|

시장보고서

상품코드

1906960

인도의 에스테틱 기기 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Aesthetic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

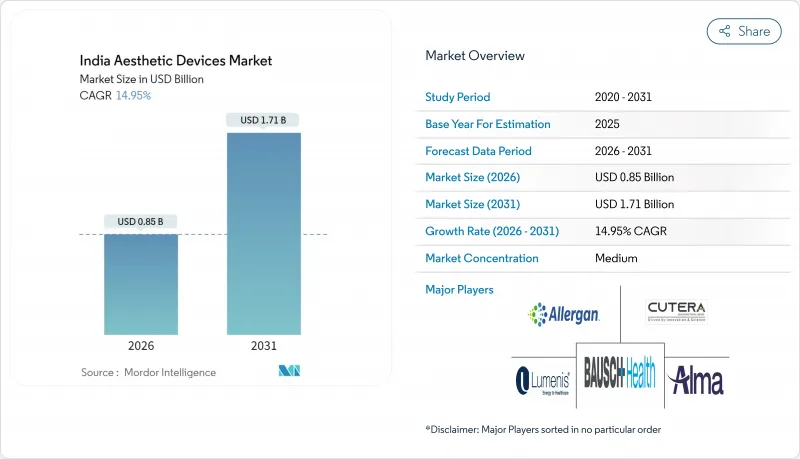

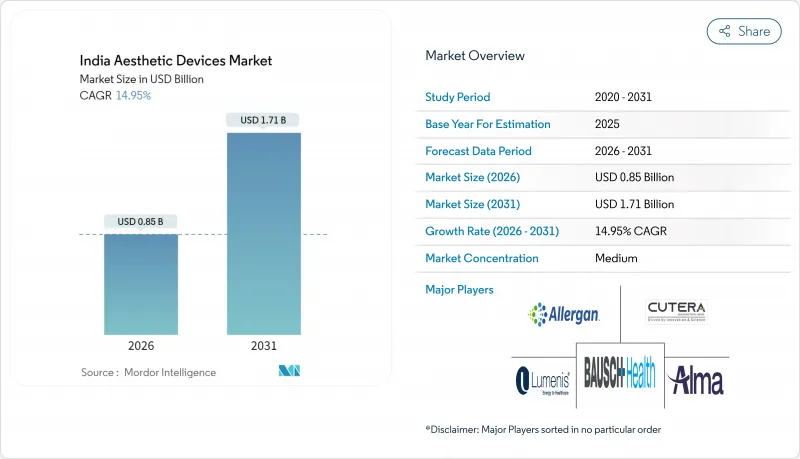

인도의 에스테틱 기기 시장은 2025년 7억 4,000만 달러에서 2026년에는 8억 5,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 14.95%를 나타낼 전망입니다. 2031년까지 17억 1,000만 달러에 이를 것으로 예상됩니다.

수요 증가는 가처분 소득 상승, 의료 관광 유입, 수입 의존도 감소 및 국내 생산 촉진을 위한 정책 인센티브에 기인합니다. 에너지 기반 시스템이 시술실에서 주류를 차지하고, 클리닉에서는 치료 계획에 AI를 도입하고, 정부의 생산 보조금에 의해 제조 거점에 새로운 자본이 유입하고 있습니다. 대도시의 소비자가 조기 도입을 견인해 왔습니다만, 인지도 향상과 자금 조달 수단의 개선에 수반해, 지방 도시에서도 급속한 보급이 진행되고 있습니다. 장비 제조업체는 여러 양식을 통합한 맞춤형 플랫폼에서 기회를 발견하고 의료 제공업체는 소셜 미디어를 활용하여 남녀를 불문하고 미용 의료의 보급을 추진하고 있습니다. 세계 OEM과 인도의 위탁제조업체와의 제휴로 공급망이 단축되어 수입 의존형 유통에서 국내 생산을 결합한 모델로의 이행이 가속화되고 있습니다.

인도의 에스테틱 기기 시장 동향과 인사이트

미용 시술에 대한 인지도의 높아짐

도시의 소비자들은 미용 시술을 허영심이 아닌 일상적인 건강 관리로 파악하고 있으며, 이 인식의 변화는 유명인의 추천과 소셜 미디어의 정보에 의해 더욱 가속화되고 있습니다. 인도는 현재 코 성형술의 실시 건수로 세계 2위, 지방 흡인술에서는 3위를 차지하고 있으며, 클리닉의 풍부한 사례 경험이 추가 수용을 촉진하고 있습니다. 남성으로부터의 유방비대증 치료나 식모 수요가 증가해, 종래는 여성 고객 중심이었던 성별 구성이 확산을 보이고 있습니다. 지방 도시(티아 2 도시)에서는 상담 건수가 급증하고 있는 것, 인프라의 부족에 의해 대도시권 이외에서의 시술 건수는 여전히 제한되고 있습니다. 이에 대응해, 연수기관에서는 단기 집중 프로그램을 실시하고 있어, 이것이 소규모 도시 클러스터에 새로운 클리닉의 설립으로 이어지고 있습니다.

가처분 소득 증가 및 의료 관광

국내 구매력도 상승하고 고급 미용 분야에서는 보험 적용 외 시술에 대한 지불 의향이 높아지고 있습니다. 경쟁력 있는 가격 설정으로 미용시술은 구미 기준보다 60-80% 낮고, 이 가격 차이는 외국인 고객의 여행비를 상쇄하는 충분한 규모입니다. 2023년에는 수도권에서 1,851명의 외국인 장기 이식 환자가 치료를 받고 인도의 임상 능력의 높이가 평가되었습니다. 이 국내·국제의 이중 수요 구조가, 제공업체에 의한 선진적인 멀티 모달 플랫폼에 대한 투자를 촉진해, 시술 메뉴의 확충에 연결되고 있습니다.

미용시술·기기의 고비용

에너지 기반 시스템은 150만-500만 루피(1만 7,100-5만 7,000달러)로 고액이며, 신흥 도시권을 서비스 대상으로 하는 소규모 클리닉에는 과제가 있어 대도시권 밖에서의 기기 보급을 제한하고 있습니다. 보험이 미용 목적의 치료를 다루는 것은 드물며, 자기 부담 모델을 강요함으로써 중소득층의 예산을 압박하고 있습니다. 수입관세가 착륙비용을 끌어올리는 반면, 초기 생산연동형 장려책(PLI)의 성과에 따라 특정 RF 핸드피스의 가격차가 줄어들고 있습니다. 휴대용 장비는 일부 시술자가 시장 진입에 도움이 되지만, 출력과 듀티 사이클의 제약으로 인해 종종 초보적인 서비스로 제한됩니다. OEM이 제공하는 대출 플랜은 초기 부담을 경감합니다만, 신흥 지역에서 환자수가 두드러지면, 채산 라인 도달 시기를 늦추는 요인이 됩니다.

부문 분석

에너지 기반 기기는 2025년 시점에서 인도 에스테틱 기기 시장 규모의 47.44%를 차지했고, 2031년까지 연평균 복합 성장률(CAGR) 17.65%로 성장하는 고주파 시스템이 주도권을 유지합니다. 레이저 플랫폼은 탈모 메뉴와 고에너지 염료 제거의 기반이 되고 있으며, 초음파 시스템은 복부 치료에서 비수술적 지방분해로 수요를 확대하고 있습니다. 고주파와 펄스광, 또는 HIFEM을 조합한 멀티모드 콘솔은 복수의 적응증에 대응하는 단일 헤드 유닛을 요구하는 클리닉을 매료시켜, 컴팩트한 시술실내의 설치 면적을 삭감합니다.

인도 제조업체는 현지 인체공학을 기반으로 한 크기의 핸드피스를 공동 설계하고 수입 광학 부품을 국내 조달 파이버 번들로 대체함으로써 부품 원가를 30-40% 삭감하고 있습니다. AI 대시보드는 임피던스 곡선과 피부 온도 데이터를 시각화하여 인도에서 일반적인 피츠패트릭 IV-V형 피부질을 위해 시술자가 조사 시간을 미세 조정할 수 있도록 유도합니다. 일회용 칩의 수익은 OEM 제조업체에 지속적인 수입원을 가져오고 예지 보전 경고는 예정되지 않은 다운 타임을 줄였습니다. 이를 통해 주요 공급업체는 장비 가동률 계약 보증을 96% 이상으로 향상시킵니다. 클리닉에서는 환자 수가 급증하는 제사 시즌에 맞추어 다운타임 제로의 프랙셔널 리서피싱 시술을 팔고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미용시술에 관한 인지도의 향상

- 가처분 소득 증가와 의료 관광

- 급속한 기술 진보

- 고령화 사회와 안티 에이징에 대한 관심 증가

- 정부의 생산 연동형 보조금 제도(PLI)가 국내 제조를 촉진

- AI를 활용한 맞춤형 치료 프로토콜

- 시장 성장 억제요인

- 미용시술·기기의 고비용

- 사회적 편견과 윤리적 우려

- CDSCO 분류하에 있어서 규제상의 모호성

- 주요 도시 이외의 지역에서의 훈련을 받은 시술자의 부족

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액 : 달러)

- 기기 유형별

- 에너지 기반 미용 기기

- 레이저 기반 미용 기기

- 고주파 기반 미용 기기

- 광 기반 미용 기기

- 초음파 미용 기기

- 기타 에너지 기반 미용 기기

- 비에너지 기반 미용기기

- 보툴리눔툭신(보톡스)

- 피부 필러 및 실

- 미세 박피술

- 임플란트

- 기타 비에너지 기반 미용기기

- 에너지 기반 미용 기기

- 용도별

- 피부 재생 및 탄력 개선

- 체형 교정 및 셀룰라이트 감소

- 안면 미용 시술

- 제모

- 유방 확대술

- 기타 용도

- 최종 사용자별

- 병원

- 클리닉 및 미용 센터

- 재택 케어 환경

- 지역별

- 북인도

- 서인도

- 남인도

- 동인도

- 중부 인도

- 북동부 인도

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Allergan Aesthetics(AbbVie Inc.)

- Alma Lasers (Sisram Medical)

- Bausch Health(Solta Medical)

- BTL Aesthetics

- Cutera Inc.

- Zimmer Biomet

- Lumenis Ltd.

- Venus Concept India

- 7e Wellness

- Cynosure(Hologic Inc.)

- Candela Medical

- InMode Ltd.

- Merz Pharma GmbH & Co. KGaA

- Fotona doo

- Syneron Medical Ltd.

- Lutronic Corporation

- Stryker Corporation

- Iridex Corp.

- Invasix Aesthetic Solutions

- Quanta System SpA

제7장 시장 기회와 향후 전망

KTH 26.01.20The India Aesthetic Devices Market is expected to grow from USD 0.74 billion in 2025 to USD 0.85 billion in 2026 and is forecast to reach USD 1.71 billion by 2031 at 14.95% CAGR over 2026-2031.

Strong demand stems from rising disposable incomes, medical-tourism inflows, and policy incentives that cut import reliance and boost local output. Energy-based systems dominate procedure rooms, clinics adopt AI for treatment planning, and government production subsidies attract fresh capital into manufacturing hubs. Metro consumers drive early adoption, but tier-2 cities now show rapid uptake as awareness grows and financing options improve. Device makers see opportunity in customizable platforms that bundle multiple modalities, while providers leverage social media to normalize aesthetic care among men and women alike. Partnerships between global OEMs and Indian contract manufacturers shorten supply chains, reinforcing a shift from import-heavy distribution to mixed domestic production models.

India Aesthetic Devices Market Trends and Insights

Increasing Awareness Regarding Aesthetic Procedures

Urban consumers view cosmetic enhancement as routine wellness rather than vanity, a perception shift amplified by celebrity endorsements and social-media narratives. India now ranks second in rhinoplasty volume and third in liposuction counts worldwide, giving clinics deeper case experience that feeds further acceptance. Male demand grows for gynecomastia correction and hair restoration, broadening the gender mix once skewed toward female clientele. Consultation numbers surge in tier-2 cities yet infrastructure gaps still limit procedural throughput outside metros. Training institutes respond by running short intensive programs, which in turn seed new clinics in smaller urban clusters.

Rising Disposable Income & Medical Tourism

Domestic purchasing power also rises, with the luxury beauty segment signaling readiness to pay for non-reimbursed procedures. Competitive pack ages price aesthetic treatments 60-80% below Western benchmarks, a gap large enough to offset travel costs for foreign clients. The National Capital Region treated 1,851 foreign organ-transplant patients in 2023, underscoring India's perceived clinical competence. This dual domestic-international demand profile encourages providers to invest in advanced multimodal platforms that broaden menu offerings.

High Cost of Aesthetic Procedures & Devices

Energy-based systems priced between INR 15-50 lakh (USD 17.1 to 57 thousands) challenge smaller clinics that serve emerging-city catchments, limiting device penetration outside metros. Insurance rarely pays for cosmetic indications, forcing self-pay models that strain middle-income budgets. Import duties inflate landed costs, though early PLI outputs are starting to close the price gap on select RF handpieces. Portable units help some practitioners enter the market, yet power ratings and duty cycles of such devices often restrict them to entry-level services. Financing schemes bundled by OEMs relieve upfront burdens but extend break-even horizons if patient volumes plateau in nascent geographies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technological Advancements

- Government PLI Scheme Spurring Domestic Manufacturing

- Shortage of Trained Practitioners Beyond Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Energy-based equipment generated 47.44% of India aesthetic devices market size in 2025 and will stay in the lead as radiofrequency systems post an 17.65% CAGR to 2031. Laser platforms still anchor hair-removal menus and high-fluence pigment correction, while ultrasound systems gain appeal for non-surgical fat disruption in mid-section treatments. Multi-modal consoles that mate RF with pulsed light or HIFEM lure clinics seeking one head-unit for multiple indications, reducing real-estate footprints inside compact procedure rooms.

Indian manufacturers now co-design handpieces sized for local ergonomics, substituting imported optics with domestically sourced fiber bundles to hit 30-40% lower BOM costs. AI dashboards visualize impedance curves and skin-temperature data, guiding operators to micro-adjust dwell times for Fitzpatrick IV-V skin types common across India. Disposable tip revenues create annuity streams for OEMs, while predictive-maintenance alerts cut unscheduled downtime, boosting device uptime contractual guarantees above 96% for premier providers. Clinics market zero-downtime fractional resurfacing sessions framed around festival seasons when patient volumes spike.

The India Aesthetic Devices Market Report is Segmented by Type of Device (Energy-Based Aesthetic Device, Non-Energy-Based Aesthetic Device), Application (Skin Resurfacing & Tightening, Body Contouring & Cellulite Reduction, and More), End User (Hospitals, and More), and Region (North India, West India, South India, East India, Central India, North-East India). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Allergan Aesthetics (AbbVie Inc.)

- Alma Lasers (Sisram Medical)

- Bausch Health (Solta Medical)

- BTL

- Cutera

- Zimmer Biomet

- Lumenis

- Venus Concept

- 7e Wellness

- Cynosure (Hologic Inc.)

- Candela Medical

- InMode Ltd.

- Merz Pharma

- Fotona d.o.o.

- Candela Medical

- Lutronic

- Stryker

- Iridex Corp.

- Invasix Aesthetic Solutions

- Quanta System S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Awareness Regarding Aesthetic Procedures

- 4.2.2 Rising Disposable Income & Medical Tourism

- 4.2.3 Rapid Technological Advancements

- 4.2.4 Aging Population & Focus on Anti-Aging

- 4.2.5 Government PLI Scheme Spurring Domestic Manufacturing

- 4.2.6 AI-Driven Personalized Treatment Protocols

- 4.3 Market Restraints

- 4.3.1 High Cost of Aesthetic Procedures & Devices

- 4.3.2 Social Stigma & Ethical Concerns

- 4.3.3 Regulatory Ambiguity Under CDSCO Classifications

- 4.3.4 Shortage of Trained Practitioners Beyond Tier-1 Cities

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Type of Device

- 5.1.1 Energy-based Aesthetic Device

- 5.1.1.1 Laser-based Aesthetic Device

- 5.1.1.2 Radiofrequency-based Aesthetic Device

- 5.1.1.3 Light-based Aesthetic Device

- 5.1.1.4 Ultrasound Aesthetic Device

- 5.1.1.5 Other Energy-based Aesthetic Devices

- 5.1.2 Non-energy-based Aesthetic Device

- 5.1.2.1 Botulinum Toxin

- 5.1.2.2 Dermal Fillers & Threads

- 5.1.2.3 Microdermabrasion

- 5.1.2.4 Implants

- 5.1.2.5 Other Non-energy-based Aesthetic Devices

- 5.1.1 Energy-based Aesthetic Device

- 5.2 By Application

- 5.2.1 Skin Resurfacing & Tightening

- 5.2.2 Body Contouring & Cellulite Reduction

- 5.2.3 Facial Aesthetic Procedures

- 5.2.4 Hair Removal

- 5.2.5 Breast Augmentation

- 5.2.6 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics & Beauty Centers

- 5.3.3 Home Care Settings

- 5.4 By Region

- 5.4.1 North India

- 5.4.2 West India

- 5.4.3 South India

- 5.4.4 East India

- 5.4.5 Central India

- 5.4.6 North-East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Allergan Aesthetics (AbbVie Inc.)

- 6.3.2 Alma Lasers (Sisram Medical)

- 6.3.3 Bausch Health (Solta Medical)

- 6.3.4 BTL Aesthetics

- 6.3.5 Cutera Inc.

- 6.3.6 Zimmer Biomet

- 6.3.7 Lumenis Ltd.

- 6.3.8 Venus Concept India

- 6.3.9 7e Wellness

- 6.3.10 Cynosure (Hologic Inc.)

- 6.3.11 Candela Medical

- 6.3.12 InMode Ltd.

- 6.3.13 Merz Pharma GmbH & Co. KGaA

- 6.3.14 Fotona d.o.o.

- 6.3.15 Syneron Medical Ltd.

- 6.3.16 Lutronic Corporation

- 6.3.17 Stryker Corporation

- 6.3.18 Iridex Corp.

- 6.3.19 Invasix Aesthetic Solutions

- 6.3.20 Quanta System S.p.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment