|

시장보고서

상품코드

1905993

석고 보드 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Plasterboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

석고 보드 시장은 2025년에 122억 5,000만 평방미터로 평가되었고, 2026년 128억 5,000만 평방미터에서 2031년까지 163억 1,000만 평방미터에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 4.88%를 나타낼 전망입니다.

이러한 성장 추세는 건식 시공 기술의 가속화된 도입, 더욱 엄격해진 친환경 건축 규정, 그리고 합성 석고 공급망의 확장을 반영합니다. 프로젝트 주기 단축을 원하는 건설사들은 노동 시간을 줄여주는 경량 보드를 선택하고 있으며, 규제 당국은 재활용 성분이 포함된 석고 솔루션을 선호하는 저휘발성 유기화합물(VOC) 요구 사항을 시행하고 있습니다. 아시아태평양 지역의 급속한 도시화, 걸프 지역의 메가 프로젝트, 북미 및 유럽의 상업용 부동산 회복은 석고보드의 잠재적 시장을 확대하고 있습니다. 석탄 의존 경제권에서 플루 가스 탈황 설비에서 생산되는 가격 경쟁력 있는 합성 석고는 원자재 비용을 낮추며 제조업체의 생산량 확대를 촉진하고 있습니다. 주요 브랜드들이 매립지 규제를 준수하고 지속가능성 측면에서 차별화를 위해 폐쇄형 재활용 시스템을 도입함에 따라 경쟁 강도는 더욱 높아질 전망입니다.

세계의 석고 보드 시장 동향 및 인사이트

습식 공법에서 건식 공법으로의 급속한 전환

건설사들은 노동 효율성과 예측 가능한 일정 관리 측면에서 건식 시스템을 선호합니다. NEOM과 같은 사우디의 초대형 개발 프로젝트는 현장 경화 지연을 최소화하기 위해 표준화된 건식 벽체 조립을 지정합니다. 건축 규정은 이제 일관된 품질과 수분 결함 감소로 건식 벽체를 인정하고 있습니다. 수요가 설치 도구, 조인트 컴파운드, 마감 액세서리로 확산되면서 석고보드 시장이 확대되고 있습니다. 제조업체들은 사전 제작 모듈과 호환되는 더 얇고 치수 안정성이 뛰어난 보드를 개발하고 있습니다.

아시아 및 GCC 지역의 주거 메가 프로젝트 계획이 수요량 확대를 주도

인도, 인도네시아, 사우디아라비아의 도시화 정책은 판재 생산업체와의 장기 공급 계약을 기반으로 한 대규모 주택 프로그램을 추진 중입니다. 2035년까지 1조 4천억 달러 규모의 인도 인프라 계획은 지역 제조업체들의 생산 능력 확장을 뒷받침합니다. 집적 개발은 물류 거리를 단축하고 일관된 판재 사양을 촉진하여 규모의 경제를 강화합니다.

습기 민감성과 곰팡이 위험 증가로 인한 복구 비용

습기가 많은 보드는 곰팡이 발생을 초래하여 주택 1호당 평균 15,000-5만 달러의 보험 청구를 유발합니다. 해안 지역 건축 당국은 이제 내습 등급을 지정하지만, 이러한 제품은 15-25% 더 비쌉니다. 일부 개발사는 고위험 지역에 섬유 시멘트 제품을 전환합니다. 신흥 지역에서는 증기 차단막을 올바르게 설치할 숙련된 인력이 부족하여 석고보드 시장 도입이 지연되고 있습니다.

부문 분석

테이퍼드 엣지 보드는 2025년 석고보드 시장 점유율의 61.42%를 차지했습니다. 오목한 가장자리는 이음매 마감 작업을 단순화하며 주거용 인테리어의 기본 옵션으로 유지되고 있습니다. 모듈식 건축이 확산되면서 테이퍼드 보드 석고보드 시장 규모는 전체 수요보다 느린 성장세를 보일 전망입니다. 물류 및 산업 프로젝트 건축가들이 미니멀리즘 디자인에 부합하는 노출 조인트를 점점 더 채택함에 따라 스퀘어 엣지 제품은 2031년까지 연평균 5.03% 성장할 것으로 예상됩니다.

스퀘어 엣지 보드는 공장 생산 건축에 사용되는 금속 프레임 및 사전 마무리 패널과 원활하게 통합되어 연마 및 퍼티 사용의 필요성을 줄입니다. 시공업체는 숙련도가 낮은 노동시간의 삭감을 주요 이점으로 꼽고 있습니다. 한편, 주택 소유자와 인테리어 리모델링 업체는 여전히 테이퍼드 엣지가 실현하는 원활한 외관을 선호합니다. 제조업체는 속도와 미관의 균형을 맞추는 마이크로 베벨 가공 가장자리가있는 하이브리드 보드를 판매합니다. 이는 석고 보드 시장에서 모양 선호도의 수렴을 나타내는 징후입니다.

석고 보드 시장 보고서는 형상(스퀘어 엣지, 테이퍼드 엣지), 유형(표준, 내화, 단열, 내습, 방음, 내충격), 최종 용도 분야(주거용과 비주거용), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 예측은 수량(제곱미터) 단위로 제공됩니다.

지역별 분석

아시아태평양 석고보드 시장은 지속적인 공공 주택 사업과 드라이월을 기본으로 채택하는 공장 건설로 혜택을 보고 있습니다. 지역 발전소에서 조달된 합성 석고는 비용을 낮추고 경쟁력 있는 가격을 지원합니다. 정부는 보드 두께 기준을 높이는 내진 및 방화 규정을 채택하여 제곱미터당 평균 재료 집약도를 높이고 있습니다.

중동 및 아프리카 지역은 사우디아라비아, 쿠웨이트, 이집트의 초대형 프로젝트를 통해 보드 소비량을 확대하고 있습니다. 가혹한 기후 조건과 촉박한 공사 일정은 내습성과 경량 보드의 매력을 높입니다. 현지 생산자들은 세계의 대기업과 협력하여 기술 이전을 촉진하고 공동 물류 네트워크를 구축함으로써 수입 의존도를 낮추고 있습니다.

유럽은 순환 경제 목표를 강조하며, 회수 제도와 거의 제로에 가까운 폐기물 처리 성과를 달성한 공장에 인센티브를 제공합니다. 영국 석고(British Gypsum)의 재생 소재 함유 SoundBloc 라인은 엄격한 매립 제한 기준을 충족합니다. 북미는 재생 에너지로 전력을 조달하는 전기화 공장에 투자하며, 이 지역을 탄소 제로 보드 생산의 시험장으로 자리매김하고 있습니다. 라틴 아메리카는 1인당 소비량에서는 뒤처지지만 상업용 인테리어 현대화와 연계된 점진적 성장을 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 습식 공법에서 건식 공법으로의 급속한 이행

- 아시아 및 GCC 지역의 주거용 메가 프로젝트 추진으로 수요량 증가

- 강화된 친환경 건축 규정으로 저휘발성 유기화합물(VOC), 고재활용 함량 보드 의무화

- 흥 시장의 가격 경쟁력 있는 합성 석고 공급으로 채택 확대

- 서구 지역의 재활용 등급 석고 부족으로 폐쇄형 순환 시스템 투자 촉진

- 시장 성장 억제요인

- 습기 민감성과 곰팡이 위험 증가로 인한 보수 비용 상승

- 석고 및 에너지 가격의 변동이 생산자의 마진 압박

- 석고 폐기물에 대한 엄격한 매립 금지 조치로 인한 처리 비용 증가

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 형태별

- 스퀘어 엣지

- 테이퍼드 엣지

- 유형별

- 표준

- 내화성

- 단열성

- 내습성

- 방음성

- 내충격성

- 용도별

- 주거

- 비주거

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율**/랭킹 분석

- 기업 프로파일

- Ahmed Yousuf & Hassan Abdullah Co.(AYHACO)

- American Gypsum Company LLC

- AtIskan AlcI

- AWI Licensing LLC

- CSR Limited

- Etex Group

- Fletcher Building

- Georgia-Pacific

- GYPSEMNA CO LLC

- Gyptec Iberica

- Holcim

- Jason New Materials

- Knauf Group

- Mada Gypsum Company

- National Gypsum Services Company

- Saint-Gobain

- USG Boral

- VOLMA

제7장 시장 기회와 장래의 전망

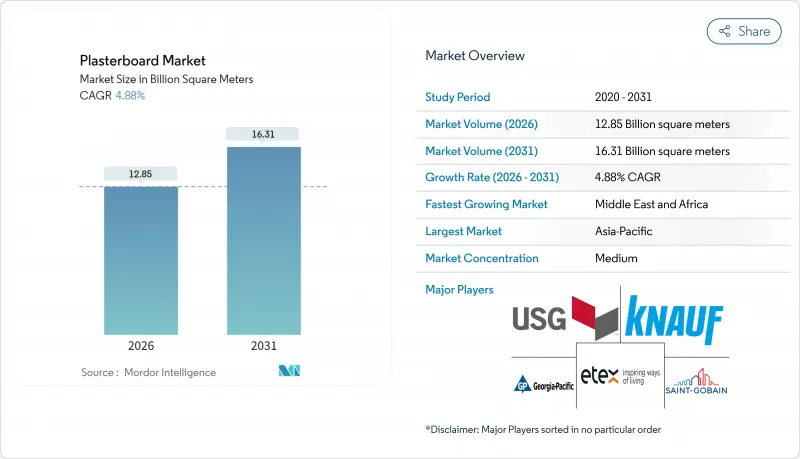

HBR 26.01.26The Plasterboard Market was valued at 12.25 Billion square meters in 2025 and estimated to grow from 12.85 Billion square meters in 2026 to reach 16.31 Billion square meters by 2031, at a CAGR of 4.88% during the forecast period (2026-2031).

This growth trajectory reflects the accelerating adoption of dry construction techniques, stricter green-building mandates, and the expansion of synthetic gypsum supply chains. Contractors seeking shorter project cycles are opting for lightweight boards that reduce labor hours, while regulators are implementing low-VOC requirements that favor gypsum solutions formulated with recycled content. Rapid urbanization in the Asia-Pacific, megaprojects in the Gulf, and commercial real-estate recovery in North America and Europe are widening the addressable plasterboard market. Price-competitive synthetic gypsum sourced from flue-gas desulfurization plants in coal-reliant economies is lowering raw material costs, encouraging manufacturers to scale up their output. Competitive intensity is poised to rise as leading brands deploy closed-loop recycling systems to comply with landfill restrictions and differentiate on sustainability.

Global Plasterboard Market Trends and Insights

Rapid Shift Toward Dry Construction Techniques Over Wet Methods

Builders favor dry systems for labor efficiency and predictable timelines. Saudi mega-developments, such as NEOM, specify standardized drywall assemblies to minimize on-site curing delays. Building codes now recognize drywall for its consistent quality and reduced moisture defects. Demand is spreading to installation tools, joint compounds, and finishing accessories, enlarging the plasterboard market. Manufacturers are engineering thinner, dimensionally stable boards compatible with prefabricated modules.

Residential Megaproject Pipelines in Asia and GCC Boost Volume Demand

Urbanization policies in India, Indonesia, and Saudi Arabia are driving mass housing programs that anchor long-term supply contracts with board producers. India's infrastructure plan valued at USD 1.4 trillion up to 2035 underpins capacity expansions by regional manufacturers. Clustered developments reduce logistics miles and promote consistent board specifications, reinforcing economies of scale.

Moisture Sensitivity and Mold Risk Increase Remediation Costs

Boards that remain damp can foster mold, triggering insurance claims that average USD 15,000-50,000 per dwelling. Building authorities in coastal zones now specify moisture-resistant grades, yet these products cost 15-25% more. Some developers switch to fiber cement in high-risk sites. Skilled labor for correct vapor-barrier installation is limited in emerging regions, which slows the uptake of plasterboard in the market.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Green-Building Codes Mandate Low-VOC, High-Recycled-Content Boards

- Price-Competitive Synthetic Gypsum Supply in Emerging Markets Widens Adoption

- Volatile Gypsum and Energy Prices Squeeze Producer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tapered-edge boards commanded 61.42% of the plasterboard market share in 2025. Their recessed edges simplify joint finishing and remain the default for residential interiors. The plasterboard market size for tapered boards is expected to grow at a slower pace than overall demand as modular construction gains ground. Square-edge products are projected to advance at a 5.03% CAGR through 2031, as architects in logistics and industrial projects increasingly adopt exposed joints that align with minimalist design.

Square-edge boards integrate seamlessly with metal framing and pre-finished panels used in factory-built construction, reducing the need for sanding and compound use. Contractors cite lower-skilled labor hours as the chief gain. In contrast, homeowners and interior renovators still prefer the seamless appearance enabled by tapered edges. Manufacturers are marketing hybrid boards with micro-beveled edges that balance speed and aesthetics, a sign of converging form preferences within the plasterboard market.

The Plasterboard Market Report is Segmented by Form (Square-Edge and Tapered), Type (Standard, Fire-Resistant, Thermal-Insulated, Moisture-Resistant, Sound-Resistant, and Impact-Resistant), End-Use Sector (Residential and Non-Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Square Meters).

Geography Analysis

The Asia-Pacific's plasterboard market benefits from sustained public housing initiatives and factory construction that adopts drywalling as the default. Synthetic gypsum sourced from regional power plants lowers costs and supports competitive pricing. Governments are adopting seismic and fire regulations that increase board thickness standards, pushing average material intensity per square meter higher.

The Middle East and Africa region is scaling board consumption through giga-projects in Saudi Arabia, Kuwait, and Egypt. Harsh climate conditions and rapid schedules make moisture-resistant and lightweight boards attractive. Local producers partner with global majors to facilitate technology transfer and establish joint logistics networks, thereby reducing import dependency.

Europe emphasizes circular economy objectives, rewarding plants with take-back schemes and near-zero-waste performance. British Gypsum's recycled-content SoundBloc line meets stringent landfill limits. North America invests in electrified factories sourcing renewable power, positioning the region as a testing ground for zero-carbon board production. Latin America lags in per-capita consumption but is seeing gradual growth tied to commercial interiors modernization.

- Ahmed Yousuf & Hassan Abdullah Co. (AYHACO)

- American Gypsum Company LLC

- AtIskan AlcI

- AWI Licensing LLC

- CSR Limited

- Etex Group

- Fletcher Building

- Georgia-Pacific

- GYPSEMNA CO LLC

- Gyptec Iberica

- Holcim

- Jason New Materials

- Knauf Group

- Mada Gypsum Company

- National Gypsum Services Company

- Saint-Gobain

- USG Boral

- VOLMA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift toward dry construction techniques over wet methods

- 4.2.2 Residential megaproject pipelines in Asia and GCC boost volume demand

- 4.2.3 Tightening green-building codes mandate low-VOC, high-recycled-content boards

- 4.2.4 Price-competitive synthetic gypsum supply in emerging markets widens adoption

- 4.2.5 Recycling-grade gypsum shortages in the West spur investment in closed-loop systems

- 4.3 Market Restraints

- 4.3.1 Moisture sensitivity and mould risk increase remediation costs

- 4.3.2 Volatile gypsum/energy prices squeeze producer margins

- 4.3.3 Stringent landfill bans on gypsum waste raise disposal costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Square-edge

- 5.1.2 Tapered

- 5.2 By Type

- 5.2.1 Standard

- 5.2.2 Fire-resistant

- 5.2.3 Thermal-insulated

- 5.2.4 Moisture-resistant

- 5.2.5 Sound-resistant

- 5.2.6 Impact-resistant

- 5.3 By End-use Sector

- 5.3.1 Residential

- 5.3.2 Non-residential

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Nordic Countries

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Ahmed Yousuf & Hassan Abdullah Co. (AYHACO)

- 6.4.2 American Gypsum Company LLC

- 6.4.3 AtIskan AlcI

- 6.4.4 AWI Licensing LLC

- 6.4.5 CSR Limited

- 6.4.6 Etex Group

- 6.4.7 Fletcher Building

- 6.4.8 Georgia-Pacific

- 6.4.9 GYPSEMNA CO LLC

- 6.4.10 Gyptec Iberica

- 6.4.11 Holcim

- 6.4.12 Jason New Materials

- 6.4.13 Knauf Group

- 6.4.14 Mada Gypsum Company

- 6.4.15 National Gypsum Services Company

- 6.4.16 Saint-Gobain

- 6.4.17 USG Boral

- 6.4.18 VOLMA

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment