|

시장보고서

상품코드

1906136

포토레지스트 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Photoresist - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

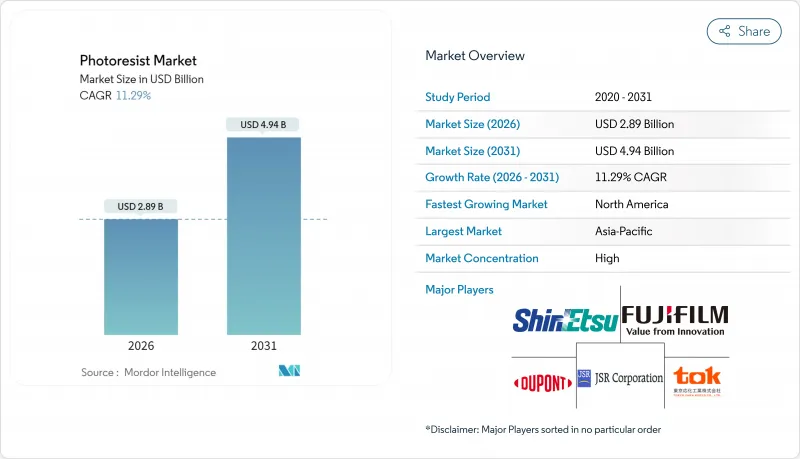

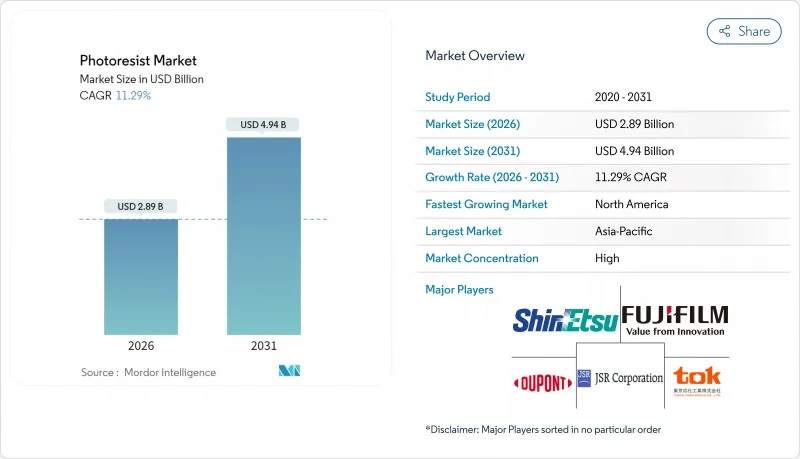

포토레지스트 시장은 2025년에 26억 달러로 평가되었고, 2026년 28억 9,000만 달러에서 2031년까지 49억 4,000만 달러에 이를 것으로 예측되고 있습니다.

예측기간(2026-2031년)의 CAGR은 11.29%로 전망되고 있습니다.

10나노미터 이하의 미세가공에서의 극자외선(EUV) 리소그래피 보급, 인공지능(AI) 가속기의 수요 급증, 정부 주도의 팹 장려책이 확대를 뒷받침하고 있습니다. 대만, 한국, 미국의 반도체 제조업체는 EUV 흡수율이 높고 선단거칠기가 낮은 금속 산화물 레지스트 및 건식 포토레지스트를 점점 도입하고 있어, 처리량이 향상되고 층당 레지스트 사용량이 줄어듭니다. 5G 및 사물인터넷(IoT) 디바이스의 병렬 기세는 성숙 노드를 위한 G선, I선, KrF 재료에 대한 수요를 유지하고 있습니다. 한편, 칩렛, 팬아웃 웨이퍼 레벨 패키징, 공동 패키징 광학 등의 선진 패키징 구조에서는 구리 필러나 실리콘 관통 전극(TSV) 구조에 대응한 후막 레지스트가 요구됩니다. 첨단 레지스트의 약 60%를 일본의 제조업체 3곳에서 차지하기 때문에 공급망 리스크는 여전히 높고, 북미나 유럽에서는 지역 분산화와 현지 생산 능력의 증강이 진행되고 있습니다.

세계의 포토레지스트 시장의 동향 및 전망

반도체 및 AI 가속기에서의 수요 증가

대규모 언어 모델 훈련 및 추론 워크로드를 구동하는 하드웨어를 제조하는 칩 제조업체는 현재 각 장치에 대해 여러 재배선층, 인터포저 및 TSV를 패터닝하고 있습니다. NVIDIA의 H100 및 향후 등장 예정인 Blackwell 시리즈는 칩렛 레이아웃을 도입하고 있어, 종래의 모놀리식 GPU에 비해 완성품 1개당 3-5배의 포토레지스트를 소비합니다. 타이완 반도체 제조(TSMC)에 의한 CoWoS(칩 온 웨이퍼 온 실리콘) 생산 능력의 확대에 따라 최대 50μm의 후막 레지스트에 대한 수요가 증가하고 있습니다. 반면, 고급 구리 필러 도금은 종횡비 3:1 이상으로 최적화된 네거티브 제제를 사용합니다. 생산량 증가는 우선적으로 대만과 한국에서 발생하지만 2027년까지 미국의 신규 공장으로도 파급될 전망입니다.

EUV 리소그래피 도입 가속화 및 높은 NA 로드맵

ASML사의 0.55NA EUV 노광 장치는 8nm 피치의 단일 노광 패터닝을 가능하게 하며, 고비용의 다중 패터닝 공정을 필요로 하지 않습니다. 1.5nm 미만이라는 보다 엄격한 선단거칠기 목표를 달성하기 위해, 팹에서는 유기계 레지스트보다 EUV를 9배 효율적으로 흡수하는 하프늄 및 지르코늄 클러스터계 금속 산화물 레지스트의 도입을 진행하고 있습니다. 이를 통해 노출 선량은 40 mJ/cm2에서 20 mJ/cm2 미만으로 줄어들어 처리량을 높이고 웨이퍼 단가를 줄일 수 있습니다. 2025년 삼성 평택 라인에서 실시되는 파일럿 가동의 결과를 바탕으로 2026년에는 2nm 공정 노드에서의 상업 도입이 전망됩니다.

용매 및 포토애시드 발생제에 대한 엄격한 HSE 규정

유럽연합(EU)은 2024년 규제(EU) 2024/573을 개정하여 2045년까지 하이드로플루오로카본 사용량을 90% 저감하는 단계적 폐지를 지정했습니다. 많은 EUV 포토레지스트는 현재 등록, 평가, 허가 대상인 퍼플루오로화 포토애시드 발생제 및 용매를 사용하고 있습니다. 규제 준수에는 불순물 수준을 1ppb 미만으로 억제하는 분석적 검증이 필요하며, 품질 관리 비용 증가를 초래함과 동시에 성능 저하의 위험을 수반하는 대체 화학 물질의 시험을 제제 제조업체에 요구하는 결과를 낳고 있습니다.

부문 분석

ArF 침지 포토레지스트는 TSMC, 삼성, 인텔에서의 7nm 및 5nm 공정에 대한 지속적인 수요로 2025년 포토레지스트 시장 규모의 31.85% 점유율을 유지했습니다. 한편, EUV용 금속 산화물 레지스트 및 건식 레지스트는 팹이 2nm 로직으로 이행함에 따라 12.94%의 연평균 복합 성장률(CAGR)로 성장하여 최대 매출을 창출할 것으로 예측되고 있습니다. 하프늄계 클러스터는 유기 폴리머의 25배 이상의 에칭 저항성을 발휘하여 하드 마스크 없이 유전체층으로의 직접 전사를 가능하게 함으로써 프로세스 플로우를 단축합니다.

램리서치사의 건식 증착형 레지스트는 스핀 공정의 폐기물을 제거하고 화학물질 소비량을 최대 90%까지 줄입니다. 2026년 대량 생산을 목표로 하는 이 플랫폼은 재료 수익을 습식 화학제품 공급업체에서 장비 통합 공급으로 전환시킬 수 있습니다. KrF, G선, I선 레지스트는 자동차 및 산업용 노드에서 여전히 필수적이며, 선진 노드가 성장을 견인하는 중에서도 안정된 기반 수익을 지지하고 있습니다.

2025년 시점에서 포지티브형 재료가 포토레지스트 시장의 71.45%를 차지했습니다. 네거티브 레지스트와 특히 에폭시 및 금속 산화물 시스템은 첨단 패키징에서 고후막층 수요가 급증함에 따라 2031년까지 연평균 복합 성장률(CAGR) 11.38%로 증가할 것으로 예측됩니다.

네거티브 레지스트는 구리 필러 도금 시의 고전류 밀도를 견디며, 종횡비 3:1을 넘는 특성을 실현합니다. 이는 미세 피치 범프 형성에 매우 중요합니다. 신규 듀얼 톤 산화 주석 플랫폼은 노광량 제어를 통한 톤 전환으로 공정 유연성을 제공합니다. imec의 초기 시험에서는 20mJ/cm2의 노광으로 16nm 미만의 해상도를 달성하고 있습니다.

지역별 분석

2025년 아시아태평양은 세계 시장에서 72.10%의 점유율을 차지했습니다. 이는 대만과 한국의 고밀도 로직 생산 능력과 중국의 성숙 노드 공장의 확장이 견인하고 있습니다. TSMC의 2nm 공정 양산과 고성능 컴퓨팅을 위한 패키지 라인은 EUV 및 후막 재료의 소비량 증가를 가져온 반면 삼성의 3D NAND 생산 능력은 고선택성 KrF 레지스트에 대한 수요를 촉진하고 있습니다. 일본의 장비 생태계, 도쿄 일렉트론사의 코팅 장비, 니콘사의 스테퍼는 국내 공급업체를 지원하고 긴밀하게 통합된 공급망을 형성합니다.

북미에서는 CHIPS법의 시행에 의해 신규 그린필드 공장의 건설이 촉진되어 2031년까지 연평균 복합 성장률(CAGR) 11.49%의 성장이 전망되고 있습니다. 인텔의 오하이오주 캠퍼스, TSMC의 애리조나 사이트, 삼성의 텍사스 시설은 2028년까지 총 30만wpm 이상의 첨단 생산 능력을 추가하여 지역의 레지스트 및 관련 화학 수요를 지원합니다. 듀폰의 콜로라도 확장과 다우의 미시간 확장은 지역으로 공급을 확장하고 태평양 횡단 물류 위험을 줄이기 위한 노력입니다.

유럽에서는 REACH 규제의 엄격한 준수가 혼합 비용을 밀어 올리는 한편, 인텔의 아일랜드에서의 대규모 투자나 독일에서의 공장 건설 계획이 원동력이 됩니다. 현지 재료 공급업체인 머크 KGaA와 BASF는 규제 대응 전문성을 살려 EUV 라인용 인증 확보에 주력하고 있습니다. 동유럽 국가들은 패키징 테스트 업무 유치에 주력하여 지역적인 발자국의 다양화를 추진하고 있습니다.

중동, 아프리카 및 남미는 개발도상지역이지만 특히 통신 기지국 및 자동차 센서용 고기능 패키징 및 MEMS 제조를 추진하고 있습니다. 지역정부는 백엔드 조립을 유치하기 위해 세제우대조치를 제공하고 있으며, 이는 G라인 및 I라인 프로세스용 포토레지스트 수요를 증가시키고 있지만, 선진 노드는 다른 지역에 집중되는 상태가 유지되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 반도체 및 AI 가속기에서의 수요 증가

- EUV 리소그래피의 도입 가속과 높은 NA 로드맵

- 5G 및 IoT 디바이스의 보급 확대에 의한 웨이퍼 생산량 증가

- 정부에 의한 팹 장려 프로그램(미국 및 EU CHIPS법)

- 건식 증착 금속 산화물 레지스트가 EUV 처리량을 높임

- 억제요인

- 용제 및 포토애시드 발생제에 대한 엄격한 HSE 규제

- 공급망 집중과 수출 관리 위험

- EU REACH 규제 및 불소계 용제를 대상으로 한 F-Gas 규제의 단계적 폐지

- 밸류체인 분석

- 규제 상황

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 레지스트 유형별

- ArF 액침

- ArF 건식

- KrF

- G-Line

- I-라인

- EUV용 금속 산화물 및 건식 레지스트

- 기타 유형

- 톤별

- 포지티브

- 네거티브

- 용도별

- 반도체 및 집적회로(IC)

- 고급 패키징(FOWLP(Fan-Out WLP), RDL)

- 플랫 패널 디스플레이(액정 및 OLED)

- 프린트 기판

- MEMS 및 센서

- 기타 용도

- 최종 사용자 산업별

- 전자 및 전기기기

- 자동차 및 전기이동성

- 항공우주 및 방위

- 소비재(포장)

- 기타 산업

- 지역별

- 아시아태평양

- 중국

- 일본

- 한국

- 대만

- 인도

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- ALLRESIST GmbH

- Asahi Kasei Corporation

- Avantor, Inc.

- Brewer Science, Inc.

- DJ MicroLaminates

- DONGJIN SEMICHEM CO. LTD

- DuPont

- Eternal Materials Co., Ltd.

- FUJIFILM Corporation

- Inpria

- JSR Corporation

- SEMI

- Kolon Industries, Inc.

- LG Chem

- Merck KGaA

- micro resist technology GmbH

- Microchemicals GmbH

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- TOKYO OHKA KOGYO CO., LTD.

- Jiangsu Nata Opto-electronic Material Co., Ltd.

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Photoresist Market was valued at USD 2.60 billion in 2025 and estimated to grow from USD 2.89 billion in 2026 to reach USD 4.94 billion by 2031, at a CAGR of 11.29% during the forecast period (2026-2031).

The widespread deployment of extreme-ultraviolet (EUV) lithography at sub-10-nanometer dimensions, the fast-growing demand for artificial-intelligence (AI) accelerators, and government-funded fab incentives underpin this expansion. Semiconductor manufacturers in Taiwan, South Korea, and the United States are increasingly favoring metal-oxide and dry photoresists that deliver higher EUV absorption and lower line-edge roughness, thereby boosting throughput and reducing per-layer resist usage. Parallel momentum in 5G and Internet-of-Things (IoT) devices sustains demand for mature-node G-line, I-line, and KrF materials. Meanwhile, advanced packaging architectures-such as chiplets, fan-out wafer-level packaging, and co-packaged optics-require thick-film resists that are compatible with copper pillar and through-silicon-via (TSV) structures. Supply-chain risks remain elevated because three Japanese suppliers collectively account for roughly 60% of advanced resists, prompting regional diversification and localized capacity additions in North America and Europe.

Global Photoresist Market Trends and Insights

Growing Demand from Semiconductor and AI Accelerators

Chipmakers producing hardware for training large language models and powering inference workloads now pattern multiple redistribution layers, interposers, and TSVs for each device. NVIDIA's H100 and forthcoming Blackwell series adopt chiplet layouts that consume three to five times more photoresist per finished part than previous monolithic GPUs. Taiwan Semiconductor Manufacturing Company's (TSMC) expansion of CoWoS capacity lifts thick-film resist of up to 50 µm, while advanced copper pillar plating uses negative-tone formulations optimized for aspect ratios above 3:1. Volume gains occur first in Taiwan and South Korea but ripple into new fabs in the United States by 2027.

Accelerated EUV Lithography Adoption and High-NA Roadmap

ASML's 0.55-NA EUV scanners enable single-exposure patterning with an 8 nm pitch, eliminating costly multiple-patterning steps. To meet the tighter line-edge roughness target of below 1.5 nm, fabs qualify metal-oxide resists based on hafnium and zirconium clusters that absorb EUV 9 times more effectively than organic formulations . The dose can be reduced from 40 mJ/cm2 to sub-20 mJ/cm2, increasing throughput and lowering the cost per wafer. Pilot runs at Samsung's Pyeongtaek lines in 2025 suggest commercial adoption at 2 nm nodes in 2026.

Stringent HSE Regulations on Solvents and Photo-Acid Generators

The European Union's 2024 revision to Regulation (EU) 2024/573 schedules a phase-down of hydrofluorocarbon usage by 90% before 2045. Many EUV photoresists now employ perfluorinated photoacid generators and solvents, which are subject to registration, evaluation, and authorization. Compliance requires analytical verification of impurity levels below 1 ppb, which drives up quality-control costs and forces formulators to test alternative chemistries that may risk lower performance.

Other drivers and restraints analyzed in the detailed report include:

- 5G/IoT Device Proliferation Expanding Wafer Starts

- Government Fab-Incentive Programs (US/EU Chips Acts)

- Supply-Chain Concentration and Export-Control Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ArF immersion formulations retained a 31.85% share of the photoresist market size in 2025, thanks to sustained demand for 7 nm and 5 nm volumes at TSMC, Samsung, and Intel. Conversely, EUV metal-oxide and dry resists are projected to post a 12.94% CAGR, generating the largest incremental value as fabs transition to 2 nm logic. Hafnium-based clusters deliver etch resistance exceeding 25 times that of organic polymers, enabling direct transfer into dielectric layers without a hard mask and thus shortening the process flow.

Lam Research's dry-deposited resist eliminates spin waste and cuts chemical consumption by up to 90%. With mass production targeted for 2026, this platform could shift material revenue from wet-chemistry suppliers toward equipment-integrated delivery. KrF, G-line, and I-line resists remain essential for automotive and industrial nodes, anchoring a steady base revenue even as advanced nodes dominate growth.

Positive-tone materials dominated the photoresist market with a 71.45% share in 2025. Negative-tone resists, particularly epoxy-based and metal-oxide systems, are forecast to rise at 11.38% CAGR through 2031 as demand for high-thickness layers in advanced packaging surges.

Negative resists withstand high current densities during copper-pillar plating and achieve aspect ratios exceeding 3:1, which is critical for fine-pitch bump formation. Emerging dual-tone tin-oxide platforms offer process flexibility by switching tone with dose control; early tests at imec show sub-16 nm resolution at 20 mJ/cm2 exposure.

The Photoresist Market Report is Segmented by Resist Type (ArF Immersion and More), Tone (Positive and Negative), Application (Semiconductors and ICs and More), End-User Industry (Electronics and Electricals and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region accounted for 72.10% of global revenue in 2025, driven by dense logic capacity in Taiwan and South Korea, as well as the expansion of mature-node fabs in China. TSMC's 2nm ramp and high-performance computing package lines consume increasing volumes of EUV and thick-film materials, while Samsung's 3D NAND capacity drives demand for high-selectivity KrF resists. Japan's equipment ecosystem, Tokyo Electron coating tracks, and Nikon steppers, support domestic suppliers, creating a tightly integrated supply chain.

North America is forecast to record an 11.49% CAGR through 2031 as the CHIPS Act stimulates the construction of new greenfield fabs. Intel's Ohio campus, TSMC's Arizona site, and Samsung's Texas facility together add more than 300,000 wpm of leading-edge capacity by 2028, underpinning local resist and ancillary chemical demand. DuPont's Colorado expansion and Dow's Michigan expansion aim to supply the region and reduce trans-Pacific logistics risk.

Europe faces stringent REACH compliance, which raises formulation costs, yet benefits from Intel's large-scale investment in Ireland and prospective fabs in Germany. Local material suppliers, Merck KGaA and BASF, utilize their regulatory expertise to secure qualification for EUV lines. Eastern European countries court packaging and test operations, further diversifying the regional footprint.

Middle East & Africa and South America remain nascent but pursue specialty packaging and MEMS manufacturing, particularly for telecom base-stations and automotive sensors. Regional governments offer tax credits to attract backend assembly, bringing incremental photoresist volumes for G-line and I-line processes while advanced nodes stay concentrated elsewhere.

- ALLRESIST GmbH

- Asahi Kasei Corporation

- Avantor, Inc.

- Brewer Science, Inc.

- DJ MicroLaminates

- DONGJIN SEMICHEM CO. LTD

- DuPont

- Eternal Materials Co., Ltd.

- FUJIFILM Corporation

- Inpria

- JSR Corporation

- SEMI

- Kolon Industries, Inc.

- LG Chem

- Merck KGaA

- micro resist technology GmbH

- Microchemicals GmbH

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- TOKYO OHKA KOGYO CO., LTD.

- Jiangsu Nata Opto-electronic Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from semiconductor and AI accelerators

- 4.2.2 Accelerated EUV lithography adoption and High-NA roadmap

- 4.2.3 5G / IoT device proliferation expanding wafer starts

- 4.2.4 Government fab-incentive programs (US/EU Chips Acts)

- 4.2.5 Dry-deposited metal-oxide resists boosting EUV throughput

- 4.3 Market Restraints

- 4.3.1 Stringent HSE regulations on solvents and photo-acid generators

- 4.3.2 Supply-chain concentration and export-control exposure

- 4.3.3 EU REACH and F-gas phase-outs targeting fluorinated solvents

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resist Type

- 5.1.1 ArF Immersion

- 5.1.2 ArF Dry

- 5.1.3 KrF

- 5.1.4 G-Line

- 5.1.5 I-Line

- 5.1.6 EUV Metal-Oxide and Dry Resists

- 5.1.7 Other Types

- 5.2 By Tone

- 5.2.1 Positive

- 5.2.2 Negative

- 5.3 By Application

- 5.3.1 Semiconductors and ICs

- 5.3.2 Advanced Packaging (Fan-Out WLP, RDL)

- 5.3.3 Flat-Panel Displays (LCD/OLED)

- 5.3.4 Printed Circuit Boards

- 5.3.5 MEMS and Sensors

- 5.3.6 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Electronics and Electricals

- 5.4.2 Automotive and Mobility

- 5.4.3 Aerospace and Defense

- 5.4.4 Consumer Packaged Goods (Packaging)

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 Taiwan

- 5.5.1.5 India

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 ALLRESIST GmbH

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Avantor, Inc.

- 6.4.4 Brewer Science, Inc.

- 6.4.5 DJ MicroLaminates

- 6.4.6 DONGJIN SEMICHEM CO. LTD

- 6.4.7 DuPont

- 6.4.8 Eternal Materials Co., Ltd.

- 6.4.9 FUJIFILM Corporation

- 6.4.10 Inpria

- 6.4.11 JSR Corporation

- 6.4.12 SEMI

- 6.4.13 Kolon Industries, Inc.

- 6.4.14 LG Chem

- 6.4.15 Merck KGaA

- 6.4.16 micro resist technology GmbH

- 6.4.17 Microchemicals GmbH

- 6.4.18 Shin-Etsu Chemical Co., Ltd.

- 6.4.19 Sumitomo Chemical Co., Ltd.

- 6.4.20 TOKYO OHKA KOGYO CO., LTD.

- 6.4.21 Jiangsu Nata Opto-electronic Material Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment