|

시장보고서

상품코드

1906206

유럽의 인트라로지스틱스 자동화 시장 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Europe Intralogistics Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

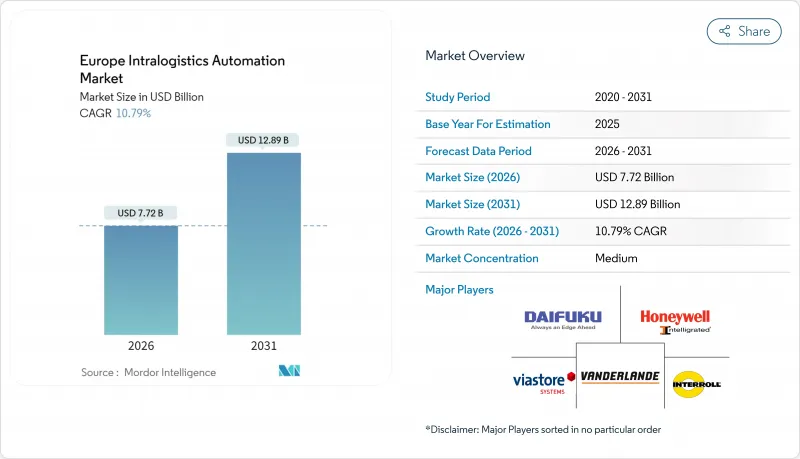

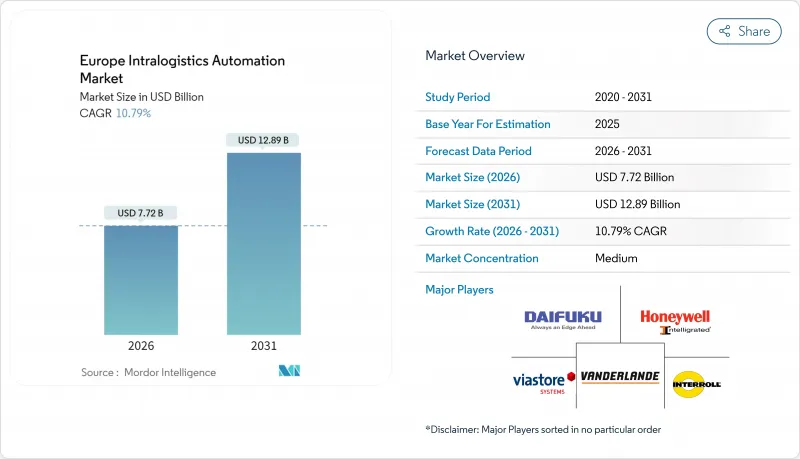

유럽의 인트라 물류 자동화 시장 규모는 2026년 77억 2,000만 달러로 평가되었습니다. 이는 2025년 69억 7,000만 달러에서 성장한 수치이며, 2031년에는 128억 9,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 10.79%로 성장할 전망입니다.

급증하는 전자상거래 물량, 구조적 노동력 부족, 강화되는 EU 지속가능성 규제가 자동화된 저장, 피킹, 자재 처리 솔루션에 대한 자본 지출을 가속화하고 있습니다. 시설 전체를 아우르는 전용 5G 네트워크로 가능해진 실시간 오케스트레이션은 자산 활용도를 높이고 있으며, AI 기반 예측 유지보수 및 디지털 트윈 소프트웨어는 시스템 가동 시간을 향상시키고 있습니다. 독일은 여전히 핵심 수요 중심지이자 기술 인큐베이터 역할을 하지만, 신흥 동유럽 공급업체들이 가격 경쟁력을 높이고 투자 회수 기간을 단축하기 시작했습니다. 이러한 요인들이 복합적으로 작용하며 유럽 내부 물류 자동화 시장은 향후 10년간 두 자릿수 성장세를 이어갈 전망입니다.

