|

시장보고서

상품코드

1907214

유럽의 분자진단 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe Molecular Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

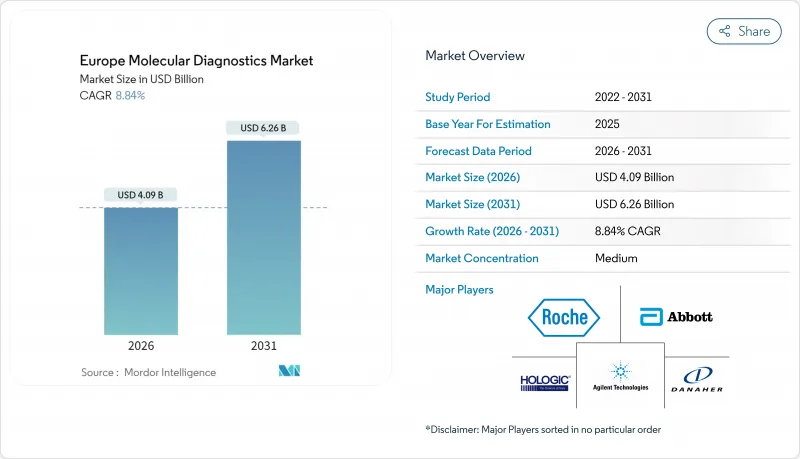

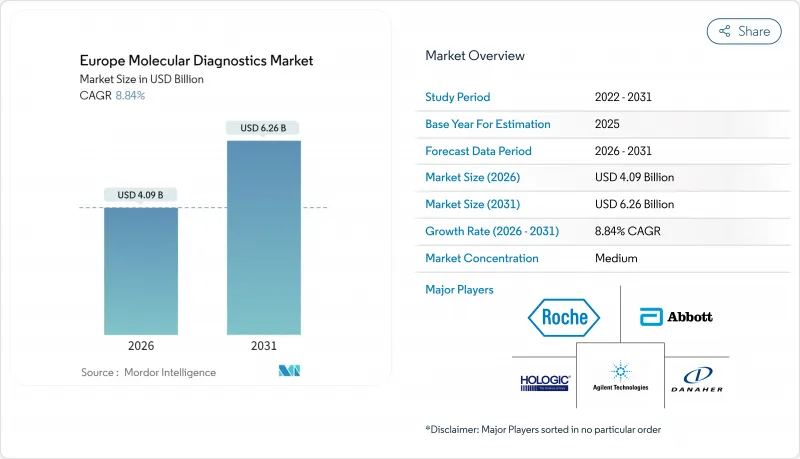

유럽의 분자진단 시장 규모는 2026년에 40억 9,000만 달러로 추정되고, 2025년 37억 6,000만 달러에서 성장이 예상됩니다. 2031년 62억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR) 8.84%로 확대될 전망입니다.

정밀의료 프로토콜 채용, 체외 진단용 의료기기 규칙(IVDR)의 완전 시행, 항균제 내성 감시에 대한 안정적인 자금 제공이 이 전망을 형성하고 있습니다. 포인트 오브 케어(POC) 플랫폼은 진단 결과의 보고 시간을 1시간 미만으로 단축하고, 차세대 시퀀싱(NGS)은 루틴 검사를 단일 유전자 PCR에서 종합적인 유전체 프로파일링으로 이동시키고 있습니다. NGS의 실행 비용은 현재 모든 엑솜당 500달러 이하로 되어 있으며, 중규모 연구소에서도 높은 처리량 시퀀싱을 도입할 수 있게 되었습니다. 프라이머 및 프로브 설계를 최적화하는 인공지능(AI) 엔진은 어세이 개발 사이클을 단축하고 독일, 네덜란드, 프랑스에서 벤처 자금을 불러옵니다. 이러한 요인들이 결합되어 유럽 분자진단 시장은 지역 전체의 병원 근대화 프로그램의 기초로서 그 중요성을 높이고 있습니다.

유럽의 분자진단 시장 동향 및 인사이트

포인트 오브 케어 분자 검사의 보급 확대

유럽의 병원에서는 현재, 카트리지식 PCR 장치나 등온 반응 장치를 구급 부문이나 외래에 배치해, 호흡기 병원체의 검사 결과 보고 시간을 24시간에서 45분으로 단축하고 있습니다. 독일의 3차 의료기관에서는 2024년까지 구급 부문의 60%가 패혈증 트리아지에 POC 분자 패널을 도입하는 것으로 보고되었습니다. 통합 분석기는 결과를 전자 의료 기록에 직접 업로드하므로 항균제 적정 사용 팀은 한 시프트 내에서 치료를 조정할 수 있습니다. 스칸디나비아의 1차 의료 클리닉은 인플루엔자, RSV, SARS-CoV-2를 위한 환자 근처 멀티플렉스 패널을 시험 도입하여 역학 모니터링을 강화하고 있습니다. 공급업체는 베드사이드 운영이 검증된 견고한 장비, 바코드 시약 추적 및 GDPR(EU 개인정보보호규정) 요구 사항을 충족하는 보안 클라우드 대시보드를 지원합니다.

차세대 시퀀싱(NGS) 및 약물 유전학 플랫폼의 진보

시퀀싱 소모품 가격은 2023-2025년 38% 하락했으며, 중규모 검사 기관에서도 500 유전자 종양 패널을 시료당 450유로(489달러) 이하로 제공할 수 있게 되었습니다. 액체 생검 검사는 영상 진단보다 몇 달 빨리 미세 잔류 병변을 검출하므로 침습적인 조직 채취 없이 치료 조정을 촉진합니다. 유럽의약청(EMA)은 현재 NGS를 필요로 하는 동반진단약을 28유형 등록하고 있으며, 이는 2022년의 배수입니다. 이것에 의해 검사 메뉴의 확충이 가속하고 있습니다. 프랑스 보험자는 CYP450 및 DPYD 패널의 비용을 상환하고 항우울제와 플루오로피리미딘의 안전성을 향상시키고 있습니다. 동유럽의 기준검사기관은 프랑크푸르트와 더블린에 호스팅된 클라우드 파이프라인에 바이오인포매틱스 업무를 외부 위탁하여 현지 기술 부족을 피하면서 데이터 거주 규칙을 충족하고 있습니다. 이러한 요인들이 결합되어 유럽의 분자진단 시장은 데이터가 풍부한 종양학 워크플로우로 추진되고 있습니다.

고급 검사 인프라의 필요성

고급 워크플로우에는 ISO 15189 인증, 바이오 세이프티 캐비닛 및 고정밀 열 순환기가 필요하지만, 이들은 서유럽 이외의 지역에서는 부족합니다. 2024년에는 임상 바이오인포마티션 수요가 공급을 40% 웃돌았으며 동유럽의 많은 연구소에서 검사 결과 보고 승인이 지연되었습니다. 지방부에서는 광대역 환경이 제한되어 있어 클라우드 파이프라인의 이용이 방해되고 있습니다. EU의 결속 기금이 설비 갱신을 자금 원조하고 있습니다만, 지출 사이클은 5년에 이릅니다. 이러한 인프라의 격차는 단기적인 보급을 억제하고 자원이 부족한 지역에서의 유럽 분자진단 시장의 발전을 둔화시키고 있습니다.

부문 분석

PCR 플랫폼은 2025년에 14억 7,000만 달러(유럽 분자진단 시장 규모의 39.12%)를 창출했습니다. 성숙한 워크플로우로 증후군별 호흡기 및 패혈증 패널은 qPCR을 기반으로 계속하고 있습니다. 시퀀싱은 9.45%의 연평균 복합 성장률(CAGR)로 모든 기술을 능가하고 종양학 및 감염증의 타이아웃을 포착하고 있습니다. 옥스포드 나노포어의 휴대형 시퀀서는 수막염 병원체를 45분 내에 확인하여 신속 PCR에 의한 일반 감염의 배제와 온디맨드 NGS에 의한 내성 프로파일의 명확화를 조합한 하이브리드 전략을 촉진하고 있습니다. 질량 분석법 및 마이크로어레이는 틈새 시장을 유지하고 있지만, AI를 활용한 시약 설계에 의해 플랫폼 경계가 점차 모호해지고, 유럽 분자진단 시장 전체에서 벤더 간의 경쟁이 격화하고 있습니다.

감염증 검사는 2025년에 17억 3,000만 달러(유럽 분자진단 시장 규모의 46.10%)를 창출했습니다. 멀티플렉스 패널은 검체당 20종 이상의 병원체를 검출할 수 있어 연속 검사를 삭감합니다. 모든 유전체 시퀀싱은 병원 내 아웃브레이크를 추적하고 감염 관리 대시보드에 정보를 제공합니다. 종양학 검사는 액체 생검 및 표적 요법 선택에 견인되어 CAGR 9.52%로 확대되고 있습니다. 약리 유전체학 패널은 정신의학과 심장병학에 진출하고 있지만, 남유럽에서는 지불자 지원이 늦어지고 있습니다. 신생아 스크리닝 프로그램의 확충은 유전성 질환 검사를 추진하는 한편, 항균제 내성 검사는 qPCR과 시퀀싱을 통합하여 감시 체제를 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 포인트 오브 케어(POC) 분자 검사의 보급 확대

- 차세대 시퀀싱(NGS) 및 약리 유전체학 플랫폼 진전

- EU 전역에 있어서 항균제 내성 감시 의무 급증

- IVDR에 기초한 CE-IVD 동반진단약 수요

- AI 지원형 프라이머 및 프로브 설계 스타트업의 성장

- 시장 성장 억제요인

- 고도로 복잡한 검사 인프라의 필요성

- EU27 국가에서의 지불자 간 상환 제도의 단편화

- 인정 분자 바이오인포마티션의 부족

- GDPR(EU 개인정보보호규정)과 관련된 국경을 넘은 검체 이전의 제한

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액 : 달러)

- 기술별

- 원위 하이브리드화

- 칩 및 마이크로어레이

- 질량 분석법(MS)

- 시퀀싱

- PCR

- 기타 기술

- 용도별

- 감염증 진단

- 종양학 및 액체 생검

- 약리 유전체학

- 유전성 질환 검사

- 미생물학 및 항균제 내성

- 기타 용도

- 제품별

- 기기 및 분석장치

- 시약 및 키트

- 소프트웨어 및 서비스

- 최종 사용자별

- 병원 및 병원 검사실

- 독립 검사 기관

- 포인트 오브 케어 및 니어 환자 환경

- 학술기관 및 연구기관

- 검체 유형별

- 혈액 및 혈장

- 조직 및 FFPE

- 타액 및 구강 내 스와브

- 소변 및 기타 체액

- 검사 환경별

- 중앙 검사실

- 분산형 및 POC 사이트

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Agilent Technologies

- Becton, Dickinson and Company

- bioMerieux SA

- Biocartis NV

- Cepheid(Danaher)

- Danaher Corporation(Beckman, Leica, Cepheid)

- Eurofins Scientific

- F. Hoffmann-La Roche Ltd

- GenMark Diagnostics

- Hologic Inc.

- Illumina Inc.

- Luminex(DiaSorin)

- Myriad Genetics

- Oxford Nanopore Technologies

- QIAGEN NV

- Seegene Inc.

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

- T2 Biosystems

제7장 시장 기회 및 장래 전망

AJY 26.01.26Europe molecular diagnostics market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.76 billion with 2031 projections showing USD 6.26 billion, growing at 8.84% CAGR over 2026-2031.

Adoption of precision-medicine protocols, full enforcement of the In Vitro Diagnostic Regulation (IVDR), and stable funding for antimicrobial-resistance surveillance shape this outlook. Point-of-care (POC) platforms reduce diagnostic turnaround to under an hour, while next-generation sequencing (NGS) moves routine testing from single-gene PCR toward comprehensive genomic profiling. NGS run costs, now below USD 500 per whole exome, make high-throughput sequencing affordable for mid-tier laboratories. Artificial-intelligence (AI) engines that optimize primer and probe design shorten assay-development cycles, attracting venture funding in Germany, the Netherlands, and France. Together, these factors reinforce the Europe molecular diagnostics market as a cornerstone of hospital modernization programs across the region.

Europe Molecular Diagnostics Market Trends and Insights

Rising Adoption of Point-of-Care Molecular Assays

Europe's hospitals now place cartridge-based PCR and isothermal devices in emergency and outpatient units, cutting respiratory-pathogen turnaround from 24 hours to 45 minutes. German tertiary centers report that 60% of emergency departments use POC molecular panels for sepsis triage by 2024. Integrated analyzers upload results directly to electronic records, enabling antibiotic stewardship teams to adjust therapy within a single shift. Scandinavian primary-care clinics pilot near-patient multiplex panels for influenza, RSV, and SARS-CoV-2, reinforcing epidemiologic surveillance. Vendors respond with ruggedized instruments validated for bedside operation, barcoded reagent tracking, and secure cloud dashboards that meet GDPR requirements.

Advances in NGS & Pharmacogenomics Platforms

Sequencing consumable prices dropped 38% between 2023 and 2025, enabling mid-tier labs to offer 500-gene oncology panels under EUR 450 per sample (USD 489). Liquid-biopsy assays detect minimal residual disease months before imaging, prompting therapy adjustments without invasive tissue sampling. The European Medicines Agency now lists 28 companion diagnostics requiring NGS-double the 2022 count-which accelerates test-menu expansion. French payers reimburse CYP450 and DPYD panels, improving antidepressant and fluoropyrimidine safety. Eastern European reference labs outsource bioinformatics to cloud pipelines hosted in Frankfurt and Dublin, bypassing local skill shortages while meeting data-residency rules. Collectively, these factors propel the Europe molecular diagnostics market toward data-rich oncology workflows.

Requirement for High-Complexity Testing Infrastructure

Advanced workflows need ISO 15189 accreditation, biosafety cabinets, and precision thermocyclers-assets scarce outside Western Europe. In 2024, demand for clinical bioinformaticians exceeded supply by 40%, delaying report sign-off in many Eastern European labs. Limited broadband hampers cloud pipelines in rural districts. EU cohesion funds finance upgrades, yet disbursement cycles stretch to five years. These infrastructure gaps temper near-term uptake, moderating the Europe molecular diagnostics market's reach in less-resourced regions.

Other drivers and restraints analyzed in the detailed report include:

- Surge in EU-wide Antimicrobial-Resistance Surveillance Mandates

- IVDR-Driven Demand for CE-IVD Companion Diagnostics

- Fragmented Payer Reimbursement Across EU-27

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCR platforms generated USD 1.47 billion in 2025, equal to 39.12% of the Europe molecular diagnostics market size. Syndromic respiratory and sepsis panels remain anchored in qPCR due to mature workflows. Sequencing outpaces all technologies at a 9.45% CAGR, capturing oncology and infectious-disease tie-outs. Oxford Nanopore's portable sequencers type meningitis pathogens in 45 minutes, encouraging hybrid strategies in which rapid PCR rules out common infections and on-demand NGS clarifies resistance profiles. Mass spectrometry and microarrays retain niches, but AI-enabled reagent design increasingly blurs platform borders, deepening vendor competition across the Europe molecular diagnostics market.

Infectious disease assays produced USD 1.73 billion in 2025, or 46.10% of the Europe molecular diagnostics market size. Multiplex panels detect 20+ pathogens per sample, reducing sequential testing. Whole-genome sequencing traces hospital outbreaks, feeding infection-control dashboards. Oncology assays grow at 9.52% CAGR, driven by liquid biopsy and targeted therapy selection. Pharmacogenomics panels cross into psychiatry and cardiology, though payer support lags in Southern Europe. Expanded newborn-screening programs push genetic-disease testing, while antimicrobial-resistance assays integrate qPCR with sequencing to oversee surveillance.

The Europe Molecular Diagnostics Market Report is Segmented by Technology (In Situ Hybridization, and More), Application (Infectious Disease Diagnostics, and More), Product (Instruments & Analysers, and More), End-User (Hospitals, and More), Sample Type (Blood, and More), Test Setting (Centralised Laboratories, and More), and Geography (Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Agilent Technologies

- Beckton Dickinson

- bioMerieux

- Biocartis NV

- Cepheid (Danaher)

- Danaher Corporation (Beckman, Leica, Cepheid)

- Eurofins

- Roche

- GenMark Diagnostics

- Hologic

- Illumina

- Luminex (DiaSorin)

- Myriad Genetics

- Oxford Nanopore Technologies

- QIAGEN

- Seegene

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

- T2 Biosystems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Point-of-care (POC) Molecular Assays

- 4.2.2 Advances in NGS & Pharmacogenomics Platforms

- 4.2.3 Surge in EU-wide Antimicrobial-resistance Surveillance Mandates

- 4.2.4 IVDR-driven Demand for CE-IVD Companion Diagnostics

- 4.2.5 Growth of AI-assisted Primer/probe Design Startups

- 4.3 Market Restraints

- 4.3.1 Requirement for High-complexity Testing Infrastructure

- 4.3.2 Fragmented Payer Reimbursement Across EU-27

- 4.3.3 Shortage of Certified Molecular-bioinformaticians

- 4.3.4 GDPR-related Restrictions on Cross-border Sample Transfer

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Technology

- 5.1.1 In Situ Hybridization

- 5.1.2 Chips and Microarrays

- 5.1.3 Mass Spectrometry (MS)

- 5.1.4 Sequencing

- 5.1.5 PCR

- 5.1.6 Other Technologies

- 5.2 By Application

- 5.2.1 Infectious Disease Diagnostics

- 5.2.2 Oncology & Liquid Biopsy

- 5.2.3 Pharmacogenomics

- 5.2.4 Genetic Disease Testing

- 5.2.5 Microbiology & Antimicrobial-Resistance

- 5.2.6 Other Applications

- 5.3 By Product

- 5.3.1 Instruments & Analysers

- 5.3.2 Reagents & Kits

- 5.3.3 Software & Services

- 5.4 By End-user

- 5.4.1 Hospitals & Hospital Labs

- 5.4.2 Independent Reference Laboratories

- 5.4.3 Point-of-Care / Near-Patient Settings

- 5.4.4 Academic & Research Institutes

- 5.5 By Sample Type

- 5.5.1 Blood / Plasma

- 5.5.2 Tissue / FFPE

- 5.5.3 Saliva & Buccal Swab

- 5.5.4 Urine & Other Body Fluids

- 5.6 By Test Setting

- 5.6.1 Centralised Laboratories

- 5.6.2 Decentralised / POC Sites

- 5.7 By Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 France

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Agilent Technologies

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 bioMerieux SA

- 6.3.5 Biocartis NV

- 6.3.6 Cepheid (Danaher)

- 6.3.7 Danaher Corporation (Beckman, Leica, Cepheid)

- 6.3.8 Eurofins Scientific

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 GenMark Diagnostics

- 6.3.11 Hologic Inc.

- 6.3.12 Illumina Inc.

- 6.3.13 Luminex (DiaSorin)

- 6.3.14 Myriad Genetics

- 6.3.15 Oxford Nanopore Technologies

- 6.3.16 QIAGEN N.V.

- 6.3.17 Seegene Inc.

- 6.3.18 Siemens Healthineers

- 6.3.19 Sysmex Corporation

- 6.3.20 Thermo Fisher Scientific

- 6.3.21 T2 Biosystems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment