|

시장보고서

상품코드

1906964

리드리스 심장 페이스메이커 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Leadless Cardiac Pacemaker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

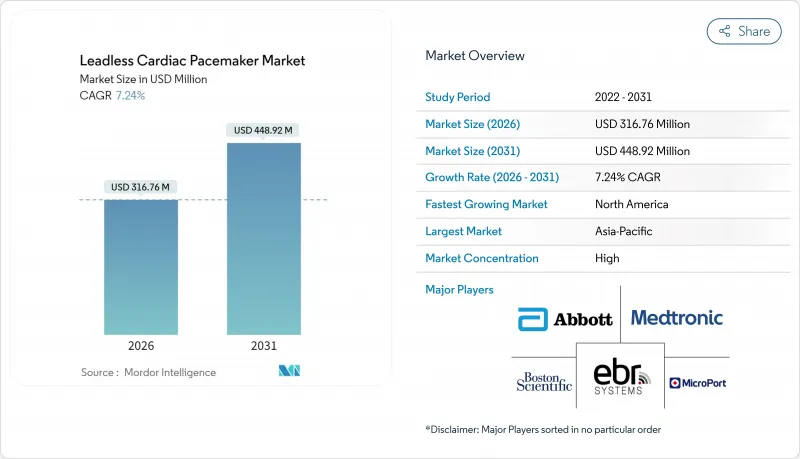

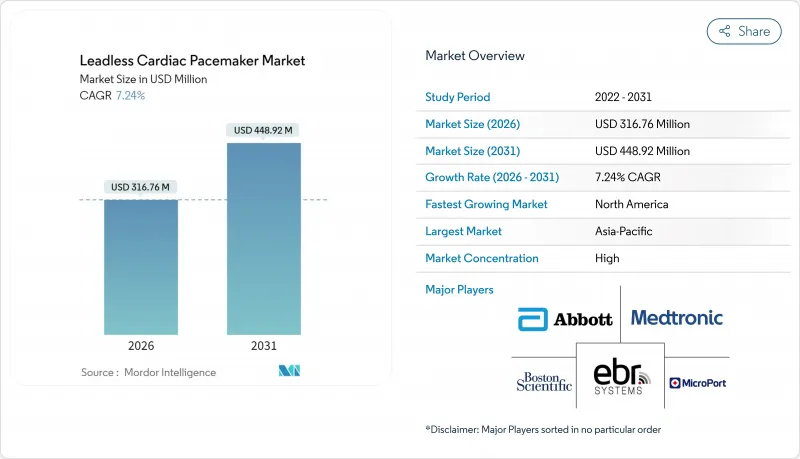

리드리스 심장 페이스메이커 시장은 2025년 2억 9,537만 달러로 평가되었고, 2026년에는 3억 1,676만 달러로 성장할 전망이며, 2026-2031년 CAGR 7.24%로 성장을 지속하여, 2031년까지 4억 4,892만 달러에 달할 것으로 예측되고 있습니다.

수요의 기세는 단실 심실 페이싱에서 2실 페이싱, 그리고 경정맥 리드를 사용하지 않고 생리적 동기화를 약속하는 전도계 솔루션으로의 급속한 전환에 의해 지원되고 있습니다. 북미에서 상환의 명확화, MRI 대응 표시 확대, 그리고 고령화가 진행되는 인구 동태가 판매량의 성장을 지지하고 있습니다. 애봇 및 메드트로닉은 차별화된 기술과 충실한 임상시험 파이프라인에 의해 확고한 지위를 지키고 있기 때문에 경쟁이 치열한 상황이지만, 보스턴 사이언티픽의 모듈형 플랫폼은 새로운 아키텍처가 기존 질서를 파괴할 수 있는 방법을 보여줍니다. 아시아태평양에서는 승인 절차의 효율성 및 병원 투자가 지속적인 가격 장벽을 상쇄하고 시장 기회가 확대되고 있습니다.

세계의 리드리스 심장 페이스메이커 시장 동향 및 인사이트

서맥성 부정맥 및 심혈관 질환의 유병률 증가

심혈관 질환 부담이 증가함에 따라 선진국에서는 연간 약 60만 명의 신규 페이스메이커 후보자가 발생하고 있으며, 노화에 따른 전도 장애로 인해 고령층의 디바이스 수요가 높아지고 있습니다. 리드리스 심장 페이스메이커는 기흉이나 포켓 감염의 리스크를 경감해, 영국의 3차 의료 센터에서 치료를 받은 허약한 환자에 있어서, 96.9%의 이식 성공률과 불과 4.5%의 합병증 발생률을 실현하고 있습니다. 임상 용도 범위는 TAVR 후의 전도 장애로도 확대되어 적응 대상층이 넓어지고 있습니다.

경정맥 리드에 비해 우수한 안전성 프로파일

레지스트리 데이터에 따르면, 미크라 이식 환자는 5년 경과 시점에 동등한 경정맥 리드 그룹에 비해 심각한 합병증이 63% 감소했습니다. 리드와 포켓의 폐지는 장치 감염의 주요 온상을 효과적으로 제거하며, 이점은 투석 환자 및 면역 결핍 환자에서 더욱 두드러집니다. 심막 천공 위험은 약 1.5%로 여전히 현저하지만, 술자의 숙련도가 향상되면 실제 임상 데이터는 기존 시스템과 동등한 안전성을 확인하고 있습니다.

비용에 민감한 지역에서 장비 가격 상승

정가는 경정맥 시스템(5,000달러 미만)에 비해 1만 5,000달러를 넘어 상환이 GDP 성장을 따라잡지 않는 지역에서는 도입이 제한됩니다. 경제 분석에서는, 호주에서 비용 효과의 역치는 QALY당 47,379호 달러로 산출되고 있으며, 성숙 시장에서는 허용 범위이지만, 신흥 지불자에게는 장벽이 됩니다. 저자원 환경에서는 전문적인 교육 및 영상 진단의 추가 비용이 총 절차 비용을 더욱 높일 수 있습니다.

부문 분석

2025년의 데이터에 따르면, 단실 시스템의 리드리스 심장 페이스메이커 시장 규모는 96.88%의 점유율을 차지했습니다만, 애봇사의 AVEIR DR이 시험으로 98.1%의 방실 동기율을 달성했기 때문에 2031년까지의 2실 디바이스의 CAGR은 7.82%의 전망이 되고 있습니다. 단실 모델은 지속적인 심방 세동 및 종말 시나리오에서 임상적으로 여전히 필수적입니다.

지속적인 소형화 및 임플란트 간의 통신으로 이강 플랫폼은 표준 치료로 추진되어 고가의 구성으로 수익 구성의 비율이 증가하고 있습니다. 제조업체는 또한 경정맥 리드를 사용하지 않고 생생한 번들을 활성화시키는 전도계 페이싱 캡슐도 연구하고 있으며, 이 기술은 우심실 중격 페이싱과 관련된 심부전으로 인한 입원이 감소할 것으로 예측됩니다. 특허 동향을 보면 무선 에너지 전송 및 회수 도구에 대한 25건 이상의 유효한 출원이 있으며 지속적인 연구개발 투자가 강조되고 있습니다.

지역별 분석

북미는 2025년 41.88%의 점유율로 선두를 유지했습니다. 메디케어 커버리지 위즈 에비던스 개발(MCD) 제도가 성과 데이터를 수집하면서 상환하는 강점 때문입니다. 병원 네트워크는 감염으로 인한 재입원 감소를 평가하는 가치 기반 의료 패키지에 리드리스 심장 페이스메이커를 통합합니다.

유럽에서는 CE 마크 취득의 근거 프로그램과 지역 횡단적인 레지스트리가 진료 가이드라인을 정교하게 하고 견조한 도입량을 유지하고 있습니다. 그러나 의료기기 규제(MDR)에 대응함으로써 인증 비용이 증가하고 있습니다. 아시아태평양은 8.74%라는 가장 빠른 CAGR을 기록했습니다. 인도는 2024년 AVEIR VR을 승인했으며, 중국의 주요 의료 센터에서는 국가 보험 약품 목록에 신청을 지원하기 위해 현지 임상시험을 확대 중입니다. 중산계급의 보험 가입률 향상과 인프라 정비의 진전에 의해 시술 건수는 증가 경향에 있습니다. 그러나 비용 효과적인 문제는 여전히 남아 있습니다.

라틴아메리카, 중동 및 아프리카는 민간 보험의 보급률과 공공 입찰 사이클이 보급 속도를 늦출 기회가 있는 시장으로 남아 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 서맥성 부정맥 및 심혈관 질환(CVD)의 유병률 상승

- 경정맥 리드에 비해 우수한 안전성 프로파일

- 급속히 고령화하는 세계 인구

- MRI 대응 승인의 확대에 의해 대상 환자층 확대

- 카테터 기반 소형화 기술에 의한 비수술실에서의 이식 실현

- 당일치기 수술에 있어서의 새로운 상환 모델

- 시장 성장 억제요인

- 비용에 민감한 지역의 디바이스 가격 상승

- 한정적인 제거 프로토콜 및 배터리 수명 불확실성

- 전지 불필요의 생체 흡수성 기술에 의한 경쟁 위협

- 신흥 시장에서의 전기 생리학 전문의의 육성 부족

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 경쟁 기업간 경쟁 관계

- 공급자의 협상력

- 구매자의 협상력

- 대체품의 위협

- 신규 참가업체의 위협

제5장 시장 규모 및 성장 예측

- 제품 유형별(금액, 백만 달러)

- 단실형 리드리스 심장 페이스메이커

- 듀얼 챔버 및 리드리스 심장 페이스메이커

- 적응증별(금액, 백만 달러)

- 서맥성 부정맥

- 방실 블록

- 심방세동

- 기타

- 최종 사용자별(금액, 백만 달러)

- 병원

- 심장센터

- 외래수술센터(ASC)

- 지역별(금액, 백만 달러)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- BIOTRONIK SE & Co. KG

- Boston Scientific Corporation

- EBR Systems, Inc.

- Lepu Medical Technology(Beijing) Co., Ltd.

- Medtronic plc

- MicroPort Scientific Corporation

제7장 시장 기회 및 장래 전망

AJY 26.01.26The leadless pacemaker market is expected to grow from USD 295.37 million in 2025 to USD 316.76 million in 2026 and is forecast to reach USD 448.92 million by 2031 at 7.24% CAGR over 2026-2031.

Demand momentum rests on the rapid shift from single-chamber ventricular pacing toward dual-chamber and forthcoming conduction-system solutions that promise physiologic synchrony without transvenous leads. North American reimbursement clarity, expanding MRI-conditional labeling, and aging demographics continue to anchor volume growth. Competitive intensity is high because Abbott and Medtronic defend entrenched positions through differentiated technology and deep clinical trial pipelines, yet Boston Scientific's modular platform illustrates how new architectures can disrupt the established order. Market opportunities widen in Asia-Pacific where streamlined approvals and hospital investments offset persistent pricing barriers.

Global Leadless Cardiac Pacemaker Market Trends and Insights

Rising Prevalence of Bradyarrhythmias & CVD

Increasing cardiovascular disease burden results in some 600,000 new pacing candidates annually across developed economies, and age-related conduction deficits intensify device demand in older cohorts. Leadless pacing reduces pneumothorax and pocket infection risks, enabling 96.9% implant success and only 4.5% complications in frail patients treated at U.K. tertiary centers. Clinical applicability also extends to conduction disturbances post-TAVR, broadening the eligible base.

Superior Safety Profile Versus Transvenous Leads

Registry evidence shows Micra recipients experienced 63% fewer major complications than comparable transvenous cohorts at five years. The abolition of leads and pockets effectively removes the principal nidus for device infection, an advantage magnified in dialysis and immunocompromised populations. Cardiac perforation risk remains salient at roughly 1.5% of cases, yet real-world data confirm overall safety parity with conventional systems once operator proficiency matures.

Elevated Device Price in Cost-Sensitive Regions

List prices surpass USD 15,000 against transvenous systems below USD 5,000, constraining uptake where reimbursement lags GDP growth. Economic analyses place cost-effectiveness thresholds at AUD 47,379 per QALY in Australia, an acceptable range for mature markets but a hurdle for emerging payers. Specialized training and imaging overhead further inflate total procedural cost in low-resource settings.

Other drivers and restraints analyzed in the detailed report include:

- Rapidly Aging Global Population

- MRI-Conditional Approvals Widening Eligible Cohort

- Limited Extraction Protocols & Battery Life Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

2025 data show the leadless pacemaker market size for single-chamber systems at 96.88% share, yet dual-chamber devices exhibit an 7.82% CAGR outlook through 2031 as Abbott's AVEIR DR secures 98.1% atrioventricular synchrony in trials. Single-chamber models remain clinically indispensable for permanent atrial fibrillation and end-of-life scenarios where procedural simplicity overrides physiologic pacing benefits.

Continued miniaturization and implant-to-implant communication propel dual-chamber platforms toward standard of care, elevating revenue mix toward premium-priced configurations. Manufacturers also explore conduction-system pacing capsules that deliver native bundle activation without transvenous leads, a step anticipated to compress heart-failure admissions linked with RV septal pacing. Patent landscaping indicates more than 25 active filings covering wireless energy transfer and retrieval tooling, underscoring sustained R&D investment.

The Leadless Pacemaker Market Report is Segmented by Product Type (Single-Chamber Ventricular Leadless Pacemaker, Dual-Chamber Leadless Pacemaker), Indication (Bradyarrhythmia, Atrioventricular Block, Atrial Fibrillation, Others), End User (Hospitals, Cardiac Centres, Ambulatory Surgical Centres), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 41.88% share in 2025 on the strength of Medicare Coverage with Evidence Development that reimburses while capturing outcomes data. Hospital networks integrate leadless pacemakers into value-based bundles that reward reduced infection readmissions.

Europe sustains robust volume through CE-marked evidence programs and pan-regional registries that refine practice guidelines, although MDR compliance adds incremental certification cost. Asia-Pacific posts the fastest 8.74% CAGR as India cleared AVEIR VR in 2024 and major Chinese centers ramp local clinical trials to support National Reimbursement Drug List petitions. Rising middle-class coverage and infrastructure builds accelerate procedure counts despite lingering affordability challenges.

Latin America and Middle East & Africa remain opportunity pockets where private insurance penetration and public tender cycles dictate slower diffusion trajectories.

- Abbott Laboratories

- BIOTRONIK

- Boston Scientific

- EBR Systems, Inc.

- Lepu Medical Technology (Beijing) Co., Ltd.

- Medtronic

- MicroPort

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of bradyarrhythmias & CVD

- 4.2.2 Superior safety profile versus trans-venous leads

- 4.2.3 Rapidly ageing global population

- 4.2.4 MRI-conditional approvals widening eligible cohort

- 4.2.5 Catheter-based miniaturisation enabling non-OR implants

- 4.2.6 Emerging reimbursement models for day-case procedures

- 4.3 Market Restraints

- 4.3.1 Elevated device price in cost-sensitive regions

- 4.3.2 Limited extraction protocols & battery life uncertainty

- 4.3.3 Competitive threat from battery-less bio-resorbable tech

- 4.3.4 Electrophysiologist training gap in developing markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Supplier Power

- 4.7.3 Buyer Power

- 4.7.4 Threat of Substitutes

- 4.7.5 Threat of New Entrants

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value, USD million)

- 5.1.1 Single-Chamber Ventricular Leadless Pacemaker

- 5.1.2 Dual-Chamber Leadless Pacemaker

- 5.2 By Indication (Value, USD million)

- 5.2.1 Bradyarrhythmia

- 5.2.2 Atrioventricular Block

- 5.2.3 Atrial Fibrillation

- 5.2.4 Others

- 5.3 By End User (Value, USD million)

- 5.3.1 Hospitals

- 5.3.2 Cardiac Centres

- 5.3.3 Ambulatory Surgical Centres

- 5.4 By Geography (Value, USD million)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 BIOTRONIK SE & Co. KG

- 6.3.3 Boston Scientific Corporation

- 6.3.4 EBR Systems, Inc.

- 6.3.5 Lepu Medical Technology (Beijing) Co., Ltd.

- 6.3.6 Medtronic plc

- 6.3.7 MicroPort Scientific Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment