|

시장보고서

상품코드

1907260

필리핀의 태양 에너지 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Philippines Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

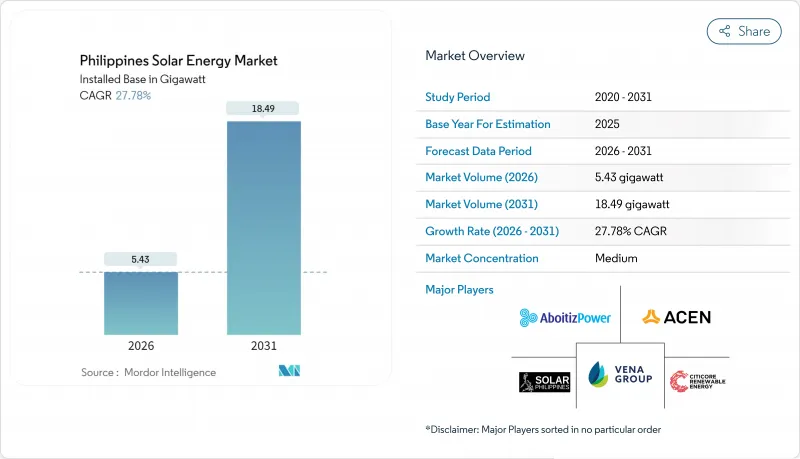

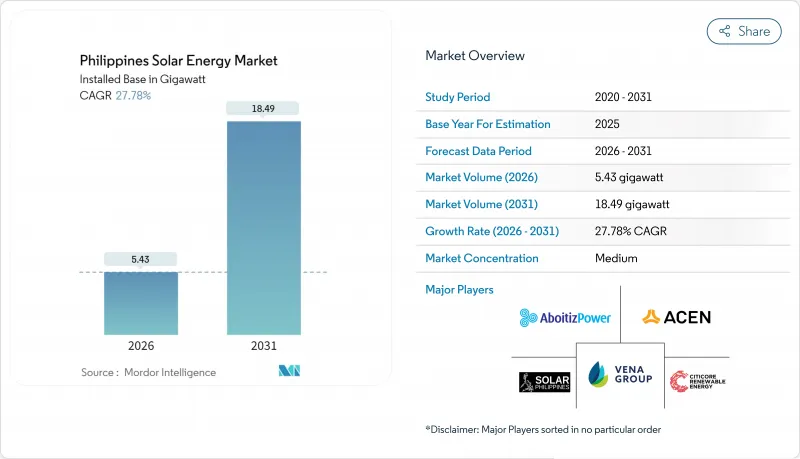

필리핀의 태양 에너지 시장은 2025년 4.25기가와트로 평가되었고, 2026년에는 5.43기가와트로 성장할 전망이며, 2026-2031년 CAGR 27.78%로 성장을 지속하여, 2031년까지 18.49기가와트에 달할 것으로 예측되고 있습니다.

모듈 및 시스템 전체의 비용 절감으로 인해 대규모 태양광 발전의 균등화 발전원가는 1kWh당 0.044달러까지 감소하고, 신규 태양광 발전 용량은 베이스 로드 수요를 충족하기 위한 최저 비용 옵션이 되고 있습니다. 하이퍼스케일 데이터센터와 비즈니스 프로세스 아웃소싱 기업으로부터의 강한 수요가 24시간 365일의 클린 전력을 보증하는 태양광+축전의 하이브리드 프로젝트를 가속시키고 있습니다. 한편, 에너지부의 녹색 에너지 입찰 프로그램(GEAP)은 제4회 입찰에서 10.2기가와트의 용량을 채택했으며, 국내 개발 파이프라인은 36기가와트를 넘어섰습니다. 라구나 호수와 관개용 저수지의 부체식 태양광발전은 토지를 필요로 하지 않는 대체안으로 대두하고 있으며, 넷미터링의 상한을 100kW에서 1메가와트로 끌어올린 규제 개혁에 의해 상업 시설 및 공업 시설의 옥상 이용이 촉진될 전망입니다.

필리핀 태양 에너지 시장 동향 및 인사이트

태양광 모듈 및 BOS 비용의 급격한 감소

세계 유틸리티 규모 태양광 발전 균등화 발전원가(LCOE)는 2023년 0.044달러/kWh로 떨어졌으며 2010년 대비 90% 감소했습니다. 이로 인해 필리핀 국내의 모든 프로젝트에서 자본 지출이 크게 줄어 듭니다. 현지 기업은 현재, Tier 1 모듈을 0.19 USD/W 미만으로 조달 가능하게 되어, 프로젝트 이익률이 확대됩니다. 이것을 받아 Sol-Go사는 국내에 조립 라인을 설치하는 방침입니다. 아시아의 태양광 예산의 75%를 차지해 온 BOS(밸런스 오브 시스템) 지출은 새로운 국내 부가가치 창출의 길이 되고 있으며, 금속 프레임, 인버터, 케이블 제조업체가 수출용 재편을 진행하고 있습니다. 이 비용 동향은 수입 LNG와 기존 석탄에 대한 필리핀 태양광 시장의 경쟁력을 높이며 전력 회사 조달과 기업 간 PPA(전력 구매 계약)를 가속화하고 있습니다. 중기적으로는 2030년까지 연간 3-5GW의 모듈 공급이 가능한 신흥의 국내 제조거점을 지지해, 공급망의 정착을 한층 더 촉진합니다.

그린에너지 입찰(GEAP)에 의해 2025년 이후에 1기가와트 이상의 태양광 발전 파이프라인이 창출될 전망입니다.

에너지부의 경쟁 입찰 모델은 고정 가격 매입제도 대신 가격 발견 기능을 도입하여 첫 입찰로 1GW의 태양광 발전을 채택합니다. 제4회 입찰에서는 태양광 및 축전 하이브리드를 포함한 9,378MW의 목표를 설정했습니다. 개발자의 의욕은 여전히 높고, GEA-3에서는 4,650MW의 상한에 대해 7,500MW의 태양광 입찰이 모여, 임베디드 가격의 압축과 20년간의 안정적인 전력 임베디드을 보증하고 있습니다. 경매 연동형 PPA는 자금 조달 위험을 줄이고 대출자는 스프레드를 축소할 수 있으며 개발자는 축전 설비를 추가하여 설비 가동률을 향상시킬 수 있습니다. GEA-4 이후에 있어서의 축전지 시스템의 의무화는 주간의 출력 억제 문제에 대응 가능한, 계통 친화적인 재생에너지를 향한 정책의 성숙을 나타내고 있습니다. 이러한 경매는 종합적으로 필리핀 태양광 시장을 예측 가능한 건설 사이클과 투명한 비용 기준으로 이끌고 있습니다.

비사야스 민다나오 회랑의 취약한 송전망 용량

2023년까지 우선 송전 프로젝트 16건 중 6건 만이 완료되었으며, 520억 페소 규모의 민다나오 비사야 간선 송전망은 3년 지연되고 있습니다. 병목에 의해 루손 섬 이남의 태양광 도입이 제한되어, 개발 사업자는 접속 가능한 지역에 집중하지 않을 수 없고, 풍부한 일사량이 미활용인 채 남아 있습니다. 2022-2040년 송전망 개발 계획은 확장 계획을 보여주지만, 실행은 수요를 따라잡지 않았습니다. 고압 송전선이 따라잡을 때까지 프로젝트 계획은 루손 섬으로 치우친 상태가 계속될 것입니다.

부문 분석

태양광 발전은 2025년의 설치 베이스의 전량을 차지해, 필리핀에 있어서의 태양 에너지 시장 점유율 100.00%를 확고한 것으로 하고 있습니다. 고효율 n형 i-TOPCon 및 양면 모듈은 발전량 향상과 토지 수요 삭감을 실현하여 필리핀 태양광 발전 시장 규모를 CAGR 27.78%로 확대하고 있습니다. 한편, CSP(집광형 태양광 발전)는 토지 부족과 태풍의 영향으로 상업적으로 비현실적이며, 에너지성(DOE)의 마스터 플랜에서는 당해 기술에 대한 목표치는 설정되어 있지 않습니다.

시장의 설비는 스트링 인버터와 태양광발전+축전의 하이브리드 구조로 이행하고 있어 가동률의 향상과 기업용 PPA에 있어서의 24시간 365일의 조달 조항을 충족하고 있습니다. 테라솔라사의 3.5GW 태양광 발전과 4.5GWh 축전 설비는 이 하이브리드화 동향을 뒷받침해 하이퍼스케일러와의 장기 공급 계약을 확약하고 있습니다.

필리핀의 태양 에너지 시장 보고서는 기술별(태양광 발전 및 집광형 태양열 발전), 계통 접속 유형별(계통 연계형 및 독립형), 최종 사용자별(대규모 사업용, 상업 및 산업용, 주택용)으로 분류되어 있습니다. 시장 규모 및 예측은 설치 용량(GW) 단위로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 태양광 모듈 및 BOS 비용의 급격한 저하

- 그린에너지 입찰(GEAP)에 의해 2025년 이후에 1GW이상의 태양광 발전 프로젝트가 실현 가능해짐

- 하이퍼스케일러 및 BPO 기업에 의한 기업용 전력 구입 계약(PPA)이 24시간 365일의 클린 전력 요구

- DOE 넷미터링 개혁에 의한 100kW 상한의 1MW에 인상(2024년)

- 관개용 저수지에 있어서 부체식 태양광 발전 도입(국가 관개국과의 각서)

- ASEAN 역내의 탄소 국경 조정에 의한 수출 제조업에 대한 압력

- 시장 성장 억제요인

- 비사야스 민다나오 회랑에서 취약한 송전망 용량

- 베트남 및 말레이시아와 비교한 높은 자금 조달 비용(WACC 9% 이상)

- CARP 농지법에 근거한 토지 취득 분쟁

- 태풍 관련 O&M(운용 및 보수) 중단에 의한 LCOE(평균 발전 비용) 약 4%의 상승

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- PESTEL 분석

제5장 시장 규모 및 성장 예측

- 기술별

- 태양광 발전(PV)

- 집광형 태양열 발전(CSP)

- 그리드 유형별

- 온그리드

- 오프 그리드

- 최종 사용자별

- 유틸리티 규모

- 상업 및 산업용(C&I)

- 주택용

- 컴포넌트별(정성적 분석)

- 태양광 모듈 및 패널

- 인버터(스트링형, 중앙 집약형, 마이크로형)

- 가대 및 추적 시스템

- 시스템 주변기기 및 전기기기

- 에너지 저장 및 하이브리드 통합

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 제휴, 전력 구입 계약)

- 시장 점유율 분석(주요 기업의 시장 순위 및 점유율)

- 기업 프로파일

- Solar Philippines Power Project Holdings

- ACEN Corp.

- Vena Energy

- Citicore Power Inc.

- Aboitiz Power Corp.

- Solenergy Systems Inc.

- SunAsia Energy

- Helios Solar Energy Corp.

- Cleantech Global Renewables

- Trina Solar Ltd.

- Canadian Solar

- JinkoSolar

- First Gen Corp.

- Meralco PowerGen(MGen)

- Shell Pilipinas-Solar

- TotalEnergies-Solar

- NextGen Power

- Enfinity Global

- Rizal Wind-Solar Energy Corp.

- Greenergy Holdings

제7장 시장 기회 및 장래 전망

AJY 26.01.26The Philippines Solar Energy Market is expected to grow from 4.25 gigawatt in 2025 to 5.43 gigawatt in 2026 and is forecast to reach 18.49 gigawatt by 2031 at 27.78% CAGR over 2026-2031.

Declining module and balance-of-system costs have driven the levelized cost of utility-scale solar down to USD 0.044 per kWh, making new photovoltaic capacity the least-cost choice for meeting baseload demand. Strong demand from hyperscale data centers and business-process outsourcing firms is accelerating hybrid solar-plus-storage projects that guarantee 24/7 clean power. Meanwhile, the Department of Energy's Green Energy Auction Program (GEAP) has awarded 10.2 GW of capacity in its fourth round, pushing the national development pipeline above 36 GW. Floating solar on Laguna Lake and irrigation reservoirs is emerging as a land-neutral alternative, and reforms that lifted the net-metering ceiling from 100 kW to 1 MW are expected to unlock commercial and industrial rooftops.

Philippines Solar Energy Market Trends and Insights

Rapid Decline in PV Module & BOS Costs

Global utility-scale solar leveledized costs fell to USD 0.044 /kWh in 2023, a 90% drop since 2010, slashing capital outlays for every Philippine project.Local firms now receive price quotes under USD 0.19 /W for Tier-1 modules, widening project margins and spurring Sol-Go to locate assembly lines in the country. Balance-of-system spending, historically 75% of Asian solar budgets, is becoming a new domestic value-add avenue, with metal frame, inverter, and cable manufacturers repositioning for export. This cost trajectory raises the competitive standing of the Philippines' solar energy market against imported LNG and legacy coal, accelerating utility procurement and corporate PPAs. Over the medium term, it also underpins a nascent local manufacturing base that could supply 3-5 GW of modules annually by 2030, further anchoring the supply chain.

Green Energy Auctions (GEAP) Unlocking >=1 GW Solar Pipeline from 2025

The Department of Energy's competitive tender model replaces static feed-in tariffs with price discovery, awarding 1 GW of solar in its inaugural round and setting a 9,378 MW target for the fourth auction that includes solar-storage hybrids. Developer appetite remains robust, GEA-3 drew 7,500 MW of solar bids for a 4,650 MW cap, compressing tariffs and ensuring 20-year off-take certainty. Auction-linked PPAs lower financing risk, enabling lenders to trim spreads and developers to stretch capacity factors with storage add-ons. The integration of mandatory battery systems from GEA-4 onwards signals policy maturation toward grid-friendly renewables that can address midday curtailment. Collectively, auctions move the Philippines' solar energy market toward predictable build-out cycles and transparent cost benchmarks.

Weak Grid Capacity in Visayas-Mindanao Corridor

Only 6 of 16 priority transmission projects were completed by 2023, delaying the PHP 52 billion Mindanao-Visayas backbone by three years.Bottlenecks restrict solar additions south of Luzon, compelling developers to cluster where interconnection is available and leaving ample irradiance unexploited. The Transmission Development Plan 2022-2040 maps expansions, but execution lags grid demand. Until high-voltage lines catch up, project pipelines will stay skewed toward Luzon.

Other drivers and restraints analyzed in the detailed report include:

- Corporate PPAs by Hyperscalers & BPOs Demanding 24/7 Clean Power

- DOE Net-Metering Reform Lifting 100 kW Cap to 1 MW (2024)

- High Financing Costs vs Vietnam & Malaysia (>=9% WACC)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar photovoltaic accounted for the entire 2025 installation base, reinforcing a Philippines solar energy market share of 100.00%. High-efficiency n-type i-TOPCon and bifacial modules lift output and cut land needs, helping the Philippines' solar energy market size for PV rise at a 27.78% CAGR. CSP remains commercially non-viable due to land scarcity and typhoons, and the DOE master plan allocates no targets for the technology.

The market's equipment shift toward string inverters and hybrid PV-plus-storage architectures improves uptime and meets 24/7 procurement clauses in corporate PPAs. Terra Solar's 3.5 GW PV and 4.5 GWh storage confirm this hybrid trend, locking in long-duration supply contracts with hyperscalers.

The Philippines Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Solar Philippines Power Project Holdings

- ACEN Corp.

- Vena Energy

- Citicore Power Inc.

- Aboitiz Power Corp.

- Solenergy Systems Inc.

- SunAsia Energy

- Helios Solar Energy Corp.

- Cleantech Global Renewables

- Trina Solar Ltd.

- Canadian Solar

- JinkoSolar

- First Gen Corp.

- Meralco PowerGen (MGen)

- Shell Pilipinas - Solar

- TotalEnergies - Solar

- NextGen Power

- Enfinity Global

- Rizal Wind-Solar Energy Corp.

- Greenergy Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid decline in PV module & BOS costs

- 4.2.2 Green energy auctions (GEAP) unlocking >=1 GW solar pipeline from 2025

- 4.2.3 Corporate PPAs by hyperscalers & BPOs demanding 24/7 clean power

- 4.2.4 DOE net-metering reform lifting 100 kW cap to 1 MW (2024)

- 4.2.5 Floating-solar deployment on irrigation reservoirs (National Irrigation Admin MoU)

- 4.2.6 ASEAN-wide carbon border adjustment pressure on export manufacturers

- 4.3 Market Restraints

- 4.3.1 Weak grid capacity in Visayas-Mindanao corridor

- 4.3.2 High financing costs vs. Vietnam & Malaysia (>=9 % WACC)

- 4.3.3 Land-acquisition disputes under CARP agrarian rules

- 4.3.4 Typhoon-related O&M disruptions raising LCOE by ~4 %

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Solar Philippines Power Project Holdings

- 6.4.2 ACEN Corp.

- 6.4.3 Vena Energy

- 6.4.4 Citicore Power Inc.

- 6.4.5 Aboitiz Power Corp.

- 6.4.6 Solenergy Systems Inc.

- 6.4.7 SunAsia Energy

- 6.4.8 Helios Solar Energy Corp.

- 6.4.9 Cleantech Global Renewables

- 6.4.10 Trina Solar Ltd.

- 6.4.11 Canadian Solar

- 6.4.12 JinkoSolar

- 6.4.13 First Gen Corp.

- 6.4.14 Meralco PowerGen (MGen)

- 6.4.15 Shell Pilipinas - Solar

- 6.4.16 TotalEnergies - Solar

- 6.4.17 NextGen Power

- 6.4.18 Enfinity Global

- 6.4.19 Rizal Wind-Solar Energy Corp.

- 6.4.20 Greenergy Holdings

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment