|

시장보고서

상품코드

1852092

임상시험 이미징 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Clinical Trial Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

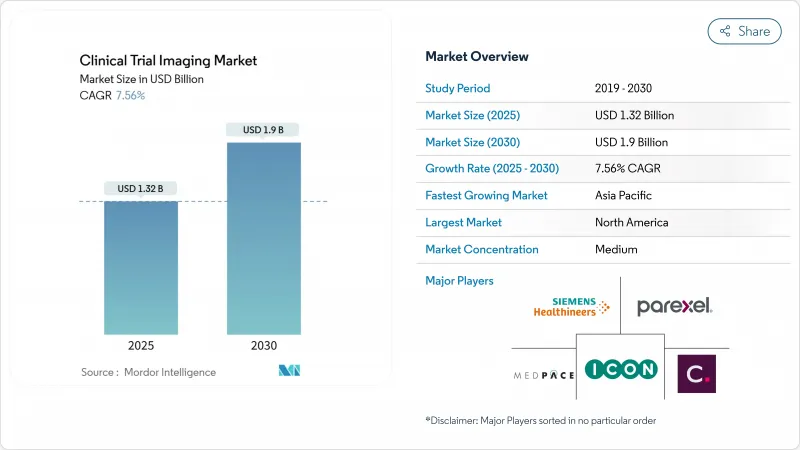

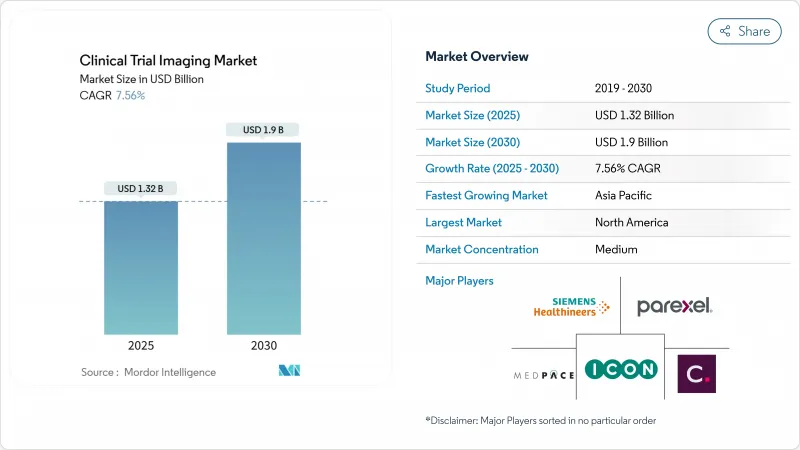

임상시험 이미징 시장 규모는 2025년에 13억 2,000만 달러로 추정되고, 2030년에는 19억 달러에 이를 것으로 예측되며, CAGR 7.56%로 성장할 전망입니다.

이 확대는 세계적인 의약품 연구개발 예산의 급증, 복잡한 시험에서의 이미지 바이오마커의 이용 증가, AI를 활용한 데이터 분석으로의 꾸준한 전환을 반영하고 있습니다. 종양학과 신경학의 임상시험은 치료 가치를 증명하기 위한 시각적 종점에 의존하기 때문에 수요의 대부분을 차지합니다. 반면에 분산형 및 하이브리드형 임상시험 모델은 환자 풀에 대한 액세스를 확대하고 등록 일정을 가속화하고 있습니다. 인공지능의 도입으로, 이미지 판독의 가속화, 독자의 편차 감소, 여러 시설에 걸친 프로그램의 프로토콜 준수 개선이 진행되고 있습니다. 하드웨어, 소프트웨어, 애널리틱스를 번들로 엔드 투 엔드 서비스를 제공하기 위해 이미징 진단의 핵심 시설과 모더리티 벤더의 통합이 진행되고 있습니다. EU 임상시험규칙(EU CTR)으로 대표되는 규제의 변화는 국경을 넘어서는 프로세스의 조화를 도모하고 표준화된 이미지 워크플로우를 권장합니다.

세계의 임상시험 이미징 시장 동향 및 인사이트

의약품 및 바이오테크놀러지 연구개발비 증가

주요 의약품 제조업체의 연구개발 예산은 2024년 9.7% 증가했으며, 파이프라인은 현재 8,000건을 넘어 치료 효과를 객관적으로 추적하는 이미징 평가 항목에 대한 수요가 높아지고 있습니다. 2030년까지 신규 승인의 60% 이상을 차지할 것으로 예상되는 생물제제와 유전자 치료는 분자 수준의 가시화를 필요로 하는 경우가 많으며, 스폰서는 정교한 이미징 코어 랩의 지원을 확보할 필요가 있습니다. 엘리 릴리와 같은 대기업은 GLP-1 프로그램에 대한 투자를 확대하고 있으며, 각 프로토콜에는 대사 및 심혈관 매개변수를 모니터링하기 위한 특수 MRI 또는 PET가 포함되어 있습니다. 아웃소싱이 확대되는 가운데 대륙을 가로질러 이미징 서비스를 확장할 수 있는 공급업체는 두드러지며 연구개발 간부의 80% 이상이 외부 파트너에 대한 지출을 2자리 증가로 계획하고 있습니다. 이 자금 조달의 기세는 임상시험 이미징 시장에 장기적인 추풍이 될 것입니다.

CRO(의약품 개발 업무 수탁 기관)에 대한 화상 진단 서비스 아웃소싱의 확대

CRO 매출은 2023년 521억 9,000만 달러에 이르렀으며, 고정비 절감 및 시험 실시 가속화를 위해 외부 이미징 진단 전문가로 의약품 개발 기업이 전략적으로 축족을 옮기고 있음을 반영합니다. 아이콘은 단독으로 2024년 중 99억 7,400만 달러의 신규 비즈니스 획득을 보고하고 있으며 프로토콜의 정합화, 실시간 QC, 자동화된 AI 분석이 가능한 통합 이미징 네트워크에 대한 스폰서의 의욕을 뒷받침하고 있습니다. 아웃소싱은 이미지 데이터를 중앙 집중화하고 미리 정의된 읽기 알고리즘을 적용하여 테스트 기간을 최대 30% 단축할 수 있습니다. 이 장점은 지역 시설 및 환자 집에서 스캔을 수집하는 하이브리드 및 분산 모델로 확대됩니다. CRO는 치료 영역 전반에 걸친 서비스의 폭을 넓히기 위해 텔레라디올로지, 안과 이미징, 정량적 바이오마커 플랫폼을 타겟으로 하는 인수로 수요를 충족하고 있습니다.

이미징 진단 장비의 높은 설비 투자 및 운영 비용

최신 PET-MRI 시스템은 400만-600만 달러가 들고 광자 계수 CT 플랫폼은 설치, 차폐, 유지보수를 고려하기 전에 200만-300만 달러의 부담이 더해집니다. 핵 의학 프로그램은 엄격한 cGMP 기준을 충족하는 현장 방사성 의약품 시설이 필요하며 많은 지역의 CRO 및 아카데믹 코어 랩을 훨씬 초과하는 총 창업 비용을 절감할 수 있습니다. 빠른 하드웨어 주기는 ROI 계산을 더욱 복잡하게 하여 이해관계자들을 규모의 경제를 확보하기 위한 어피니티 에퀴티 파트너스의 6억 5,800만 달러 규모의 루머스 이미징 인수에서 볼 수 있듯이 합병이나 전략적 제휴를 추진하고 있습니다.

부문 분석

이미징 소프트웨어는 2024년 임상시험 이미징 시장의 32.33%를 차지했으며, 세계 기지 간 데이터 흐름의 백본으로 자리매김하고 있습니다. 이러한 플랫폼은 QC를 자동화하고 데이터 세트를 익명화하며 전자 데이터 수집 시스템과 원활하게 통합하여 오류율을 낮추고 일관성을 보장합니다. 수익 측면에서 이 부문은 임상시험 이미징 시장 규모에서 가장 큰 슬라이스를 형성하고 있으며, AI 모듈이 파일럿에서 프로덕션으로 전환함에 따라 그 영향력이 확대될 것으로 보입니다. SaaS 전개 모델의 상승으로 예산은 설비 투자에서 옥스로 이동하고 있으며, 많은 인프라 투자 없이 확장성을 요구하는 중소규모의 후원자에게 매력적입니다.

한편, 이미지 바이오마커 개발 서비스는 CAGR 9.45%로 확대될 것으로 예측되고 있습니다. 이는 규제 당국과 지불자를 설득할 수 있는 검증된 정량적 엔드포인트에 대한 수요 증가를 반영합니다. 이러한 급성장의 배경은 신속한 승인에서 이미지 바이오마커의 가치를 강조하는 FDA의 노력과 치료 반응의 고감도 측정이 필요한 맞춤형 치료에 대한 움직임을 포함합니다. 소프트웨어, 바이오마커 과학, 약사 컨설팅을 융합시킨 벤더가 이익률이 높은 프로젝트를 획득하고 있으며, 임상시험 이미징 시장의 이 성장 영역에서의 경쟁이 격화되고 있습니다.

컴퓨터 단층 촬영은 그 편재성, 신속한 촬영 시간, 고형암 임상시험에 있어서 유효한 역할에 의해 2024년에는 임상시험 이미징 시장의 25.23%를 차지했습니다. 그 이점은 또한 대규모 3상 시험에 필수적인 요소인 상환 지원과 광범위한 독자들에게 잘 알려져 있습니다. 그럼에도 불구하고 스폰서가 더 낮은 선량의 광자 계수 시스템과 연조직의 변화를 더 잘 해상하는 하이브리드 이미징으로 축발을 옮기고 있기 때문에 이 양식의 점유율은 점차 감소하고 있습니다.

양전자 방사선 단층 촬영은 2030년까지 연평균 복합 성장률(CAGR)이 9.57%로 모달리티 중 가장 빨라질 것으로 예측됩니다. 성장의 핵심은 포도당 대사에 그치지 않고 세포 표면 수용체, 저산소 마커 및 아밀로이드 응집체를 표적으로하는 새로운 방사선 추적기의 파이프라인입니다. PET는 해부학적 변화에 앞서 분자 변화를 감지하는 민감도가 높기 때문에 조기 용량 반응 연구 및 적응 시험 설계에 유용합니다. 선량을 줄이고 처리량을 향상시키는 전신 PET 스캐너의 보급은 PET의 매력을 더욱 두드러지게 하고 임상시험 이미징 시장에서의 역할을 확대하고 있습니다.

지역 분석

북미는 성숙한 보험상환제도, 산학연계의 치밀한 네트워크, 이미징진단 엔드포인트를 관리하는 FDA의 명확한 가이던스를 강점으로 2024년 세계매출의 38.54%를 유지했습니다. 미국은 또한 제약 후원자 상위 20개 기업을 많이 보유하고 있으며, 치료 프랜차이즈에 걸쳐 확장 가능한 고처리량 코어 실험실에 대한 국내 수요를 높이고 있습니다. 프라이빗 주식에 의한 투자와 인수(RadNet은 2024년에 대상에 5,400만 달러를 투자), 이미지 처리 능력이 통합되어 AI 플랫폼이 통합되어 이 지역의 경쟁의 해자가 깊어지고 있습니다.

아시아태평양은 2030년까지 CAGR 8.67%로 가장 높은 성장이 예측되며, 윤리 승인의 합리화 및 매력적인 비용 구조에 뒷받침되고 있습니다. 일본, 한국, 싱가포르의 규제 당국은 임상시험 신청을 6개월 이내에 완료하는 것을 일상적으로 실시하고 있어, 종래 시장에 비해 시험 개시까지의 기간이 단축되고 있습니다. 무석 AppTec과 같은 지역 CRO는 국내 및 서양 스폰서에 서비스를 제공하는 이미징 부문을 확장하고 광범위한 조사 시설 네트워크 및 정부 인센티브를 활용하여 다국적 프로그램을 수락하고 있습니다. 분산 임상시험, 원격 이미징 진단, BYOD(Bring-Your-Own-Device) 이미징 진단 앱의 인기 증가는 APAC의 임상시험 이미징 시장에서의 역할을 강화하고 있습니다.

유럽은 2025년 1월까지 임상시험 정보 시스템의 완전한 이용을 의무화하는 EU CTR로 전환하기 위해 양극의 중간에 위치하고 있습니다. 통일된 포털은 30개국에서 일관된 신청 심사를 약속하고 국경을 넘어선 이미지 프로토콜의 관리상의 오버헤드를 줄여야 합니다. 그러나 방사성 의약품의 취급 및 데이터 프라이버시에 관한 규칙이 특히 독일과 프랑스에서 다르다는 것이 장애가 되고 있습니다. EMA가 AI에 대한 리플렉션 페이퍼를 발표하고 검증에 대한 기대를 명확히 하는 노력을 하고 있다는 것은 운영이 진화해도 유럽이 거버넌스의 주도적 지위를 유지하는 것을 목표로 하고 있음을 나타냅니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의약품 및 바이오테크놀러지 연구개발비 증가

- 수탁 연구 기관에 대한 화상 진단 서비스의 아웃소싱 확대

- 메디컬 이미징 모달리티의 기술적 진보

- 임상시험 이미징에 있어서 인공지능 채용 증가

- 암 영역과 신경 영역의 임상시험 성장

- 분산형 및 하이브리드형 임상시험 모델의 확대

- 시장 성장 억제요인

- 이미징 진단 장치의 높은 설비 투자 및 운용 비용

- 숙련된 이미징 진단 전문가 부족

- 엄격한 규제 및 데이터 프라이버시 요건

- 임상시험 간에 표준화된 이미징 진단 프로토콜의 부족

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 및 서비스별

- 시험 디자인 컨설팅 서비스

- 독영 분석 서비스

- 오퍼레이션 이미징 서비스

- 이미징 소프트웨어

- 이미징 데이터 관리 서비스

- 이미징 바이오마커 개발 서비스

- 모달리티별

- 자기 공명 이미징

- 컴퓨터 단층 촬영

- PET

- 초음파

- 심 에코 검사

- 기타 모달리티

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 수탁연구기관

- 의료기기 제조업체

- 학술 및 정부연구기관

- 치유 영역별

- 종양

- 신경학

- 심장병학

- 내분비 및 대사질환

- 희귀질환

- 기타 치료 영역

- 임상시험 페이즈별

- 페이즈 I

- 페이즈 II

- 페이즈 III

- 페이즈 IV

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Clario

- Icon plc

- IXICO plc

- Parexel International Corp.

- Medpace Holdings, Inc.

- Navitas Clinical Research

- WorldCare Clinical LLC

- Radiant Sage LLC

- Resonance Health

- WCG(WIRB-Copernicus Group)

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Calyx

- Signant Health

- Imaging Endpoints

- Perspectum Diagnostics

- BioClinica Inc.

- Collective Minds Research(CMRAD)

제7장 시장 기회 및 향후 전망

AJY 25.11.26The clinical trial imaging market size stands at USD 1.32 billion in 2025 and is poised to reach USD 1.90 billion by 2030, advancing at a 7.56% CAGR.

This expansion mirrors the surge in global pharmaceutical R&D budgets, the growing use of imaging biomarkers in complex studies, and the steady migration toward AI-enabled data analysis. Oncology and neurology trials dominate demand because they rely on visual endpoints to prove therapeutic value, while decentralized and hybrid trial models are widening access to patient pools and accelerating enrollment timelines. AI adoption is speeding image interpretation, cutting reader variability, and improving protocol compliance across multi-site programs. Consolidation among imaging core laboratories and modality vendors is intensifying as firms bundle hardware, software, and analytics to deliver end-to-end services. Regulatory shifts-most notably the European Union Clinical Trials Regulation (EU CTR)-are harmonizing processes across borders and encouraging standardized imaging workflows.

Global Clinical Trial Imaging Market Trends and Insights

Increasing Pharmaceutical and Biotechnology R&D Expenditure

R&D budgets climbed 9.7% in 2024 among large drug makers, and pipelines now exceed 8,000 active assets, deepening demand for imaging endpoints that objectively track therapeutic impact. Biologics and gene therapies-expected to represent more than 60% of new approvals by 2030-often require molecular-level visualization, pushing sponsors to secure sophisticated imaging core lab support. Leading firms such as Eli Lilly have extended investments in GLP-1 programs, and each protocol embeds specialized MRI or PET components to monitor metabolic and cardiovascular parameters. As outsourcing grows, suppliers able to scale imaging services across continents stand out, with over 80% of R&D executives planning double-digit spending increases on external partners. This funding momentum anchors a long-term tailwind for the clinical trial imaging market.

Growing Outsourcing of Imaging Services to Contract Research Organizations

CRO revenues hit USD 52.19 billion in 2023, reflecting a strategic pivot by drug developers toward external imaging expertise to cut fixed costs and speed trial execution. ICON alone reported USD 9.974 billion in new business wins during 2024, underscoring sponsor appetite for integrated imaging networks capable of protocol harmonization, real-time QC, and automated AI analytics. Outsourcing can trim study timelines by up to 30% by centralizing image data and applying predefined read algorithms, advantages magnified in hybrid and decentralized models that collect scans from community sites and patients' homes. CROs are matching demand with targeted acquisitions in teleradiology, ophthalmic imaging, and quantitative biomarker platforms to widen service breadth across therapeutic areas.

High Capital Investment and Operational Costs of Imaging Equipment

State-of-the-art PET-MRI systems can cost USD 4-6 million, and photon-counting CT platforms add another USD 2-3 million burden before siting, shielding, and maintenance are factored in. Nuclear medicine programs require on-site radiopharmaceutical facilities that meet stringent cGMP standards, lifting total start-up spending far beyond many regional CROs or academic core labs. Rapid hardware cycles further complicate ROI calculations, pushing stakeholders toward mergers or strategic alliances, as seen in Affinity Equity Partners' USD 658 million purchase of Lumus Imaging aimed at gaining scale economies.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Medical Imaging Modalities

- Rising Adoption of Artificial Intelligence in Clinical Trial Imaging

- Shortage of Skilled Imaging Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Imaging software accounted for 32.33% of the clinical trial imaging market in 2024, cementing its status as the backbone of data flow across global sites. These platforms automate QC, anonymize datasets, and integrate seamlessly with electronic data capture systems, lowering error rates and ensuring consistency. In revenue terms, the segment formed the largest slice of the clinical trial imaging market size, and its influence will grow as AI modules move from pilot to production. The rise of SaaS deployment models is shifting budgets from capex to opex, appealing to small and mid-sized sponsors seeking scalability without heavy infrastructure outlay.

Imaging biomarker development services, meanwhile, are projected to expand at a 9.45% CAGR, reflecting escalating demand for validated, quantitative endpoints capable of persuading regulators and payers. Underpinning this surge are FDA initiatives that underscore the value of imaging biomarkers in accelerated approvals, and the movement toward personalized therapies that require sensitive measures of treatment response. Vendors that fuse software, biomarker science, and regulatory consulting are capturing higher-margin projects, intensifying competition in this growth pocket of the clinical trial imaging market.

Computed tomography held 25.23% of the clinical trial imaging market in 2024 thanks to its ubiquity, rapid acquisition times, and validated role in solid tumor trials. Its dominance also stems from reimbursement support and wide reader familiarity, factors essential to large phase III studies. Even so, the modality's share is slowly eroding as sponsors pivot to lower-dose photon-counting systems and hybrid imaging that better resolve soft-tissue changes.

Positron emission tomography is expected to post a 9.57% CAGR through 2030, the fastest among modalities. Growth hinges on a pipeline of novel radiotracers that move beyond glucose metabolism to target cell-surface receptors, hypoxia markers, and amyloid aggregates. PET's sensitivity in detecting molecular changes ahead of anatomical shifts makes it invaluable for early dose-response studies and adaptive trial designs. The spread of total-body PET scanners, which cut dose and bolster throughput, further sharpens its appeal and enlarges its role within the clinical trial imaging market.

The Clinical Trial Imaging Market Report is Segmented by Product & Service (Trial Design Consulting Services, and More), Modality (Magnetic Resonance Imaging, and More), Phase of Clinical Trial (Phase I, and More), End-User (Pharmaceutical & Biotechnology Companies, and More), Therapeutic Area (Oncology, and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.54% of global revenue in 2024 on the strength of mature reimbursement systems, a dense network of academic-industrial partnerships, and clear FDA guidance governing imaging endpoints. The United States also hosts many of the top 20 pharma sponsors, amplifying domestic demand for high-throughput core labs that can scale across therapeutic franchises. Private-equity investments and acquisitions-RadNet spent USD 54 million on targets in 2024-are consolidating imaging capacity and integrating AI platforms, deepening the region's competitive moat.

Asia-Pacific is projected to deliver the highest regional CAGR at 8.67% through 2030, propelled by streamlined ethics approvals and attractive cost structures. Regulatory agencies in Japan, South Korea, and Singapore routinely finalize clinical trial applications within six months, shortening study start-up compared with legacy markets. Local CROs such as Wuxi AppTec have scaled imaging units that serve domestic and Western sponsors alike, leveraging broad site networks and government incentives to host multinational programs. The growing popularity of decentralized trials, tele-radiology, and bring-your-own-device imaging apps augments APAC's role in the clinical trial imaging market.

Europe sits between these poles as it transitions to the EU CTR, which mandates full use of the Clinical Trials Information System by January 2025. The unified portal promises consistent application reviews across 30 countries and should lower administrative overhead on cross-border imaging protocols. Yet divergent rules governing radiopharmaceutical handling and data privacy remain obstacles, particularly in Germany and France. Efforts by the EMA to publish an AI reflection paper and clarify validation expectations indicate that Europe aims to retain a leadership position in governance even as operational execution evolves.

- Clario

- Icon plc

- IXICO

- Parexel International Corp.

- Medpace Holdings, Inc.

- Navitas Clinical Research

- WorldCare Clinical LLC

- Radiant Sage

- Resonance Health

- WCG (WIRB-Copernicus Group)

- Siemens Healthineers

- GE HealthCare Technologies Inc.

- Calyx

- Signant Health

- Imaging Endpoints

- Perspectum Diagnostics

- BioClinica Inc.

- Collective Minds Research (CMRAD)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pharmaceutical and Biotechnology R&D Expenditure

- 4.2.2 Growing Outsourcing of Imaging Services to Contract Research Organizations

- 4.2.3 Technological Advancements in Medical Imaging Modalities

- 4.2.4 Rising Adoption of Artificial Intelligence in Clinical Trial Imaging

- 4.2.5 Growth in Oncology and Neurology Clinical Trials

- 4.2.6 Expansion of Decentralized and Hybrid Clinical Trial Models

- 4.3 Market Restraints

- 4.3.1 High Capital Investment and Operational Costs of Imaging Equipment

- 4.3.2 Shortage of Skilled Imaging Professionals

- 4.3.3 Stringent Regulatory and Data Privacy Requirements

- 4.3.4 Lack of Standardized Imaging Protocols Across Trial Sites

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Trial Design Consulting Services

- 5.1.2 Read Analysis Services

- 5.1.3 Operational Imaging Services

- 5.1.4 Imaging Software

- 5.1.5 Imaging Data-management Services

- 5.1.6 Imaging Biomarker Development Services

- 5.2 By Modality

- 5.2.1 Magnetic Resonance Imaging

- 5.2.2 Computed Tomography

- 5.2.3 Positron Emission Tomography

- 5.2.4 Ultrasound

- 5.2.5 Echocardiography

- 5.2.6 Other Modalities

- 5.3 By End-User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Contract Research Organizations

- 5.3.3 Medical Device Manufacturers

- 5.3.4 Academic & Government Research Institutes

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Neurology

- 5.4.3 Cardiology

- 5.4.4 Endocrinology & Metabolic Disorders

- 5.4.5 Rare Diseases

- 5.4.6 Other Therapeutic Areas

- 5.5 By Phase of Clinical Trial

- 5.5.1 Phase I

- 5.5.2 Phase II

- 5.5.3 Phase III

- 5.5.4 Phase IV

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Clario

- 6.3.2 Icon plc

- 6.3.3 IXICO plc

- 6.3.4 Parexel International Corp.

- 6.3.5 Medpace Holdings, Inc.

- 6.3.6 Navitas Clinical Research

- 6.3.7 WorldCare Clinical LLC

- 6.3.8 Radiant Sage LLC

- 6.3.9 Resonance Health

- 6.3.10 WCG (WIRB-Copernicus Group)

- 6.3.11 Siemens Healthineers AG

- 6.3.12 GE HealthCare Technologies Inc.

- 6.3.13 Calyx

- 6.3.14 Signant Health

- 6.3.15 Imaging Endpoints

- 6.3.16 Perspectum Diagnostics

- 6.3.17 BioClinica Inc.

- 6.3.18 Collective Minds Research (CMRAD)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment