|

시장보고서

상품코드

1907209

유럽의 난연 화학물질 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe Flame Retardant Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

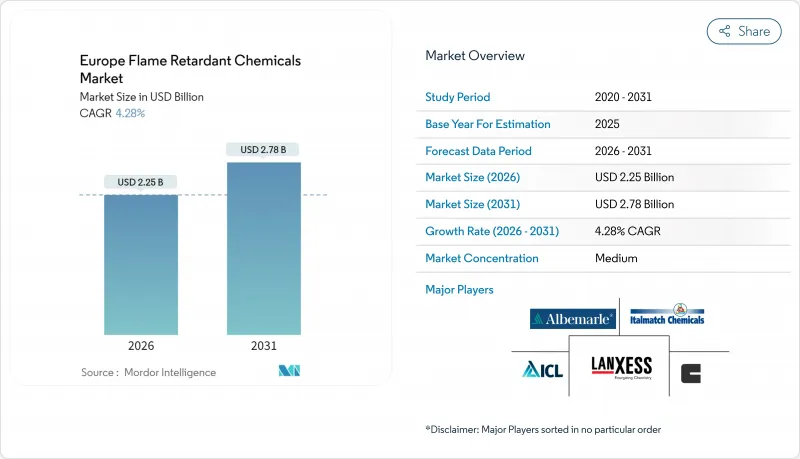

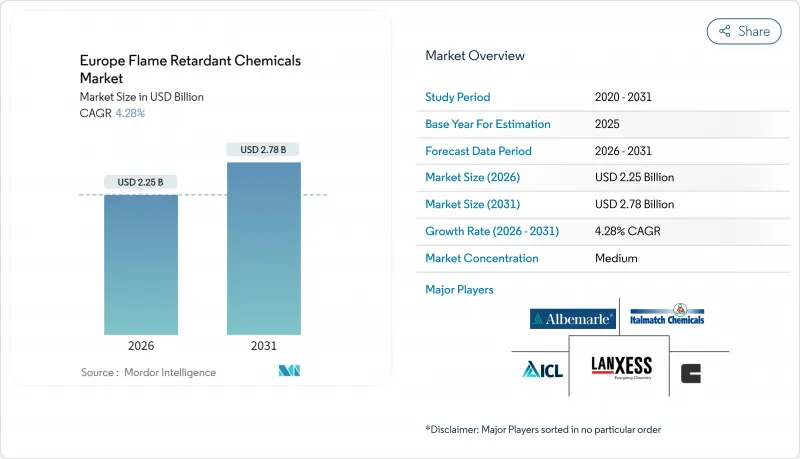

유럽의 난연 화학물질 시장 규모는 2026년에 22억 5,000만 달러로 추정되고 있습니다. 2025년 21억 6,000만 달러에서 성장하여 2031년에는 27억 8,000만 달러에 이를 것으로 전망되며, 2026-2031년 CAGR 4.28%로 성장이 확대될 것으로 예측됩니다.

REACH 규정 준수, 브롬계 시스템의 가속 대체, 지속적인 인프라 투자로 인해 이 지역은 비할로겐 첨가제의 신뢰할 수 있는 수요 기지가 되었습니다. 외벽재, 단열재, 구조용 강재에 대한 방화 안전 기준의 강화에 의해 건설 분야가 소비량의 주도역을 담당하고 있습니다. 반도체 자급률 향상책과 5G 전개에 의해 활성화된 전자기기 생산이 제2 성장 엔진이 되어 중동 유럽의 자동차 경량화 및 가구 제조가 다운스트림 고객 기반을 확대하고 있습니다. 생산자가 EU의 향후 지속가능성 목표를 충족하는 PFAS 프리로 순환형 경제 대응의 그레이드를 겨루고 투입하는 중, 경쟁의 격화가 진행되고 있습니다. 알루미늄, 인, 마그네슘 시장의 원재료 가격 변동은 여전히 주요 위험 요인이지만 공급업체의 다양화 전략과 재고 버퍼의 강화로 인해 공급 측의 변동성이 부분적으로 완화되고 있습니다.

유럽의 난연 화학물질 시장 동향 및 분석

소비자용 전기및 전자기기 제조 증가

유럽의 전자기기 제조업체는 공급 라인을 단축하고 EU 칩스 법에 따른 리쇼어링 계획을 강화하고 있습니다. 난연 화학물질 선택은 배터리 하우징 및 5G 무선 장치용 무할로겐 규제에 의해 규정됩니다. LANXESS사가 최근 도입한 폴리아미드 6등급은 1.5mm 두께로 UL 94 V-0 규격을 달성하고 있어 자동차 제조업체가 안전성을 손상시키지 않고 두꺼운 배터리 커버를 통합하는데 기여하고 있습니다. USB-C 케이블용 배합 제조업체는 현재 데이터센터 및 충전 인프라의 요구 사항인 저연제로 할로겐 기준도 충족하는 무할로겐 TPE 블렌드를 채용하고 있습니다. EU가 지역 내 규격 폴리머 조달을 선호하는 반도체 팹에 보조금을 제공하는 것도 수요의 힘을 뒷받침하고 있습니다.

건축 분야의 방화 규제 강화

EN 13501-1 규격의 2024년 개정판 및 목질 외장재에 관한 각국 규제에 의해 저층 주택 외관에는 클래스 D-s3, d1이 의무화되고, 고층 건축물에는 종래대로 B-s3, d1이 유지되었습니다. 이에 따라 팽창성 도료나 수산화알루미늄 충전재의 채용이 촉진되고 있습니다. 독일의 DIBt(건축기술연구소)는 불연성 보드 및 페인트 강판 시스템의 허가 목록을 확충하여 제조업체에게 명확한 인증 취득 경로를 제공했습니다. EU 그린딜을 기반으로 한 프로젝트는 난연성과 탄소 배출량 감소를 양립하는 인계 팽창 시스템을 지정합니다. 신규 주택 및 개수 공사는 보다 높은 기준을 충족할 필요가 있어, 법적 틀에 의해 장기적인 소비 확대가 확실시됩니다.

브롬계 난연 화학물질에 대한 독성 우려

유럽 화학물질청(ECHA)은 2025년 4월 보고서에서 여러 방향족 브롬화 화합물에 대한 허가 요건의 가능성을 시사하고 시장에서 이 화학물질에 대한 기피감을 강화하고 있습니다. 북유럽 각료이사회는 2030년까지 완전 폐지를 계속해서 요구하고 있으며 수요를 더욱 감퇴시키고 있습니다. 브롬계 시스템은 얇은 전자 기기에 뛰어나지만, 대체 압력에 의해 OEM 제조업체는 케이스 형상의 재설계나, 린 질소의 이중 시너지 효과 시스템에 대한 이행을 강요당하고 있습니다. 컴플라이언스 비용 및 잠재적 진부화는 새로운 브롬계 생산 능력에 대한 투자 의욕을 낮추고 향후 판매 감소로 이어질 것입니다.

부문 분석

유럽의 난연 화학물질 시장에서 비할로겐계 시스템의 점유율은 88.83%를 차지하고 있습니다. 건설 및 전자기기 분야에 있어서 REACH 규제 대응을 간소화하는 인계, 무기계 및 질소계 화학물질의 채용 확대에 의해 2031년까지 연평균 복합 성장률(CAGR) 5.52%로 성장이 계속될 전망입니다. 수산화알루미늄은 연기 억제 작용에 의해 벽판 및 전선 케이블 분야에서 최대 점유율을 유지, 수산화마그네슘은 고온 용도로 진출 중입니다. 인계 첨가제는 전기자동차 배터리 케이스에 필수적인 얇은 두께 효율을 실현합니다.

혁신 활동은 폴리우레탄 및 에폭사이드 네트워크에 중합하는 반응성 인 올리고머를 중심으로 전개되어 재활용시의 이행을 방지합니다. 특수화학 분야의 신규 진출기업은 금속 포스피네이트계 첨가제의 시너지 효과를 활용하여 첨가량을 줄이면서 재료의 기계적 특성을 유지합니다. 자사 생산의 인계 제조업체가 고순도 유도체에 수직 통합함으로써 비용 경쟁력이 향상되어 가격 급등의 완화를 도모할 수 있습니다. 재생 원료 등급에 대한 액세스는 여전히 병목 현상이지만 독일에서의 파일럿 시험에서는 회수 폴리카보네이트에 인산 에스테르를 25% 봉입한 혼합물의 도입에 성공하여 UL-94 V-0 규격을 손상시키지 않고 실현하고 있습니다.

유럽의 난연 화학물질 화학 보고서는 제품 유형별(비할로겐계, 할로겐계), 최종 사용자 산업별(전기전자, 건축 건설, 수송, 섬유 가구), 지역별(독일, 영국, 이탈리아, 프랑스, 스페인, 기타 유럽)로 분류되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 소비자용 전기 및 전자 기기 제조 증가

- 건설 분야에서의 방화 안전 규제의 강화

- 중동 유럽에서의 가구 및 실내 장식품 생산의 성장

- 순환형 경제에 적합한 난연 화학물질 첨가제로의 이행

- 5G 케이블 및 데이터센터 설치의 급증

- 시장 성장 억제요인

- 브롬계 난연 화학물질의 독성에 관한 우려

- 원재료 가격의 변동성(알루미늄, 인, 마그네슘 광석)

- EU에서 폴리머 사용을 제한하는 마이크로 플라스틱 규제의 시행 대기

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 비할로겐계

- 무기계

- 수산화알루미늄

- 수산화마그네슘

- 붕소 화합물

- 인계

- 질소계

- 기타

- 무기계

- 할로겐화

- 브롬계 화합물

- 염소계 화합물

- 비할로겐계

- 최종 사용자 업계별

- 전기 및 전자 기기

- 건축 및 건설

- 교통기관

- 섬유 및 가구

- 지역별

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant

- DIC Corporation

- Dow

- Eti Maden

- ICL

- Italmatch Chemicals SpA

- JM Huber Corp.(Huber Engineered Materials)

- LANXESS

- MPI Chemie BV

- Nabaltec AG

- RTP Company

- THOR Group

- TOR Minerals

제7장 시장 기회 및 장래 전망

AJY 26.01.26The Europe Flame Retardant Chemicals Market size in 2026 is estimated at USD 2.25 billion, growing from 2025 value of USD 2.16 billion with 2031 projections showing USD 2.78 billion, growing at 4.28% CAGR over 2026-2031.

Regulatory alignment with REACH, accelerated replacement of brominated systems, and sustained infrastructure investment make the region a dependable demand center for non-halogenated additives. Construction leads the volume offtake owing to tightened fire-safety rules for cladding, insulation, and structural steel. Electronics production, revitalized by semiconductor sovereignty initiatives and 5G rollouts, adds a second growth engine, while automotive lightweighting and furniture manufacturing in Central and Eastern Europe expand the downstream customer base. Competitive intensity is rising as producers race to launch PFAS-free, circular-economy-ready grades that satisfy upcoming EU sustainability targets. Raw-material price swings in aluminum, phosphorus, and magnesium markets remain the chief risk, yet supply-side volatility is partly cushioned by diversified sourcing strategies and higher inventory buffers.

Europe Flame Retardant Chemicals Market Trends and Insights

Rising Consumer Electrical and Electronics Manufacturing

European electronics producers have intensified reshoring programs that shorten supply lines and align with the EU Chips Act. Flame-retardant selection is governed by halogen-free mandates for battery housings and 5G radio units. Recent polyamide 6 grades introduced by LANXESS achieve UL 94 V-0 at 1.5 mm, helping automakers integrate thicker battery covers without sacrificing safety. Formulators targeting USB-C cables now deploy halogen-free TPE blends that also meet low-smoke zero-halogen criteria, a requirement for data centers and charging infrastructure. Demand strength is reinforced by EU subsidies for local semiconductor fabs that prioritize in-region procurement of compliant polymers.

Stricter Fire-Safety Regulations in Construction

The 2024 update of EN 13501-1 and national rules for wood cladding imposed class D-s3,d1 for low-rise residential facades and maintained B-s3,d1 for taller buildings, spurring uptake of intumescent coatings and aluminum hydroxide fillers. Germany's DIBt expanded its list of non-combustible boards and coated steel systems, giving manufacturers clear pathways for approval. Projects funded under the EU Green Deal specify phosphorus-based intumescent systems that provide both flame retardancy and embodied-carbon reductions. The legal framework locks in long-term consumption growth as new dwellings and retrofits must meet higher standards.

Toxicity Concerns Over Brominated FRs

ECHA signaled potential authorization requirements for several aromatic brominated compounds in its April 2025 report, intensifying market aversion toward this chemistry. The Nordic Council of Ministers continues to lobby for a complete phase-out by 2030, further dampening demand. While brominated systems excel in thin-wall electronics, substitution pressures compel OEMs to redesign housing geometries or shift to dual-synergy phosphorus-nitrogen systems. Compliance costs and potential obsolescence reduce investment appetite for new brominated capacity, lowering future sales.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Furniture and Upholstery Production in CEE

- Shift to Circular-Economy Compliant FR Additives

- Pending EU Microplastics Legislation Limiting Polymer Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Europe flame retardant chemicals market size for non-halogenated systems is equal to 88.83% share. Growth continues at 5.52% CAGR through 2031 as construction and electronics buyers adopt phosphorus, inorganic, and nitrogen chemistries that simplify REACH compliance. Aluminum hydroxide remains volume leader in wallboard and wire-cable owing to its smoke-suppressant action, while magnesium hydroxide penetrates higher-temperature applications. Phosphorus-based additives deliver thin-wall efficiency critical for electric vehicle battery enclosures.

Innovation activity clusters around reactive phosphorus oligomers that polymerize into polyurethane or epoxide networks, preventing migration during recycling. Market entrants from specialty chemicals leverage metal phosphinate-based synergies to lower loading levels, preserving material mechanics. Cost competitiveness improves as captive phosphorus producers forward-integrate into high-purity derivatives, smoothing price spikes. Access to recycled feedstock grades remains a bottleneck; however, pilot trials in Germany demonstrate successful incorporation of reclaimed polycarbonate blended with locked-in phosphorus esters at 25% levels without sacrificing UL-94 V-0 ratings.

The Europe Flame Retardant Chemicals Report is Segmented by Product Type (Non-Halogenated and Halogenated), End-User Industry (Electrical and Electronics, Buildings and Construction, Transportation, and Textiles and Furniture), and Geography (Germany, United Kingdom, Italy, France, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant

- DIC Corporation

- Dow

- Eti Maden

- ICL

- Italmatch Chemicals SpA

- J.M. Huber Corp. (Huber Engineered Materials)

- LANXESS

- MPI Chemie BV

- Nabaltec AG

- RTP Company

- THOR Group

- TOR Minerals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumer electrical and electronics manufacturing

- 4.2.2 Stricter fire-safety regulations in construction

- 4.2.3 Growth in furniture and upholstery production in CEE

- 4.2.4 Shift to circular-economy compliant FR additives

- 4.2.5 Surge in 5G cable and data-center installations

- 4.3 Market Restraints

- 4.3.1 Toxicity concerns over brominated FRs

- 4.3.2 Raw-material price volatility (Al, P, Mg ores)

- 4.3.3 Pending EU micro-plastics legislation limiting polymer uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Non-Halogenated

- 5.1.1.1 Inorganic

- 5.1.1.1.1 Aluminum Hydroxide

- 5.1.1.1.2 Magnesium Hydroxide

- 5.1.1.1.3 Boron Compounds

- 5.1.1.2 Phosphorus-based

- 5.1.1.3 Nitrogen-based

- 5.1.1.4 Others

- 5.1.1.1 Inorganic

- 5.1.2 Halogenated

- 5.1.2.1 Brominated Compounds

- 5.1.2.2 Chlorinated Compounds

- 5.1.1 Non-Halogenated

- 5.2 By End-user Industry

- 5.2.1 Electrical and Electronics

- 5.2.2 Buildings and Construction

- 5.2.3 Transportation

- 5.2.4 Textiles and Furniture

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Spain

- 5.3.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adeka Corporation

- 6.4.2 Albemarle Corporation

- 6.4.3 BASF

- 6.4.4 Clariant

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 Eti Maden

- 6.4.8 ICL

- 6.4.9 Italmatch Chemicals SpA

- 6.4.10 J.M. Huber Corp. (Huber Engineered Materials)

- 6.4.11 LANXESS

- 6.4.12 MPI Chemie BV

- 6.4.13 Nabaltec AG

- 6.4.14 RTP Company

- 6.4.15 THOR Group

- 6.4.16 TOR Minerals

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment