|

시장보고서

상품코드

1907301

발포 폴리스티렌(EPS) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Expanded Polystyrene (EPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

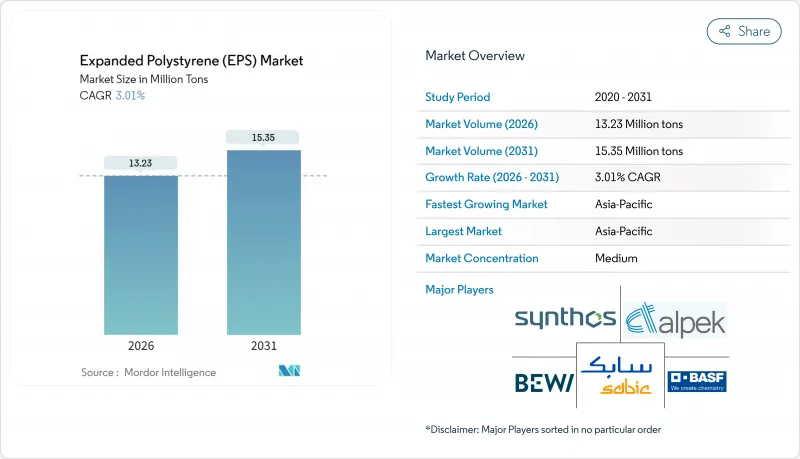

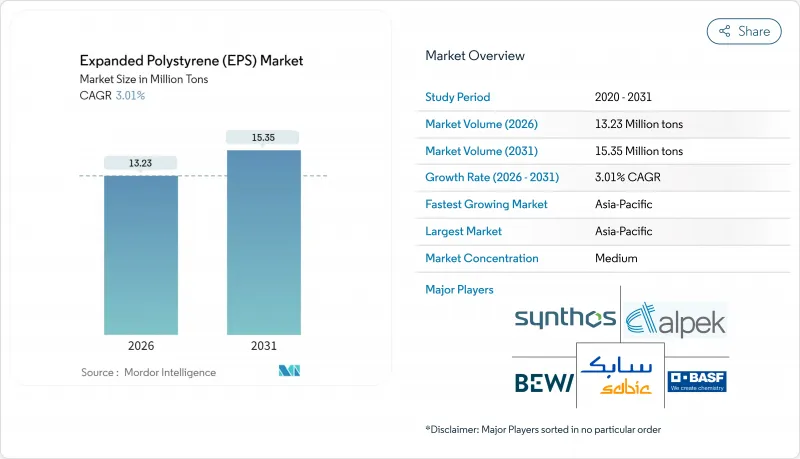

2026년 발포 폴리스티렌(EPS) 시장 규모는 1,323만 톤으로 평가되었고, 2025년 1,284만 톤에서 성장할 전망입니다.

2031년 예측치는 1,535만톤으로 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 3.01%로 성장할 전망입니다.

이 수량 성장은 건설 및 포장 분야의 소비 증가와 스티렌 가공에 대한 엄격한 휘발성 유기 화합물(VOC) 제한으로 인한 비용 압박 사이의 상충 관계를 반영합니다. 발포 폴리스티렌 시장은 우수한 열전도율 대비 가격 비율을 지속적으로 활용하여 성형 펄프, 바이오 폼, 종이 기반 라이너의 규모 확대에도 불구하고 수요를 안정적으로 유지하고 있습니다. 아시아태평양 지역은 여전히 최대 단일 시장으로 자리매김하고 있으며, 북미 지역은 전자상거래 최종 배송 단계 단열재로 이 소재를 활용하고 있습니다. 기업 전략은 점차 화학적 재활용 경로와 원료 다각화에 중점을 두며, 발포 폴리스티렌 시장 전반에 걸쳐 순환경제 준수가 새로운 경쟁 필수 요건으로 부상하고 있음을 시사합니다.

세계의 발포 폴리스티렌(EPS) 시장 동향 및 인사이트

탄소중립 건물 가속화 추세

급속한 탈탄소화 목표가 전 세계 단열재 규격을 재편하고 있습니다. 유럽의 에너지 성능 의무화 기준은 신축 건물에 근접 제로 에너지(nearly-zero-energy)를 요구하며, 건축가들로 하여금 낮은 λ값과 검증된 내구성을 겸비한 소재를 선택하도록 유도합니다. 회색 및 은색 EPS는 표준 등급 대비 최대 20% 낮은 열전도율을 제공하여 U값 준수를 저해하지 않으면서도 더 얇은 벽체 조립이 가능하게 합니다. 일본의 2024년 에너지 효율 개정안은 열 외피 기준을 강화하여 흑연 강화 발포 폴리스티렌 시장 솔루션에 대한 수요를 더욱 증폭시키고 있습니다. 건물 소유주들이 운영 비용 절감을 최우선으로 삼으면서, EPS는 연속 단열재 및 구조용 단열 패널 분야에서 입지를 넓혀 고성능 건축 부문에서 발포 폴리스티렌 시장의 위상을 강화하고 있습니다.

신흥 아시아태평양의 콜드체인 투자 부활

동남아시아 정부들은 식품 부패 억제 및 의약품 안전 기준 유지를 위해 콜드체인 물류에 수십억 달러를 투자하고 있습니다. EPS 박스와 라이너는 단위당 최저 배송 비용으로 R값 안정성과 충격 흡수 기능을 결합하여 시장을 주도합니다. 베트남의 반도체 조립 허브는 좁은 열적 창을 유지하기 위해 EPS 클램쉘을 의존하며, 지역 백신 캠페인은 온도에 민감한 생물학적 제제를 보호하기 위해 검증된 EPS 운송 용기에 의존합니다.

스티렌의 VOC 배출 상한값 계약

EU는 2024년 직업적 스티렌 노출 한도를 20ppm으로 낮추면서, 제조업체들이 운영 비용을 3-5% 증가시킬 수 있는 저감 시스템을 개조하도록 강제하고 있습니다. 같은 해 미국 EPA의 집행 조치는 40% 증가하여 규정 준수 위험을 높였습니다. 재생 열산화 장치(RTO) 설치 자금이 부족한 중소 변환업체들은 시장에서 퇴출될 수 있으며, 이는 지역별 공급을 축소시키고 발포 폴리스티렌 시장 전반에 걸쳐 가격 상승 압력을 가할 전망입니다.

부문 분석

2025년 백색 EPS는 발포 폴리스티렌 시장의 95.12%를 차지했으나, 회색 EPS는 2031년까지 연평균 3.89%의 성장률로 더 빠르게 확대될 전망입니다. 독일과 프랑스 건설사들은 두꺼운 벽체 없이도 U-값 기준을 충족시키기 위해 흑연 함유 패널을 지정하며, 가격 상승에도 성능 개선이 수요를 전환시키는 사례를 보여줍니다. BASF와 같은 제조사들은 이러한 건설 수요를 충족시키기 위해 2024년 네오포르 생산 능력을 40% 증설했습니다. 동시에 반사성 은색 EPS 등급은 표면 온도가 80°C를 초과하는 산업용 단열 틈새 시장에 진입하며, 규모는 작지만 성장 중인 전문 분야 기회를 활용하고 있습니다. 일반 포장재 시장은 여전히 흰색 폼에 크게 의존하는데, 물류 구매자들이 초기 비용 절감을 우선시하기 때문입니다. 그러나 건축 규정이 강화됨에 따라 고단열성 제품군이 팽창 폴리스티렌 시장에서 흰색 EPS의 지배력을 점차 잠식할 전망입니다.

백색 EPS의 비용 경쟁력은 가전제품 완충재, 성형 어류 운반용 상자, 블록 성형 건축 자재 분야에서 그 입지를 공고히 합니다. 회색 EPS는 프리미엄 가격에도 불구하고 에너지 효율적인 외장 시스템을 통해 물량을 확보하며, 모든 신규 제로 에너지 프로젝트가 흑연 등급에 톤수를 할당하도록 보장합니다. 은색 EPS의 확장은 석유화학 파이프 단열재 및 LNG 터미널의 고온 콜드박스 라이닝에 적합하다는 점을 고려할 때 소폭이지만 수익성이 높습니다. 이러한 추세는 차별화된 성능이 대체로 상품화된 발포 폴리스티렌 시장 내에서도 방어 가능한 가치 영역을 창출함을 입증합니다.

발포 폴리스티렌 시장 보고서는 제품 유형(백색 EPS, 회색 EPS, 은색 EPS), 최종 사용자 산업(건축, 건설, 전기, 전자, 포장 및 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양 지역은 2025년 글로벌 톤수 기준 66.75%를 차지했으며, 2031년까지 연평균 3.21% 성장률(CAGR)로 증가할 것으로 전망됩니다. 중국의 도시화 추진은 주택 착공을 지속시키는 반면, 인도의 PM 가티 샤크티(PM Gati Shakti) 프로그램은 도로 및 창고 프로젝트에 수십억 달러를 투입하여 단열재 수요 증가로 이어지고 있습니다. 태국과 베트남이 주도하는 동남아시아는 식품 안전 지침 충족을 위한 콜드체인 확장에 투자하며, 팔레트 크기 어류 상자와 백신 쿨러용 EPS 물량 증가를 이끌고 있습니다. 해당 지역의 수직 통합 스티렌 복합체는 지속적으로 낮은 비용을 유지하여, 팽창 폴리스티렌 시장 전반에 걸쳐 현지 생산자들에게 구조적 우위를 제공합니다.

북미는 전자상거래 및 모듈식 건축 사이클에 의해 주도되는 주요 시장입니다. 미국 주별 에너지 규정은 연속 단열층 설치를 점점 더 의무화하고 있으며, 공장 조립식 벽 패널은 현장 시공 기간 단축을 위해 EPS 코어를 내장하는 경우가 빈번합니다. 캐나다 퀘벡과 온타리오에서 진행 중인 수십억 달러 규모의 냉장 시설 건설은 신선식품 포장 수요를 촉진하여 지역 EPS 수요의 안정적인 기반을 확보하고 있습니다. 멕시코는 전자제품 수출 증가로 인쇄회로기판 운송용 정전기 방지 EPS 포장재 수요가 증가하며 북미 시장을 완성합니다.

유럽은 폐기물 감축 규제가 강화되었으나, EU 그린딜 자금으로 추진되는 심층 에너지 개조를 위해 여전히 EPS에 의존하고 있습니다. 이탈리아의 내진 보강 인센티브와 독일의 건물 에너지법은 패널 판매를 유지시키는 반면, 영국의 급성장하는 배달 서비스는 일회용 식기용 성형 펄프 금지 조치로 인한 판매량 감소를 상쇄하고 있습니다. 사우디아라비아의 석유화학 확장 및 브라질의 인프라 회랑은 물류 네트워크가 성숙함에 따라 이들 지역의 점유율이 증가할 수 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 탄소중립 준비 건물에 대한 가속화된 추진

- 신흥 아시아태평양의 콜드체인 투자 부활

- 전자상거래의 라스트마일 단열 포장 수요 증가

- 유럽 및 일본의 의무적 내진 단열 규정

- 모듈식 조립식 건축의 보급

- 시장 성장 억제요인

- 스티렌에 대한 VOC 배출 상한선 강화

- 성형 펄프 단열 라이너의 급속한 규모 확대

- EU 「리사이클 설계」지령에 의한 일회용 EPS의 억제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 수출입 동향

제5장 시장 규모와 성장 예측(금액 및 수량)

- 제품 유형별

- 백색 EPS

- 회색 및 은색 EPS

- 최종 사용자 산업별

- 건축 및 건설

- 전기 및 전자 기기

- 포장

- 기타 최종 사용자 산업(농업 및 자동차 산업)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd.(Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis SpA

- Wuxi Xingda foam plastic new material Limited

제7장 시장 기회와 장래의 전망

HBR 26.02.04Expanded Polystyrene market size in 2026 is estimated at 13.23 million tons, growing from 2025 value of 12.84 million tons with 2031 projections showing 15.35 million tons, growing at 3.01% CAGR over 2026-2031.

Volume growth reflects the push-pull between rising consumption in construction and packaging and the cost pressures generated by stringent volatile-organic-compound limits on styrene processing. The Expanded Polystyrene market continues to capitalize on its favorable thermal conductivity-to-price ratio, which keeps demand steady even as molded pulp, bio-foams, and paper-based liners scale up. Asia-Pacific remains the single largest outlet, while North America leverages the material for e-commerce last-mile insulation. Corporate strategies increasingly pivot on chemical recycling pathways and feedstock diversification, signaling that circular-economy compliance is an emerging competitive prerequisite across the Expanded Polystyrene market.

Global Expanded Polystyrene (EPS) Market Trends and Insights

Accelerated Push for Net-Zero-Ready Buildings

Rapid decarbonization targets are redrawing insulation specifications worldwide. Energy-performance mandates in Europe require near-zero-energy new builds, pushing architects toward materials that combine low λ-values with proven durability. Gray and silver EPS deliver up to 20% lower thermal conductivity than standard grades, enabling thinner wall assemblies without compromising U-value compliance. Japan's 2024 energy-efficiency revision tightens thermal-envelope criteria, further amplifying demand for graphite-enhanced Expanded Polystyrene market solutions. As building owners prioritize operating-cost reductions, EPS gains traction in continuous insulation and structural insulated panels, reinforcing the Expanded Polystyrene market's profile in the high-performance building segment.

Resurgent Cold-Chain Investments in Emerging APAC

Southeast Asian governments are funneling billions into cold-chain logistics to curb food spoilage and uphold drug-safety standards. EPS boxes and liners dominate because they combine R-value stability with shock absorption at the lowest delivered cost per unit. Semiconductor assembly hubs in Vietnam rely on EPS clamshells to maintain narrow thermal windows, while regional vaccine campaigns depend on validated EPS shippers to protect temperature-sensitive biologics.

Tightening VOC Emission Ceilings on Styrene

The EU lowered occupational styrene limits to 20 ppm in 2024, forcing manufacturers to retrofit abatement systems that can add 3-5% to operating costs. EPA enforcement actions in the United States climbed 40% the same year, raising compliance risk. Smaller converters lacking capital for regenerative thermal oxidizers may exit, narrowing regional supply and nudging prices upward across the Expanded Polystyrene market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Last-Mile Insulated Packaging Boom

- Mandatory Seismic Insulation Codes in Europe and Japan

- EU "Design for Recycling" Mandates Curbing Single-Use EPS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White EPS accounted for 95.12% of the Expanded Polystyrene market in 2025, yet gray variants are on track to expand faster at 3.89% CAGR through 2031. Builders in Germany and France specify graphite-infused panels to meet U-values without thicker walls, illustrating how performance upgrades redirect demand even when prices are higher. Manufacturers such as BASF added 40% Neopor capacity in 2024 to satisfy this construction pull. Concurrently, reflective silver EPS grades penetrate industrial insulation niches where surface temperatures exceed 80 °C, tapping small but growing specialized opportunities. Commodity packaging still leans heavily on white foam because logistics buyers prioritize low upfront cost. As building codes tighten, however, higher-R-value lines will gradually chip away at white EPS dominance within the Expanded Polystyrene market.

White EPS's cost edge keeps it entrenched in appliance cushioning, molded fish crates, and block-molded architectural shapes. Gray EPS, despite its premium, secures volume through energy-efficient facade systems, ensuring that every new near-zero-energy project allocates tonnage to graphite grades. The expansion of silver EPS stays modest but lucrative, given its fit for petrochemical pipe insulation and high-temperature cold-box linings in LNG terminals. These trends confirm that differentiated performance creates defensible value pockets, even inside a largely commoditized Expanded Polystyrene market.

The Expanded Polystyrene Market Report is Segmented by Product Type (White EPS and Gray and Silver EPS), End-User Industry (Building and Construction, Electrical and Electronics, Packaging, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific secured 66.75% of global tonnage in 2025 and is projected to rise at a 3.21% CAGR to 2031. China's urbanization pipeline sustains housing starts, while India's PM Gati Shakti program channels billions into road and warehousing projects, translating into higher insulation demand. Southeast Asia, led by Thailand and Vietnam, bankrolls cold-chain expansion to meet food-safety directives, pulling incremental EPS volumes for pallet-sized fish boxes and vaccine coolers. The region's vertically integrated styrene complexes keep delivering costs low, giving local producers a structural advantage across the Expanded Polystyrene market.

North America is a significant market, driven by e-commerce and modular construction cycles. U.S. state-level energy codes increasingly require continuous-insulation layers, and factory-assembled wall panels frequently embed EPS cores to accelerate job-site completion. Canada's multibillion-dollar cold-storage builds in Quebec and Ontario drive fresh packaging orders, ensuring a dependable baseline for regional EPS demand. Mexico rounds out the North American picture with rising electronics exports, necessitating anti-static EPS packs for printed-circuit-board transit.

Europe confronts stricter waste-reduction rules but still leans on EPS for deep-energy retrofits funded by the EU Green Deal. Italy's seismic-retrofit incentives and Germany's Building Energy Act sustain panel sales, while the United Kingdom's booming meal-delivery services offset volume lost to molded-pulp bans in single-use cutlery. Petrochemical expansions in Saudi Arabia and infrastructure corridors in Brazil suggest these territories could increase their shares as logistics networks mature.

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd. (Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis S.p.A.

- Wuxi Xingda foam plastic new material Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated push for net-zero ready buildings

- 4.2.2 Resurgent cold-chain investments in emerging APAC

- 4.2.3 E-commerce last-mile insulated packaging boom

- 4.2.4 Mandatory seismic insulation codes in Europe and Japan

- 4.2.5 Modular prefab construction uptake

- 4.3 Market Restraints

- 4.3.1 Tightening VOC emission ceilings on styrene

- 4.3.2 Rapid scale-up of molded pulp thermal liners

- 4.3.3 EU "Design for Recycling" mandates curbing single-use EPS

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import-Export Trends

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 White EPS

- 5.1.2 Gray and Silver EPS

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Electrical and Electronics

- 5.2.3 Packaging

- 5.2.4 Other End-user Industries (Agriculture and Automotive)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Nordic Countries

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alpek SAB de CV

- 6.4.2 BASF

- 6.4.3 BEWi

- 6.4.4 Epsilyte LLC

- 6.4.5 Ineos

- 6.4.6 Kaneka Corporation

- 6.4.7 Ravago

- 6.4.8 SABIC

- 6.4.9 Shuangliang Group Co., Ltd. (Jiangsu Leasty Chemical Co.,Ltd.)

- 6.4.10 SIBUR International GmbH

- 6.4.11 Sunde Group

- 6.4.12 Sunpor

- 6.4.13 Synthos

- 6.4.14 TotalEnergies

- 6.4.15 Versalis S.p.A.

- 6.4.16 Wuxi Xingda foam plastic new material Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Bio-based and Chemically Recycled EPS Roadmap