|

시장보고서

상품코드

1906016

금속 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

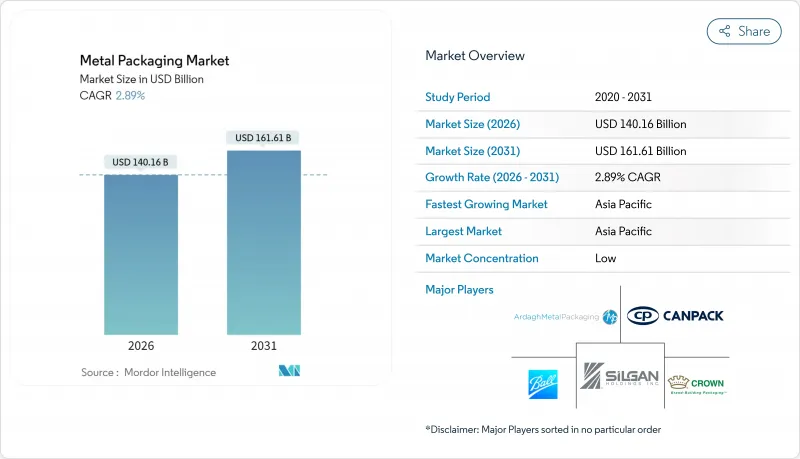

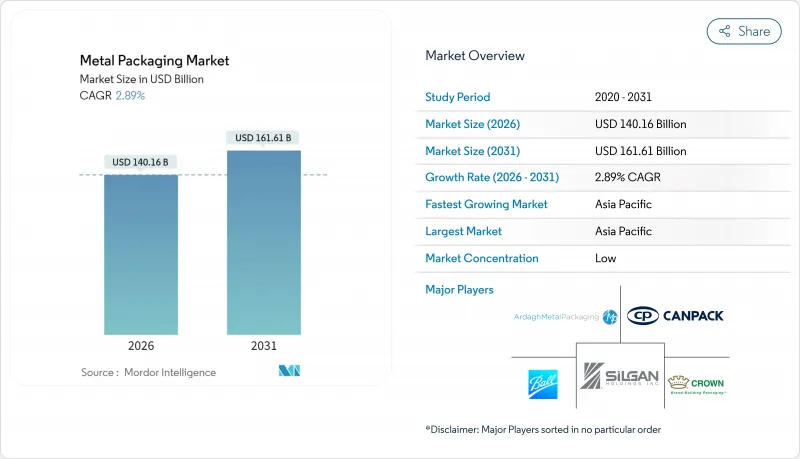

금속 포장 시장은 2025년 1,362억 2,000만 달러에서 2026년 1,401억 6,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 2.89%로 성장을 지속하여 2031년까지 1,616억 1,000만 달러에 다다를 전망입니다.

이 꾸준한 성장은 순환 경제에 대한 법 규제, RTD 음료의 고급화, 소매업체의 플라스틱을 금속으로 대체하려는 노력에 의해 발생합니다. 알루미늄의 뛰어난 재활용 경제성과 재료 경량화의 진전, 브랜드 오너의 스코프 3 배출 저감 목표가 결합되어, 금속 포장 시장은 탄산 음료나 기능성 음료에서의 기본 선택으로서의 지위를 강화하고 있습니다. 제조업체는 장기 계약 및 스크랩 기반 공급 전략을 통해 알루미늄 및 강재 가격의 변동 위험을 계속 헤지하고 있습니다. 한편 코팅 공급업체는 소비자 안전에 대한 요구를 지원하는 BPA 프리 화학물질로의 이행을 가속화하고 있습니다. 경쟁 구도는 중간 정도에 머물러 있지만, 주요 캔 제조업체는 성숙하면서도 기회가 풍부한 시장 환경에서 점유율을 지키기 위해 코팅, 재활용, 디지털 인쇄 능력의 수직 통합을 강화하고 있습니다.

세계의 금속 포장 시장의 동향 및 인사이트

순환형 경제에 대한 요구가 캔의 재활용 순환 촉진

규제 강화로 알루미늄 캔이 달성한 최저 재생재 함량 의무화가 밸류체인 경제를 재구축하고 금속 포장 시장에 컴플라이언스 우위를 가져오고 있습니다. EU의 PPWR(포장 폐기물 지침)은 2030년까지 음료 용기의 재생재 함유율을 30%로 요구하지만, 알루미늄 캔의 평균 재생재 함유율은 71%에 달하고 있습니다. 보증금 반환 시스템은 회수율을 2029년까지 90%로 높여 예측 가능한 스크랩 공급을 뒷받침하고 신규 금속에 대한 의존도를 줄일 전망입니다. 볼사와 같은 세계적인 제조업체들은 85%의 재생재 사용을 목표로 하고 있으며 원료 비용 위험을 완화하는 폐쇄 루프의 효율성을 강화하고 있습니다. 호주는 EU 규정에 따라 2040년까지 식품용 캔의 80%를 소비 후 재생재로 하는 기준을 도입했습니다. 지속적인 규제 기세는 특히 음료 분야의 조달 과정에서 순환성 점수가 공급자의 입찰 평가에 통합됨에 따라, PET에 대한 알루미늄의 우위성을 확고하게 하고 있습니다.

신흥 아시아에서의 RTD 음료 고급화

프리미엄 캔 음료 수요 급증이 아시아태평양의 금속 포장 시장 성장을 가속화하고 있습니다. 일본에서는 2018년부터 2023년에 걸쳐 저칼로리 및 저알코올 음료를 요구하는 소비자층에 의해 캔 츄하이 시장이 3배로 확대되었습니다. 아사히의 '나마조키'와 같은 브랜드는 포장 기술의 혁신이 가정 환경에서 주점에서의 경험을 재현하는 좋은 사례입니다. 중국과 인도의 가처분 소득 증가는 프리미엄 RTD 커피, 콤부차 및 기능성 식이 대체 음료를 일반 소매 시장으로 변화시키고 있으며, 이들 모두가 풍미 보호와 단열 성능을 위해 캔에 의존하고 있습니다. 프리미엄화의 물결은 제조업체가 원재료 비용 상승을 소비자에게 전가하게 하여 알루미늄 가격의 변동에도 불구하고 이익률을 유지합니다.

LME 알루미늄 및 강재의 가격 변동성

에너지 가격 변동으로 인한 제품 가격 변동은 금속 포장 시장이 여전히 현물 시세 변동에 뒤처지는 전가 조항 계약에 의존하기 때문에 이익률을 압박합니다. 북미 관세는 복잡성을 높이고 생산자는 경쟁력을 보호하기 위해 위험 회피 수단과 지역 조달을 결합해야 합니다. 유럽의 제련소는 지속적인 에너지 비용 압력에 직면하고 있으며, 이는 세계 가격 변동의 원인이 되었습니다. 대기업은 스크랩 원료나 다년간 계약으로 변동을 상쇄하고 있지만, 중소 컨버터는 여전히 영향을 받기 쉽고, 이는 설비 투자 사이클의 둔화로 이어질 수 있습니다.

부문 분석

2025년 시점에서 알루미늄은 금속 포장 시장의 42.80%를 차지하였고 PPWR 규제를 충족하는 폐쇄 루프 재활용 시스템의 혜택으로 2031년까지 연평균 복합 성장률(CAGR) 3.57%로 확대될 전망됩니다. 강철은 대형 식품 용기나 산업용 드럼통 분야에서 존재감을 유지하지만, 중량과 에너지 효율의 관점에서 성장은 완만합니다. 노벨리스가 캔 재활용 능력 증강을 위해 영국에서 9,000만 달러를 투자한 확장 계획은 이 소재의 전략적 중요성을 뒷받침하고 있습니다. 알루미늄의 경량성은 물류 배출량을 저감하고 ESG 스코어 카드와의 무결성을 높임과 동시에 음료 브랜드에서 고객 충성도의 강화에 기여하고 있습니다. 시장 진출기업은 재용해 기술에 대한 투자를 계속하고 있으며, 이는 2차 알루미늄과 관련된 금속 포장 시장 규모의 꾸준한 확대를 가능하게 하고 있습니다.

2차 알루미늄의 가격 이점은 브랜드가 신규 금속에 비해 원재료 비용을 관리하고 조달 위험을 줄이는 데 도움이 됩니다. 힌달코의 100억 달러 규모 생산 능력 계획은 통합된 제련 및 재활용 거점이 공급망을 단축하고 적극적인 재생재 함량 목표를 지원하는 방법을 시사합니다. 강철의 자기 회수성은 혼합 폐기물 스트림에서 여전히 이점이지만, 용기 중량 증가는 탄소세의 보급에 따라 운송 비용을 밀어 올리고 있습니다. 종합적으로 보면 알루미늄의 비용, 순환성, 중량면에서의 우위성은 그 주도적 지위를 확고하게 하고 있습니다. 한편, 강철은 기계적 강도와 뚫림 강도를 선호하는 견조한 틈새 시장에서 주도적 역할을 담당합니다.

2025년 시점에서 금속 포장 시장의 41.12%를 차지한 캔은 세계 간편 음료 채널에서 RTD 커피, 하드 셀처, 기능성 음료의 고급화를 배경으로 CAGR 6.08%로 확대될 것으로 전망됩니다. 볼사의 다이너마크 어드밴스드 프로 가변 그래픽 시스템은 대규모 맞춤 캔 생산을 가능하게 하고, 마케팅 담당자의 참여 향상과 매장에서의 호소력 강화를 뒷받침합니다. 식품 캔은 안정적인 기반을 유지하고 토마토 페이스트, 수프, 반려동물 식품의 세계 무역을 지원하는 높은 장벽 보호 특성을 제공합니다. 에어로졸 캔은 팬데믹 이후 수요 회복으로 신흥 시장에서 헤어 스타일링, 데오도란트 및 가정용 세제 부문에서 성장하는 개인 관리 분야를 흡수합니다.

경량화 이니셔티브는 강도를 손상시키지 않고 단위당 알루미늄 사용량을 줄여 비용 억제 및 스코프 3 배출량 감소에 기여합니다. 캡, 마개, 러그 뚜껑은 변조 방지 기능과 편의성을 제공하여 틈새 시장에서의 존재감을 유지합니다. 벌크 드럼과 중간 강철 컨테이너는 재사용성과 유엔 운송 인증이 중요한 농약 및 식용유 분야에서 인기를 유지하고 있습니다. 이러한 동향이 더하여 금속 포장 시장의 주력 제품으로서 캔의 지위를 확고히 하고, 재료 과학과 디자인 혁신을 통해 주변 부문이 진화하고 있습니다.

지역별 분석

아시아태평양은 2025년 금속 포장 시장의 38.21%를 차지하였으며 중국의 급성장하는 RTD 부문과 인도의 중산층 확대를 바탕으로 2031년까지 연평균 복합 성장률(CAGR) 5.89%로 추이할 전망입니다. 현지에서 생산된 캔용 강판 공급과 힌달코에 의한 수십억 달러 규모의 제련소 및 리사이클 시설 확장 계획이 결합하여 비용 우위성과 순환형 경제에 공헌하여, 세계의 브랜드 오너의 관심을 모으고 있습니다. 일본은 디자인면에서 리더십을 발휘해, 고품질의 츄하이 용기를 수출하여 지역의 도입 패턴에 영향을 주고 있습니다. 한편, 동남아시아 국가들은 관광 수요에 뒷받침된 음료 수요와 도입이 진행되는 보증금 반환제도의 파일럿 사업을 활용하고 있습니다.

북미는 성숙시장이며 주요 맥주 및 청량음료 충전업자와의 장기 공급 계약으로 국내 캔 생산 라인은 거의 완전 가동을 유지하고 있습니다. 관세제도에 의해 캔 제조업체는 국내 금속 조달을 요구받고, 스크랩 기반의 빌릿 시설이나 창고 자동화에 대한 투자가 촉진되어, 단가 비용 절감이 진행되고 있습니다. 주 수준의 광범위한 정책에 의해 알루미늄 회수율은 60% 이상을 유지하고 있으며, 이는 2차 생산 원료의 공급 안정성을 높이고 있습니다.

유럽에서는 엄격한 PPWR(제품 포장 폐기물 규제) 요건과 첨단 재활용 네트워크가 융합되어 코팅 기술 혁신과 디지털 워터마크 시험의 기준 지역이 되고 있습니다. 스페인과 이탈리아에 거점을 두는 크라운사의 확장 가능한 공장에서는 크래프트 맥주 수출업체용으로 고속 라인을 신설하여 포화 시장에서도 지속적인 성장 기회가 있음을 보여줍니다. 브라질을 필두로 하는 남미에서는 맥주 브랜드가 프리미엄화와 물류 효율화를 목적으로 캔 포장으로 전환하는 움직임으로 인해, 수요량이 견조하게 성장하고 있습니다.

중동 및 아프리카는 인프라 면에서 뒤처져 있지만, 인구 증가와 소득 향상에 의해 에어로졸식 데오도란트나 통조림 식품 시장 침투를 향한 신규 참가의 기회가 발생하여, 지역 전체적으로 세계의 금속 포장 시장의 성장에 공헌하는 것이 확실시되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 순환형 경제의 의무화가 캔의 재활용 루프를 촉진

- 신흥 아시아 시장에서의 RTD 음료 프리미엄화

- 소매업체의 플라스틱을 금속으로 대체하려는 노력

- 높은 스크랩 회수율로 인해 PET 대비 실질 비용 저감

- 캔 내 QR/NFC 기술에 의한 소비자 데이터의 수익화 실현

- 전자상거래 및 DTC 음료 소매업 확대

- 억제요인

- LME 알루미늄 및 강재의 가격 변동성

- 스코프 3 CO2 배출량에 대한 브랜드 소유자의 반발

- 단일 소재 종이 병의 상승

- 금속 포장의 높은 생산 비용 및 운용 비용

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 지정학적 시나리오가 시장에 미치는 영향

- 투자분석

제5장 시장 규모 및 성장 예측

- 재료 유형별

- 알루미늄

- 철강

- 제품 유형별

- 캔

- 식품 통조림

- 음료 캔

- 에어로졸 캔

- 벌크 컨테이너

- 드럼통 및 드럼의 수송

- 뚜껑 및 마개

- 캔

- 최종 사용자 업계별

- 음료

- 식품

- 화장품 및 퍼스널케어

- 가정

- 기타 최종 사용자 산업

- 코팅 및 라이닝 유형별

- BPA 에폭시 수지

- BPA-NI 에폭시 수지

- 폴리에스테르 및 PET

- 기타 코팅 및 라이닝 유형

- 컨테이너 용량별

- 250ml 미만

- 251-500 ml

- 501-1000 ml

- 1000ml 이상

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Ardagh Metal Packaging SA

- Ball Corporation

- Crown Holdings Inc.

- CANPACK SA

- Silgan Holdings Inc.

- Greif Inc.

- TUBEX Packaging GmbH

- Mauser Packaging Solutions

- Nampak Limited

- Colep Packaging

- CPMC Holdings Ltd.

- Toyo Seikan Group Holdings

- Amcor plc(Metal division)

- AptarGroup Inc.

- Alcoa Corporation

- Sherwin-Williams(Can Coatings)

- Novelis Inc.

- Hindalco Industries Ltd.

- RPC Group plc

- BWAY Corporation

- Berlin Packaging

제7장 시장 기회 및 미래 전망

CSM 26.01.21The metal packaging market is expected to grow from USD 136.22 billion in 2025 to USD 140.16 billion in 2026 and is forecast to reach USD 161.61 billion by 2031 at 2.89% CAGR over 2026-2031.

Steady growth stems from circular-economy legislation, premiumisation of ready-to-drink beverages, and retailers' plastic-to-metal substitution pledges. Aluminium's superior recycling economics, combined with material-lightweighting advances and brand-owner scope-3 reduction targets, reinforce the metal packaging market as the default option for carbonated and functional beverages. Producers continue to hedge aluminium and steel price swings through long-term contracts and scrap-based supply strategies, while coating suppliers accelerate the shift to BPA-free chemistries that underpin consumer safety narratives. Competitive intensity remains moderate as the leading canmakers deepen vertical integration across coating, recycling, and digital printing capabilities to defend share in a mature yet opportunity-rich landscape.

Global Metal Packaging Market Trends and Insights

Circular-Economy Mandates Boost Can-to-Can Recycling Loops

Tighter legislation is reshaping value-chain economics by mandating minimum recycled-content thresholds that aluminium cans already exceed, giving the metal packaging market a compliance edge. The EU's PPWR requires 30% recycled material in beverage containers by 2030, yet aluminium cans average 71% recycled content. Deposit-return schemes are driving collection rates toward 90% by 2029, supporting predictable scrap flows and reducing virgin-metal dependency. Global producers such as Ball target 85% recycled content, reinforcing closed-loop efficiencies that temper raw-material cost risk. Australia mirrors EU rules with an 80% post-consumer threshold for food-grade cans by 2040.Sustained regulatory momentum cements aluminium's moat over PET, particularly in beverages where procurement now factors circularity scores into supplier bids.

Premiumization of RTD Beverages in Emerging Asia

Surging demand for premium canned drinks is accelerating the metal packaging market growth in Asia-Pacific. Japan's canned chuhai segment tripled in the United States between 2018 and 2023 as consumers seek low-calorie, low-alcohol options. Brands like Asahi's Nama Jokki can demonstrate how packaging innovations replicate on-premise experiences in at-home settings. Rising disposable incomes in China and India push premium RTD coffee, kombucha, and functional meal-replacement beverages into mainstream retail, all of which rely on cans for flavor protection and thermal performance. The premiumisation wave enables manufacturers to pass higher material costs through to consumers, sustaining margins despite aluminium volatility.

Price Volatility of LME Aluminium and Steel

Energy-driven price swings strain margins because the metal packaging market still relies on contracts with pass-through clauses that lag spot fluctuations. North American tariffs add complexity, forcing producers to blend hedging tools with regional sourcing to protect competitiveness.European smelters face persistent energy-cost pressure, contributing to global price turbulence. While large players offset volatility through scrap-based feedstocks and multi-year agreements, smaller converters remain exposed, which can slow capital investment cycles.

Other drivers and restraints analyzed in the detailed report include:

- Retailers' Plastic-to-Metal Substitution Pledges

- High Scrap Recovery Rates Lower True Cost vs. PET

- Brand-Owner Push-Back on Scope-3 CO2 Footprint

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminium generated 42.80% of the metal packaging market share in 2025 and is projected to grow at a 3.57% CAGR through 2031, benefiting from closed-loop recycling systems that meet PPWR mandates. Steel maintains relevance in large-format food and industrial drums but grows more slowly due to weight and energy considerations. Novelis's USD 90 million UK expansion to double can-recycling capacity underscores the material's strategic importance. Aluminium's light weight reduces logistics emissions, aligning with ESG scorecards and deepening customer loyalty among beverage brands. Market participants continue to invest in remelt technology, enabling the metal packaging market size associated with secondary aluminium to expand steadily.

Secondary aluminium pricing advantages help brands manage raw-material costs relative to virgin metal, mitigating procurement risk. Hindalco's USD 10 billion capacity plan illustrates how integrated smelting and recycling hubs shorten supply chains and support aggressive recycled-content targets. Steel's magnetic recoverability remains a plus in mixed-waste streams, yet higher container weight raises transport costs as carbon taxes spread. Altogether, aluminium's cost, circularity, and weight advantages cement its leadership position, even as steel serves resilient niches that prioritize mechanical strength and puncture resistance.

Cans represented 41.12% of the metal packaging market in 2025 and are set to grow at a 6.08% CAGR, propelled by the premiumisation of RTD coffee, hard seltzer, and functional beverages across global convenience channels. Ball's Dynamark Advanced Pro variable-graphics system personalizes cans at scale, allowing marketers to boost engagement and shelf appeal. Food cans hold a stable base, supplying high-barrier protection that underwrites global trade in tomato paste, soups, and pet food. Aerosol cans tap personal-care growth as pent-up post-pandemic demand lifts hair styling, deodorant, and household-cleaning categories in emerging markets.

Light-weighting initiatives reduce aluminium per unit without compromising integrity, helping contain costs and shrink scope-3 footprints. Caps, closures, and lug lids maintain niche relevance by providing tamper evidence and convenience. Bulk drums and intermediate steel containers retain popularity for agrochemicals and edible oils, where reusability and UN transport certifications are critical. Collectively, these dynamics guarantee that cans remain the metal packaging market's flagship product while ancillary segments evolve through material science and design innovation.

The Metal Packaging Market Report is Segmented by Material Type (Aluminum, Steel), Product Type (Bulk Containers, Shipping Barrels and Drums, Caps and Closures, and More), End-User Industry (Beverage, Food, and More), Coating/Lining Type (BPA-Based Epoxy, BPA-NI Epoxy and More), Container Capacity (less Than 250 Ml, 251-500, and More), Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.21% of the metal packaging market in 2025 and is tracking a 5.89% CAGR through 2031, anchored by China's burgeoning RTD sector and India's rising middle class. Localised can-sheet supply, combined with Hindalco's multi-billion-dollar smelter-plus-recycling build-out, underpins cost leadership and circular credentials that appeal to global brand owners. Japan contributes design leadership, exporting high-quality chuhai formats that influence regional adoption patterns, while Southeast Asian nations leverage tourism-driven beverage demand and emerging deposit-return pilots.

North America represents a mature arena where domestic can lines run near full utilisation, cushioned by long-term supply contracts with major beer and soft-drink fillers. Tariff regimes compel canmakers to source metal domestically, spurring investment in scrap-based billet facilities and warehouse automation to drive down per-unit costs. Widespread state-level bottle bills keep aluminium recovery rates above 60%, bolstering feedstock security for secondary production.

Europe combines rigorous PPWR requirements with sophisticated recycling networks, making it a crucible for coating innovations and digital watermark pilots. Crown's scalable plants in Spain and Italy recently added high-speed lines to serve craft-beer exporters, evidencing sustained opportunity even within a saturated market. South America, spearheaded by Brazil, exhibits strong volume growth as beer brand owners convert to cans for premium positioning and logistics efficiency.

The Middle East and Africa trail on infrastructure, yet population expansion and rising incomes provide greenfield prospects for aerosol deodorant and canned-food penetration, ensuring region-wide growth contributions to the global metal packaging market.

- Ardagh Metal Packaging S.A.

- Ball Corporation

- Crown Holdings Inc.

- CANPACK S.A.

- Silgan Holdings Inc.

- Greif Inc.

- TUBEX Packaging GmbH

- Mauser Packaging Solutions

- Nampak Limited

- Colep Packaging

- CPMC Holdings Ltd.

- Toyo Seikan Group Holdings

- Amcor plc (Metal division)

- AptarGroup Inc.

- Alcoa Corporation

- Sherwin-Williams (Can Coatings)

- Novelis Inc.

- Hindalco Industries Ltd.

- RPC Group plc

- BWAY Corporation

- Berlin Packaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Circular-economy mandates boost can-to-can recycling loops

- 4.2.2 Premiumisation of RTD beverages in emerging Asia

- 4.2.3 Retailers' plastic-to-metal substitution pledges

- 4.2.4 High scrap recovery rates lower true cost vs. PET

- 4.2.5 In-can QR/NFC tech unlocking consumer-data monetisation

- 4.2.6 Expansion of e-commerce and DTC beverage retailing

- 4.3 Market Restraints

- 4.3.1 Price volatility of LME aluminium and steel

- 4.3.2 Brand-owner push-back on scope-3 CO? footprint

- 4.3.3 Rise of mono-material paper bottles

- 4.3.4 High production and operational costs of metal packaging

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitical Scenario on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Product Type

- 5.2.1 Cans

- 5.2.1.1 Food Cans

- 5.2.1.2 Beverage Cans

- 5.2.1.3 Aerosol Cans

- 5.2.2 Bulk Containers

- 5.2.3 Shipping Barrels and Drums

- 5.2.4 Caps and Closures

- 5.2.1 Cans

- 5.3 By End-user Industry

- 5.3.1 Beverage

- 5.3.2 Food

- 5.3.3 Cosmetics and Personal Care

- 5.3.4 Household

- 5.3.5 Other End-user Industry

- 5.4 By Coating / Lining Type

- 5.4.1 BPA-Based Epoxy

- 5.4.2 BPA-NI Epoxy

- 5.4.3 Polyester / PET

- 5.4.4 Other Coating / Lining Type

- 5.5 By Container Capacity

- 5.5.1 Less than 250 ml

- 5.5.2 251 - 500 ml

- 5.5.3 501 - 1000 ml

- 5.5.4 More than 1000 ml

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardagh Metal Packaging S.A.

- 6.4.2 Ball Corporation

- 6.4.3 Crown Holdings Inc.

- 6.4.4 CANPACK S.A.

- 6.4.5 Silgan Holdings Inc.

- 6.4.6 Greif Inc.

- 6.4.7 TUBEX Packaging GmbH

- 6.4.8 Mauser Packaging Solutions

- 6.4.9 Nampak Limited

- 6.4.10 Colep Packaging

- 6.4.11 CPMC Holdings Ltd.

- 6.4.12 Toyo Seikan Group Holdings

- 6.4.13 Amcor plc (Metal division)

- 6.4.14 AptarGroup Inc.

- 6.4.15 Alcoa Corporation

- 6.4.16 Sherwin-Williams (Can Coatings)

- 6.4.17 Novelis Inc.

- 6.4.18 Hindalco Industries Ltd.

- 6.4.19 RPC Group plc

- 6.4.20 BWAY Corporation

- 6.4.21 Berlin Packaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment