|

시장보고서

상품코드

1906908

작물 보호 화학제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

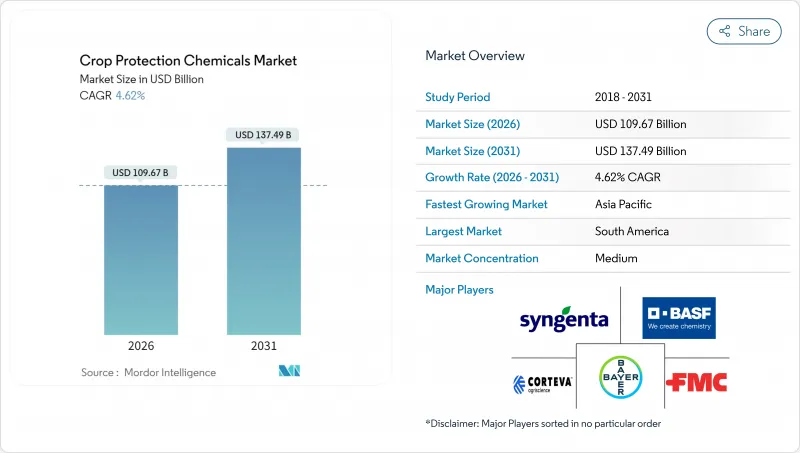

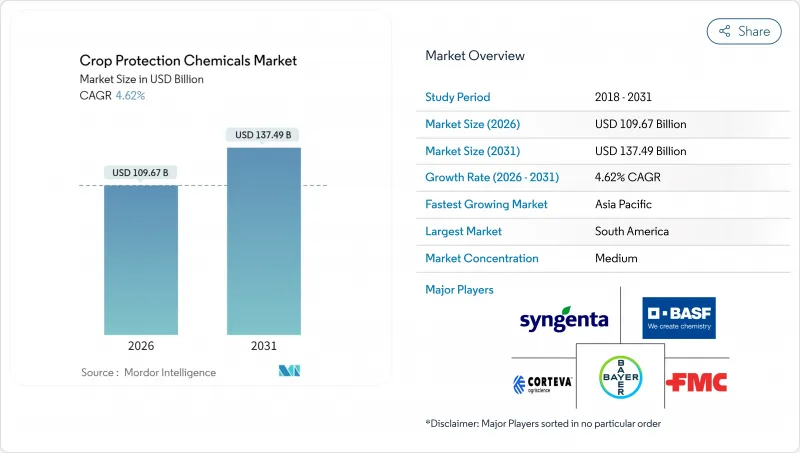

농약 시장은 2025년의 1,048억 3,000만 달러로 평가되었고, 2026년에는 1,096억 7,000만 달러로 성장할 것으로 예측되며, 2026-2031년 CAGR 4.62%로 성장을 지속하여, 2031년까지 1,374억 9,000만 달러에 달할 것으로 전망됩니다.

제초제 다용형의 유전자 변형 작물에 대한 안정적인 수요, 정밀 농업의 도입, 기후 변화에 따른 해충의 이동이 규제 강화에도 불구하고 성장 곡선을 지지하고 있습니다. 정밀 살포기, 드론에 의한 스폿 처리, 가변율 살포 시스템에 의해 생산자는 효과를 유지하면서 폐기물을 삭감할 수 있어 노동력 부족에 직면하는 지역에서도 농약 시장이 생산성 향상을 파악하는 데 도움이 되고 있습니다. 남미는 브라질에서 대두 생산 확대를 배경으로 가장 큰 점유율을 차지하고 있지만 아시아태평양은 주로 인도와 중국의 상업 농업 통합으로 가장 높은 CAGR을 기록하고 있습니다. 엽면 처리가 여전히 가장 일반적인 투여 방법인 반면, 토양 처리가 가장 높은 성장률을 나타내고 있으며, 재생 농업의 실천이 발아 전처리제의 이용을 촉진하고 있습니다.

세계의 작물 보호 화학제품 시장 동향 및 인사이트

유전자 재조합 작물의 제작 면적 확대

제초제 내성 대두, 옥수수, 면화가 현재 아메리카에서의 작제 결정을 지배하고 있으며, 농지 전체가 확대되는 가운데 헥타르당 화학제품 사용량은 증가하고 있습니다. 브라질에서는 2024년에 제작 면적의 95%에서 유전자 변형 대두가 재배되어 글리포세이트와 디캄바의 판매량을 과거 최고로 밀어 올렸습니다. 생산자는 저항성 발생을 지연시키기 위해 여러 작용 기전을 조합하여 시즌을 통한 수익을 확보할 수 있는 종자와 농약의 통합 패키지를 제공하는 공급업체를 선호합니다. 아르헨티나가 내건성 대두 'HB4'를 승인한 것으로, 특히 물 스트레스에 의해 역사적으로 제약을 받아 온 변경 지역에 있어서, 대상 작부 면적이 더욱 확대되고 있습니다. 특허 기한이 다가오는 가운데, 브랜드 제조업체는 이익률 유지를 위해 특성 강화형 화학제품 패키지의 개발을 가속시키고 있습니다. 한편, 제네릭 제조업체는 특허 만료 활성 성분 공급량 확대에 주력하고 있습니다. 유전자 변형 기술의 파도는 종합적으로 제초제 수요를 지속시켜 복합 제품의 프리미엄 가격 설정을 지지하고, 특성 패키지에 특화된 제제 기술에 대한 추가 투자를 촉진하고 있습니다.

제초제 내성 잡초 증가

글리포세이트 내성 파머 아마란서스는 미국 27개 주로 확대되어 남미 전역으로 진행 중이며, 생산자는 약물의 회전 및 살포 빈도 증가를 강요하고 있습니다. 내성 생물형은 현재 ALS 억제제에도 위협을 주고 2-4제의 탱크 믹스가 새로운 표준이 되고 있습니다. 이 내성 경쟁은 새로운 작용기전을 가진 약물과 관리를 단순화하는 프리미엄 프리믹스 수요를 높이고 있습니다. 화학 혁신 파이프라인은 정체된 10년을 거쳐 다시 중요성을 늘리고, 디지털 스카우팅 툴은 피해가 제어 불능이 되기 전에 발생 장소를 특정하는 수단으로서 보급이 진행되고 있습니다. 1에이커당 제초제 비용 상승 및 잠재적인 수율 손실로 인한 경제적 부담은 방제 효과를 회복시키는 솔루션에 대한 투자 의욕을 생산자에게 유지하고 있으며, 혁신자는 가까운 미래에 명확한 수익 기반을 형성하고 있습니다.

엄격한 농약 금지 및 잔류 기준치 계약(유럽 연합에 초점)

유럽 당국은 유효 성분의 심사를 계속하고 있으며, 2024년에는 15개 주요 화학제품이 갱신을 상실할 전망입니다. 동시에 잔류 기준값은 꾸준히 인하됩니다. 남미와 아프리카의 수출 지향형 생산자는 다른 지역에 판매하는 경우에도 EU의 허용 기준을 충족하기 위한 컴플라이언스 비용에 직면하고 있습니다. 이는 세계 곡물 구매자가 가장 엄격한 기준을 준수하기 때문입니다. 중소 제조업체는 신규 데이터 패키지의 자금 조달에 고민해, 독성학 및 환경 영향 평가 자료에 대한 투자가 가능한 대기업의 시장 점유율 확대를 가속시키고 있습니다. 생산자는 잔류 프로파일이 낮은 신형 고가농약으로 전환하는 한편, 헥타르당 지출은 증가하는 반면, 상품 가격이 연화되면 이익률이 압박됩니다. 유효한 농약 부족으로 인해 일부 농가들은 기존 제품으로의 회귀와 살포 빈도 증가를 강요하고 정책 의도와는 반대로 화학제품 총 사용량이 증가하는 모순이 발생하고 있습니다. 조사의 우선순위는 바이오기반 또는 저잔존성 분자로 이행하여, 개발 기간이 장기화함과 동시에 진입 장벽이 높아집니다. 규제 및 상업적 압력의 복합 효과로 인해 예측 CAGR은 0.8포인트 감소하고 유예 기간이 끝나면 2027년까지 가장 심각한 수익 영향을 미칠 것으로 예측됩니다. EU 규제 대응 팀이 충실하고 신속한 승인이 예상되는 파이프라인 활성 물질을 가진 기업은 신규제하에서 상대적 우위성을 획득합니다.

부문 분석

제초제는 2025년 작물 보호 화학제품 시장에서 42.35%의 점유율을 차지하였고, 시장 규모의 최대 부분을 형성함과 동시에 증분수익 성장의 대부분을 창출하였습니다. 팔머 아마란서스나 코니자 속종에 있어서 지속적인 내성 문제에 의해 멀티 사이트 대책이 불가결하게 되어, 생산자는 프리미엄 가격대의 복합 제제를 채용하는 경향에 있습니다. 글리포세이트는 여전히 판매량에서 우위를 유지하고 있으며, 수요는 HPPD 억제제, PPO 억제제 및 내성 발생 후 방제를 목적으로 하는 신규 독자 화학물질로 이행하고 있습니다. 이 제품 구성의 향상은 2031년까지 견고한 5.02% CAGR 예측을 지원합니다.

유전자 변형 작물의 특성 도입이 계속되고 있으며, 특히 브라질과 아르헨티나에서는 헥타르당 제초제 사용량이 높은 수준을 유지하고 있습니다. 종자와 농약을 통합한 제공 형태를 통해 주요 공급업체는 특성을 맞춤형 살포제와 결합할 수 있어 지적 재산과 조익률을 모두 보호합니다. 살균제는 날씨에 연동한 병해의 발생 증가와, 대두 녹병에 대한 새로운 작용기전을 가지는 레비솔(Revysol)의 2024년 브라질 발매에 지지되어 거의 동등한 점유율을 유지하고 있습니다. 살충제는 기후 변화에 따른 해충의 침입이 발생했을 때 산발적인 수요 급증을 볼 수 있습니다. 살선충제 및 살연체 동물제는 틈새 분야이지만, 약간의 수율 감소로도 수익성을 손상시키는 고부가가치 원예 분야에 있어서 필수적입니다.

작물 보호 화학제품 시장 보고서는 기능별(살균제, 제초제, 살충제, 살패제 등), 적용 방법별(화학 관주, 잎면 살포, 종자 처리 등), 작물 유형별(상업 작물, 과일 및 야채, 곡물 및 곡류, 콩류 및 지방 종자 등), 지역별(아프리카, 유럽, 북미 등)으로 구성되어 있습니다. 시장 예측은 금액(달러) 및 수량(메트릭톤)으로 제공됩니다.

지역별 분석

남미는 2025년 작물 보호 화학제품 시장 점유율의 41.85%를 차지했습니다. 이것은 브라질 셀라드 사바나에서 대규모 대두 옥수수 생산이 견인한 것입니다. 브라질 단독으로 지역 총량의 60% 이상을 소비했으며, 2024년 시즌 연속 작제 사이클에서 기록적인 농약 구입이 이를 지원했습니다. 아르헨티나에서는 수출 지향형 농장이 성장에 기여하고, 유전자 변형(GM) 작물의 도입률이 국내 제작 면적의 95%를 넘어 제초제 다용형 농업을 강화하고 있습니다. 호천과 외화 획득을 우선하는 정부 정책이 항만에서의 물류 과제가 산견되는 가운데도 남미의 꾸준한 성장을 지지하고 있습니다.

아시아태평양은 가장 성장하는 시장이며, 2031년까지의 연평균 성장률(CAGR)은 4.73%로 예측됩니다. 인도, 중국, 동남아시아 국가에서 농지 집약화 및 기계화의 진전이 성장을 이끌고 있습니다. 인도에서는 상업 농업의 추진으로 2024년 농약 사용량이 15% 증가했습니다. 이는 대규모화된 농지에서 시즌을 통한 해충 방제 프로그램이 필요했기 때문입니다. 중국에서는 환경 정책에 의해 농약 공장의 집약화가 진행되는 한편, 국가 식품 안전 기준에 적합한 고효능 및 저잔류 농약의 사용이 촉진되고 있습니다. 또한 인도네시아, 태국, 베트남에서는 습윤 기후 하에서의 작물 보호에 특수한 살균제 및 살충제를 필요로 하는 팜유의 확대와 집약적 벼농사 시스템이 수요 증가에 기여하고 있습니다.

북미는 세계 소비량의 대부분을 차지하고 있으며, 정밀 농업의 도입(대규모 농장의 35%로 채용되어 시용 시기를 최적화)이 이것을 지지하고 있습니다. 미국에서는 유전자 변형 작물의 작물 면적 확대 및 잡초 내성 증가로 이익률이 심한 상황에도 불구하고 1에이커당 제초제 지출이 유지되고 있습니다. 유럽도 수요의 대부분을 차지하고 있지만, 엄격한 규제 및 잔류 기준으로 저용량 화학제품 및 생물학적 솔루션에 대한 투자가 이동하고 있습니다. 이러한 제약이 있음에도 불구하고 특수 과일 및 채소 분야는 높은 시장 가치를 유지하고 있습니다. 아프리카는 여전히 가장 작은 지역 시장이지만 남아프리카의 상업 농업 프로젝트와 서 아프리카의 신흥 기지에서는 현대 작물 보호 프로그램의 도입이 시작되어 장기적인 수요가 점차 증가하고 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제2장 보고서 제공

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

- 헥타르당 농약 소비량

- 유효 성분의 가격 분석

- 규제 프레임워크

- 아르헨티나

- 호주

- 브라질

- 캐나다

- 칠레

- 중국

- 프랑스

- 독일

- 인도

- 인도네시아

- 이탈리아

- 일본

- 멕시코

- 미얀마

- 네덜란드

- 파키스탄

- 필리핀

- 러시아

- 남아프리카

- 스페인

- 태국

- 우크라이나

- 영국

- 미국

- 베트남

- 밸류체인 및 유통 채널 분석

- 시장 성장 촉진요인

- 유전자 변형 작물의 제작 면적 확대

- 제초제 내성 잡초 증가

- 정밀 농업 기술의 채용

- 아시아태평양 및 남미에서 상업 농업의 급속한 성장

- 선택적 화학제품을 선호하는 재생 농업

- 기후 변화에 따른 해충의 온대 지역으로의 이동

- 시장 성장 억제요인

- 농약의 엄격한 금지 및 잔류 기준치(MRL) 계약(유럽 연합(EU)에 초점)

- 글리포세이트 및 ALS 억제제에 대한 잡초 내성의 가속화

- 불안정한 중국산 테크니컬 등급 공급망

- 생물 농약의 급속한 보급에 의한 합성 농약 매출의 분쟁

제5장 시장 규모 및 성장 예측(금액 및 수량)

- 기능별

- 살균제

- 제초제

- 살충제

- 연체동물용 살충제

- 살선충제

- 적용 방법별

- 화학관주

- 잎면 살포

- 훈증

- 종자 처리

- 토양 처리

- 작물 유형별

- 상업 작물

- 과일 및 채소

- 곡물 및 곡류

- 콩류 및 지방 종자

- 잔디 및 관상식물

- 지역별

- 아프리카

- 남아프리카

- 기타 아프리카

- 아시아태평양

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 미얀마

- 파키스탄

- 필리핀

- 태국

- 베트남

- 기타 아시아태평양

- 유럽

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 기타 유럽

- 북미

- 캐나다

- 멕시코

- 미국

- 기타 북미

- 남미

- 아르헨티나

- 브라질

- 칠레

- 기타 남미

- 아프리카

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 개황

- 기업 프로파일

- BASF SE

- Bayer AG

- Corteva Inc.

- FMC Corporation

- Jiangsu Yangnong Chemical Group Co., Ltd.

- Nufarm Limited

- Sumitomo Chemical Co., Ltd.

- Syngenta Group Co., Ltd.

- UPL Ltd.

- Lallemand Inc.(Animal Nutrition)

- EW Nutrition GmbH

- Kemin Industries Inc.

- Novus International Inc.

- Vitafor NV

제7장 CEO에 대한 주요 전략적 질문

AJY 26.01.26The crop protection chemicals market is expected to grow from USD 104.83 billion in 2025 to USD 109.67 billion in 2026 and is forecast to reach USD 137.49 billion by 2031 at 4.62% CAGR over 2026-2031.

Steady demand for herbicide-intensive, genetically modified crops, the adoption of precision agriculture, and climate-driven pest migration continue to sustain the growth curve, despite tighter regulatory oversight. Precision sprayers, drone-based spot treatments, and variable-rate application systems enable growers to cut waste while maintaining efficacy, helping the crop protection chemicals market capture productivity gains even in regions facing labor shortages. South America accounts for the largest share, driven by Brazil's expansion of soybean production, while the Asia-Pacific region records the fastest CAGR, largely due to commercial farming consolidation in India and China. Foliar treatments remain the most common delivery mode, yet soil treatments post the highest growth, and regenerative practices encourage pre-emergent chemistries.

Global Crop Protection Chemicals Market Trends and Insights

GM-Crop Acreage Expansion

Herbicide-tolerant soybeans, corn, and cotton now dominate planting decisions in the Americas, lifting per-hectare chemical intensity even as overall farmland expands. Brazil planted GM soybeans on 95% of its area in 2024, which propelled glyphosate and dicamba sales to record highs. Growers stack multiple modes of action to delay resistance, favoring suppliers with integrated seed and chemical bundles that lock in season-long revenue. Argentina's approval of HB4 drought-tolerant soybeans further broadens the addressable acreage, especially in marginal regions that have been historically constrained by water stress. As patents expire, branded players accelerate the development of trait-plus-chemistry packages to protect their margins, while generic manufacturers focus on increasing volume in off-patent actives. Collectively, the GM wave sustains herbicide demand, supports premium pricing on combination products, and drives incremental investments in formulation technologies tailored to trait packages.

Rising Herbicide-Resistant Weeds

Glyphosate-resistant Palmer amaranth has spread to 27 U.S. states and is advancing across South America, forcing growers to rotate chemistries and increase application frequency. Resistant biotypes now challenge ALS inhibitors as well, making two- to four-way tank mixes the new norm. This resistance arms race elevates demand for novel modes of action and premium premixes that simplify stewardship. Chemical innovation pipelines regain urgency after a slow decade, while digital scouting tools gain traction to pinpoint outbreaks before they become unmanageable. The economic burden of higher herbicide costs per acre and potential yield loss keeps growers willing to pay for solutions that restore control, giving innovators a clear revenue runway in the near term.

Stringent Pesticide Bans and MRL Tightening (European Union focus)

European authorities continue to review active ingredients, with 15 key chemistries set to lose renewal in 2024, while maximum residue limits are being steadily lowered. Export-oriented producers in South America and Africa now face compliance costs to meet EU tolerances, even when selling to other destinations, because global grain buyers conform to the strictest standards. Smaller manufacturers struggle to finance new data packages, accelerating market share gains for top-tier firms that can invest in toxicology and environmental dossiers. Growers switch to newer, more expensive actives that carry lower residue profiles, lifting per-hectare spend but squeezing margins when commodity prices soften. Missing tools force some farmers to revert to older, more frequent applications, paradoxically increasing the overall chemical load despite the policy intent. Research priorities shift toward bio-based or low-residue molecules, lengthening development timelines and raising the bar for entry. The combined regulatory and commercial pressure subtracts 0.8 percentage points from the forecast CAGR, with the sharpest revenue impact projected to arrive before 2027 as grace periods expire. Companies with robust EU regulatory teams and pipeline actives positioned for fast approval gain a relative advantage under the new rules.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Precision-Ag Technologies

- Rapid Growth of Commercial Farming in Asia-Pacific and South America

- Fast Uptake of Biologicals Cannibalizing Synthetic Sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Herbicide captured a 42.35% market share of the crop protection chemicals market in 2025, representing the largest slice of the market size and generating the bulk of incremental revenue growth. Persistent resistance in Palmer amaranth and Conyza species necessitates multi-site programs, prompting growers to adopt stacked formulations that carry premium price points. Glyphosate still dominates the volume, but demand is increasingly shifting to HPPD inhibitors, PPO inhibitors, and new proprietary chemistries positioned for post-resistance control. The resulting mix upgrade underpins a robust 5.02% CAGR forecast to 2031.

Continued GM trait adoption, especially in Brazil and Argentina, sustains high herbicide intensity per hectare. Integrated seed-and-chemical offerings allow leading suppliers to bundle traits with tailored sprays, protecting both intellectual property and gross margins. Fungicides hold roughly significant share, supported by weather-linked disease flare-ups and the 2024 launch of Revysol in Brazil, which offers a new mode of action against soybean rust. Insecticides are seeing sporadic spikes when climate-driven pest incursions occur. Nematicides and molluscicides remain niche but essential for high-value horticulture, where even minor yield losses undermine profitability.

The Crop Protection Chemicals Market Report is Segmented by Function (Fungicide, Herbicide, Insecticide, Molluscicide, and More), Application Mode (Chemigation, Foliar, Seed Treatment, and More), Crop Type (Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, and More), and Geography (Africa, Europe, North America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

South America accounted for 41.85% of the crop protection chemicals market share in 2025, driven by Brazil's extensive soybean and corn production in the Cerrado savanna. Brazil alone consumed over 60% of the regional volume, supported by record pesticide purchases for consecutive planting cycles during the 2024 season. Argentina's export-focused farms contributed to growth, with genetically modified (GM) crop adoption surpassing 95% of national acreage, reinforcing herbicide-intensive farming practices. Favorable weather conditions and government policies prioritizing foreign exchange earnings have supported steady growth in South America, despite occasional logistical challenges at ports.

The Asia-Pacific region is the fastest-growing market, with a compound annual growth rate (CAGR) of 4.73% projected through 2031. Growth is driven by land consolidation and increased mechanization in countries such as India, China, and Southeast Asia. In India, commercial farming initiatives led to a 15% increase in chemical usage in 2024, as larger field sizes required season-long pest control programs. In China, environmental policies have prompted pesticide plant consolidation while encouraging the use of higher-efficacy, lower-residue chemicals that align with national food safety standards. Additionally, Indonesia, Thailand, and Vietnam have contributed to incremental demand through expanding palm oil and intensive rice farming systems, which rely on specialized fungicides and insecticides to protect crops in humid climates.

North America represents a significant portion of global consumption, supported by the adoption of precision agriculture, which now covers 35% of large farms and optimizes application timing. In the United States, high GM-crop acreage and increasing weed resistance have sustained per-acre herbicide expenditures, despite tight profit margins. Europe accounts for a substantial share of demand, but stringent regulations and residue limits have shifted investments toward low-dose chemistries and biological solutions. Despite these restrictions, the specialty fruit and vegetable segments maintain high market value. Africa remains the smallest regional market; however, commercial farming projects in South Africa and emerging hubs in West Africa are beginning to adopt modern crop protection programs, indicating a gradual increase in long-term demand.

- BASF SE

- Bayer AG

- Corteva Inc.

- FMC Corporation

- Jiangsu Yangnong Chemical Group Co., Ltd.

- Nufarm Limited

- Sumitomo Chemical Co., Ltd.

- Syngenta Group Co., Ltd.

- UPL Ltd.

- Lallemand Inc. (Animal Nutrition)

- EW Nutrition GmbH

- Kemin Industries Inc.

- Novus International Inc.

- Vitafor N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 Report Offers

3 Executive Summary and Key Findings

4 Key Industry Trends

- 4.1 Consumption of Pesticide per Hectare

- 4.2 Pricing Analysis for Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 GM-crop acreage expansion

- 4.5.2 Rising herbicide-resistant weeds

- 4.5.3 Adoption of precision-ag technologies

- 4.5.4 Rapid growth of commercial farming in Asia-Pacific and South America

- 4.5.5 Regenerative agriculture favoring selective chemistries

- 4.5.6 Climate-driven pest migration into temperate zones

- 4.6 Market Restraints

- 4.6.1 Stringent pesticide bans and MRL tightening (European Union focus)

- 4.6.2 Accelerating weed resistance to glyphosate and ALS inhibitors

- 4.6.3 Volatile Chinese technical-grade supply chain

- 4.6.4 Fast uptake of biologicals cannibalizing synthetic sales

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits and Vegetables

- 5.3.3 Grains and Cereals

- 5.3.4 Pulses and Oilseeds

- 5.3.5 Turf and Ornamental

- 5.4 Geography

- 5.4.1 Africa

- 5.4.1.1 South Africa

- 5.4.1.2 Rest of Africa

- 5.4.2 Asia-Pacific

- 5.4.2.1 Australia

- 5.4.2.2 China

- 5.4.2.3 India

- 5.4.2.4 Indonesia

- 5.4.2.5 Japan

- 5.4.2.6 Myanmar

- 5.4.2.7 Pakistan

- 5.4.2.8 Philippines

- 5.4.2.9 Thailand

- 5.4.2.10 Vietnam

- 5.4.2.11 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 France

- 5.4.3.2 Germany

- 5.4.3.3 Italy

- 5.4.3.4 Netherlands

- 5.4.3.5 Russia

- 5.4.3.6 Spain

- 5.4.3.7 Ukraine

- 5.4.3.8 United Kingdom

- 5.4.3.9 Rest of Europe

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Chile

- 5.4.5.4 Rest of South America

- 5.4.1 Africa

6 Competitive Landscape

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Inc.

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Group Co., Ltd.

- 6.4.6 Nufarm Limited

- 6.4.7 Sumitomo Chemical Co., Ltd.

- 6.4.8 Syngenta Group Co., Ltd.

- 6.4.9 UPL Ltd.

- 6.4.10 Lallemand Inc. (Animal Nutrition)

- 6.4.11 EW Nutrition GmbH

- 6.4.12 Kemin Industries Inc.

- 6.4.13 Novus International Inc.

- 6.4.14 Vitafor N.V.