|

시장보고서

상품코드

1906072

가정용 살충제 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Household Insecticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

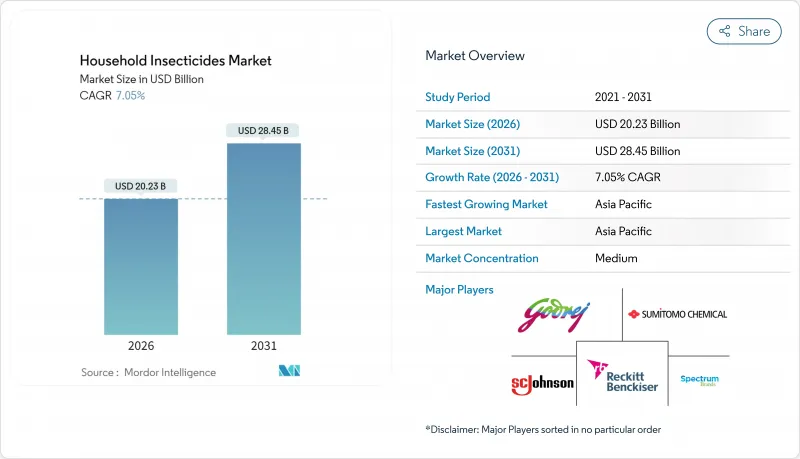

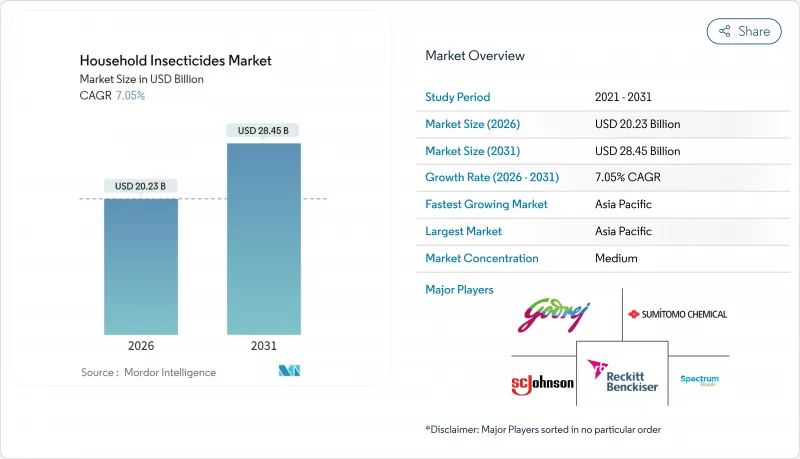

가정용 살충제 시장 규모는 2025년 189억 달러였고, 2026년 202억 3,000만 달러에 이르고, 2031년에는 284억 5,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지는 CAGR 7.05%로 성장할 전망입니다.

중재 질환의 발생 증가, 급속한 도시화, 저독성 활성 성분에 대한 규제적 우대 조치가 가정용 살충제 시장에서 이 확대를 견인하고 있습니다. 2024년 1,240만 건으로 증가한 뎅기열 사례의 급증은 모기와 파리 제거 솔루션에 대한 프리미엄 수요를 촉진하는 공중 보건 긴급성을 돋보이게 합니다. 규제 당국은 합성 피레스로이드계 살충제에 대한 감시를 강화하는 한편, 바이오 유래 성분의 승인을 가속화하고 있어, 제조업체는 천연 유래 제품의 개발을 가속시키고 있습니다. 아시아태평양은 중재생물의 번식을 조장하는 밀집도시이기 때문에 가정용 살충제 시장에서 40.0%의 최대 점유율을 차지하고 있습니다. 이 지역의 기업은 지역의 저항 패턴에 대항하기 위해 독자 개발의 분자를 투입하고 있습니다. 한편, 전자상거래 플랫폼은 세계의 전개를 확대해, 데이터 풍부한 소비자 직접 판매 모델을 가능하게 하고 있어 강력한 디지털 인게이지먼트를 가지는 브랜드에 이익을 가져오고 있습니다. 원재료공급 체인 변동은 비용 압력이 되는 것, 프리미엄인 아웃도어 생활 분야나 스마트 IoT 대응 디바이스가 새로운 수익 경로를 열고 있습니다.

세계 가정용 살충제 시장 동향과 인사이트

곤충 매개 질환 증가 경향

뎅기열, 말라리아, 치쿤구니아열의 유행이 역사적 수준을 크게 웃돌고, 질병 예방이 가정용 살충제 시장의 주요 구매 동기가 되고 있습니다. 2023년부터 2024년까지 세계 뎅기열 발생률은 230% 급증하고 소비자는 고가격대의 지속적인 보호 제품으로 향하고 있습니다. 기후 변화에 의해 모기 번식기가 장기화되고 넷타이시마카가 온대지역으로 확대되고 있기 때문에 유럽과 북미에서 새로운 판매 기회가 탄생하고 있습니다. 특히 뎅기열의 만연이 경제생산성을 위협하는 남미에서는 정부가 취약한 커뮤니티를 위해 스프레이와 모기향을 구입하는 것을 돕고 있습니다. 살충제가 일용품에서 필수 건강 보호 수단으로 전환하는 동안 의학적 권장 사항과 과학적 메시지를 활용하는 브랜드는 가정에 대한 침투도를 높이고 있습니다. 브라질의 기록적인 뎅기열 발생 연도는 지속성 제제의 개발을 촉진하고 역학적 압력과 연구 개발의 중점화와의 연관성을 강화했습니다.

현대 소매 및 전자상거래 채널 확대

DIY 해충 제거 분야에서 디지털 플랫폼은 전통적인 홈 센터를 능가합니다. 2024년 독일의 아마존 해충 방제 제품 판매액은 13억 달러에 달했고, 전문 소매점 판매량을 크게 웃돌았습니다. 온라인 판매는 제품 투명성을 높이고 신규 진출기업이 풍부한 상품 정보와 리뷰 기능으로 기존 기업과 경쟁할 수 있도록 하고 있습니다. 정기 구입 모델은 보충 수요를 고정화하고, 고객 평생 가치를 높이는 것과 동시에, 가정용 살충제 시장 수요 변동을 평준화합니다. 클릭 스트림 및 구매 내역에서 수집한 데이터는 타겟팅된 프로모션 지침이 되며 제품 처방을 개선하는 데에도 활용됩니다. 이 채널 시프트는 브랜드가 기존 도매업체를 거치지 않고 직접 판매할 수 있기 때문에 국경을 넘어서는 사업 확대를 가속화하고 있습니다. 그러나 복잡한 표시 규정으로 인해 현지에 맞는 패키징이 여전히 필요합니다. 밀레니얼 세대와 Z세대 소비자가 온라인 구매층을 주도하고 있으며, 곤충제제 구매 빈도는 모바일을 통해 연장자보다 60% 높은 경향이 있습니다.

엄격한 국제 및 국내 화학물질 규제

주요 공급업체의 REACH 등록 비용 및 시험 비용은 연간 5,000만 유로(5,400만 달러)를 초과합니다. 피레스로이드류의 재평가에 의해 제품 발매가 최대 2년 지연되는 경우도 발생하고 있습니다. 중소기업은 이러한 장벽을 극복하는 자금력이 부족하여 업계 재편이나 혁신의 다양성 저하를 초래할 우려가 있습니다. 각국마다 다른 규제로 인해 브랜드는 여러 처방을 유지해야 하며 운영비용은 통일된 규제체제보다 15-20% 높아지고 있습니다. 예방 원칙은 불확실성을 조장하고 장기적인 R&D 투자의 위험을 높입니다.

부문 분석

2025년 모기와 파리 대책 제품은 가정용 살충제 시장 점유율의 33.62%를 차지했습니다. 뎅기열이나 말라리아에 대한 우려가 높아져 지속성 스프레이나 모기 향의 보급이 뒷받침한 결과입니다. 기후 변화로 유행지역이 확대되는 가운데 이러한 매개생물대책에 의한 가정용 살충제 시장 규모는 주도적 지위를 유지할 전망입니다. 고드레이의 레노플루트린 출시는 피레스로이드 내성 모기를 직접 대처하는 것으로, 매개 생물의 위협이 연구 개발의 초점을 어떻게 이끌어내는지를 보여줍니다. 빈대 및 딱정벌레 대책은 9.41%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 여행 수요의 회복이 도시에서의 만연을 가속시키고 있기 때문입니다. 인구밀집도시의 대가님은 입주자의 교환을 막기 위해 잔류성 에어로졸을 구입하고 있습니다. 흰개미 대책은 열대 지역에서 지역적으로 중요성을 유지하고 있으며, 재산 손해 방지와 관련된 프리미엄 가격이 지속되고 있습니다. 쥐 구제는 정체기에 접어들었으나, 식품 폐기물 수거가 원활하지 않은 고층 복합 시설에서는 수요가 증가하고 있으며, 하이브리드 미끼와 포획 장치의 병용 시스템이 도입되고 있습니다.

소비자의 지출 패턴은 재산보호보다 건강보호를 우선하는 계층성이 분명합니다. 유효 성분 비용이 동등하더라도, 매개 생물 방제 제품은 10-15%의 가격 프리미엄이 허용됩니다. 마케팅은 질병 통계를 강조하고 긴급성을 호소하는 경향이 커지고 있습니다. 여행 수요의 회복에 수반해, 가방에 휴대 가능한 빈대 퇴치 스프레이나 세탁 첨가제가 대형 할인마트에 도입되고 있습니다. 아파트 고층동의 공동구는 바퀴벌레나 개미의 이동 경로로서 기능해, 잔류성 약제나 스마트 감시 트랩 수요를 증가시키고 있습니다. 이를 통해 건물 전체에 만연하기 전에 관리 직원에게 경보를 발신할 수 있습니다.

지역별 분석

아시아태평양은 2025년 시점에서 가정용 살충제 시장 규모의 39.58%를 차지하고, 메가시티 확대, 높은 질병 부담, 연간을 통한 온난한 기후를 배경으로 CAGR7.12%로 확대될 것으로 전망됩니다. 인도는 판매 수량으로 선두를 두고, 고드레지(Godrej)사가 국산 유효성분의 개발을 주도해, 일반 소매점망을 활용한 광범위한 유통망을 구축하고 있습니다. 중국에서는 확대하는 중산계급이 프리미엄 천연 코일과 스마트 디바이스에 대한 지출을 증가시키고 있습니다. 한편, 일본의 아스 제약(Earth Corporation)은 특허 취득 바퀴벌레 먹이제에 의해 우위성을 유지해 2024년에는 1,390억엔(9억 3,000만 달러)의 매출을 기록했습니다(EARTH.JP). 동남아시아에서는 에어로졸 구매를 돕는 정부의 뎅기열 대책 캠페인이 가장 급속한 성장을 보입니다.

미국에서는 화학물질에 대한 감시 강화로 천연계 제품이 합성계 시장 점유율을 침식하는 반면 DEET는 캠프나 하이킹 용도로 확고한 지위를 유지하고 있습니다. 캐나다의 엄격한 표시 규제는 신제품 투입을 지연시키는 것, 인가 브랜드에의 소비자 신뢰를 강화합니다. 멕시코는 뎅기열의 북상과 소매 인프라 근대화에 의해 고성장 지역으로서 대두되면서, 지역별 EC 보급률 40% 이상으로 도시 가구에서는 소비자를 위한 직접 판매 구독이 표준화되고 있습니다.

유럽 시장에서는 REACH 규제 대응 부담과 온대 지역의 해충 발생 시즌 단축이 확대를 억제하고 있습니다. 스페인에서 그리스에 이르는 남유럽에서는 여름이 장기화하기 때문에 1인당 사용량이 높아지고 있습니다. 독일에서는 DIY 체인과 온라인 플랫폼을 통한 판매 수량이 주도적이지만, 영국 시장에서는 천식 위험에 관한 보도가 잇따르면서 반려동물에 안전한 무연 스프레이로의 이행이 급속히 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 세계의 가정용 살충제 시장의 목차

제2장 소개

- 조사의 전제조건과 시장의 정의

- 조사 범위

제3장 조사 방법

제4장 주요 요약

제5장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 곤충 매개 질환 증가 경향

- 현대 소매 및 전자상거래 채널 확대

- 급속한 도시화와 인구밀도 증가

- 저독성 바이오 베이스 활성 성분으로의 규제 전환

- 스마트/IoT 연동 해충 방제 기기의 등장

- 아웃도어 리빙 트렌드에 따른 테라스 및 정원 솔루션 수요를 촉진

- 시장 성장 억제요인

- 엄격한 국제적 및 국내적인 화학물질 규제

- 건강 및 환경 독성에 대한 우려

- 관세에 따른 원재료 공급망의 변동성

- 해충의 저항성이 높아져, 제품의 효과가 저하

- 기술의 전망

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제6장 시장 규모와 성장 예측

- 곤충 유형별

- 모기 및 파리

- 쥐 및 기타 설치류

- 흰개미

- 빈대 및 딱정벌레

- 기타 곤충 유형

- 화학 유형별

- 합성

- DEET

- 피카리딘

- 기타 합성 화학

- 천연

- 시트로넬라 오일

- 제라니올 오일

- 기타 천연 오일

- 합성

- 형태별

- 분제 및 과립

- 리퀴드

- 에어로졸 스프레이

- 모기향 및 훈증기

- 크림 및 로션

- 기타 형태

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제7장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SC Johnson & Son, Inc.

- Reckitt Benckiser Group plc

- Godrej Consumer Products Ltd.

- Spectrum Brands Holdings, Inc.

- Sumitomo Chemical Co., Ltd.

- Henkel AG & Co. KGaA(Combat)

- Bayer AG

- BASF SE

- FMC Corporation

- Central Garden & Pet Company

- Rentokil Initial plc

- Rollins, Inc.

- Ecolab Inc.

- UPL Limited

- Dabur India Limited

제8장 시장 기회와 장래의 전망

SHW 26.01.22The household insecticides market size in 2026 is estimated at USD 20.23 billion, growing from 2025 value of USD 18.9 billion with 2031 projections showing USD 28.45 billion, growing at 7.05% CAGR over 2026-2031.

Intensifying vector-borne disease outbreaks, rapid urbanization, and regulatory incentives for low-toxicity actives drive this expansion within the household insecticides market. Escalating dengue fever cases, which rose to 12.4 million in 2024, underscore the public health urgency that fuels premium demand for mosquito and fly control solutions. Regulatory agencies are expediting approvals for bio-based ingredients while tightening scrutiny on synthetic pyrethroids, prompting manufacturers to accelerate natural portfolio development. Asia-Pacific holds the largest household insecticides market share at 40.0% due to dense cities that favor vector breeding, and the region's players are debuting indigenous molecules to counter local resistance patterns. Meanwhile, e-commerce platforms widen global reach and enable data-rich, direct-to-consumer models that reward brands with strong digital engagement. Supply chain volatility in raw materials adds cost pressure, but premium outdoor living segments and smart IoT-enabled devices open new revenue pathways.

Global Household Insecticides Market Trends and Insights

Rising Prevalence of Insect-Borne Diseases

Dengue, malaria, and chikungunya outbreaks are surging far beyond historical baselines, making disease prevention the primary purchase trigger in the household insecticides market. Global dengue incidence jumped 230% from 2023 to 2024, propelling consumers toward continuous protection products that command premium price points. Climate change lengthens mosquito breeding seasons and expands Aedes aegypti into temperate zones, which opens new sales pockets in Europe and North America. Governments subsidize spray and coil purchases for vulnerable communities, especially in South America, where the dengue burden threatens economic productivity. Brands leveraging medical endorsements and scientific messaging enjoy stronger household penetration, as insecticides shift from convenience goods to essential health safeguards. Brazil's record dengue year drove innovation in long-lasting formulations, reinforcing the link between epidemiological pressure and research and development focus.

Expansion of Modern Retail and E-commerce Channels

Digital platforms now outpace traditional hardware stores for do-it-yourself pest control. Amazon alone moved USD 1.3 billion of pest control products in Germany during 2024, dwarfing specialty retail volumes. Online availability elevates product transparency, letting challengers compete with incumbents through content-rich listings and review engines. Subscription models lock in replenishment, increasing customer lifetime value and smoothing demand seasonality in the household insecticides market. Data captured from clickstream and purchase histories guides targeted promotions and informs formulation tweaks. The channel shift accelerates cross-border expansion because brands bypass legacy wholesalers, although complex labeling laws still require localized packaging. Millennial and Gen Z shoppers lead the online cohort, purchasing insect repellents 60% more often via mobile than older consumers.

Stringent Global and National Chemical Regulations

REACH registration fees and testing costs now exceed EUR 50 million (USD 54 million) annually for leading suppliers. Pyrethroid re-evaluations delay launches by up to two years. Smaller firms lack the capital to clear such hurdles, leading to potential consolidation and reduced innovation diversity. Divergent national rules force brands to maintain multiple formulations, pushing operational costs 15-20% higher than under harmonized regimes. The precautionary principle fuels uncertainty, making long-horizon research and development investments riskier.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization and Population Density Growth

- Regulatory Shift Toward Low-Toxicity Bio-based Actives

- Health and Environmental Toxicity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mosquitoes and flies controlled 33.62% of the household insecticides market share in 2025, propelled by dengue and malaria fears and boosted by continuous spray and coil adoption. The household insecticides market size attributable to these vectors will maintain leadership as climate change widens endemic zones. Godrej's renofluthrin launch directly tackles pyrethroid-resistant mosquitoes and underscores how vector pressure guides research and development focus. Bedbugs and beetles climb fastest at 9.41% CAGR because resurgent travel accelerates urban infestations; landlords in dense cities purchase residual aerosols to avert tenant turnover. Termite treatments remain regionally important in the tropics, sustaining premium pricing tied to property damage prevention. Rodent control plateaus but gains incremental volume in high-rise complexes where food waste collection lags, prompting hybrid bait and snap systems.

Consumer spending patterns reveal a hierarchy that favors health protection over property preservation. Vector control products tolerate 10-15% price premiums even when active ingredient costs are similar. Marketing increasingly highlights disease statistics to reinforce urgency. As travel rebounds, luggage-compatible bedbug sprays and laundry additives enter big box chains. Utility corridors in apartment towers serve as superhighways for cockroaches and ants, elevating demand for residual formulations and smart monitoring traps that alert maintenance staff before infestations spread building-wide.

The Household Insecticides Market Report is Segmented by Insect Type (Termites, Bedbugs and Beetles, and More), Chemical Type (Synthetic and Natural), Form (Dust and Granules, Liquids, Aerosol Sprays, Creams and Lotions, and More), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded a 39.58% share of the household insecticides market size in 2025 and is projected to rise at a 7.12% CAGR driven by megacity sprawl, high disease burden, and year-round warmth. India leads volume as Godrej pioneers indigenous actives and leverages vast distribution across general trade outlets. China's expanding middle class channels spending into premium natural coils and smart devices, while Japan's Earth Corporation sustains dominance through patented cockroach baits and recorded sales of JPY 139 billion (USD 930 million) in 2024 EARTH.JP. Southeast Asia shows the fastest incremental growth owing to government dengue campaigns that subsidize aerosol purchases.

The United States sees naturals encroaching on synthetic market share amid heightened chemical scrutiny, yet DEET remains entrenched for camping and hiking. Canada's stricter labeling laws slow new product launches but reinforce consumer trust in approved brands. Mexico emerges as a high-growth pocket as dengue spreads northward and retail infrastructure modernizes. Regional e-commerce penetration above 40% makes direct-to-consumer subscriptions the norm for urban households.

REACH compliance burdens and shorter pest seasons in temperate zones restrain Europe's market expansion. Southern Europe, from Spain to Greece, exhibits higher per-capita usage due to extended summers. Germany leads unit sales through DIY chains and online platforms, whereas the United Kingdom market pivots heavily toward pet-safe fume-free sprays following high press coverage of asthma concerns.

- SC Johnson & Son, Inc.

- Reckitt Benckiser Group plc

- Godrej Consumer Products Ltd.

- Spectrum Brands Holdings, Inc.

- Sumitomo Chemical Co., Ltd.

- Henkel AG & Co. KGaA (Combat)

- Bayer AG

- BASF SE

- FMC Corporation

- Central Garden & Pet Company

- Rentokil Initial plc

- Rollins, Inc.

- Ecolab Inc.

- UPL Limited

- Dabur India Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents for Global Household Insecticides Market

2 Introduction

- 2.1 Study Assumptions and Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rising prevalence of insect-borne diseases

- 5.2.2 Expansion of modern retail and e-commerce channels

- 5.2.3 Rapid urbanization and population density growth

- 5.2.4 Regulatory shift toward low-toxicity bio-based actives

- 5.2.5 Emergence of smart/IoT-enabled insect-control devices

- 5.2.6 Outdoor living trend boosting demand for patio/yard solutions

- 5.3 Market Restraints

- 5.3.1 Stringent global and national chemical regulations

- 5.3.2 Health and environmental toxicity concerns

- 5.3.3 Tariff-driven volatility in raw-material supply chains

- 5.3.4 Rising pest resistance reducing product efficacy

- 5.4 Technological Outlook

- 5.5 Regulatory Landscape

- 5.6 Porter's Five Forces Analysis

- 5.6.1 Bargaining Power of Suppliers

- 5.6.2 Bargaining Power of Buyers

- 5.6.3 Threat of New Entrants

- 5.6.4 Threat of Substitute Products

- 5.6.5 Intensity of Competitive Rivalry

6 Market Size and Growth Forecasts

- 6.1 By Insect Type (Value)

- 6.1.1 Mosquitoes and Flies

- 6.1.2 Rats and Other Rodents

- 6.1.3 Termites

- 6.1.4 Bedbugs and Beetles

- 6.1.5 Other Insect Types

- 6.2 By Chemical Type (Value)

- 6.2.1 Synthetic

- 6.2.1.1 DEET

- 6.2.1.2 Picaridin

- 6.2.1.3 Other Synthetic Chemicals

- 6.2.2 Natural

- 6.2.2.1 Citronella Oil

- 6.2.2.2 Geraniol Oil

- 6.2.2.3 Other Natural Oils

- 6.2.1 Synthetic

- 6.3 By Form (Value)

- 6.3.1 Dust and Granules

- 6.3.2 Liquids

- 6.3.3 Aerosol Sprays

- 6.3.4 Coils and Vaporizers

- 6.3.5 Creams and Lotions

- 6.3.6 Other Forms

- 6.4 By Geography (Value)

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.1.3 Mexico

- 6.4.1.4 Rest of North America

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.2.6 Russia

- 6.4.2.7 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Australia

- 6.4.3.5 Singapore

- 6.4.3.6 Rest of Asia-Pacific

- 6.4.4 Middle East

- 6.4.4.1 Saudi Arabia

- 6.4.4.2 United Arab Emirates

- 6.4.4.3 Rest of Middle East

- 6.4.5 Africa

- 6.4.5.1 South Africa

- 6.4.5.2 Egypt

- 6.4.5.3 Rest of Africa

- 6.4.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 7.4.1 SC Johnson & Son, Inc.

- 7.4.2 Reckitt Benckiser Group plc

- 7.4.3 Godrej Consumer Products Ltd.

- 7.4.4 Spectrum Brands Holdings, Inc.

- 7.4.5 Sumitomo Chemical Co., Ltd.

- 7.4.6 Henkel AG & Co. KGaA (Combat)

- 7.4.7 Bayer AG

- 7.4.8 BASF SE

- 7.4.9 FMC Corporation

- 7.4.10 Central Garden & Pet Company

- 7.4.11 Rentokil Initial plc

- 7.4.12 Rollins, Inc.

- 7.4.13 Ecolab Inc.

- 7.4.14 UPL Limited

- 7.4.15 Dabur India Limited