|

시장보고서

상품코드

1906861

라틴아메리카의 공장 자동화 및 산업용 제어 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Latin America Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

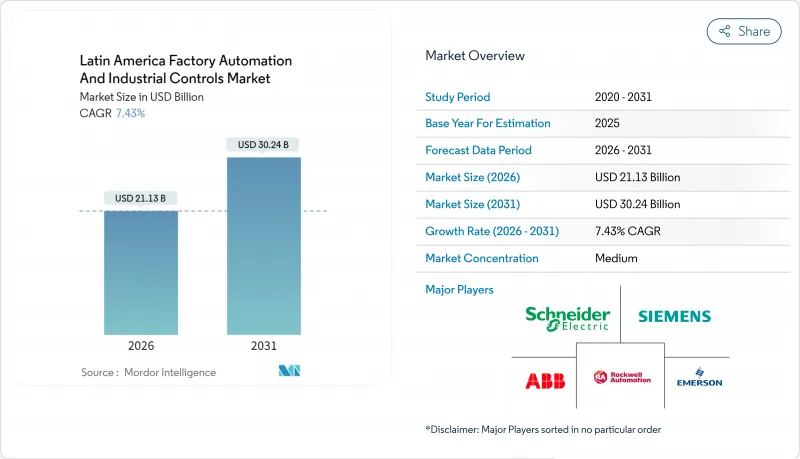

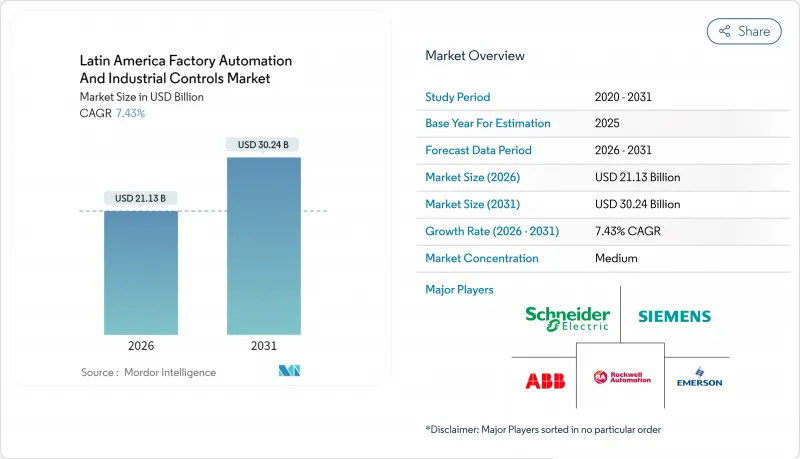

라틴아메리카의 공장 자동화 및 산업용 제어 시장은 2025년 196억 7,000만 달러로 평가되었으며, 2026년 211억 3,000만 달러에서 2031년까지 302억 4,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 7.43%로 전망됩니다.

디지털 전환 가속화, 니어쇼어링 활동 확대, 정부의 우대 조치가 엔드 투 엔드 자동화 솔루션에 대한 지속적인 수요를 창출하고 있습니다. 다양한 부문의 제조업체들은 가동 중지 시간을 줄이고 수출 지향 품질 기준을 달성하기 위해 실시간 분석, 예지보전 및 유연한 생산 라인을 선호합니다. 벤더 전략은 통화 변동과 공급망의 혼란을 줄이기 위해 현지 생산, 부가가치 서비스 및 특정 분야와의 파트너십을 강조합니다. 또한 이 지역에서는 공장의 레거시 자산 근대화에 따라 협동 로봇, AI 탑재 디지털 트윈, 클라우드 기반 감시 시스템의 도입이 급속히 진행되고 있습니다.

라틴아메리카의 공장 자동화 및 산업용 제어 시장의 동향 및 인사이트

전체 제조 산업에서 Industry 4.0 및 IIoT 도입 확대

브라질의 인더스트리 4.0 관련 지출은 2028년까지 3배로 증가할 것으로 예측되어 기업 전체의 센서 도입과 엣지 분석을 촉진하고 있습니다. 아르카 컨티넨탈은 클라우드 기반 플랫폼을 활용하여 4개국에 걸쳐 45곳의 공장과 1억 2,500만 명의 소비자를 연결하여 실시간 성능 대시보드를 실현하고 있습니다. 제조업체는 월별 지표에서 거의 실시간 KPI로 이행하여 대응력을 높이고 생산 병목 현상을 해소하고 있습니다. 시멘트 분야의 선도기업인 Votorantim Cimentos사는 예측 분석을 활용하여 제품 1개당 2,300만 레알(460만 달러)의 개량적 유지보수 비용을 절감하고 자산 신뢰성을 6% 향상시켰습니다. 그 결과, 라틴아메리카의 공장 자동화 및 산업용 제어 시장에서는 개별 생산 산업과 공정 산업 모두에 스마트 센서 네트워크와 데이터 구동 워크플로의 도입이 계속되고 있습니다.

정부 인센티브 프로그램이 스마트 공장에 대한 투자 가속화

브라질은 산업시설의 현대화에 1,866억 레알(373억 달러)을 계상하고 있습니다. 멕시코는 2024년 1-7월기에 480억 달러의 신규 제조 투자를 목력했으며, 그 절반 이상이 자동화 이니셔티브와 관련되어 있습니다. 대상을 좁힌 보조금, 세액 공제, 기술자 파견 제도는 라틴아메리카의 공장 자동화 및 산업용 제어 시장에서 중점 부문인 중소기업의 도입 장벽을 낮춥니다. WEG사 단독으로만 로봇에 의한 피킹, 반송, MES 플랫폼을 통합한 양국 간 생산 능력 확장에 1억 2,200만 달러를 계획하고 있습니다. 아르헨티나의 광업정책에서는 첨단제어시스템에 대한 관세 면제도 인정되고 있으며, 이 나라가 지역에서 가장 급속히 도입이 진행되는 지역임을 뒷받침하고 있습니다. 이러한 우대조치는 공적자금과 민간자본을 융합시킴으로써 시너지 효과를 낳고 기술의 보급을 가속화하고 있습니다.

중소기업의 높은 초기 설비 투자와 ROI 불확실성

조사 데이터에 따르면, 브라질의 중소기업은 자동화 도입에 대기업에 최대 2배의 지연을 겪고 있으며, 자금 조달이나 기술적 노하우의 부족이 장벽이 되고 있습니다. 협동 로봇은 이러한 격차를 줄이며 기존 로봇보다 도입 비용이 20-30% 낮아 단기간에 투자 회수가 가능합니다. 그러나 총 투자액은 여전히 자본 예산을 압박합니다. 임대 모델과 공급업체 중심의 교육은 위험의 일부를 줄일 수 있지만, 라틴아메리카의 공장 자동화 및 산업용 제어 시장은 중소기업의 잠재력을 끌어내기 위해 자금 조달 구조의 추가적인 적응을 요구합니다. SENAI와 같은 공공기관은 장비 구매 전에 ROI 시나리오를 검증할 수 있는 저비용 시뮬레이션 워크숍을 제공합니다.

부문 분석

산업용 제어 시스템(ICS)은 2025년 라틴아메리카의 공장 자동화 및 산업용 제어 시장에서 30.38%의 점유율을 차지했으며, 석유, 가스, 광업, 식품 플랜트에 PLC, SCADA, DCS를 도입했습니다. 페트로브라스사는 예측 분석을 활용하여 정유소의 최적화를 도모하고, 페멕스사는 지역 전체의 파이프라인용 SCADA를 도입하여 누설 감지와 유량 제어를 실현하고 있습니다. 업그레이드는 MES(제조 실행 시스템)와 HMI(휴먼 머신 인터페이스) 계층을 통합하는 경우가 많으며, 운영자는 배치 시퀀싱 및 규제 보고 업무의 효율화를 실현할 수 있습니다. 공정 산업이 노후화된 제어장치의 업그레이드와 사이버 보안 대책의 확충을 진행하는 가운데, 이 부문의 성장은 안정화되고 있습니다.

필드 디바이스는 8.46%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 라틴아메리카의 공장 자동화 및 산업용 제어 시장에서 가장 빠른 성장 속도를 보이고 있습니다. 이는 로봇 도입의 급증과 스마트 센서 업그레이드가 견인하고 있습니다. 브라질에서는 2021년에 1,595대의 산업용 로봇이 신규 도입되었으며 협동 로봇(코봇)의 도입 대수는 기존 로봇의 4배에 달했습니다. 품질검사용 비전시스템과 내부물류용 무인반송차(AGV)는 전자기기, 금속, 제약산업에서 보급이 진행되고 있습니다. 또한 에너지 효율적인 구동장치는 제조업체가 kW당 전력 소비를 줄이고 유지보수 비용을 줄이는 가운데 지속가능성 요구사항을 달성하는 데에도 기여합니다.

하드웨어는 50억 달러 규모의 수쿠리 제지 공장 등 대규모 프로젝트(광범위한 센서, 액추에이터, 개폐 장치가 필요함)에 힘입어 2025년 라틴아메리카의 공장 자동화 및 산업용 제어 시장에서 30.25%의 점유율을 유지했습니다. 그러나 세계 공급망의 재조정 및 환율 변동으로 인해 부품 마진이 축소되는 경향이 있습니다.

서비스 분야는 고객이 턴키 통합, 트레이닝, 예지보전을 요구하는 가운데 8.07%의 연평균 복합 성장률(CAGR)로 확대되고 있으며, 벤더는 지속적인 수익원을 확보하는 입장에 있습니다. 실적 연동 계약은 일반적이며 Votorantim Cimentos는 가동 중지 시간 회피에 연동된 서비스 수수료를 지불합니다. 소프트웨어는 시장 점유율의 약 4분의 1을 차지하며, 자산 중심의 분석과 여러 기지에 대한 가시성을 제공함으로써 이러한 모델을 지원합니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 제조업 전체에서의 인더스트리 4.0 및 IIoT 도입 확대

- 정부의 인센티브 프로그램이 스마트 공장 투자를 가속화

- 비용 절감 압력과 생산성 최적화 요청

- 저탄소 재생에너지 제조를 위한 브라질로의 파워 쇼어링

- 마킬라도라 관련 니어쇼어링의 급증이 멕시코에서의 자동화 수요를 견인

- 기존 플랜트에서 AI 탑재 디지털 트윈의 파일럿 도입이 급속히 진전

- 억제요인

- 중소기업을 위한 고액의 초기 설비 투자와 ROI 불확실성

- 고도의 자동화에 필요한 숙련 노동자의 심각한 부족

- 현지 통화의 변동성으로 장기 투자 정체

- 산업용 제어 시스템에 대한 사이버 피지컬 공격의 격화

- 업계 밸류체인 분석

- 규제 상황

- 기술 전망

- 거시경제 요인의 영향

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급자의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 산업용 제어 시스템

- 분산제어시스템(DCS)

- 프로그래머블 로직 컨트롤러(PLC)

- 모니터링 제어 및 데이터 수집(SCADA)

- 제조 실행 시스템(MES)

- 제품 수명주기 관리(PLM)

- 휴먼 머신 인터페이스(HMI)

- 전사적 자원 계획(ERP)

- 필드 디바이스

- 머신 비전

- 산업용 로봇

- 센서 및 트랜스미터

- 모터 및 드라이브

- 릴레이 및 스위치

- 산업용 제어 시스템

- 컴포넌트 유형별

- 하드웨어

- 소프트웨어

- 서비스

- 최종 사용자 산업별

- 자동차

- 식품 및 음료

- 석유 및 가스

- 화학제품 및 석유화학제품

- 전력 및 유틸리티

- 제약

- 전자 및 전기기기

- 광업 및 금속

- 기타 최종 사용자 산업

- 전개 모드별

- 온프레미스

- 클라우드

- 하이브리드

- 국가별

- 브라질

- 멕시코

- 아르헨티나

- 칠레

- 콜롬비아

- 기타 라틴아메리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Siemens AG

- ABB Ltd

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- General Electric Co.

- Dassault Systemes SE

- Autodesk Inc.

- Aspen Technology Inc.

- Bosch Rexroth AG

- Yokogawa Electric Corporation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Festo SE and Co. KG

- Endress Hauser Group Services AG

- WEG Industrias SA

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Latin America factory automation and industrial controls market was valued at USD 19.67 billion in 2025 and estimated to grow from USD 21.13 billion in 2026 to reach USD 30.24 billion by 2031, at a CAGR of 7.43% during the forecast period (2026-2031).

Accelerated digital transformation, growing nearshoring activity, and government incentives are creating sustained demand for end-to-end automation solutions. Manufacturers across diverse sectors are prioritizing real-time analytics, predictive maintenance, and flexible production lines to reduce downtime and meet export-oriented quality standards. Vendor strategies emphasize localized production, value-added services, and domain-specific partnerships to mitigate currency volatility and supply chain disruptions. The region is also witnessing rapid uptake of collaborative robots, AI-enabled digital twins, and cloud-based supervisory systems as plants modernize legacy assets.

Latin America Factory Automation And Industrial Controls Market Trends and Insights

Rising Industry 4.0 and IIoT Adoption Across Manufacturing

Brazil's Industry 4.0 spending is forecast to triple by 2028, catalyzing enterprise-wide sensor rollouts and edge analytics. Arca Continental uses a cloud-based platform to connect 45 plants and serve 125 million consumers across four countries, enabling real-time performance dashboards. Manufacturers are shifting from monthly metrics to near-instant KPIs, elevating responsiveness and trimming production bottlenecks. Cement major Votorantim Cimentos reduced corrective maintenance costs by BRL 23 million (USD 4.6 million) per site through the use of predictive analytics, improving asset reliability by 6%. As a result, the Latin America factory automation and industrial controls market continues to embed smart-sensor networks and data-driven workflows across both discrete and process industries.

Government Incentive Programs Accelerating Smart-Factory Investments

Brazil earmarked BRL 186.6 billion (USD 37.3 billion) for modernizing industrial facilities, while Mexico reported USD 48 billion in new manufacturing commitments during the first seven months of 2024, over half of which was tied to automation initiatives. Targeted subsidies, tax credits, and technical residencies lower adoption barriers for small and mid-sized enterprises, a priority segment for the Latin America factory automation and industrial controls market. WEG alone plans USD 122 million in dual-country capacity expansions that integrate robotic picking, conveyance, and MES platforms. Argentina's mining policy also grants duty exemptions on advanced controls, supporting its position as the region's fastest-growing adopter. These incentives deliver a multiplier effect by blending public finance with private capital, thereby accelerating the diffusion of technology.

High Upfront Capex and ROI Uncertainty for SMEs

Survey data show that Brazilian SMEs lag behind large firms by as much as 2 times in automation adoption, constrained by access to finance and technical know-how. Collaborative robots narrow this gap, costing 20-30% less to deploy than traditional robots and offering quick paybacks, yet total investment still stretches capital budgets. Leasing models and vendor-led training mitigate some risk, but the Latin America factory automation and industrial controls market must further adapt financing structures to unlock SME potential. Public institutions, such as SENAI, offer low-cost simulation workshops that enable companies to validate ROI scenarios before committing to equipment purchases.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Reduction Pressure and Productivity Optimization Mandates

- Rapid Uptake of AI-Enabled Digital-Twin Pilots in Brownfield Plants

- Acute Skilled-Labor Shortage for Advanced Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial Control Systems (ICS) represented 30.38% of the Latin America factory automation and industrial controls market in 2025, underpinned by deployments of PLC, SCADA, and DCS across oil and gas, mining, and food plants. Petrobras leverages predictive analytics to optimize refineries, while PEMEX employs region-wide pipeline SCADA for leak detection and flow control. Upgrades frequently bundle MES and HMI layers, enabling operators to streamline batch sequencing and regulatory reporting. The segment's growth remains steady as process industries refresh aging controllers and expand cybersecurity safeguards.

Field Devices are advancing at an 8.46% CAGR, the fastest pace within the Latin America factory automation and industrial controls market, propelled by surging robot installations and smart-sensor retrofits. Brazil added 1,595 new industrial robots in 2021, with cobots outpacing conventional units by a factor of four. Vision systems for quality inspection and autonomous guided vehicles for intralogistics are gaining traction in the electronics, metals, and pharmaceutical industries. Energy-efficient drives also support sustainability mandates, as manufacturers target lower kilowatt-hour intensity and reduced maintenance bills.

Hardware retained a 30.25% share of the Latin America factory automation and industrial controls market size in 2025, supported by mega-projects such as the USD 5 billion Sucuriu pulp mill that requires extensive sensors, actuators, and switchgear. However, component margins are tightening due to global supply chain rebalancing and currency fluctuations.

Services are expanding at 8.07% CAGR as clients demand turnkey integration, training, and predictive maintenance, positioning vendors for recurring revenue streams. Outcome-based contracts are common, with Votorantim Cimentos paying service fees tied to the avoidance of downtime. Software, at roughly one-quarter market share, anchors these models by providing asset-centric analytics and multi-site visibility.

The Latin America Factory Automation and Industrial Controls Market Report is Segmented by Product Type (Industrial Control Systems, Field Devices), Component Type (Hardware, Software, Services), End-User Industry (Automotive, Food and Beverages, and More), Deployment Mode (On-Premise, Cloud, Hybrid), and Country (Brazil, Mexico, Argentina, Chile, Colombia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens AG

- ABB Ltd

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- General Electric Co.

- Dassault Systemes SE

- Autodesk Inc.

- Aspen Technology Inc.

- Bosch Rexroth AG

- Yokogawa Electric Corporation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Festo SE and Co. KG

- Endress+Hauser Group Services AG

- WEG Industrias S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Industry 4.0 and IIoT adoption across manufacturing

- 4.2.2 Government incentive programmes accelerating smart-factory investments

- 4.2.3 Cost-reduction pressure and productivity optimisation mandates

- 4.2.4 Powershoring to Brazil for low-carbon renewable-energy manufacturing

- 4.2.5 Maquiladora-linked near-shoring surge driving automation demand in Mexico

- 4.2.6 Rapid uptake of AI-enabled digital-twin pilots in brownfield plants

- 4.3 Market Restraints

- 4.3.1 High upfront capex and ROI uncertainty for SMEs

- 4.3.2 Acute skilled-labour shortage for advanced automation

- 4.3.3 Local-currency volatility stalling long-cycle investments

- 4.3.4 Escalating cyber-physical attacks on industrial control systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Industrial Control Systems

- 5.1.1.1 Distributed Control System (DCS)

- 5.1.1.2 Programmable Logic Controller (PLC)

- 5.1.1.3 Supervisory Control AND Data Acquisition (SCADA)

- 5.1.1.4 Manufacturing Execution System (MES)

- 5.1.1.5 Product Lifecycle Management (PLM)

- 5.1.1.6 Human Machine Interface (HMI)

- 5.1.1.7 Enterprise Resource Planning (ERP)

- 5.1.2 Field Devices

- 5.1.2.1 Machine Vision

- 5.1.2.2 Robotics (Industrial)

- 5.1.2.3 Sensors and Transmitters

- 5.1.2.4 Motors and Drives

- 5.1.2.5 Relays and Switches

- 5.1.1 Industrial Control Systems

- 5.2 By Component Type

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Food and Beverages

- 5.3.3 Oil and Gas

- 5.3.4 Chemical and Petrochemical

- 5.3.5 Power and Utilities

- 5.3.6 Pharmaceutical

- 5.3.7 Electronics and Electrical

- 5.3.8 Mining and Metals

- 5.3.9 Other End-user Industries

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Mexico

- 5.5.3 Argentina

- 5.5.4 Chile

- 5.5.5 Colombia

- 5.5.6 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 ABB Ltd

- 6.4.3 Rockwell Automation Inc.

- 6.4.4 Schneider Electric SE

- 6.4.5 Emerson Electric Co.

- 6.4.6 Honeywell International Inc.

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 General Electric Co.

- 6.4.9 Dassault Systemes SE

- 6.4.10 Autodesk Inc.

- 6.4.11 Aspen Technology Inc.

- 6.4.12 Bosch Rexroth AG

- 6.4.13 Yokogawa Electric Corporation

- 6.4.14 Omron Corporation

- 6.4.15 FANUC Corporation

- 6.4.16 Yaskawa Electric Corporation

- 6.4.17 KUKA AG

- 6.4.18 Festo SE and Co. KG

- 6.4.19 Endress+Hauser Group Services AG

- 6.4.20 WEG Industrias S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment