|

시장보고서

상품코드

1910625

위식도 역류증 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Gastroesophageal Reflux Disease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

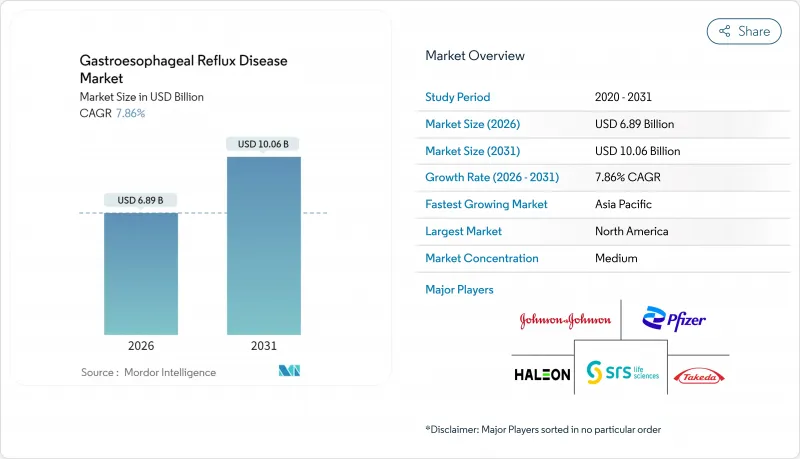

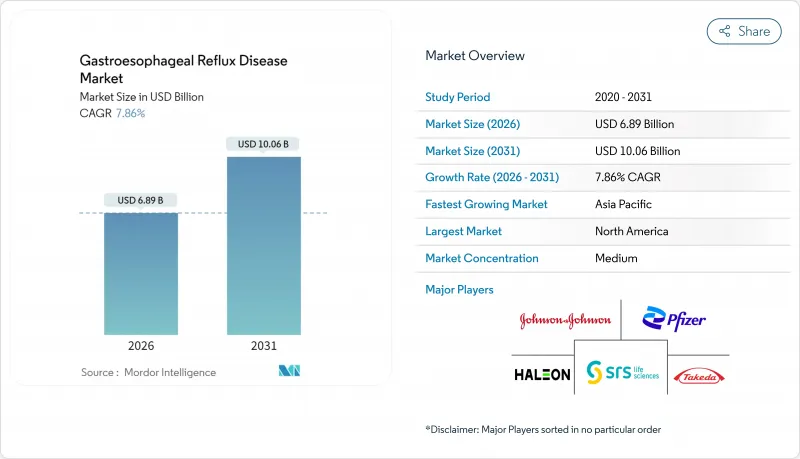

세계의 위식도 역류증(GERD) 시장은 2025년 63억 9,000만 달러에서 2026년 68억 9,000만 달러로 성장하고, 2026년부터 2031년까지 CAGR 7.86%로 성장을 지속하여 100억 6,000만 달러에 달할 것으로 전망됩니다.

2024년 보노프라잔 승인은 30년에 걸친 양성자 펌프 억제제(PPI)의 지배 체제로부터 결정적인 전환을 나타내며, 칼륨 경쟁 산분비 억제제(PCAB)는 현재 난치성 환자에서의 효능 차이를 줄이고 있습니다. 비만 증가, 급속한 인구 고령화, 대사 증후군과 하부 식도 괄약근 기능 장애의 강한 상관 관계가 수요 증가를 지원합니다. 병행하여 실시되는 ESG 주도의 약제 삭감 프로그램은 안전성을 유지하면서 부적절한 PPI 사용을 약 30% 삭감하고 있습니다. 진단 분야에서 AI 탑재 고해상도 압력 측정은 워크플로우 효율을 재정의하고 LINX 자기 괄약근 증강술은 약물 저항성 사례에 효과적인 수술 치료를 제공합니다. 아시아태평양의 견조한 연평균 복합 성장률(CAGR) 9.87%이 성장 스토리를 마무리하고 있으며, 이는 서양화가 진행되는 식생활과 확대하는 헬스케어 인프라에 지지되고 있습니다.

세계의 위식도 역류증(GERD) 시장 동향과 통찰

세계 비만률 상승과 고령화 인구 증가

비만에 의한 복강내압의 상승과 노화에 따른 운동기능의 저하가 함께 GERD의 유병률을 높이고 있습니다. 일본을 비롯한 아시아태평양 국가에서는 고령화와 젊은층의 비만 증가가 동시에 진행되고 있으며, 보험자에게는 만성 질환 케어 패스웨이와 조기 진단 전략의 통합이 요구되고 있습니다. 치료되지 않은 GERD 및 병존 질환 관리로 인한 생산성 손실은 예방적 접근의 경제적 합리성을 더욱 강력하게 합니다.

산분비 억제제의 OTC 자기 치료 문화 상승

자유화된 의료 제도에서 고액의 자기 부담 비용이, 소비자를 시판약의 PPI(양성자 펌프 억제제)나 알긴산염 제제로 향하게 하고 있습니다. 약사 주도의 스크리닝은 중복 치료 및 부적절한 장기 사용의 예방에 효과적임이 입증되었습니다. 전자상거래 플랫폼과 연계된 디지털 증상 추적 앱은 안전 모니터링을 유지하면서 셀프 케어의 범위를 확대하고 있습니다. 디지털 헬스 플랫폼은 개인에 맞는 지도와 증상 추적을 제공하기 위해 OTC 구매와의 연계를 강화하고 있습니다. 이 추세는 건강 관리 비용이 높은 시장에서 가속화되고 있으며, 소비자는 치료 효과를 유지하면서 처방약을 대체하는 비용 효율적인 옵션을 찾고 있습니다.

블록버스터 PPI 및 H2 차단제 특허 만료

판토프라졸, 오메프라졸, 에소메프라졸의 제네릭 의약품은 특허 보호가 끝나면 가격이 압축됩니다. Protonix의 독점권은 2026년에, Dexilant는 2030년에 종료됩니다. 브랜드 기업은 라이프사이클 전략에 대응하고 있지만, 가격에 민감한 지역에서는 제네릭 의약품이 출시 후 수개월 만에 점유율을 얻을 수 있기 때문에 가격 하락세는 더욱 깊어질 것입니다.

부문 분석

상부 내시경 검사는 2025년에도 위식도 역류증(GERD) 시장에서 46.21%의 점유율을 유지해 주류 검사법으로서의 지위를 유지했습니다. 이것은 검사의 보급과 임상의의 숙련도가 높은 배경입니다. 그러나 AI를 활용한 해석 기술은 병변 검출의 효율화와 검사시간의 단축을 실현하고 있으며, 내시경 검사 부문은 소프트웨어 업그레이드 도입을 강요받고 있습니다. 고해상도 압력 검사는 CAGR 9.38%로 가장 급성장하는 진단법으로, 자동 패턴 인식에 의한 판독 시간 단축이 견인하고 있습니다. 캡슐 내시경 기술은 전통적인 내시경 검사가 어려운 환자에게 비 침습적 점막 관찰을 제공합니다.

임상 알고리즘의 개별화가 새로운 표준이 되어, 머신러닝이 증상군에 근거한 최적의 진단 경로를 추천하는 것으로, 중복 검사가 삭감되고 있습니다. SEA-HRM은 진정 곤란 환자에서 완전한 이행률을 달성하고 치료 실패를 진단 성공으로 전환시킬 가능성이 높습니다. MNBI 기준치는 지역 차이를 인정하고, 베트남 코호트에서는 1,500옴의 임계값을 나타내며, 집단 고유의 컷오프 값 설정의 중요성을 강조하고 있습니다.

2025년 위식도 역류증 시장 규모의 67.84%를 양성자 펌프 억제제가 차지해, CAGR 8.31%로 확대하고 있지만, 이 수치는 선진국 시장에서의 PCAB(양성자 펌프 억제제 대체 요법) 조기 카니발리제이션을 은폐하고 있습니다. H2 수용체 길항제는 즉각적인 틈새 시장에서 살아남으며, 제산제와 알긴산염 제제는 간헐적 증상에 대한 효능을 유지합니다. 보노프라잔의 발매에 의해 PCAB 파이프라인이 확대되어, 약동학이 유망한 리나플라잔 글루레이트가 미란성 GERD 치료제으로서 개발이 진행되고 있습니다.

PCAB는 PPI보다 변동이 적고 보다 안정된 위내 pH를 제공합니다. 알긴산 장벽과 PCAB를 결합한 병용 요법이 여러 산 생산 경로를 동시에 표적화하기 위해 연구 중입니다. 그러나 2032년 이후의 독점기간 단축에 따라 후발 의약품의 위협이 다가오고 있습니다.

지역별 분석

북미는 2025년에도 위식도 역류증 시장의 35.12%를 차지했습니다. 이것은 PCAB의 조기 도입, 진단 수단의 보급, 고가격 전략의 혜택 때문입니다. 임상 가이드라인에서는 이미 PPI 저항성 미란성 식도염에 대한 보노플라잔 사용이 통합되어 있어 치료 전환에 선행하고 있습니다. LINX를 비롯한 저침습 디바이스의 보험 적용이 수입 수입을 더욱 강화하고 있습니다.

유럽에서는 체계적인 원격 의료 프로그램과 ESG 지향 약물 체중 감량 프로토콜을 배경으로 견조한 성장을 유지하고 있습니다. 독일은 원격 고해상도 식도 내압 측정의 해석을 지원하는 상환 모델을 통해 디지털 도입을 선도하고 있습니다. EU 규제 당국은 만성 PPI 사용에 대한 FDA의 우려를 공유하고 H2 길항제와 알긴산염을 포함한 단계적 감약 접근법을 처방 의사에게 촉구합니다. 그러나 시장 성숙에 따라 기존 PPI의 판매 수량 성장은 둔화 경향이 있습니다.

아시아태평양은 가처분 소득 증가와 지방과 당분을 많이 포함하는 도시 지역의 식생활 변화에 견인되어 9.42%의 연평균 복합 성장률(CAGR)로 가장 급성장하고 있는 지역입니다. 중국의 현지 생산 거점은 API의 부족을 완화하고 인도의 PLI 체계는 중국의 중간체에 대한 70%의 의존도를 축소하고 있습니다. 일본에서는 노인이면서 기술에 정통한 인구가 원격의료 도입을 촉진하고 한국에서는 스마트폰의 보급률이 높아 디지털 어드히어런스 프로그램을 지원하고 있습니다. 진단 기준의 조정과 낮은 바렛 식도의 유병률은 지역마다 다른 관리의 필요성을 강조합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 비만 및 고령화 인구 증가

- 산분비 억제제에 있어서 OTC 자가치료 문화 확대

- 칼륨 경쟁형 산분비 억제제(PCAB)의 급속한 보급

- 자기식 괄약근 보조 장치(LINX)의 도입 확대

- AI 탑재 고해상도 압력 측정에 의한 진단 정밀도 향상

- PPI 과잉처방을 억제하기 위한 기업의 ESG 추진

- 시장 성장 억제요인

- 블록버스터급 양성자 펌프 억제제(PPI) 및 H2 차단제의 특허 만료

- 만성 PPI 사용에 대한 FDA 안전 경고 증가

- 신규 내시경 치료의 보험자에 의한 도입의 지연

- 주요 원약(오메프라졸, 에소메프라졸)의 공급망 변동성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(달러)

- 진단별

- 상부 내시경 검사

- 외래 pH 및 임피던스 모니터링

- 식도 및 고분해능 신경계

- 캡슐 내시경 검사

- 기타

- 약제 클래스별

- 양성자 펌프 억제제(PPI)

- H2 수용체 길항제

- 칼륨 억제형 산분비 억제제(PCABs)

- 제산제 및 알긴산염

- 소화관 운동 촉진제 및 기타

- 최종 사용자별

- 병원

- 전문의료센터 및 클리닉

- 재택치료 환경

- 유통 채널별

- 병원 약국

- 소매 약국 및 드럭 스토어

- 온라인 약국

- 기타 유통 채널

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AstraZeneca

- Takeda Pharmaceutical Company Limited

- Haleon

- Johnson & Johnson Services, Inc.

- Pfizer Inc.

- Medtronic

- Olympus Corporation

- Reckitt Benckiser

- Teva Pharmaceutical Industries Ltd.

- Zydus Lifesciences

- Glenmark

- Aurobindo Pharma

- Eisai Co.

- Dr Reddy's Laboratories

- Hetero Drugs Limited(Camber Pharmaceuticals, Inc.)

- Perrigo Company

- Boston Scientific

- The Procter & Gamble Company

- Torax Medical

- SRS Life Sciences

- Implantica AG

제7장 시장 기회와 미래 전망

SHW 26.01.26The Gastroesophageal Reflux Disease market is expected to grow from USD 6.39 billion in 2025 to USD 6.89 billion in 2026 and is forecast to reach USD 10.06 billion by 2031 at 7.86% CAGR over 2026-2031.

Vonoprazan's 2024 approval signaled a decisive break from the 30-year dominance of proton pump inhibitors, and potassium-competitive acid blockers (PCABs) are now closing efficacy gaps for refractory patients. Escalating obesity, rapid population aging, and a strong correlation between metabolic syndrome and lower esophageal sphincter dysfunction sustain demand growth. Parallel ESG-driven deprescribing programs are trimming inappropriate PPI use by almost 30% while preserving safety outcomes. On the diagnostic front, AI-enabled high-resolution manometry is redefining workflow efficiency, and LINX magnetic sphincter augmentation offers effective surgical relief for medication-refractory cases. Asia-Pacific's robust 9.87% CAGR rounds out the growth narrative, underpinned by westernizing diets and expanding healthcare infrastructure.

Global Gastroesophageal Reflux Disease Market Trends and Insights

Escalating Global Obesity and Aging Population

Obesity-driven intra-abdominal pressure and age-related motility decline combine to raise GERD prevalence. Asia-Pacific countries such as Japan now confront simultaneous aging and a rise in adolescent obesity, compelling payers to integrate chronic care pathways and early diagnosis strategies. Productivity losses from untreated GERD and comorbidity management strengthen the economic rationale for preventive approaches.

Rising OTC Self-Medication Culture for Acid-Suppressants

High out-of-pocket costs in liberalized health systems are pushing consumers toward OTC PPIs and alginates. Pharmacist-led screening has proven effective in preventing duplicate therapy and inappropriate chronic use. Digital symptom-tracking apps tethered to e-commerce platforms are extending self-care while preserving safety oversight. Digital health platforms increasingly integrate with OTC purchases to provide personalized guidance and symptom tracking. The trend accelerates in markets with high healthcare costs, where consumers seek cost-effective alternatives to prescription medications while maintaining treatment efficacy.

Patent Cliffs for Blockbuster PPIs and H2 Blockers

Generic pantoprazole, omeprazole, and esomeprazole have compressed prices as patent shields fall; Protonix exclusivity ends in 2026 and Dexilant in 2030. Branded firms answer with lifecycle tactics, but erosion will deepen in price-sensitive regions where generics can grab share within months of launch.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Potassium-Competitive Acid Blockers

- Growing Adoption of Magnetic Sphincter Augmentation (LINX)

- Increasing FDA Safety Alerts on Chronic PPI Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Upper endoscopy continued to dominate with a 46.21% share of the Gastroesophageal Reflux Disease market in 2025, driven by widespread availability and clinician familiarity. Yet AI-powered analysis is streamlining lesion detection and reducing procedure time, forcing endoscopy units to integrate software upgrades. High-resolution manometry is the fastest-growing diagnostic at 9.38% CAGR, fueled by automated pattern recognition that cuts interpretation times. Capsule techniques deliver non-invasive mucosal views for patients unable to tolerate conventional scopes.

Clinical algorithm personalization is the new norm; machine learning now recommends the optimal diagnostic pathway based on symptom clusters, reducing redundant testing. SEA-HRM achieved perfect completion rates in sedation-challenged patients and is likely to convert procedural failures into diagnostic successes. MNBI reference values display regional variation-Vietnamese cohorts show a 1,500-Ohm threshold, stressing the importance of population-specific cut-offs.

Proton pump inhibitors still represent 67.84% of the Gastroesophageal Reflux Disease market size in 2025 and grow at 8.31% CAGR, but the metric disguises early PCAB cannibalization in developed markets. H2 antagonists hang on in rapid-relief niches, while antacids and alginates retain relevance for intermittent symptoms. Vonoprazan's launch has sparked wider PCAB pipelines; linaprazan glurate is advancing for erosive GERD with promising pharmacokinetics.

PCABs provide more stable intragastric pH with less variability than PPIs. Combination regimens pairing alginate barriers with PCABs are under investigation to target multiple acid pathways simultaneously. Generic threats, however, loom as exclusivity windows narrow post-2032.

The Gastroesophageal Reflux Disease Market Report Segments the Industry Into by Diagnosis (Upper Endoscopy, and More), Drug Class (Proton Pump Inhibitors (PPIs), H2-Receptor Antagonists, and More), End User (Hospitals, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America continued to command 35.12% of the Gastroesophageal Reflux Disease market in 2025, benefiting from early PCAB adoption, widespread diagnostic availability, and premium pricing. Clinical guidelines have already integrated vonoprazan for PPI-refractory erosive esophagitis, giving the region a head start in the therapeutic transition. Insurer coverage for LINX and other minimally invasive devices further strengthens procedural revenues.

Europe maintains solid growth on back of structured telehealth programs and ESG-oriented deprescribing protocols. Germany leads digital adoption with reimbursement models supporting remote high-resolution manometry interpretation. EU regulators echo FDA concerns on chronic PPI use, nudging prescribers toward step-down approaches that include H2 antagonists and alginates. Market maturity, however, tempers volume growth for legacy PPIs.

Asia-Pacific is the fastest-growing geography at 9.42% CAGR, driven by rising disposable incomes and urban dietary shifts rich in fat and sugar. China's local manufacturing base cushions API shortages, while India's PLI scheme is narrowing its 70% dependency on Chinese intermediates. Japan's aging yet tech-savvy population fuels telemedicine adoption, whereas South Korea's high smartphone penetration supports digital adherence programs. Tailored diagnostic thresholds and lower Barrett's prevalence underscore the need for region-specific management.

- AstraZeneca

- Takeda Pharmaceuticals

- Haleon

- Johnson & Johnson

- Pfizer

- Medtronic

- Olympus

- Reckitt Benckiser Group

- Teva Pharmaceutical Industries

- Zydus Lifesciences

- Glenmark Pharmaceuticals

- Aurobindo Pharma

- Eisai

- Dr Reddy's Laboratories

- Hetero Drugs Limited (Camber Pharmaceuticals, Inc.)

- Perrigo Company

- Boston Scientific

- Procter & Gamble

- Torax Medical

- SRS Life Sciences

- Implantica AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Obesity and Ageing Population

- 4.2.2 Rising OTC Self-Medication Culture for Acid-Suppressants

- 4.2.3 Rapid Uptake of Potassium-Competitive Acid Blockers (PCABs)

- 4.2.4 Growing Adoption of Magnetic Sphincter Augmentation (LINX)

- 4.2.5 AI-Enabled High-Resolution Manometry Improving Diagnosis

- 4.2.6 Corporate ESG Push to Curb PPI Over-Prescription

- 4.3 Market Restraints

- 4.3.1 Patent Cliffs for Blockbuster Proton Pump Inhibitors (PPIs) and H2 Blockers

- 4.3.2 Increasing FDA Safety Alerts on Chronic PPI Use

- 4.3.3 Slow Payer Adoption of Novel Endoscopic Therapies

- 4.3.4 Supply-Chain Volatility in Key API (Omeprazole, Esomeprazole)

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Diagnosis

- 5.1.1 Upper Endoscopy

- 5.1.2 Ambulatory pH & Impedance Monitoring

- 5.1.3 Esophageal & High-Resolution Manometry

- 5.1.4 Capsule Endoscopy

- 5.1.5 Others

- 5.2 By Drug Class

- 5.2.1 Proton Pump Inhibitors (PPIs)

- 5.2.2 H2-Receptor Antagonists

- 5.2.3 Potassium-Competitive Acid Blockers (PCABs)

- 5.2.4 Antacids and Alginates

- 5.2.5 Prokinetics and Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Speciality Centers and Clinics

- 5.3.3 Home-Care Settings

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies & Drug Stores

- 5.4.3 Online Pharmacies

- 5.4.4 Other Distribution Channel

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AstraZeneca

- 6.3.2 Takeda Pharmaceutical Company Limited

- 6.3.3 Haleon

- 6.3.4 Johnson & Johnson Services, Inc.

- 6.3.5 Pfizer Inc.

- 6.3.6 Medtronic

- 6.3.7 Olympus Corporation

- 6.3.8 Reckitt Benckiser

- 6.3.9 Teva Pharmaceutical Industries Ltd.

- 6.3.10 Zydus Lifesciences

- 6.3.11 Glenmark

- 6.3.12 Aurobindo Pharma

- 6.3.13 Eisai Co.

- 6.3.14 Dr Reddy's Laboratories

- 6.3.15 Hetero Drugs Limited (Camber Pharmaceuticals, Inc.)

- 6.3.16 Perrigo Company

- 6.3.17 Boston Scientific

- 6.3.18 The Procter & Gamble Company

- 6.3.19 Torax Medical

- 6.3.20 SRS Life Sciences

- 6.3.21 Implantica AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment