|

시장보고서

상품코드

1906069

히알루론산 제품 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hyaluronic Acid Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

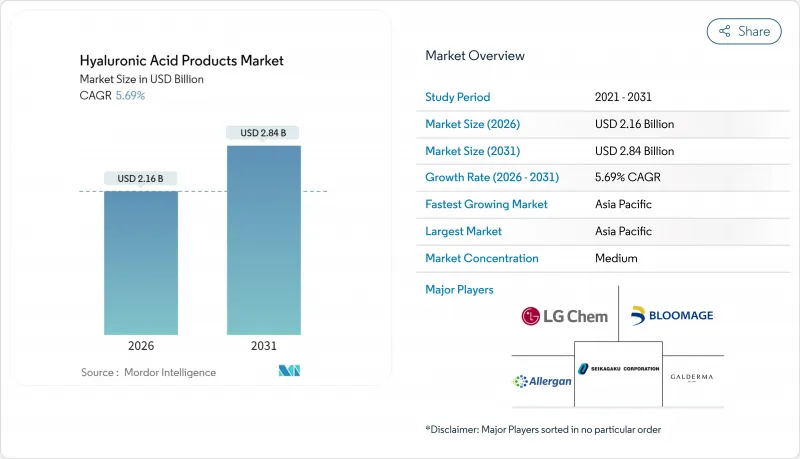

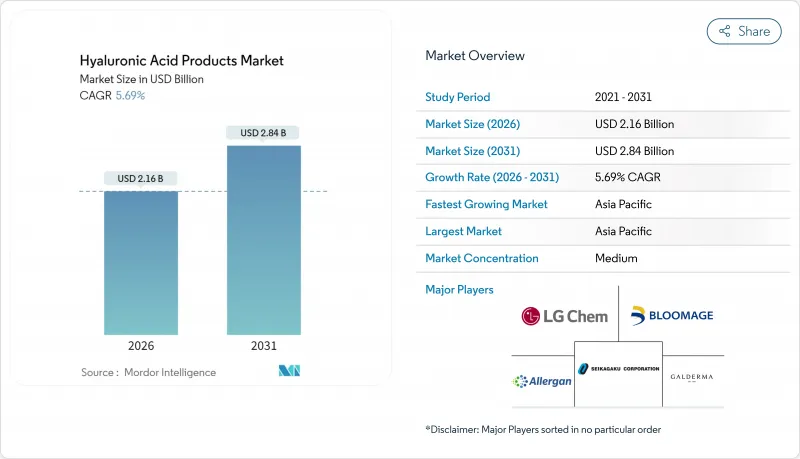

히알루론산 제품 시장의 규모는 2026년에는 21억 6,000만 달러로 추정되고 있으며, 2025년 20억 4,000만 달러에서 성장할 것으로 예상됩니다.

2031년까지 28억 4,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 5.69%로 확대될 전망입니다.

성분을 중시하는 젊은 층 소비자가 시장의 성장을 견인하고 있습니다. 이 변화는 소비자가 제품의 배합 성분을 조사하는 경향이 강해짐에 따라 투명성과 클린 라벨 제품에 대한 선호가 높아지고 있음을 반영합니다. 식품 등급 용도의 규제 승인과 최근 특허 만료에 따라 공급업체의 선택이 확산되고 경쟁이 촉진되어 이 동향을 더욱 강화하고 있습니다. 확립된 소비자 기반에 의해 페이셜케어가 여전히 주력 분야인 한편, 다기능성에 대한 기대로 인해 헤어케어 제품이나 경구 섭취 제품에 대한 수요가 현저하게 증가하고 있습니다. 또한 의료 및 미용 분야에서는 기술의 진보와 미용 치료에 대한 인지도 향상을 배경으로 저침습성 피부 필러의 도입이 증가하고 있습니다. 모든 카테고리에서의 임상적 입증은 소비자가 가격보다 효과를 중시하는 경향을 높이면서 프리미엄 제품의 성장이 히알루론산 제품 시장 전체를 웃돌고 있습니다. 유통 형태는 온라인으로 전환하고 있으며, 소비자 직접 판매 모델은 원료에 대한 이해와 편의성을 높이고, 보다 쉬운 접근과 개인화된 쇼핑 체험을 제공합니다.

세계의 히알루론산 제품 시장의 동향 및 인사이트

Z세대와 밀레니얼 세대의 피부 재생 수요

2024년 조사에 따르면 구매자의 64%가 히알루론산의 보습 효과를 신뢰하고 있으며, 이는 레티놀과 비타민 C의 기대 효과를 초과합니다. 소셜 미디어가 히알루론산의 인지도를 높여 모든 가격대에서 주요 성분이 되었습니다. 이 변화는 Instagram 및 TikTok과 같은 플랫폼에서 인플루언서와 피부과 의사가 히알루론산의 이점을 홍보함으로써 소비자의 지식과 이해가 깊어진 것이 요인입니다. 브랜드 각사는 투명성에 대한 요구에 응하기 위해, 제품 라벨에 분자량을 명기하는 움직임을 확대하고 있습니다. 이는 소비자가 정보를 바탕으로 선택을 하면서 상세한 제품 정보를 요구하는 경향이 강해지고 있기 때문입니다. 제3자 기관에 의한 시험에 투자하는 기업은 임상적으로 입증된 처방에 대한 소비자의 지불 의향이 높아지면서 수익률이 향상되고 있습니다. 미국과 EU의 규제 프레임워크는 컴플라이언스 기반을 제공하고 있지만, 집행 방법의 차이가 제품 출시 시기에 영향을 주고 있으며, 기업은 이러한 지역별 차이를 효과적으로 극복하기 위해 전략을 조정하는 경우가 많아지고 있습니다.

저침습성 피부 필러의 급속한 보급

2024년 미국의 피부 필러 시장에서는 히알루론산이 압도적인 점유율을 차지하였고 안전성과 적응성으로 인해 의사가 가역적이고 생체 적합성이 높은 소재를 선호하는 경향이 부각되었습니다. '프리쥬비네이션(노화 방지)'의 동향이 현저하고, 25-34세의 환자층이 젊은 외모 유지와 노화 징후의 지연을 목적으로, 예방적인 탄력 개선을 추구하는 케이스가 증가하고 있습니다. 가교 처리된 제제는 최대 18개월간의 효과가 지속되기 때문에 의료기관은 내원 빈도 감소, 환자 만족도 향상, 예약 스케줄 최적화에 의한 경제성 향상 등의 이점을 얻을 수 있습니다. 확립된 제조업체는 엄격한 510(k) 승인 프로세스(높은 기준을 설정하여 제품의 유효성과 안전성을 보장)을 통해 시장에서의 입지를 확고히 하고 있습니다. 한편, 라틴아메리카와 걸프 국가에서도 이러한 동향이 받아들여지고 있으며 미용 의식의 높아짐과 가처분 소득 증가를 배경으로, 종래의 구미권을 넘어 시장이 확대하고 있습니다.

주사제의 부작용에 대한 규제 우려

2015년부터 2024년까지 FDA는 히알루론산 필러와 관련된 5,500건 이상의 부작용을 보고했으며, 혈관 폐색에서 시력 상실에 이르기까지 다양한 사례가 보고되었습니다. 이러한 부작용은 심각한 안전 문제를 야기하여 FDA가 보다 엄격한 규제 조치를 시행하도록 촉구했습니다. 이에 따라 FDA는 승인 전에 상세한 위험 경감 계획과 시판 후 조사의 실시를 의무화하여 환자의 안전성과 제품의 책임 추궁 체제의 강화를 도모하고 있습니다. 유럽의 의료기기 규제(MDR)에서 필러는 클래스 III로 분류되어 보다 높은 안전성과 유효성 기준을 충족하기 위해 엄격한 임상시험과 감사 의무가 부과됩니다. 2020년 이후 컴플라이언스 비용은 40%에서 60%로 급증하여 시장 투입까지의 시간을 연장시켜, 이러한 재무적 및 규제적 압력에 대처하는 체제가 갖추어져 있는 기존 기업에 우위성을 제공하고 있습니다. 의료과실 보험료의 상승에 따라 일부 클리닉에서는 책임 문제를 해결하기 위해 필러 제품의 제공 범위를 축소하거나 가격을 인상하는 움직임이 나타나고 있어 시장 역학과 소비자의 접근성에 더욱 영향을 미치고 있습니다.

부문 분석

2025년 히알루론산 제품 시장에서 페이셜케어 제품이 81.63%의 압도적 점유율을 차지하였습니다. 업계 표준에서는 보습제에 1-2%의 히알루론산나트륨을 배합하는 한편, 토너는 가볍고 여러 단계로 스킨 케어를 요구하는 소비자 수요에 대응하고 있습니다. 지속적인 보습 효과를 실현하는 캡슐화 마이크로 스피어가 도입되어 프리미엄 가격 설정의 기반이 되고 있습니다. 임상시험은 이러한 추세를 뒷받침하고 4주만에 경표피 수분 증발량이 15% 감소한다는 것을 입증하여 소비자의 신뢰를 높이고 있습니다. 게다가 세안료나 화장수에 0.5% 미만의 히알루론산을 배합함으로써, 계면활성제에 의한 건조를 효과적으로 줄이고, 과학적으로 증명된 효과를 통해 카테고리의 가치를 높이고 있습니다.

헤어케어 분야는 히알루론산 제품 시장에서 가장 성장이 현저한 부문으로 부상하고 있으며, 2026년부터 2031년에 걸쳐 CAGR 7.18%의 확대가 전망됩니다. 2031년까지 모근의 보습에는 저분자 히알루론산, 큐티클의 부드러움에는 고분자 히알루론산의 사용이 증가하여 이 성장을 견인할 전망입니다. 시세이도 및 LG생활건강을 비롯한 주요 K-뷰티 브랜드는 건조와 미소 염증에 대한 대책으로 히알루론산과 세라마이드를 배합한 두피용 세럼 부스터를 전개하고 있습니다. 일본과 한국의 전문점에서는 특히 머리카락의 탄력성 향상에 대해 제품 효과를 적극적으로 실증하고 있습니다. 헹구지 않는 두피 에센스와 샴푸 전 마스크 같은 혁신적인 제품이 사용 기회를 확대하고 평균 구매 금액을 밀어 올리고 있습니다.

지역별 분석

아시아태평양은 수익의 41.10%를 차지하였으며 2031년까지 견조한 6.05%의 연평균 복합 성장률(CAGR)이 전망되고 있습니다. 중국에서 식품 등급 히알루론산의 인가는 섭취형 미용의 급성장을 가속하고 한국은 K-뷰티 현상의 혜택을 받아 수출이 호황을 이루고 있습니다. 28.9%의 점유율을 차지하는 일본에서는 변형성 무릎관절증에 대한 무릎연골주사가 추진되고 있습니다. 반면 인도와 호주는 유망한 성장 시장으로 부상하고 있지만 규제 변동과 관세의 영향으로 성장 속도가 완만합니다. Bloomage Biotechnology사와 같은 지역 기업은 규모의 경제와 수직 통합을 활용하여 원재료 조달 가격에서 세계 기업을 능가하는 경쟁력을 발휘합니다.

북미는 확립된 미용 의료 인프라와 견조한 소비 지출을 배경으로 뒤를 잇고 있습니다. 미국에서는 필러 시장에서 히알루론산이 58.8%의 압도적 점유율을 차지합니다. 그러나 부작용에 대한 모니터링 강화는 승인 기간의 장기화와 컴플라이언스 비용 증가를 초래합니다. 캐나다와 멕시코는 1인당 소비량에서 지연을 겪었지만 토론토 및 멕시코시티와 같은 도시 지역에서는 성장 가능성이 입증되었습니다. 유럽은 북미와 마찬가지로 성숙 시장이며 독일, 프랑스, 영국이 수요를 견인하고 있습니다. 그러나 EU의 의료기기규정(MDR)은 더 엄격한 문서화 부담을 부과하기 때문에 이는 다국적 기업에 유리합니다. 브렉시트 후 영국은 규제의 차이로 인해 물류가 복잡해지고 있지만, 양자 간 승인에 의한 특정 신청의 간소화로 일부 완화되고 있습니다.

남미에서는 미용시술에 대한 문화적 취향에 힘입어 브라질이 주도적인 역할을 하고 있습니다. 그러나 아르헨티나에서는 경제 변동이 소비량을 억제합니다. 중동에서는 사우디아라비아와 아랍에미리트(UAE)가 특히 면세 시장에서 히알루론산 세럼을 고급품으로 자리 매김하고 있습니다. 아프리카에서는 남아프리카가 소비의 중심지이지만, 저렴한 가격과 유통망의 과제에 의해 지방으로의 보급이 방해되고 있습니다. 규제 프레임워크는 서유럽 국가에 뒤처져 시장의 불확실성을 낳는 한편, 조기 참가자에 대한 기회도 창출하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- Z세대 및 밀레니얼 세대에서의 노화 예방 수요

- 저침습성 피부 필러의 급속한 보급

- 제1세대 히알루론산 특허의 만료에 의한 저비용 참가 기업의 대두

- 중국 및 동남아시아에서 식품 등급 HA의 식품 및 음료에 대한 허가

- 노화에 따른 무릎관절에 대한 무릎연골주사용 히알루론산 수요

- AI를 활용한 히알루론산 화장품 요법의 개인화

- 억제요인

- 닭벼슬 유래 히알루론산의 가격 변동성

- 주사제의 부작용에 관한 규제 우려

- 발효 등급 원료 부족으로 인한 공급망 위험

- 보습제에서 폴리글루탐산에 의한 대체품의 위협

- 소비자 행동 분석

- 규제 상황

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 유형

- 페이셜케어 제품

- 보습제 및 크림

- 페이셜 세럼

- 세안제

- 기타

- 아이케어 제품

- 립케어 제품

- 헤어케어 제품

- 샴푸 및 컨디셔너

- 기타

- 기타 제품

- 페이셜케어 제품

- 카테고리

- 대중

- 프리미엄

- 유통채널

- 슈퍼마켓 및 하이퍼마켓

- 전문점

- 온라인 소매점

- 기타 유통채널

- 지역

- 북미

- 미국

- 멕시코

- 캐나다

- 기타 북미

- 유럽

- 영국

- 독일

- 스페인

- 프랑스

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Allergan(AbbVie)

- Galderma

- LG Chem

- Sanofi(Genzyme)

- Seikagaku Corporation

- Contipro

- Bloomage Biotechnology

- Shiseido

- Evonik Industries

- Smith & Nephew

- Zimmer Biomet

- Kewpie Corporation

- Anika Therapeutics

- Lubrizol Corporation

- Ashland Global

- HTL Biotechnology

- Fidia Farmaceutici

- Maruha Nichiro

- Medytox

- Altergon Italia

제7장 시장 기회 및 미래 전망

CSM 26.01.28Hyaluronic Acid Products market size in 2026 is estimated at USD 2.16 billion, growing from 2025 value of USD 2.04 billion with 2031 projections showing USD 2.84 billion, growing at 5.69% CAGR over 2026-2031.

Young consumers, with their ingredient-first mindset, are driving momentum in the market. This shift reflects a growing preference for transparency and clean-label products, as consumers increasingly scrutinize product formulations. Regulatory approvals for food-grade applications and recent patent expiries, which broaden supplier options and foster competition, further fuel this trend. While facial care remains the dominant player due to its established consumer base, there's a noticeable surge in demand for hair-care products and ingestibles, driven by their perceived multifunctional benefits. Additionally, the adoption of minimally invasive dermal fillers in the medical realm is on the rise, supported by advancements in technology and growing awareness of aesthetic treatments. Across all categories, premium positioning is outpacing the overall Hyaluronic Acid Products market, as clinical validation leads consumers to prioritize efficacy over price. The distribution landscape is shifting online, with direct-to-consumer models enhancing both ingredient awareness and convenience for shoppers, offering them greater accessibility and personalized shopping experiences.

Global Hyaluronic Acid Products Market Trends and Insights

Skin-rejuvenation demand in Gen Z and millennials

In 2024, surveys reveal that 64% of shoppers trust the hydration claims of hyaluronic acid, surpassing the unprompted recall of retinol and vitamin C. Social media has elevated hyaluronic acid, making it a staple ingredient across all price tiers. This shift is driven by increased consumer awareness and education, as platforms like Instagram and TikTok amplify the benefits of hyaluronic acid through influencers and dermatologists. Brands are now highlighting molecular weight on front labels to align with transparency demands, as consumers seek detailed product information to make informed decisions. Firms investing in third-party testing are seeing lifted gross margins, thanks to a higher willingness among consumers to pay for clinically proven formulas. While regulatory frameworks in the U.S. and E.U. offer a compliance foundation, their differing enforcement practices influence product launch timings, with companies often tailoring strategies to navigate these regional variations effectively.

Rapid uptake of minimally invasive dermal fillers

In 2024, U.S. dermal-filler revenue saw hyaluronic acid commanding a dominant share, underscoring practitioners' preference for reversible and biocompatible materials due to their safety profile and adaptability. The "prejuvenation" trend is evident as patients aged 25-34 increasingly pursue preventive volumization to maintain youthful appearances and delay visible signs of aging. With cross-linked formulations now offering corrections lasting up to 18 months, clinics benefit from reduced visit frequency, improved patient satisfaction, and enhanced economics through optimized appointment scheduling. Established manufacturers find their foothold solidified by rigorous 510(k) pathways, which set a high bar for evidence, ensuring product efficacy and safety. Meanwhile, as Latin America and the Gulf states embrace these trends, the addressable market expands beyond its traditional Western confines, driven by rising aesthetic awareness and increasing disposable incomes in these regions.

Regulatory overhang on injectable adverse events

From 2015 to 2024, the FDA received over 5,500 reports of adverse events linked to hyaluronic acid fillers, with incidents ranging from vascular occlusion to vision loss. These adverse events have raised significant safety concerns, prompting the FDA to implement stricter regulatory measures. In response, the FDA now mandates detailed risk-mitigation plans and commitments to post-market surveillance prior to granting clearance, aiming to ensure better patient safety and product accountability. Under Europe's Medical Device Regulation, fillers are categorized as Class III, imposing stringent clinical trial and audit obligations to meet higher safety and efficacy standards. Since 2020, compliance costs have surged by 40% to 60%, elongating the time-to-market and giving an edge to established players who are better equipped to handle these financial and regulatory pressures. In light of rising malpractice premiums, some clinics are either narrowing their filler offerings or increasing prices to manage liability concerns, further impacting market dynamics and accessibility for consumers.

Other drivers and restraints analyzed in the detailed report include:

- Expiry of first-wave ha patents enabling low-cost entrants

- Food-grade HA approval in China and South-East Asia

- Substitution threat from polyglutamic acid in moisturizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, facial-care formulations command a dominant 81.63% share of the Hyaluronic Acid Products market. Industry standards see moisturizers boasting 1-2% sodium hyaluronate, while serums cater to the rising consumer demand for lightweight, multi-step skincare. Encapsulated microspheres are being adopted for their ability to deliver sustained hydration, justifying premium pricing. Clinical studies validate this trend, showcasing a notable 15% reduction in transepidermal water loss within just four weeks, bolstering consumer trust. Additionally, reformulating cleansers and toners with sub-0.5% hyaluronic acid effectively mitigates surfactant-induced dryness, enhancing the category's value through scientifically proven benefits.

Hair care is emerging as the fastest-growing segment in the Hyaluronic Acid Products market, with projections of a 7.18% CAGR from 2026 to 2031. By 2031, fueled by the increasing use of low-molecular-weight hyaluronic acid for follicle hydration and high-molecular-weight variants for smoothing cuticles. Leading K-beauty brands, including Shiseido and LG Household & Health Care, are rolling out scalp-serum boosters that blend hyaluronic acid with ceramides, targeting dryness and micro-inflammation. Specialty stores in Japan and South Korea are actively demonstrating product efficacy, particularly in enhancing strand elasticity. Innovations like leave-on scalp essences and pre-shampoo masks are broadening usage occasions and boosting average basket sizes.

The Hyaluronic Acid Products Market Report is Segmented by Type (Facial Care Products, Eye Care Products, and More), Category (Mass, Premium), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail Stores, Other Distribution Channel), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific, commanding 41.10% of the revenue, leads with a robust 6.05% CAGR projected through 2031. China's nod to food-grade hyaluronic acid ignites a surge in ingestible beauty, while South Korea's exports bask in the glow of the K-beauty phenomenon. Japan, holding a 28.9% stake, bolsters viscosupplementation for knee osteoarthritis. Meanwhile, India and Australia emerge as promising growth arenas, albeit with tempered acceleration due to fragmented regulations and tariffs. Regional players like Bloomage Biotechnology harness scale and vertical integration, allowing them to outpace global counterparts on raw material pricing.

North America, riding on a well-established aesthetic infrastructure and robust consumer spending, follows closely. In the U.S., hyaluronic acid claims a dominant 58.8% share in fillers. However, heightened scrutiny over adverse events extends approval timelines and inflates compliance costs. While Canada and Mexico lag in per-capita consumption, urban hubs like Toronto and Mexico City signal potential growth. Europe, echoing North America's maturity, sees Germany, France, and the U.K. at the forefront of demand. Yet, the EU MDR regulations impose a heavier documentation burden, favoring multinationals. Post-Brexit, the U.K. grapples with regulatory divergence complicating logistics, though some relief comes from bilateral recognition easing specific filings.

In South America, Brazil leads the charge, driven by a cultural penchant for beauty treatments. However, Argentina's economic fluctuations temper its volume. In the Middle East, Saudi Arabia and the UAE position hyaluronic acid serums as luxury items, especially in duty-free markets. Africa's consumption is anchored in South Africa, yet challenges in affordability and distribution hinder rural access. While regulatory frameworks lag behind their Western counterparts, introducing market uncertainties, they simultaneously carve out opportunities for early entrants.

- Allergan (AbbVie)

- Galderma

- LG Chem

- Sanofi (Genzyme)

- Seikagaku Corporation

- Contipro

- Bloomage Biotechnology

- Shiseido

- Evonik Industries

- Smith & Nephew

- Zimmer Biomet

- Kewpie Corporation

- Anika Therapeutics

- Lubrizol Corporation

- Ashland Global

- HTL Biotechnology

- Fidia Farmaceutici

- Maruha Nichiro

- Medytox

- Altergon Italia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Skin-rejuvenation demand in Gen-Z and Millennials

- 4.2.2 Rapid uptake of minimally-invasive dermal fillers

- 4.2.3 Expiry of first-wave HA patents enabling low-cost entrants

- 4.2.4 Food-grade HA approval in China and South-East Asia food and beverages

- 4.2.5 Medical-grade HA demand for viscosupplementation in aging knees

- 4.2.6 AI-enabled personalization of HA cosmetic regimens

- 4.3 Market Restraints

- 4.3.1 Pricing volatility of rooster comb-derived HA

- 4.3.2 Regulatory overhang on injectable adverse events

- 4.3.3 Supply-chain risk from fermentation-grade raw material shortages

- 4.3.4 Substitution threat from polyglutamic acid in moisturizers

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Type

- 5.1.1 Facial Care Products

- 5.1.1.1 Moisturizers and Creams

- 5.1.1.2 Facial Serum

- 5.1.1.3 Cleansers

- 5.1.1.4 Others

- 5.1.2 Eye Care Products

- 5.1.3 Lip Care Products

- 5.1.4 Hair Care Products

- 5.1.4.1 Shampoo and Conditioner

- 5.1.4.2 Others

- 5.1.5 Other Products

- 5.1.1 Facial Care Products

- 5.2 Category

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Specialty Stores

- 5.3.3 Online Retail Stores

- 5.3.4 Other Distribution Channel

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Mexico

- 5.4.1.3 Canada

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Spain

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Netherlands

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Allergan (AbbVie)

- 6.4.2 Galderma

- 6.4.3 LG Chem

- 6.4.4 Sanofi (Genzyme)

- 6.4.5 Seikagaku Corporation

- 6.4.6 Contipro

- 6.4.7 Bloomage Biotechnology

- 6.4.8 Shiseido

- 6.4.9 Evonik Industries

- 6.4.10 Smith & Nephew

- 6.4.11 Zimmer Biomet

- 6.4.12 Kewpie Corporation

- 6.4.13 Anika Therapeutics

- 6.4.14 Lubrizol Corporation

- 6.4.15 Ashland Global

- 6.4.16 HTL Biotechnology

- 6.4.17 Fidia Farmaceutici

- 6.4.18 Maruha Nichiro

- 6.4.19 Medytox

- 6.4.20 Altergon Italia