유럽의 인트라 물류 자동화 시장 동향 및 인사이트

전자상거래의 급성장과 옴니채널 대응 압력

폭발적인 온라인 판매 성장은 유럽 전역의 주문 처리 방식을 재편하고 있습니다. 오토 그룹은 시간당 18,000개 품목을 처리하며 주문량의 60%에 대해 익일 배송을 목표로 하는 일로바(Ilowa)의 고처리량 시설에 2억 6천만 유로를 투자했습니다. 소매업체와 3PL 업체들은 운영 중단 없이 대량 보충과 단일 품목 피킹 사이를 유연하게 전환할 수 있는 모듈형 큐브 및 셔틀 시스템을 도입하고 있습니다. 도시 부동산 제약으로 인해 상품이 사람에게 전달되는 마이크로 풀필먼트 센터 도입이 가속화되고 있으며, 큐브 기반 저장 시스템은 기존 건물에서 SKU 밀도를 3배로 높일 수 있게 합니다. 이로 인한 생산성 향상은 중견 유통업체조차도 자동화 투자 회수 기간을 단축시키고 있습니다. 이러한 동향은 변화하는 주문 패턴에 대비해 미래를 대비한 풀필먼트를 가능케 하는 확장 가능한 소프트웨어 정의 솔루션으로의 자본 유입을 지속시킬 것으로 예상됩니다.

EU27 국가의 노동력 부족과 임금 상승

고령화되는 노동력, 브렉시트 이후의 이민 패턴, 엄격한 근로 시간 규제로 인해 많은 EU 지역에서 물류 분야의 공석률이 12% 이상으로 상승했습니다. 기업들이 협업형 자동화로 인력 공백을 메우면서 중동부 유럽의 로봇 설치량은 28% 증가했으며, 독일의 기계 공학 부문은 이러한 수요를 포착하기 위해 턴키 시스템을 동쪽으로 수출하고 있습니다. 연간 평균 6-8%의 임금 인플레이션은 비용-편익 분석을 자본 투자 쪽으로 더욱 기울게 하고 있습니다. 이 변화는 질적 측면에서도 나타나고 있습니다 : 시설들은 수동 피커보다 차량 소프트웨어를 관리할 수 있는 기술자를 찾고 있어, 근로자 역량 강화를 위한 OEM과 직업 교육 기관 간의 협력을 촉진하고 있습니다. 전반적으로 노동력 부족은 유럽의 인트라 물류 자동화 시장에서 자동화를 "선택 사항"에서 "필수 요구 사항"으로 전환시키고 있습니다.

높은 자본 지출(CAPEX)과 긴 투자 회수 기간(ROI)

종합적인 내부 물류 자동화는 일반적으로 500만-1,000만 유로의 초기 투자가 필요하며, 이는 지역 물류 시장을 주도하는 중소기업(SME)에게 장벽입니다. 설문 조사에 따르면, 입증된 생산성 향상에도 불구하고 창고 관리자의 82%가 여전히 투자 규모에 대해 불안해하고 있으며, 금리 상승은 자금 조달 부담을 가중시키고 있습니다. 비용을 다년간 계약으로 분산하는 '서비스형 로봇(RaaS)' 모델이 확대되고 있는 것, 대부분의 금융기관은 여전히 자산담보대출을 선호하고 있습니다. 헴스커크 프레시 앤 이지(Heemskerk Fresh & Easy)의 농산물 시설처럼 4년 미만의 투자 회수 기간을 입증한 프로젝트들이 우려를 완화시키고 있으나, 많은 운영사들은 거시경제적 불확실성이 해소될 때까지 규모 확대를 미루고 있습니다. 따라서 자본 지출 민감도는 유럽 내부 물류 자동화 시장의 저마진 분야 진출을 제약하고 있습니다.

부문 분석

자율주행 모바일 로봇(AMR)은 2025년 매출에서 비교적 소폭의 비중을 차지했으나, 유럽 내부 물류 자동화 시장 내 가장 빠른 연평균 복합 성장률(CAGR) 11.21%로 성장할 것으로 전망됩니다. 이 부문의 성장 동력은 최소한의 고정 인프라 요구사항에 기반합니다. 차량 군을 몇 달이 아닌 몇 주 만에 추가하거나 재배치할 수 있습니다. 반면 자동화 저장 및 검색 시스템(AS/RS)은 식료품 및 패션 물류 분야에서 널리 채택된 검증된 큐브 및 셔틀 플랫폼 덕분에 2025년 유럽 내부 물류 자동화 시장 규모에서 27.32%의 최대 점유율을 유지했습니다.

비전 SLAM 내비게이션 기술이 도입 비용을 낮추면서 AMR 적용이 전자상거래에서 예비 부품 유통 분야로 확산되고 있습니다. KION 그룹의 모듈형 로봇은 중견 기업을 위한 플러그 앤 플레이 배포 방식을 제공함으로써 이러한 전환을 보여줍니다. AS/RS 공급업체들은 로봇 셔틀을 고밀도 큐브 내부에 내장하는 하이브리드 설계로 대응하며 기존 설치 기반을 보호하고 있습니다. 자동 분류, 팔레타이징, 컨베이어 하위 시스템은 상품-인 작업대를 출고 도크에 연결하는 핵심 보완 요소로 남아 있습니다. 이러한 범주 간 융합은 혼합 차량군 전반에 걸쳐 제어 소프트웨어를 통합할 수 있는 플랫폼 공급업체를 선호하도록 구매자를 유도하며, 유럽 내부 물류 자동화 시장의 통합 생태계로의 전환을 가속화하고 있습니다.

자동차 공장은 수십 년간의 린 제조 노하우로 자동화 주도 열차, 토크 추적 피킹 시스템, 실시간 품질 분석을 조기에 도입하며 2025년 유럽 내부 물류 자동화 시장 점유율 32.10%를 차지했습니다. 그러나 제약 및 헬스케어 분야는 더 엄격한 일련번호 규정과 콜드체인 수요를 반영해 연평균 11.40% 성장률을 기록 중입니다. 약국 체인 Dr. Max는 전자상거래 성장률 55%를 지원하는 자동화 유통 허브를 구축했으며, 이는 추적성 요구사항이 자동화 예산으로 직접 전환되는 사례를 보여줍니다.

우편 및 택배 사업자들은 B2C 택배 급증에 대응하기 위해 고속 분류기를 도입하고 있으며, 식품·음료 가공업체들은 24시간 배송 시간 내 신선도 유지를 위해 케이스 피킹을 자동화하고 있습니다. 공항과 일반 제조업체는 각각 수하물 처리 시스템 개편 및 순차적 키팅(JIS)으로 수요를 보완합니다. 그 결과 고객 기반이 확대되어 유럽 내부 물류 자동화 시장이 특정 산업의 침체로부터 보호받으며, 규제를 인지하는 유연한 솔루션의 필요성이 부각되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자상거래의 급성장과 옴니채널 대응의 압력

- EU27 국가의 노동력 부족과 임금 상승

- AI 기반 모바일 로봇 및 IoT의 급속한 발전

- 실시간 오케스트레이션을 가능케 하는 5G/프라이빗 LTE 도입

- EU 그린딜의 저탄소 인트라로지스틱스에의 인센티브

- 고밀도 자동화를 주도하는 도시형 마이크로 풀필먼트 모델

- 시장 성장 억제요인

- 높은 자본 지출(CAPEX) 및 긴 투자 회수 기간(ROI)

- 레거시 IT/OT 통합의 복잡성

- 네트워크화된 로봇 공학에 대한 사이버 보안 위협 증가

- 반도체 공급망의 혼란의 프로젝트 지연

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 인접 시장의 영향 분석

- 스트레치 포장기 시장

- 화물용 엘리베이터 시장

제5장 시장 규모와 성장 예측

- 제품 유형별

- 자율주행 모바일 로봇(AMR)

- 자동화 저장 및 검색 시스템(AS/RS)

- 자동 분류 시스템

- 팔레타이징 및 디팔레타이징 시스템

- 자동 컨베이어 시스템

- 주문 피킹 시스템

- 최종 사용자 업계별

- 공항

- 우편 및 택배

- 일반 제조업

- 자동차

- 식품 및 음료

- 소매, 창고 및 유통

- 기타 최종 사용자 산업

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 기능별

- 저장

- 주문 피킹 및 검색

- 분류 및 통합

- 포장 및 팔레타이징

- 운송 및 반송

- 국가별

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- AutoStore ASA

- BEUMER Group GmbH and Co. KG

- Daifuku Co., Ltd.

- Dematic GmbH(KION Group)

- Exotec SAS

- Honeywell International Inc.

- Interroll Holding AG

- Jungheinrich Aktiengesellschaft

- Kardex Holding AG

- KNAPP AG

- KUKA Aktiengesellschaft

- Linde Material Handling GmbH

- Murata Machinery, Ltd.

- Ocado Group plc

- SSI Schafer AG

- Swisslog Holding AG

- TGW Logistics Group GmbH

- Toyota Industries Corporation

- Vanderlande Industries BV

- Viastore Systems GmbH

- WITRON Logistik Informatik GmbH

제7장 시장 기회와 장래의 전망

HBR 26.01.26Europe intralogistics automation market size in 2026 is estimated at USD 7.72 billion, growing from 2025 value of USD 6.97 billion with 2031 projections showing USD 12.89 billion, growing at 10.79% CAGR over 2026-2031.

Surging e-commerce volumes, structural labor shortages, and tightening EU sustainability mandates are accelerating capital spending on automated storage, picking, and material-handling solutions. Real-time orchestration made possible by facility-wide private 5G networks is raising asset utilization, while AI-driven predictive maintenance and digital-twin software are boosting system uptime. Germany remains the pivotal demand center and technology incubator, yet emerging Eastern European suppliers are beginning to lower price points and shorten payback periods. Taken together, these forces position the Europe intralogistics automation market for a decade of double-digit expansion.

Europe Intralogistics Automation Market Trends and Insights

E-commerce Boom and Omnichannel Fulfillment Pressure

Explosive online sales growth is rewriting fulfillment blueprints across Europe. Otto Group invested EUR 260 million in a high-throughput facility in Ilowa that processes 18,000 items per hour and targets next-day delivery for 60% of orders. Retailers and 3PLs are specifying modular cube and shuttle systems that can flex between bulk replenishment and single-item picking without halting operations. Urban real-estate constraints are accelerating adoption of goods-to-person micro-fulfillment centers, while cube-based storage allows operators to triple SKU density in legacy buildings. The resulting productivity gains are shortening the payback period on automation investments even for mid-tier merchants. These dynamics are expected to keep capital flowing toward scalable, software-defined solutions that future-proof fulfillment against shifting order profiles.

Labor Shortages and Wage Inflation Across EU27

An aging workforce, post-Brexit migration patterns, and stringent working-time regulations have pushed vacancy rates in logistics above 12% in many EU regions. Robot installations climbed 28% in Central and Eastern Europe as companies offset staff gaps with collaborative automation, and Germany's mechanical-engineering sector is exporting turnkey systems eastward to capture that demand. Wage inflation averaging 6-8% annually is further tilting the cost-benefit equation toward capital investment. The shift is also qualitative: facilities seek technicians who can manage fleet software rather than manual pickers, spurring partnerships between OEMs and vocational institutes to upskill workers. Collectively, labor scarcity is transforming automation from optional to essential across the Europe intralogistics automation market.

High CAPEX and Long ROI Horizons

Comprehensive intralogistics automation often requires EUR 5-10 million upfront, a hurdle for SMEs that dominate regional logistics. Survey work shows 82% of warehouse leaders remain uneasy about investment volumes despite proven productivity gains; rising interest rates add to financing strain. A growing Robotics-as-a-Service model spreads costs over multi-year contracts, yet most banks still prefer asset-backed lending. Projects demonstrating sub-four-year payback-such as Heemskerk Fresh & Easy's produce facility-are easing concerns, but many operators still delay scope expansion until macro-economic clarity improves. CAPEX sensitivity therefore constrains penetration of the Europe intralogistics automation market in lower-margin verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in AI-Powered Mobile Robotics and IoT

- 5G/Private-LTE Roll-outs Enabling Real-Time Orchestration

- Legacy IT/OT Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Autonomous Mobile Robots (AMRs) accounted for a comparatively modest slice of 2025 revenue but are forecast to grow at 11.21% CAGR, the fastest within the Europe intralogistics automation market. The segment's momentum rests on minimal fixed infrastructure requirements: a fleet can be added or relocated in weeks rather than months. In contrast, Automated Storage and Retrieval Systems (AS/RS) retained the largest 27.32% share of Europe intralogistics automation market size in 2025 thanks to proven cube and shuttle platforms widely adopted in grocery and fashion fulfillment.

AMR adoption is spreading from e-commerce to spare-parts distribution as vision-SLAM navigation lowers commissioning costs. KION Group's modular robots illustrate this pivot by offering plug-and-play deployment for mid-cap firms. AS/RS suppliers are countering with hybrid designs that embed robot shuttles inside dense cubes, protecting their installed base. Automated sorting, palletizing, and conveyor subsystems remain critical complements that tie goods-to-person workstations into outbound docks. Convergence across these categories is prompting buyers to favor platform providers able to harmonize control software across mixed fleets, reinforcing the Europe intralogistics automation market's move toward integrated ecosystems.

Automotive plants locked in 32.10% of Europe intralogistics automation market share in 2025 as decades of lean-manufacturing expertise made them early adopters of automated tugger trains, torque-tracking pick systems, and real-time quality analytics. Yet the pharmaceuticals and healthcare vertical is accelerating at 11.40% CAGR, reflecting stricter serialization rules and cold-chain demands. Pharmacy chain Dr. Max commissioned an automated distribution hub that supports 55% e-commerce growth and illustrates how traceability requirements convert directly into automation budgets.

Post and parcel operators are embedding high-speed sorters to keep pace with B2C parcel surges, while food and beverage processors automate case picking to protect freshness under 24-hour delivery windows. Airports and general manufacturers round out demand with baggage-handling overhauls and just-in-sequence kitting respectively. The result is a broadening customer base that shields the Europe intralogistics automation market from sector-specific downturns and underscores the need for adaptable, regulation-aware solutions.

The Europe Intralogistics Automation Market Report is Segmented by Product Type (Mobile Robots, AS/RS, and More), End-User Industry (Airport, Post and Parcel, General Manufacturing, Automotive, Retail and Distribution, and More), Component (Hardware, Software, and Services), Function (Storage, Order Picking, Sorting, Packaging, Transportation), and Geography. Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd.

- AutoStore ASA

- BEUMER Group GmbH and Co. KG

- Daifuku Co., Ltd.

- Dematic GmbH (KION Group)

- Exotec SAS

- Honeywell International Inc.

- Interroll Holding AG

- Jungheinrich Aktiengesellschaft

- Kardex Holding AG

- KNAPP AG

- KUKA Aktiengesellschaft

- Linde Material Handling GmbH

- Murata Machinery, Ltd.

- Ocado Group plc

- SSI Schafer AG

- Swisslog Holding AG

- TGW Logistics Group GmbH

- Toyota Industries Corporation

- Vanderlande Industries B.V.

- Viastore Systems GmbH

- WITRON Logistik + Informatik GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom and omnichannel fulfilment pressure

- 4.2.2 Labour shortages and wage inflation across EU27

- 4.2.3 Rapid advances in AI-powered mobile robotics and IoT

- 4.2.4 5G / private-LTE roll-outs enabling real-time orchestration

- 4.2.5 EU Green Deal incentives for low-carbon intralogistics

- 4.2.6 Urban micro-fulfilment model driving high-density automation

- 4.3 Market Restraints

- 4.3.1 High CAPEX and long ROI horizons

- 4.3.2 Legacy IT / OT integration complexity

- 4.3.3 Rising cyber-security threats to networked robotics

- 4.3.4 Semiconductor supply-chain disruptions delaying projects

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Adjacent Market Influence Analysis

- 4.7.1 Stretch-Wrapping Machines Market

- 4.7.2 Goods Elevator Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Mobile Robots

- 5.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 5.1.3 Automated Sorting Systems

- 5.1.4 Palletising and De-palletising Systems

- 5.1.5 Automated Conveyors

- 5.1.6 Order-Picking Systems

- 5.2 By End-user Industry

- 5.2.1 Airport

- 5.2.2 Post and Parcel

- 5.2.3 General Manufacturing

- 5.2.4 Automotive

- 5.2.5 Food and Beverage

- 5.2.6 Retail, Warehousing and Distribution

- 5.2.7 Other End-user Industries

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Function

- 5.4.1 Storage

- 5.4.2 Order Picking and Retrieval

- 5.4.3 Sorting and Consolidation

- 5.4.4 Packaging and Palletising

- 5.4.5 Transportation and Conveyance

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 AutoStore ASA

- 6.4.3 BEUMER Group GmbH and Co. KG

- 6.4.4 Daifuku Co., Ltd.

- 6.4.5 Dematic GmbH (KION Group)

- 6.4.6 Exotec SAS

- 6.4.7 Honeywell International Inc.

- 6.4.8 Interroll Holding AG

- 6.4.9 Jungheinrich Aktiengesellschaft

- 6.4.10 Kardex Holding AG

- 6.4.11 KNAPP AG

- 6.4.12 KUKA Aktiengesellschaft

- 6.4.13 Linde Material Handling GmbH

- 6.4.14 Murata Machinery, Ltd.

- 6.4.15 Ocado Group plc

- 6.4.16 SSI Schafer AG

- 6.4.17 Swisslog Holding AG

- 6.4.18 TGW Logistics Group GmbH

- 6.4.19 Toyota Industries Corporation

- 6.4.20 Vanderlande Industries B.V.

- 6.4.21 Viastore Systems GmbH

- 6.4.22 WITRON Logistik + Informatik GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment