|

시장보고서

상품코드

1906135

디이소노닐프탈레이트(DINP) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Diisononyl Phthalate (DINP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

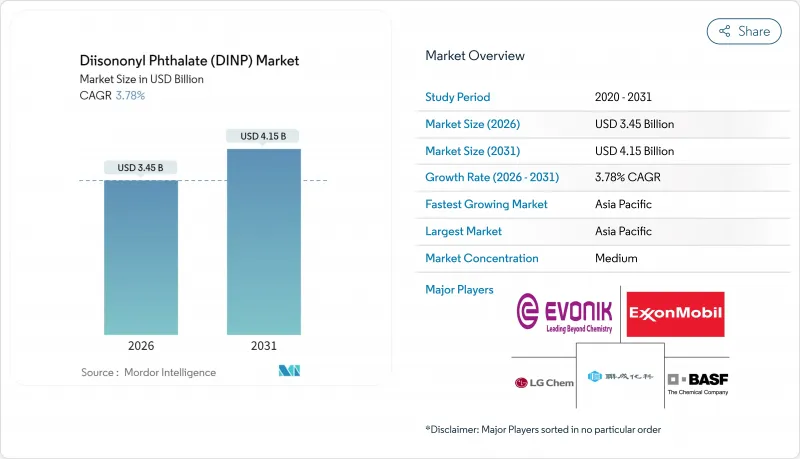

디이소노닐프탈레이트(DINP) 시장은 2025년 33억 2,000만 달러로 평가되었으며, 2026년 34억 5,000만 달러에서 2031년까지 41억 5,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 3.78%로 예상됩니다.

주요 소비 지역에서의 규제 강화의 움직임은 꾸준한 인프라 지출, 연질 PVC에 대한 근본적인 수요, 확립된 공급망의 강인성에 의해 상쇄되고 있습니다. 제조업체는 생산량을 확보하기 위해 보다 안전한 용도 전개와 추적 가능성이 있는 원료로의 전환을 진행하고 있는 한편, 건설 및 전기 분야의 비용을 중시하는 구매자는 DINP의 확실한 비용 및 효과 사이의 밸런스를 높이 평가했습니다. 아시아태평양은 수요의 주도권을 유지하고 세계 평균을 초과하는 성장률을 보여줍니다. 이는 장기적인 수지 공급을 보장하는 대규모 석유 화학 투자에 의해 지원됩니다. 북미 및 유럽에서는 2025년 1월 미국 환경보호청(EPA) 위험 평가를 통해 기업은 지속 가능한 제품의 전개를 가속화하고 컴플라이언스 중심 프로세스 개선에 대한 투자를 요구받고 있습니다.

세계의 디이소노닐프탈레이트(DINP) 시장의 동향 및 인사이트

연질 PVC 수요 증가

세계의 PVC 소비량은 2025년까지 연평균 복합 성장률(CAGR) 5.96%로 확대되었으며 중기적으로 DINP에 대한 안정적인 수요를 보장합니다. 바닥재 및 케이블 용도에서 5년에서 30년이라는 긴 서비스 수명은 예측 가능한 교환 수요를 생성합니다. 동시에 열분해 유래 원료에 의해 CO2 배출량을 50% 저감하는 순환형 PVC의 진전은 생산자에게 규모를 희생하지 않고 제품 수명 종료 시의 해결책을 제시할 것을 촉구하고 있습니다. 이러한 진전으로 디이소노닐프탈레이트 시장은 지속가능성의 신뢰성을 높이면서 생산량을 유지할 수 있게 되었습니다.

확대하는 건축 및 건설 업계

건설 수요의 회복에 따라 유연성과 내후성을 요구하는 비닐 바닥재, 벽면 마감재, 지붕 방수 시트에서 DINP 사용량이 증가하고 있습니다. 북미에서의 주택 개보수 활성화와 아시아의 도시화 진전이 수요를 지지하고 있지만, 포모사사나 신텍사에 의한 최근의 생산 능력 증강이 PVC 가격의 상승 압력을 억제하고 있습니다. 연질 LVT(라미네이트 비닐 타일)에서 경질 SPC(스톤 플라스틱 복합재)로의 이행은 가공의 복잡화를 초래해, 생산자에 의해 높은 내열성을 갖춘 DINP 등급의 개발을 촉진하고 있습니다. 디이소노닐프탈레이트 시장은 이 전문화로부터 혜택을 받고 있지만, 이익률은 저비용 수입품과의 평방 피트당 가격 경쟁력 유지 여부에 달려 있습니다.

규제 모니터링 및 건강 위험 평가

2025년 1월 미국 환경보호청(EPA)의 위험 평가에서는 특정 스프레이 도포 제품 및 소비자 바닥재에서 DINP가 위험을 초래하는 것으로 나타났으며, 특정 용도를 제한할 수 있는 강제적인 위험 관리 지시가 발동되었습니다. 캘리포니아의 65호 제안에 게시되고 미국 소비자 제품 안전 위원회(CPSC)에 의해 시행된 장난감에 대한 사용 금지는 추가적인 제약을 가하고 있습니다. 이러한 규제는 수요를 분산시키고 제조업자에게 배합 변경을 촉구하여 컴플라이언스 비용을 증가시키고 있습니다. EU의 지속적인 모니터링과 기타 관할 구역에서의 도입이 예정된 REACH 방식의 규제에 의해 디이소노닐프탈레이트 시장 진출기업은 규제 리스크를 항상 최우선 과제로 삼고 있습니다.

부문 분석

2025년에는 염화비닐 수지(PVC)가 매출액의 86.62%를 차지하였고 2031년까지 연평균 복합 성장률(CAGR) 3.96%를 보일 것으로 예측됩니다. 이 규모는 DINP의 지속적인 원료 수요를 보장하고 통합 생산자는 기존 자산을 활용하여 비용 우위를 유지합니다. 신규 순환형 PVC 수지는 생산량의 유지와 미래 컴플라이언스 대응에 공헌해 디이소노닐프탈레이트(DINP) 시장을 이 소재에 정착시키고 있습니다.

아크릴 및 폴리우레탄 틈새 시장은 나머지 수익을 차지합니다. 아크릴 페인트는 가혹한 기후 조건에서 필름의 유연성을 향상시키기 위해 DINP의 용해도를 활용합니다. 반면에 일부 폴리우레탄 폼 제조업체는 시트의 반발 수명 향상을 위해 DINP를 선택합니다. 비이소시아네이트계 폴리우레탄의 연구개발은 향후 대체 가능성을 가져오지만, 예측기간 내에서의 상업적 도입은 제한적일 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년 수익의 58.83%를 차지하였으며 2031년까지 연평균 복합 성장률(CAGR) 4.07%로 확대될 것으로 예측됩니다. BASF사의 100억 유로 규모의 통합생산시스템 투자에 힘입어 중국의 PVC 생산량에서의 세계 점유율 50%가 공급 기반을 형성하고 인도의 건설 붐이 증분 수요를 견인하고 있습니다. 중국에 의한 특정 미국 수입품에 대한 43.5%의 반덤핑 관세와 같은 무역조치는 일시적인 가격 왜곡을 낳고 있으며, 현지 DINP 생산자는 이를 활용하여 국내 시장을 보호하고 있습니다.

북미에서는 EPA의 위험 판정으로 정책 주도의 전환이 진행되고, 배합 제조업체는 안전성이 높은 도료로의 이행이나 ISCC 인증 등급의 조기 도입을 가속화하고 있습니다. 국내 화학 부문은 셰일 원료의 우위성으로 인해 침체한 2023년을 거쳐 2024년에 1.5%의 소규모 성장을 달성하였습니다. 유럽에서는 REACH 규제와 의무적 재활용 목표에 따라 순환형 경제가 추진되고, 한국산 DOTP에 대한 반덤핑 관세도 경쟁환경을 형성하고 있습니다. 이에 따라 진화하는 기준에 적합한 현지 생산 DINP 등급 수요가 간접적으로 유지될 전망입니다.

남미, 중동 및 아프리카는 산업 다각화 프로젝트와 적은 규제 마찰로 인해 소규모로 증가하는 추세에 있는 고객 기반을 제공합니다. 그러나 취약한 회수 시스템과 낮은 재활용률은 향후 개입 위험을 야기하고 2019년에 2,200만 톤의 플라스틱이 환경으로 유출되었다는 OECD의 조사 결과를 상기시킵니다. 이러한 지역을 시야에 포함하는 생산자는 저렴한 DINP 배합을 중시하면서, 궁극적으로는 OECD 기준과의 정책적 정합을 위한 준비를 진행하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 연질 PVC의 수요 증가

- 확대하는 건축 및 건설 업계

- 전기 배선 및 케이블 절연재에서의 수요 증가

- 자동차 생산 회복과 내장재 경량화

- 5G 통신 케이블 절연재로의 도입

- 억제요인

- 규제 당국의 감시와 건강 위험 평가

- 바이오 및 비프탈산계 가소제로의 이행 가속

- 솔벤트 기반 PVC 재활용 기술의 발전으로 신규 DINP 사용량 감소

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 폴리머 유형별

- PVC

- 아크릴

- 폴리우레탄

- 용도별

- 바닥재 및 벽재

- 코팅 패브릭

- 소비재

- 필름 및 시트

- 전선 및 케이블

- 기타 용도

- 최종 사용자 업계별

- 건축 및 건설

- 전기 및 전자기기

- 자동차 및 운송

- 포장 및 식품접촉재료

- 의료 및 의료기기

- 기타 최종 이용 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Azelis Group NV

- BASF SE

- Evonik Industries AG

- Exxon Mobil Corporation

- GM Chemie Pvt Ltd

- Hanwha Solutions Chemical Division Corporation

- KLJ Group

- LG Chem Ltd

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- Polynt SpA

- Shandong Qilu Plasticizers Co Ltd

- UPC Group

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Diisononyl Phthalate Market was valued at USD 3.32 billion in 2025 and estimated to grow from USD 3.45 billion in 2026 to reach USD 4.15 billion by 2031, at a CAGR of 3.78% during the forecast period (2026-2031).

Steady infrastructure spending, entrenched demand for flexible PVC, and the resilience of established supply chains offset rising regulatory scrutiny in key consuming regions. Manufacturers are pivoting toward safer application routes and traceable feedstocks to safeguard volume, while cost-focused buyers in construction and electrical sectors continue to value DINP's proven price-performance balance. Asia-Pacific maintains demand leadership and posts faster growth than the global average, helped by large-scale petrochemical investments that secure long-term resin availability. In North America and Europe, the January 2025 EPA risk evaluation forces companies to speed up sustainable product rollouts and invest in compliance-centric process upgrades.

Global Diisononyl Phthalate (DINP) Market Trends and Insights

Growing Demand for Flexible PVC

DINP remains indispensable because about 95% of global output plasticizes flexible PVC products that serve construction, automotive, and wire markets. Global PVC consumption is advancing at a 5.96% CAGR to 2025, ensuring a steady pull for DINP over the medium term. Long service lives of between 5 and 30 years in flooring and cable applications add predictable replacement demand. Parallel progress in circular PVC, where pyrolysis-sourced feedstocks cut CO2 emissions by 50%, pushes producers to demonstrate end-of-life solutions without sacrificing scale. Such developments allow the Diisononyl Phthalate market to preserve volume while improving sustainability credentials.

Expanding Building and Construction Industry

Construction rebound drives elevated use of vinyl flooring, wall cladding, and roofing membranes that require DINP for flexibility and weather resistance. Residential renovation levels in North America and ongoing urbanization in Asia sustain demand, even as recent capacity additions by Formosa and Shintech temper PVC pricing power. The shift from flexible LVT to rigid SPC formats increases processing complexity and encourages producers to refine DINP grades for higher heat stability. The Diisononyl Phthalate market benefits from this specialization, yet margins hinge on keeping cost-per-square-foot competitive with low-cost imports.

Regulatory Scrutiny and Health-Risk Assessments

The January 2025 EPA risk evaluation concluded that DINP presents unreasonable risks for certain spray-applied products and consumer floor coverings, triggering mandatory risk management that may limit specific uses. California's Proposition 65 listing and the CPSC ban in toys add further constraints. These rules fragment demand, force manufacturer reformulation, and increase compliance costs. Persistent oversight in the EU and forthcoming reach-style legislation in other jurisdictions keep regulatory risk at the forefront for participants in the Diisononyl Phthalate market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand in Electrical Wire and Cable Insulation

- Recovery in Automotive Production and Lightweight Interiors

- Accelerating Switch to Bio-/Non-Phthalate Plasticizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVC commanded 86.62% of revenue in 2025 and is forecast to grow at a 3.96% CAGR through 2031. This scale secures continuous feedstock offtake for DINP while integrated producers leverage existing assets for cost leadership. Emerging circular PVC resins help maintain volume and future-proof compliance, keeping the Diisononyl Phthalate market anchored in this substrate.

Acrylic and polyurethane niches together occupy the balance of revenue. Acrylic coatings exploit DINP's solvency to enhance film flexibility in demanding climatic conditions, whereas select polyurethane foam producers choose DINP to improve rebound life in seating. Non-isocyanate polyurethane R&D introduces future substitution risk, although commercial adoption remains limited through the forecast horizon.

The Diisononyl Phthalate (DINP) Market Report is Segmented by Polymer Type (PVC, Acrylic, and Polyurethane), Application (Floor and Wall Coverings, Coated Fabrics, and More), End-User Industry (Building and Construction, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 58.83% of 2025 revenue and is forecast to expand at a 4.07% CAGR to 2031. China's 50% global share in PVC output, supported by BASF's EUR 10 billion Verbund investment, anchors supply while India's construction boom pulls incremental tonnage. Trade actions, such as China's 43.5% anti-dumping duties on select U.S. imports, create episodic price distortions that local DINP producers exploit to defend home markets.

North America experiences policy-driven transitions following the EPA risk verdict, prompting formulators to shift toward safer coatings and to fast-track ISCC-certified grades. The domestic chemical sector ekes out a 1.5% gain in 2024 after a subdued 2023, aided by shale-advantaged feedstocks. Europe pushes circularity through REACH and mandatory recycling targets; anti-dumping duties on Korean DOTP also shape the competitive field, indirectly sustaining demand for locally made DINP grades that remain compliant with evolving standards.

South America, the Middle East, and Africa together provide a small but rising customer base driven by industrial diversification projects and limited regulatory friction. Weak collection systems and low recycling rates, however, risk future intervention, echoing the OECD finding that 22 million t of plastics leaked into the environment in 2019. Producers eyeing these regions emphasize affordable DINP formulations while preparing for eventual policy convergence with OECD norms.

- Azelis Group NV

- BASF SE

- Evonik Industries AG

- Exxon Mobil Corporation

- GM Chemie Pvt Ltd

- Hanwha Solutions Chemical Division Corporation

- KLJ Group

- LG Chem Ltd

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- Polynt SpA

- Shandong Qilu Plasticizers Co Ltd

- UPC Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Flexible PVC

- 4.2.2 Expanding Building and Construction Industry

- 4.2.3 Rising Demand in Electrical Wire and Cable Insulation

- 4.2.4 Recovery in Automotive Production and Lightweight Interiors

- 4.2.5 Adoption in 5G Telecom Cable Insulation

- 4.3 Market Restraints

- 4.3.1 Regulatory Scrutiny and Health-Risk Assessments

- 4.3.2 Accelerating Switch to Bio-/Non-Phthalate Plasticizers

- 4.3.3 Emerging Solvent-Based PVC Recycling Cuts Virgin DINP Use

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Polymer Type

- 5.1.1 PVC

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.2 By Application

- 5.2.1 Floor and Wall Coverings

- 5.2.2 Coated Fabrics

- 5.2.3 Consumer Goods

- 5.2.4 Films and Sheets

- 5.2.5 Wires and Cables

- 5.2.6 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Electrical and Electronics

- 5.3.3 Automotive and Transportation

- 5.3.4 Packaging and Food Contact Materials

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Other End-Use Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Azelis Group NV

- 6.4.2 BASF SE

- 6.4.3 Evonik Industries AG

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 GM Chemie Pvt Ltd

- 6.4.6 Hanwha Solutions Chemical Division Corporation

- 6.4.7 KLJ Group

- 6.4.8 LG Chem Ltd

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 NAN YA PLASTICS CORPORATION

- 6.4.11 Polynt SpA

- 6.4.12 Shandong Qilu Plasticizers Co Ltd

- 6.4.13 UPC Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment