|

시장보고서

상품코드

1910432

포장 필름 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Packaging Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

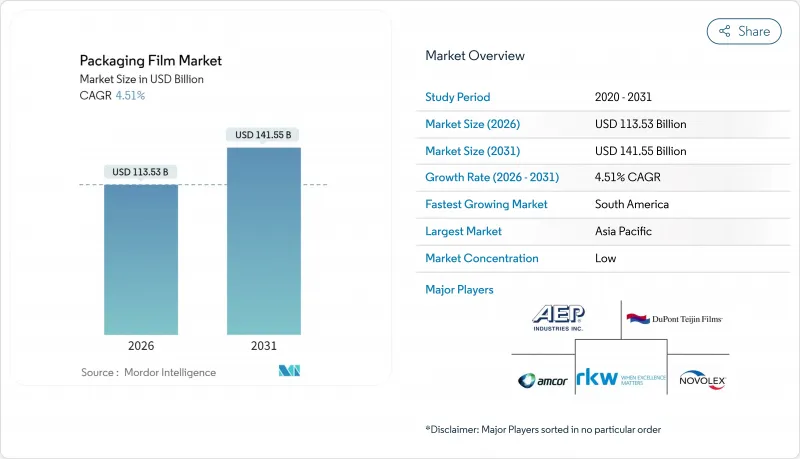

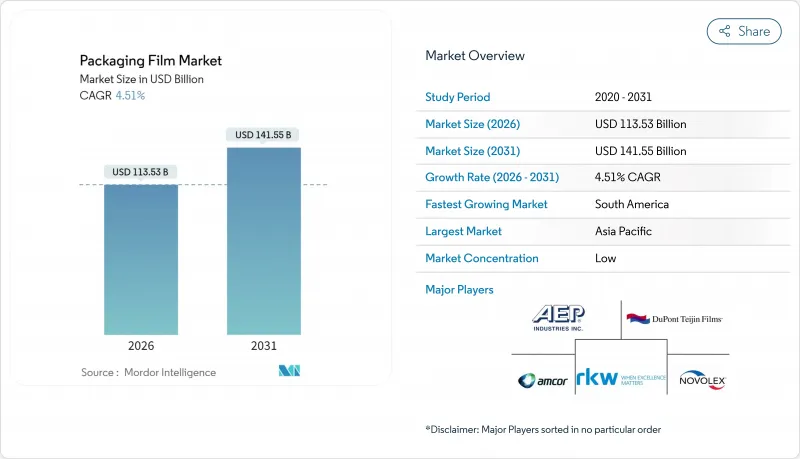

포장 필름 시장은 2025년에 1,086억 3,000만 달러로 평가되었으며, 2026년 1,135억 3,000만 달러, 2031년까지 1,415억 5,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026-2031년)의 CAGR은 4.51%를 나타낼 전망입니다.

경량 전자상거래 운송 자재에 대한 수요 증가, 유럽의 재활용 가능성에 대한 규제 강화, 신흥 아시아태평양 경제 지역의 콜드체인의 급속한 확대가 꾸준한 성장세를 지원하고 있습니다. 다층 장벽 기술 혁신, 항균 마스터 배치 및 화학적 재활용 원료에 대한 합의가 프리미엄 성장 분야를 지원하는 반면, 전략적 합병은 세계 주요 컨버터 간의 규모 우위를 더욱 강조하고 있습니다.

세계 포장 필름 시장 동향과 인사이트

전자상거래의 급성장이 경량배송필름 수요를 견인

소포량 증가에 따라, 브랜드 각 사는 배송용 포장의 크기를 줄이면서 내낙하성을 유지하면서 용적 중량을 최대 30% 삭감하고 있습니다. PAC Worldwide의 Eco PAC 재킷 시스템은 배송용 봉투의 자동화와 완성 센터의 인건비 절감을 실현하여 비용 효율성과 재활용 목표를 양립시킵니다. 이중 씰 택배 가방은 고객 로열티에 필수적인 역물류 프로그램을 지원합니다. 단납기 그래픽은 디지털 인쇄기를 활용해, 브랜드 인게이지먼트를 강화하는 테마별 프로모션을 제공하여 고액의 요금을 피할 수 있도록 합니다. 이러한 요인들과 함께 포장 필름 시장은 세계 소매 디지털화의 주요 수혜자로서 입지를 강화하고 있습니다.

EU에 의한 단일 소재 재활용 필름 추진

포장 및 포장 폐기물 규제는 2030년까지 플라스틱 식품 포장의 재생재 함량 30% 달성과 완전 재활용성을 의무화하여 폴리올레핀 단층 라미네이트로의 전환을 가속화하고 있습니다. 모팩사의 80% 재생 폴리에틸렌(rPE) 함유 인증 구조는 상업적 실용성을 실증하고, 컨버터 각 사는 탈잉크 및 세척 시스템을 설치하여 규제 대응을 추진합니다. 확대 생산자 책임(EPR) 비용은 폐쇄형 루프 회수를 가능하게 하는 설계를 촉진하는 재료 비용의 레버가 됩니다. 규제 기한이 다가오는 중, 포장 필름 시장에서는 성능과 리사이클성을 양립시키는 표준 설계 룰이 채택되고 있습니다.

북미 및 유럽의 플라스틱 금지 및 과세

일회용 제품에 대한 과세나 PFAS 금지에 의해 사양의 급격한 재검토가 강요되고, 중규모 공장에서는 연구개발 예산이 박박해, 고객의 인증 사이클이 장기화하고 있습니다. 정책 도입의 편차로 인해 브랜드가 지역별 구식 라미네이트 재료의 폐지 기한에 대응하기 때문에 재고 계획이 복잡해지고 있습니다.

부문 분석

폴리에틸렌은 2025년에도 포장 필름 시장에서 42.10%의 점유율을 유지했고 우수한 비용 성능과 광범위한 가공성을 배경으로 합니다. 고밀도 등급은 반경질 용도로, LDPE 및 LLDPE는 블로우 필름 용도의 대부분을 지원합니다. 바이오플라스틱은 정책 동향과 브랜드 공약 강화로 2031년까지 견고한 CAGR 7.75%를 기록할 전망입니다. 바이오플라스틱 제품의 포장 필름 시장 규모는 원료의 스케일업이 순조롭게 진행되면 10년 이내에 수십억 달러 규모에 달할 것으로 예측됩니다. 폴리프로필렌의 2축 연신 제품은 고급 과자 포장용으로 투명성과 강성으로 경쟁력을 발휘합니다. PET층은 레토르트 용도로 치수 안정성을 확보하고, 높은 가스 배리어성을 요구하는 경우에는 산화알루미늄 코팅과 조합되는 경우가 많습니다. 화학적 재활용 기술의 발전으로 신규 원료와 동등한 특성을 가진 폐쇄 루프 PE가 실현되고 있으며, 티타늄 실리케이트 촉매 기술은 현재 파일럿 스케일 단계에 있습니다. 블록 공중합 PLA의 혁신은 취성을 감소시키고 신선한 식품 파우치를 위한 80%의 바이오베이스 비율을 제공합니다.

폴리에틸렌 가공 업체는 고속 성형 충전 씰 라인에 필수적인 특성인 씰 투과 오염 성능을 향상시키는 메탈로센계 촉매에 대한 투자를 진행하고 있습니다. 포장 필름 시장은 비용 효율성과 지속가능성 요청 간의 균형을 모색하고 있으며 기존 제조업체가 생산량을 유지하면서 특수 바이오폴리머가 규제 요건과 소비자 선호도의 변화에 대응하고 있습니다.

다층 구조는 층별 기능성으로 기계적, 광학적, 장벽 특성을 최적화했으며, 2025년에는 매출액의 56.20%를 차지했습니다. 의약품 물류나 레토르트 식품 분야에서 장기 보존이 요구되는 가운데, EVOH 또는 AlOx층을 포함한 배리어 적층재는 CAGR6.14%로 확대 중입니다. 한편, 회수 공정이 단순한 화학 조성을 요구하는 분야(특히 북미의 점포 회수 재활용)에서는 단층 필름이 여전히 중요성을 유지하고 있습니다.

공압출기에는 인라인 연신장치를 추가하여 기계방향 연신 PE 라미네이트를 제조함으로써 재활용성을 충족하면서 내천자성을 유지합니다. 나노 클레이 분산액은 동등한 두께로 산소 투과율을 60% 감소시켜 추가적인 하향 조정의 길을 열어줍니다. 층 두께 스캐너는 프로파일 정밀도를 향상시키고 시동시 폐기물을 최소화함으로써 포장 필름 시장 진출기업의 수익성 향상에 직결되는 수율 개선을 실현합니다.

지역별 분석

아시아태평양은 풍부한 수지 공급, 경쟁력 있는 노동력, 광대한 소비자 기반에 힘입어 2025년에도 포장 필름 시장의 37.00% 점유율을 유지했습니다. 중국의 과잉 포장 규제 "GB/T 31268-2024"는 소포 중량 제한을 충족하는 초경량 파우치 수요를 환기하고 있습니다. 태국과 인도네시아에서는 시험 프로토콜을 표준화하고 현지 압출 기술의 고도화를 촉진하는 식품 접촉 규제의 조화를 이루고 있습니다. JPFL 필름즈와 같은 인도 기업들은 국내 및 수출 기회를 획득하기 위해 연간 6만 톤의 BOPP 생산 능력을 추가했습니다. 일본과 한국은 배리어 코팅의 연구개발을 추진하고, 호주는 사용한 재활용 소재의 사용률 향상에 중점을 두고 있습니다.

유럽에서는 PPWR의 재생 가능성 및 재생재 함량 기준을 충족하기 위해 변혁적인 투자 사이클에 직면하고 있습니다. 콘스탄티아 플렉서블스에 의한 알류플렉스팩 인수는 호일 가공 기술의 통합과 동남유럽에서의 기반 강화로 이어졌습니다. 브랜드 각사는 소비자용 폐기 절차의 QR코딩을 도입하여 회수품의 순도 향상을 도모하고 있습니다. 영국과 독일에서는 화학적 재활용 회수 거점의 시험 운용이 시작되어 재생 폴리에틸렌(rPE)의 통합을 추진하고 있습니다.

북미에서는 성숙한 전자상거래 네트워크와 정책의 명확화가 진행되고 있습니다. PFAS(퍼플루오로알킬 물질) 사용 금지 기한에 따라 컨버터는 금속화 BOPP나 AlOx PET로 이행, 캐나다는 원료 비용 우위성을 살려 주요 수출국으로서의 지위를 유지, 멕시코 시설은 국내 스낵 시장과 미국 남부 밸류체인 모두에 공급됩니다.

남미는 2031년까지 7.60%라는 가장 빠른 CAGR로 성장할 것으로 예상되며, 높은 배리어 필름을 필요로 하는 농산물 수출이 견인역입니다. OPP FILM COLOMBIA사와 GDM Plasticos사의 투자에 의해 BOPP 및 CPP의 생산 기반이 확대되었습니다. 지역자금기구는 에코디자인연구소를 지원하고 포장 필름 시장에서 새로운 성장 프론티어로서의 지위를 확립하고 있습니다.

중동 및 아프리카에서는 도시 소매업의 확대로 견고한 두 자리 수량 증가가 예상됩니다. 사우디아라비아와 아랍 에미리트 연합에서는 조달 선택을 유도하는 재생 가능한 플라스틱의 의무화가 도입되었으며 남아프리카의 확립된 컨버터는 비용 최적화 제품으로 광범위한 대륙 시장에 서비스를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자상거래의 급성장으로 경량 배송용 필름 수요 증가

- EU에 의한 단일 소재 리사이클 가능 필름의 추진

- 신흥 아시아태평양의 콜드체인 포장 식품 성장

- 소량 다품종 맞춤형 패키징을 가능케 하는 디지털 인쇄 기술

- 육류 포장용 필름을 위한 항균 마스터배치(Masterbatch) 첨가제 활용

- 식품 등급 재생 폴리에틸렌(rPE)용 화학 재활용 원료 공급 계약

- 시장 성장 억제요인

- 북미 및 유럽에서의 플라스틱 금지 조치/과세

- 변동하는 신재 수지 가격

- 바이오 기반 필름의 차단성 한계

- 초박막 규격(Ultra-thin gauge) 생산 시 가공 업체(Converter)의 가동 중단 리스크

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 소재 유형별

- 폴리에틸렌

- 고밀도 폴리에틸렌(HDPE)

- 저밀도 폴리에틸렌(LDPE)

- 선형 저밀도 폴리에틸렌(LLDPE)

- 폴리프로필렌

- 폴리에스테르(BOPET)

- 바이오플라스틱

- 기타 소재 유형

- 폴리에틸렌

- 필름 구조별

- 단층 필름

- 다층 필름(2-3층)

- 배리어 다층 필름(3층 초과)

- 용도별

- 식음료

- 의약품 및 의료

- 퍼스널케어 및 화장품

- 내구 소비재 및 전자 기기

- 산업 및 기관용

- 농업 및 원예

- 기타 용도

- 용도별 포맷

- 백 및 파우치

- 랩 및 뚜껑용 필름

- 라벨과 슬리브

- 블리스터 및 샤쉐 (Sachets)

- 수축 랩 및 스트레치 랩

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 싱가포르

- 말레이시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Jindal Poly Films Ltd

- Cosmo Films Ltd

- Uflex Ltd

- Huhtamaki Oyj

- ProAmpac Holdings

- Novolex Holdings

- AEP Industries

- RKW SE

- Toray Plastics

- Coveris Holdings

- Sigma Plastics Group

- SRF Limited

- Klockner Pentaplast

- Taghleef Industries

- Polyplex Corporation

- Transcontinental Inc.

- Dupont Teijin Films

제7장 시장 기회와 장래의 전망

SHW 26.01.26The packaging film market was valued at USD 108.63 billion in 2025 and estimated to grow from USD 113.53 billion in 2026 to reach USD 141.55 billion by 2031, at a CAGR of 4.51% during the forecast period (2026-2031).

Heightened demand for lightweight e-commerce shipping materials, stricter European recyclability rules, and rapid cold-chain expansion in emerging Asia-Pacific economies sustain steady momentum. Multilayer barrier innovations, antimicrobial masterbatches, and chemical-recycling feedstock agreements underpin premium growth niches, while strategic mergers accentuate scale advantages among the top global converters.

Global Packaging Film Market Trends and Insights

E-commerce Boom Driving Demand for Lightweight Shipping Films

Parcel-volume growth pushes brands to down-gauge shipping packs, trimming dimensional weight by up to 30% while preserving drop resistance. PAC Worldwide's Eco PAC jacket system automates mailer conversion and reduces labor at fulfillment centers, aligning cost efficiency with recyclability goals. Dual-seal courier bags support reverse-logistics programs that are integral to customer loyalty. Short-run graphics tap digital presses for thematic promotions that strengthen brand engagement and circumvent high plate charges. These factors collectively reinforce the packaging film market as a core beneficiary of global retail digitization.

EU Push for Mono-Material Recyclable Films

The Packaging and Packaging Waste Regulation obligates 30% recycled content in plastic food packs by 2030 and requires full recyclability, accelerating the shift toward polyolefin-only laminates. Mopack's certified structures with 80% rPE validate commercial readiness, while converters install de-inking and wash systems to secure compliance. Extended Producer Responsibility fees become a material cost lever that favors designs enabling closed-loop recovery. As compliance deadlines approach, the packaging film market adopts standardized design rules that harmonize performance with recyclability.

Plastic Bans/Taxes in North America and Europe

Single-use levies and PFAS prohibitions force rapid specification overhaul, stretching R&D budgets at mid-sized plants and lengthening customer qualification cycles. Fragmented policy rollouts complicate inventory planning as brands juggle differing regional cutoffs for legacy laminates.

Other drivers and restraints analyzed in the detailed report include:

- Cold-Chain Packaged Food Growth in Emerging Asia-Pacific

- Digital Printing Enabling Short-Run Personalised Packs

- Volatile Virgin-Resin Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene preserves 42.10% share of the packaging film market in 2025, riding its favorable price-performance profile and broad processability. High-density grades serve semi-rigid uses while LDPE and LLDPE underpin the bulk of blown-film applications. Bioplastics post a robust 7.75% CAGR through 2031 as policy signals and brand pledges intensify. The packaging film market size for bioplastic variants is projected to reach multi-billion USD territory by decade-end, provided feedstock scaling continues apace. Polypropylene's biaxially oriented formats compete on clarity and stiffness for premium confectionery. PET layers ensure dimensional stability in retort applications, often coupled with aluminum-oxide coatings for a high gas barrier. Chemical-recycling advances promise closed-loop PE that matches virgin properties, with titanosilicate catalysis now at pilot scale. Block-copolymerized PLA breakthroughs cut brittleness, offering an 80% bio-based alternative for fresh-produce pouches.

Polyethylene converters invest in metallocene catalysts that upgrade seal-through-contamination performance, an essential trait for high-speed form-fill-seal lines. The packaging film market thus balances cost efficiency against sustainability pulls, with incumbents safeguarding volume while specialty biopolymers address regulatory requirements and consumer preference shifts.

Multilayer constructions controlled 56.20% revenue in 2025 by optimizing mechanical, optical and barrier attributes through layer-specific functionality. Barrier stacks incorporating EVOH or AlOx layers are on course for 6.14% CAGR as pharma logistics and ready-meal sectors require longer shelf life. Monolayer films retain relevance where recovery streams demand simpler chemistries, notably for store drop-off recycling in North America.

Co-extruders add inline orientation units to produce machine-direction oriented PE laminates that satisfy recyclability while keeping puncture resistance. Nanoclay dispersions cut oxygen transmission by 60% at equivalent calipers, paving the way for further down-gauging. Layer-thickness scanners improve profile accuracy and minimize start-up scrap, delivering yield gains that feed directly into bottom-line improvement for participants within the packaging film market.

The Packaging Film Market Report is Segmented by Material Type (Polyethylene, Polypropylene, Polyester, and More), Film Structure (Monolayer, and More), Application (Food and Beverage, Pharmaceutical and Medical, Personal Care and Cosmetics, and More), End-Use Format (Bags and Pouches, Wraps and Lidding Films, Labels and Sleeves, and More ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific sustained 37.00% share of the packaging film market in 2025, underpinned by abundant resin supply, competitive labor, and a vast consumer base. China's GB/T 31268-2024 rule on excessive packaging triggers demand for ultra-light pouches that meet parcel weight caps. Thailand and Indonesia implement harmonized food-contact controls that standardize test protocols and elevate local extrusion sophistication. Indian players such as JPFL Films add 60,000 tpa BOPP capacity to capture domestic and export opportunities. Japan and South Korea champion barrier-coating R&D, while Australia emphasizes post-consumer recycling content.

Europe faces transformative investment cycles to satisfy PPWR recyclability and recycled-content thresholds. Constantia Flexibles' acquisition of Aluflexpack consolidates foil competencies and bolsters Southeast-European footholds. Brands introduce QR-coded disposal instructions to guide consumers and to enhance collection purity. The UK and Germany pilot chemical-recycling drop-offs, driving rPE integration.

North America leverages mature e-commerce networks and rolling policy clarity. PFAS withdrawal deadlines steer converters toward metallized BOPP and AlOx PET, while Canada capitalizes on feedstock cost advantages to remain a major exporter. Mexican facilities supply both domestic snack markets and southern U.S. value chains.

South America records the fastest 7.60% CAGR through 2031, propelled by agricultural exports that require high-barrier films. Investments by OPP FILM COLOMBIA and GDM Plasticos expand BOPP and CPP footprints, while regional funding bodies support eco-design labs. The momentum positions the region as the new growth frontier in the packaging film market.

Middle East and Africa post solid double-digit volume gains fostered by urban retail expansion. Saudi Arabia and the UAE introduce mandates for recyclable plastics that guide procurement choices, and South Africa's established converters serve the broader continent with cost-optimized offerings.

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Jindal Poly Films Ltd

- Cosmo Films Ltd

- Uflex Ltd

- Huhtamaki Oyj

- ProAmpac Holdings

- Novolex Holdings

- AEP Industries

- RKW SE

- Toray Plastics

- Coveris Holdings

- Sigma Plastics Group

- SRF Limited

- Klockner Pentaplast

- Taghleef Industries

- Polyplex Corporation

- Transcontinental Inc.

- Dupont Teijin Films

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom driving demand for lightweight shipping films

- 4.2.2 EU push for mono-material recyclable films

- 4.2.3 Cold-chain packaged food growth in emerging Asia-Pacific

- 4.2.4 Digital printing enabling short-run personalised packs

- 4.2.5 Antimicrobial additive masterbatches for meat films

- 4.2.6 Chemical-recycling feedstock agreements for food-grade rPE

- 4.3 Market Restraints

- 4.3.1 Plastic bans / taxes in NA and Europe

- 4.3.2 Volatile virgin-resin prices

- 4.3.3 Barrier limits of bio-based films

- 4.3.4 Converter downtime from ultra-thin gauges

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Polyethylene

- 5.1.1.1 High-Density Polyethylene (HDPE)

- 5.1.1.2 Low-Density Polyethylene (LDPE)

- 5.1.1.3 Linear Low-Density Polyethylene (LLDPE)

- 5.1.2 Polypropylene

- 5.1.3 Polyester (BOPET)

- 5.1.4 Bioplastics

- 5.1.5 Other Material Types

- 5.1.1 Polyethylene

- 5.2 By Film Structure

- 5.2.1 Monolayer

- 5.2.2 Multilayer (2-3 layers)

- 5.2.3 Barrier multilayer (More than 3 layers)

- 5.3 By Application

- 5.3.1 Food and Beverage

- 5.3.2 Pharmaceutical and Medical

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Consumer Durables and Electronics

- 5.3.5 Industrial and Institutional

- 5.3.6 Agriculture and Horticulture

- 5.3.7 Other Application

- 5.4 By End-Use Format

- 5.4.1 Bags and Pouches

- 5.4.2 Wraps and Lidding Films

- 5.4.3 Labels and Sleeves

- 5.4.4 Blister and Sachets

- 5.4.5 Shrink and Stretch Wrap

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Sealed Air Corporation

- 6.4.3 Mondi plc

- 6.4.4 Jindal Poly Films Ltd

- 6.4.5 Cosmo Films Ltd

- 6.4.6 Uflex Ltd

- 6.4.7 Huhtamaki Oyj

- 6.4.8 ProAmpac Holdings

- 6.4.9 Novolex Holdings

- 6.4.10 AEP Industries

- 6.4.11 RKW SE

- 6.4.12 Toray Plastics

- 6.4.13 Coveris Holdings

- 6.4.14 Sigma Plastics Group

- 6.4.15 SRF Limited

- 6.4.16 Klockner Pentaplast

- 6.4.17 Taghleef Industries

- 6.4.18 Polyplex Corporation

- 6.4.19 Transcontinental Inc.

- 6.4.20 Dupont Teijin Films

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment