하가 남아 있음이 조사에서 밝혀졌고, 무균 포장된 대체품을 요구하는 목소리가 강해지고 있습니다. 시각화 장치는 병변의 특성화를 자동화하고 지속적인 학습 알고리즘의 데이터 레이크에 공급하는 AI 오버레이 모듈을 뒷받침하며 매출에서 2위를 차지했습니다. 수술 장비는 Micro-Tech가 Creo Medical의 자산을 인수하고 에너지 기반 절제 도구를 확대함으로써 기세를 늘리고 있습니다. 액세서리와 소모품은 안정적인 스톡 스트림을 제공하며 2024년 소화기 내시경 소모품에는 공공 입찰로 273만 유로가 할당되었으며, 이는 2024년 평균 EUR-USD 요금으로 295만 달러에 해당합니다. 캡슐형 플랫폼은 연간 약 24,000건으로, 틈새이지만 꾸준히 채용되고 있습니다. 내시경의 프랑스 내시경 검사 기기 시장 규모는 일회용의 보급이 가속화되고 스케일 메리트에 의한 비용 차가 줄어들면서 확대될 것으로 예측됩니다.

수요의 가속은 리유저블 및 디스포저블 라인을 모두 관리하는 제조업체에게 유리하며, 병원이 서비스 믹스로 플릿(설비)을 조정할 수 있습니다. 올림푸스 및 후지필름은 AI 클라우드와 연동한 하이엔드 타워에 주력하는 반면, 언뷰와 펜탁스는 재활용 노력과 결합한 일회용 카탈로그를 확대하고 있습니다. 지속가능성에 대한 우려로 탄소발자국을 비교하는 수명 주기 분석이 진행되고 있습니다. 최근의 조사 결과에서는 일회용 위 카메라는 재사용 가능한 것에 비해 주로 제조 단계에서 2.5배의 CO2를 배출하는 것으로 지적되고 있습니다. 따라서 시장 리더들은 바이오 핸들과 폐쇄 루프 재활용을 시험적으로 도입하고 환경에 대한 비판을 상쇄하려고 합니다. 이러한 변화를 종합하면 감염 예방, 데이터 통합, 에코디자인이 프랑스 내시경 검사 기기 시장의 다음 장을 어떻게 이끌어 갈지 밝혀집니다.

소화기내과는 2024년 프랑스 내시경 검사 기기 시장 규모의 54.9%를 차지했으며, 대장암 검진의 높은 수준 및 치료 개입의 확대를 반영하고 있습니다. AI 폴립 검출 모듈의 조기 도입은 선종 발견률을 향상시키고 고해상도 대장 내시경에 대한 병원 투자를 강화했습니다. 2024년 4월 ASGE-ESGE 가이드라인에 따라 비만 및 대사 내시경 검사는 BMI 30kg/m2 이상의 환자에게 대상을 확대하여 타워 이용 증가에 박차를 가합니다. 첨단 기관지경 내비게이션, 크라이오 바이옵시, 로봇 플랫폼이 말초 병변을 대상으로 하기 때문에 호흡기 용도는 CAGR 9%와 가장 빠른 궤도를 기록하고 있습니다. 국제 조사에 따르면 인터벤셔널 팔모니스트의 58%가 2년 이내에 새로운 기관지경 기술을 획득할 의향을 보여주며 강력한 파이프라인이 있음을 강조하고 있습니다.

대장암 검진은 전국적인 캠페인에 의해 대변 면역화학 검사 양성자는 30일 이내에 대장 내시경 검사로 이행하여 외래에서의 처리량이 향상되고 있습니다. 비뇨기과는 앙뷰가 무균 워크플로를 간소화하는 일회용 요관경 및 방광경을 출시함으로써 확대되었습니다. 이비인후과 및 부인과는 사무실 환경에서 뛰어난 이미지 해상도를 제공하는 소형 비디오 칩에 의해 지원되며 작지만 안정적입니다. 소화기 내시경의 절대량은 계속 증가하고 있지만, 호흡기 내시경 및 비만 치료의 용도 확대에 의해 소화기 내시경 시장 점유율은 점차 저하해 갈 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 진단용 내시경 수요를 높이는 정부의 암 예방 전략

- 민간 의료 보험 보급률 상승이 프리미엄 기기 구입 촉진

- 선택적 수술의 외래 및 당일치기 수술로의 이행

- HD 화상, 로봇, AI의 기술적 융합이 임상 성과 향상

- 인구 동태의 고령화와 만성 소화기 및 호흡기 질환 부담

- 시장 성장 억제요인

- 국가 예산의 핍박에 따른 높은 자본 비용 및 운영 비용

- 시장 진입을 늦추는 긴 EU-MDR 규제 패스웨이

- 2차 병원에서의 재생 기기 선호

- 규제 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 디바이스 유형별

- 내시경

- 경성 내시경

- 연성 내시경

- 캡슐 내시경

- 일회용 내시경

- 로봇 지원 내시경

- 시각화 장치

- 내시경 카메라

- 이미지 프로세서 및 광원

- 3D/4K 디스플레이 및 기록 시스템

- 수술 기기

- 내시경 치료 및 에너지 시스템

- 흡입기 및 관류 펌프

- 액세서리 및 소모품

- 내시경

- 용도별

- 소화기 내과

- 호흡기 내과

- 정형외과(관절경)

- 순환기

- 이비인후과

- 부인과

- 신경

- 비뇨기과

- 비만 및 대장암 스크리닝

- 기타 용도

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 외래 진단 시설

- 사용별

- 재사용 및 재처리 가능 내시경

- 일회용 내시경

- 리프로세스 기기 및 소모품

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Olympus Corporation

- Karl Storz SE & Co. KG

- Boston Scientific Corporation

- Fujifilm Holdings Corporation

- Medtronic plc

- Johnson & Johnson(Ethicon)

- Stryker Corporation

- Commed Corporation

- Cook Medical LLC

- Smith Nephew plc

- Ambu A/S

- Pentax Medical(Hoya)

- Richard Wolf GmbH

- B. Braun Melsungen AG

- Zimmer Biomet Holdings Inc.

- Arthrex Inc.

- Cantel Medical(Steris)

- EndoMedical Innovations SA

- Laborie Medical Technologies

- Erbe Elektromedizin GmbH

제7장 시장 기회 및 향후 전망

AJY 25.11.26The France endoscopy devices market size stands at USD 2.31 billion in 2025 and is forecast to reach USD 3.35 billion by 2030, advancing at a 7.77% CAGR.

The growth outlook is powered by government-led cancer screening mandates, rapid adoption of AI-assisted imaging, and a structural pivot toward single-use platforms that heighten infection control efficiency. Heightened private insurance coverage and the migration of elective procedures to ambulatory centers are reinforcing premium-device demand, while the EU-MDR recertification backlog is constraining near-term product launches. Competitive intensity is rising as incumbents pursue targeted M&A to secure share in the high-growth disposable subsegment, and smaller innovators differentiate through cloud-based analytics designed for gastroenterology and pulmonology workflows. Across France, hospitals face budget ceilings that stretch replacement cycles, yet ambulatory sites continue to invest in rapid-turnover systems that minimize reprocessing downtime, underpinning the next phase of the France endoscopy devices market expansion.

France Endoscopy Devices Market Trends and Insights

Government Cancer-Prevention Strategy Elevating Demand for Diagnostic Endoscopy

France's 2025-2030 cancer plan prioritizes early detection, prompting hospitals to upgrade visualization platforms and expand small-bowel capsule programs. More than 24,000 capsule procedures are now performed annually, underscoring a preference for diagnostic accuracy over therapeutic versatility. Value-based procurement criteria reward systems that shorten detection-to-treatment intervals, redirecting budgets toward AI-assisted colonoscopy that cuts missed-lesion rates. Vendors that align portfolios with screening protocols gain faster tender approvals, reinforcing the nationwide rollout of high-definition imaging. Urban oncology hubs report equipment renewal cycles two years shorter than rural peers, reflecting targeted financing that supports the France endoscopy devices market in prevention-led pathways.

Rising Private Health-Insurance Penetration Fuelling Premium Device Purchases

Complementary insurance now covers 14% of national health spending, enabling private facilities to prioritize 4K endoscopy towers and cloud-based analytics suites. Acquisition rates for AI-enhanced systems in private centers outpace the public sector by 2.3:1, creating a two-speed market where manufacturers segment offerings by funding model. Patient preference surveys show a growing willingness to travel for AI-guided diagnostics, reinforcing private investment momentum. Public purchasers respond by negotiating risk-sharing contracts that tie payments to diagnostic yield, gradually narrowing the technology gap. The virtuous cycle between reimbursement incentives and facility differentiation anchors premium growth across the France endoscopy devices market.

High Capital & Operating Costs Under National Budget Pressure

The 2025 Diagnosis Related Group tariff update trailed device inflation, forcing public hospitals to prolong equipment life cycles by 2.3 years. Forty-one percent of facilities responded by tightening procedural appropriateness thresholds to stretch resources. This prolongs installed-base aging and slows uptake of AI-ready platforms, creating a technology gap against privately funded peers. Suppliers counter by offering modular upgrades and usage-based financing that spread cost over procedure volume. Sustained fiscal pressure nevertheless caps near-term upside for capital-intensive towers within the France endoscopy devices market.

Other drivers and restraints analyzed in the detailed report include:

- Migration of Elective Procedures to Outpatient & Day-Surgery Settings

- Technological Convergence of HD Imaging, Robotics & AI Elevating Clinical Outcomes

- Lengthy EU-MDR Regulatory Pathway Slowing Market Entry

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The endoscopes category accounted for 41.1% of the France endoscopy devices market in 2024, anchored by widespread use in digestive and respiratory procedures. Disposable scopes now record a 13.6% CAGR, well ahead of reusable models, as infection-control priorities outweigh unit-price premiums. Studies revealed residual bioburden on 30% of reprocessed scopes despite guideline adherence, intensifying calls for sterile-packed alternatives. Visualization equipment ranks second in revenue, buoyed by AI overlay modules that automate lesion characterization and feed data lakes powering continuous-learning algorithms. Operative devices enjoy momentum after Micro-Tech's purchase of Creo Medical assets, which broadened its energy-based resection tools. Accessories and consumables provide stable recurring streams, with public tenders allocating EUR 2.73 million for digestive endoscopy disposables in 2024, equal to USD 2.95 million using the 2024 average EUR-USD rate. Capsule platforms complete the mix with roughly 24,000 annual procedures, underscoring niche yet steady adoption. The France endoscopy devices market size for endoscopes is projected to widen as single-use uptake accelerates, narrowing cost differentials via economies of scale.

Demand acceleration favors manufacturers that control both reusable and disposable lines, enabling hospitals to tailor fleets by service mix. Olympus and Fujifilm focus on high-end towers linked to AI clouds, whereas Ambu and Pentax expand single-use catalogs paired with recycling initiatives. Sustainability concerns prompt life-cycle analyses comparing carbon footprints; recent findings note single-use gastroscopes emit 2.5 times more CO2 than reusable counterparts, mainly in the production phase. Market leaders therefore pilot bio-based handles and closed-loop recycling that could offset environmental criticism. Cumulatively, these shifts underscore how infection prevention, data integration and eco-design will jointly steer the next chapter of the France endoscopy devices market.

Gastroenterology controlled 54.9% of the France endoscopy devices market size in 2024, reflecting high colorectal cancer screening volumes and expanded therapeutic interventions. Early adoption of AI polyp-detection modules increased adenoma-find rates, reinforcing hospital investment in high-resolution colonoscopes. Bariatric and metabolic endoscopy gains traction under April 2024 ASGE-ESGE guidelines that widened eligibility to patients with BMI >= 30 kg/m2, fueling incremental tower utilization. Pulmonology applications record the fastest trajectory at a 9% CAGR as advanced bronchoscopic navigation, cryobiopsy and robotic platforms target peripheral lesions. An international survey showed 58% of interventional pulmonologists intend to acquire new bronchoscopic technology within two years, highlighting a robust pipeline.

Colorectal cancer screening benefits from national campaigns that push fecal immunochemical test positives to colonoscopy within thirty days, hiking procedural throughput at ambulatory units. Urology broadens as Ambu launches single-use ureteroscopes and cystoscopes that simplify sterile workflow. ENT and gynecology remain smaller but stable, supported by compact video chips that deliver superior image resolution in office settings. The France endoscopy devices market share held by gastroenterology will gradually erode as pulmonology and bariatric indications expand, yet absolute volume in digestive endoscopy continues to rise.

The France Endoscopy Devices Market Report is Segmented by Device Type (Endoscopes, Visualization Equipment, Operative Devices, and Accessories & Consumables), Application (Gastroenterology, Pulmonology, Cardiology, ENT Surgery, Gynecology, Neurology, and More), End User (Public Hospitals, Private Hospitals & Clinics, and More), Usage (Reprocessable Endoscopes, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Olympus

- Karl Storz

- Boston Scientific

- FUJIFILM

- Medtronic

- Johnson & Johnson

- Stryker

- Conmed

- Cook Group

- Smith + Nephew plc

- Ambu

- Pentax Medical

- Richard Wolf

- B. Braun

- Zimmer Biomet

- Arthrex

- Cantel Medical

- EndoMedical Innovations SA

- Laborie Medical Technologies

- Erbe Elektromedizin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Cancer-Prevention Strategy Elevating Demand for Diagnostic Endoscopy

- 4.2.2 Rising Private Health-Insurance Penetration Fuelling Premium Device Purchases

- 4.2.3 Migration of Elective Procedures to Outpatient & Day-Surgery Settings

- 4.2.4 Technological Convergence of HD Imaging, Robotics & AI Elevating Clinical Outcomes

- 4.2.5 Ageing Demographics & Burden of Chronic GI and Respiratory Diseases

- 4.3 Market Restraints

- 4.3.1 High Capital & Operating Costs Under National Budget Pressure

- 4.3.2 Lengthy EU-MDR Regulatory Pathway Slowing Market Entry

- 4.3.3 Preference for Refurbished Equipment in Secondary Hospitals

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Endoscopes

- 5.1.1.1 Rigid Endoscopes

- 5.1.1.2 Flexible Endoscopes

- 5.1.1.3 Capsule Endoscopes

- 5.1.1.4 Disposable / Single-Use Endoscopes

- 5.1.1.5 Robot-Assisted Endoscopes

- 5.1.2 Visualization Equipment

- 5.1.2.1 Endoscopy Cameras

- 5.1.2.2 Image Processors & Light Sources

- 5.1.2.3 3-D / 4-K Display & Recording Systems

- 5.1.3 Operative Devices

- 5.1.3.1 Endotherapy & Energy Systems

- 5.1.3.2 Insufflators & Irrigation Pumps

- 5.1.4 Accessories & Consumables

- 5.1.1 Endoscopes

- 5.2 By Application

- 5.2.1 Gastroenterology

- 5.2.2 Pulmonology

- 5.2.3 Orthopedic (Arthroscopy)

- 5.2.4 Cardiology

- 5.2.5 ENT Surgery

- 5.2.6 Gynecology

- 5.2.7 Neurology

- 5.2.8 Urology

- 5.2.9 Bariatric & Colorectal Cancer Screening

- 5.2.10 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centres

- 5.3.3 Out-Patient Diagnostic Facilities

- 5.4 By Usage

- 5.4.1 Reusable / Reprocessable Endoscopes

- 5.4.2 Single-Use / Disposable Endoscopes

- 5.4.3 Reprocessing Equipment & Consumables

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Olympus Corporation

- 6.3.2 Karl Storz SE & Co. KG

- 6.3.3 Boston Scientific Corporation

- 6.3.4 Fujifilm Holdings Corporation

- 6.3.5 Medtronic plc

- 6.3.6 Johnson & Johnson (Ethicon)

- 6.3.7 Stryker Corporation

- 6.3.8 Conmed Corporation

- 6.3.9 Cook Medical LLC

- 6.3.10 Smith + Nephew plc

- 6.3.11 Ambu A/S

- 6.3.12 Pentax Medical (Hoya)

- 6.3.13 Richard Wolf GmbH

- 6.3.14 B. Braun Melsungen AG

- 6.3.15 Zimmer Biomet Holdings Inc.

- 6.3.16 Arthrex Inc.

- 6.3.17 Cantel Medical (Steris)

- 6.3.18 EndoMedical Innovations SA

- 6.3.19 Laborie Medical Technologies

- 6.3.20 Erbe Elektromedizin GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment